|

시장보고서

상품코드

1684113

척추 로봇 수술 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Spine Robotic Surgery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

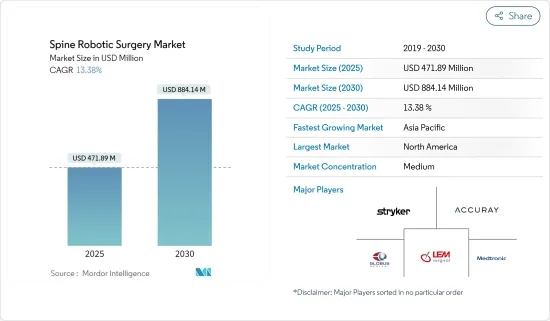

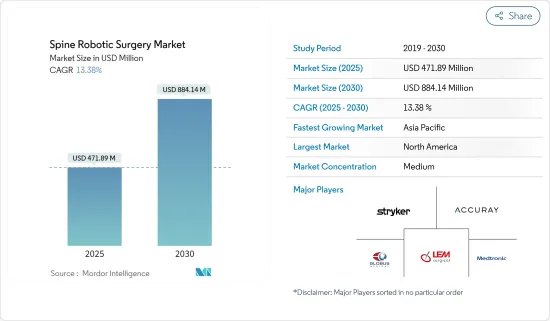

척추 로봇 수술 시장 규모는 2025년에 4억 7,189만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 13.38%로 성장할 전망이며, 2030년에는 8억 8,414만 달러에 달할 것으로 예측됩니다.

척추 로봇 수술 시장은 기술의 진보, 신규 진입, 저침습 수술에 대한 기호 증가 등의 요인 중에서 견조한 성장 기회가 전망되고 있습니다. 또한 척추질환 부담이 증가함에 따라 조사 기간 동안 시장 확대가 더욱 가속될 것으로 예상됩니다.

로봇 공학의 기술적 진보 증가는 조사 기간 동안 시장 성장을 가속할 것으로 예상되는 주요 요인 중 하나입니다. 척추 수술에서 지원 기술의 상당한 진보는 기구 장착 시 정밀도, 정확성 및 신뢰성을 높이기 위해 이루어져 왔습니다. 척추 수술은 혈관과 신경계의 합병증을 피하고 융합을 위한 고정을 극대화하기 위해 정확한 스크류 배치가 중요합니다.

로봇 공학의 응용으로 스크류 유치의 정확성을 포함한 전체 척추 수술 절차를 크게 개선하여 더 나은 치료 성과를 이끌어 냈습니다. 따라서 이러한 진보는 조사 기간 동안 시장 성장을 밀어올릴 것으로 예상됩니다.

게다가, 척추 로봇에 있어서 신흥 기업의 상승 및 척추 로봇의 변화를 위한 몇 가지 전략적 인수가 시장 성장을 더욱 끌어올릴 것으로 예상됩니다. 예를 들어 2023년 4월 Alphatec Holdings Inc.는 비상장 의료 기술인 Accelus Inc.에서 REMI Robotic Navigation System을 5,500만 달러에 인수했습니다. REMI(Robotic-Enabled Minimally Invasive) 시스템은 3D 이미지 스캔 또는 2D 투시 환자 이미지를 활용하여 척추 수술에 내비게이션과 로봇을 통합하는 수술 중 플랫폼입니다. 따라서 척추 외과 로봇을 변화시키기 위한 전략적 인수는 조사 기간 동안 시장 성장을 가속할 것으로 예측됩니다.

또한, 척추 수술에서 로봇 척추 플랫폼과 관련된 다른 혜택도 조사 기간 동안 시장 성장을 가속화할 것으로 예상되는 요인입니다. 예를 들어, 중국 국가 자연 과학 기금(National Natural Science Foundation of China)의 보조금에 의해 지원되고 EFORT Open Reviews에 게재된 2023년 11월의 연구에 따르면, 종래 기술의 페디클 스크류의 오배치율은 요추와 흉추에서 각각 30%와 55%의 성공률을 보였습니다. 이와 같이 로봇 플랫폼은 정밀도가 높고 장점이 많기 때문에 예측 기간 동안 보급이 진행될 것으로 예상됩니다.

게다가, 시장 진출기업이 사업 강화를 위해 하고 있는 몇몇 전략적 이니셔티브는 시장 성장을 가속화할 것으로 예상됩니다. 예를 들어, 2023년 10월, Spine Wave와 eCential Robotics는 새로운 로봇 기반 척추 수술 플랫폼을 개발, 시장 개척 및 상업화하기 위한 협력 계약에 서명했습니다. 따라서 이러한 개발은 조사 기간 동안 시장 성장을 뒷받침할 것으로 예상됩니다.

이와 같이 기술 진보, 저침습 수술에 대한 수요 증가, 시장 진출기업에 의한 몇 가지 전략적 이니셔티브 등 위의 요인은 예측 기간 동안 시장 성장을 밀어올릴 것으로 예상됩니다. 하지만 신흥국에서의 높은 수술 비용 및 보급 지연이 조사기간 동안 산업 확대를 방해할 것으로 예상됩니다.

척추 로봇 수술 시장 동향

시스템 부문은 예측 기간 동안 기하급수적인 성장이 예상됩니다.

시스템 부문에는 수술 로봇 및 내비게이션 시스템이 포함됩니다. 로봇 기술의 진보 및 주요 시장 진출기업의 노력 등 요인이 예측 기간 동안 시장 성장을 증가시킬 것으로 예상됩니다.

또한, 수술 로봇 및 네비게이션 시스템과 관련된 기타 혜택과 헬스케어 시설 전체에 대한 설치가 증가하고 있다는 것은 업계 확대를 가속할 것으로 예상되는 중요한 요소 중 일부입니다. 예를 들어, 2023년 11월, Mercy Hospital Northwest Arkansas는 척추 수술을 지원하고 인간 오류의 가능성을 줄이는 Mazor X 로봇의 추가를 발표했습니다. 외과의사는 로봇이 수술 전에 나사 배치를 계획하는 데도 도움이 되며 수술실에서 워크플로우를 크게 개선할 수 있을 것으로 기대합니다.

게다가 2023년 8월, 앨라배마 대학 버밍엄교(UAB)는 기구의 설치나 척추 변성 질환의 치료를 위해서, 글로버스 메디컬사의 ExcelsiusGPS 척추 로봇을 도입했다고 발표했습니다. UAB는 또한 2023년 초에 로봇 수술 건수가 20,000건을 돌파했다고 주장합니다. 이러한 동향은 척추 수술에서 로봇의 사용이 증가하고 있음을 나타내며, 부문 성장의 원동력이 될 것으로 예상됩니다.

또한, 척추 로봇 내비게이션 시스템 발전 및 자금 조달 기회 증가는 조사 기간 동안 부문의 섭취를 더욱 가속시킬 것으로 예상됩니다. 예를 들어, 2024년 4월, SpinEM Robotics는 척추 수술의 혁신에 주력하는 Spineart로부터 1,100만 달러의 전략적 투자를 받았습니다. 이 전략적 파트너십은 전자의 고급 네비게이션과 로봇 지원 기술 및 후자의 수술 솔루션의 전문 지식이 융합될 것으로 기대됩니다. 이러한 개발로 인해 예측 기간 동안 이 분야 시장 확대가 가속될 것으로 보입니다.

이와 같이 로봇 기술의 진보 및 주요 시장 기업의 대처 등 위의 요인은 예측 기간 동안 시장 성장을 증가시킬 것으로 예상됩니다.

북미는 예측 기간 동안 척추 로봇 수술 시장의 건전한 성장을 보여줄 것으로 예측됩니다.

북미는 척수 손상과 변형의 유병률 증가, 기술 진보 증가, 저침습 수술에 대한 수요 증가, 업계 참가자들의 몇 가지 전략적 이니셔티브 중에서 유리한 성장 기회가 될 것으로 기대됩니다.

퇴행성 질환, 척추 변형, 척수 손상, 척추 외상과 같은 척추 질환의 유병률은 북미에서 상승하는 경향이 있습니다. 이러한 이유로 이러한 증상을 효과적으로 치료하기 위한 고급 수술 개입에 대한 수요가 증가하고 있습니다. 예를 들어, 2023년 5월 Spinal Cord, Inc.의 보고서에 따르면, 미국에서는 매년 약 18,000건의 척수 손상이 새롭게 발생하고 있으며 연간 발생률은 100만 명당 54건입니다.

이와 같이 이 나라의 척수손상 부담이 우려할 정도로 증가하고 있기 때문에 이러한 상태를 관리하기 위한 혁신적인 외과적 개입에 대한 수요가 촉진될 것으로 예상되며, 그 결과 조사 기간 중 시장 성장이 가속될 것으로 예측됩니다.

또한 척추 외상 및 기타 기형 관리에서 척추 로봇 수술의 역할이 입증되었기 때문에 조사 기간 동안 시장 성장이 더욱 가속될 것으로 예측됩니다. 예를 들어, 2023년 9월 North American Spine Society Journal이 발표한 논문에 따르면, 척추 수술의 로봇 지원은 외상성 골절 환자에게 안전하게 수행될 수 있으며, 로봇 지원에 의한 기구 고정은 이러한 척추 외상에 도움이 됩니다. 따라서 척추 수술에서 로봇 플랫폼의 역할이 입증되었으며, 향후 몇 년동안 업계의 성장이 가속화 될 것으로 예상됩니다.

또한, 저침습 수술(MIS)에 대한 수요가 증가하고 있으며, 로봇 척추 수술의 용도가 증가하고 있습니다. 예를 들어, 2022년 11월에 Canadian Journal for Surgery가 발표한 보고서에 따르면, 저침습 수술은 입원 기간, 통증, 수술 부위 감염 등의 합병증을 감소시킵니다. 따라서 환자는 점점 더 작은 절개, 더 빠른 회복 시간 및 통증 완화를 제공하는 수술을 요구하고 있습니다. 따라서 저침습 수술의 보급은 조사 기간 동안 시장 성장을 가속화할 것으로 예상됩니다.

또한 주요 시장 진출 기업의 최근 동향은 조사 기간 동안 시장 성장을 더욱 가속화할 것으로 예상됩니다. 예를 들어 2022년 9월 Stryker는 미국에서 척추용 Q Guidance System을 출시했습니다. 새로 출시된 시스템은 척추 수술을 위한 견고한 네비게이션과 계획 기능을 갖추고 있습니다. 따라서 이러한 개발은 조사 기간 동안 시장 성장을 뒷받침할 것으로 예상됩니다.

이와 같이 척추질환의 큰 부담, 기술의 진보, 저침습 수술 수요 증가, 시장 진출기업에 의한 몇 가지 전략적 이니셔티브 등, 상기 요인은 조사 기간에 걸쳐 이 지역 시장 성장을 가속할 것으로 예상됩니다.

척추 로봇 수술 산업 개요

척추 로봇 수술 시장의 경쟁은 중간 정도이며 여러 대형 기업들이 진입하고 있습니다. 이러한 기업들은 전략적 제휴를 수립하고 세계 시장에서 사업을 전개하는 다른 기업과 협력하고 있습니다. 따라서 시장 진출기업에 의한 이러한 전략적 이니셔티브는 조사 기간 동안 업계 시장 성장을 가속할 것으로 예측됩니다. 이 시장에서 사업을 전개하는 주요 기업으로는 Stryker, Accuray Incorporated, Medtronic, Lem Surgical Ag, Zimmer Biomet 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 기술적 진보의 고조 및 신규 시장 기업 진입

- 저침습 수술에 대한 기호의 고조

- 시장 성장 억제요인

- 엄격한 규제 프로세스 및 장치의 높은 비용

- 업계의 매력-Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 제품 유형별

- 시스템

- 수술 로봇

- 네비게이션 시스템

- 소모품 및 액세서리

- 소프트웨어 및 서비스

- 시스템

- 용도별

- 융합 수술

- 비융합 수술

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Stryker

- Accuray Incorporated

- Medtronic

- Lem Surgical Ag

- Brainlab Ag

- Globus Medical, Inc.

- Zimmer Biomet

- Curexo, Inc

- Point Robotics Medtech Inc.

- Beijing Tinavi Medical Technologies Co., Ltd.

- Nanjing Perlove Medical Equipment Co., Ltd.

제7장 시장 기회 및 향후 동향

AJY 25.04.17The Spine Robotic Surgery Market size is estimated at USD 471.89 million in 2025, and is expected to reach USD 884.14 million by 2030, at a CAGR of 13.38% during the forecast period (2025-2030).

The spine robotic surgery market is expected to witness robust growth opportunities amid factors such as rising technological advancements, the entry of new market players, and the rising preference for minimally invasive surgeries. In addition, the growing burden of spinal disorders is further expected to accelerate market expansion over the study period.

The increasing technological advancements in robotics are one of the major factors expected to foster market growth over the study period. Significant advancements in assistive technology in spine surgery have been made to enhance accuracy, precision, and reliability during instrumentation. Accurate screw placement is critical in spinal surgery to avoid vascular or neurologic complications and to maximize fixation for fusion.

The application of robotics has significantly improved the entire procedure of spinal surgery, including accuracy of screw placements, leading to better outcomes. Thus, such advancements are expected to boost market growth over the study period.

Moreover, the rise of spine robotic start-ups and several strategic acquisitions to transform spinal robotics are further expected to boost market growth. For instance, in April 2023, Alphatec Holdings Inc. acquired the REMI Robotic Navigation System from the privately held medtech Accelus Inc. for USD 55 million. REMI (Robotic-Enabled Minimally Invasive) System is an intra-operative platform that integrates navigation and robotics into spine procedures by utilizing either a 3D imaging scan or 2D fluoroscopic patient images. Thus, such strategic acquisitions to transform spine surgical robotics are projected to facilitate market growth over the study period.

In addition, several benefits associated with robotic spine platforms in spine surgeries are another factor projected to accelerate market growth over the study period. For instance, as per the November 2023 study supported by a grant from the National Natural Science Foundation of China and published in EFORT Open Reviews, the pedicle screw misplacement rates of conventional techniques are 30% and 55% in the lumbar and thoracic spines, respectively, while robot-assisted pedicle screw placement reported a success rate of 91.5% to 94.4%. Thus, the greater precision and benefits associated with robotic platforms are expected to bolster their adoption over the forecast period.

Furthermore, several strategic initiatives undertaken by industry participants to strengthen their business avenues are projected to accelerate market growth. For instance, in October 2023, Spine Wave and eCential Robotics signed a collaboration agreement to develop, market, and commercialize novel robotics-based spine surgery platforms. Thus, such developments are expected to boost market growth over the study period.

Thus, the above-mentioned factors, like technological advancements, growing demand for minimally invasive surgeries, and several strategic initiatives undertaken by market players, are expected to boost market growth over the forecast period. However, the high cost of procedures and slow uptake in in emerging economies is projected to hinder industry expansion over the study period.

Spine Robotic Surgery Market Trends

System Segment is Expected to Register an Exponential Growth Over the Forecast Period

The system segment includes surgical robots and navigation systems. Factors such as advancements in robotic technology and initiatives undertaken by key market players are expected to increase market growth over the forecast period.

In addition, several benefits associated with surgical robots and navigation systems and their increasing installation across healthcare facilities are some of the significant factors expected to accelerate industry expansion. For instance, in November 2023, Mercy Hospital Northwest Arkansas announced the addition of a Mazor X robot to assist with spinal surgeries and reduce the chances of human error. The surgeons anticipate that the robot can also aid with planning the placement of the screws before surgery and can create a much better workflow in the operating room.

Moreover, in August 2023, the University of Alabama at Birmingham (UAB) announced the addition of an ExcelsiusGPS spine robot from Globus Medical for instrument placement and treating degenerative conditions in the spine. UAB also claimed that the institution surpassed 20,000 robotic surgeries in early 2023. Such trends indicate the rising usage of robots for spine surgery and are also anticipated to drive segmental growth.

Furthermore, advancements in spinal robotic navigation systems and increasing funding opportunities are further expected to accelerate segment uptake over the study period. For instance, in April 2024, SpinEM Robotics secured a USD 11 million strategic investment from Spineart, which focuses on spine surgery innovation. This strategic partnership is expected to combine the former's advanced navigation and robotic assistance technology with the latter's expertise in surgical solutions. Thus, such developments are poised to accelerate segment uptake over the forecast period.

Thus, the above-mentioned factors, such as advancements in robotic technology and initiatives undertaken by key market players, are expected to increase market growth over the forecast period.

North America is Projected to Witness Healthy Growth in The Spine Robotic Surgery Market During the Forecast Period

North America is expected to witness lucrative growth opportunities amid a rise in the prevalence of spinal cord injuries and deformities, the increase in technological advancements, the growing demand for minimally invasive surgery procedures, and several strategic initiatives undertaken by industry participants.

The prevalence of spine disorders, such as degenerative conditions, spinal deformities, spinal cord injuries, and spinal trauma, is on the rise in the North American region. This has led to a growing demand for advanced surgical interventions to treat these conditions effectively. For instance, according to a May 2023 report of Spinal Cord, Inc., around 18,000 new spinal cord injuries occur each year in the United States, with an annual incidence rate of 54 per 1 million.

Thus, such an alarming increase in the burden of spinal cord injuries in the country is expected to foster demand for innovative surgical interventions to manage such conditions, which, in turn, is projected to accelerate market growth over the study period.

In addition, the proven role of spinal robotic surgeries in the management of spinal trauma and other deformities is further projected to accelerate market growth over the study period. For instance, according to an article published by the North American Spine Society Journal in September 2023, robotic assistance in spinal surgery can be safely implemented in patients with traumatic fractures, and robot-assisted instrumented fusion can be helpful in such spinal traumas. Thus, the proven role of robotic platforms in spine surgeries is projected to accelerate industry growth over the coming years.

Furthermore, there is a growing demand for Minimally Invasive Surgery (MIS), leading to a rise in the application of robotic spinal surgeries. For instance, according to a report published by the Canadian Journal for Surgery in November 2022, minimally invasive surgery decreases length of stay, pain, and complications such as surgical site infection. Therefore, patients increasingly seek procedures offering smaller incisions, faster recovery times, and reduced pain. Thus, the increasing uptake of minimally invasive surgical procedures is projected to accelerate market growth over the study period.

Also, several recent developments undertaken by key industry participants are further expected to accelerate market growth over the study period. For instance, In September 2022, Stryker launched the Q Guidance System for spine applications in the United States. The newly launched system has robust navigation and planning capabilities for spinal surgeries. Thus, such developments are expected to boost market growth over the study period.

Thus, the above-mentioned factors, like the significant burden of spinal disorders, growing technology advancements, increasing demand for minimally invasive procedures, and several strategic initiatives undertaken by market participants, are expected to foster the region's market growth over the study period.

Spine Robotic Surgery Industry Overview

The spine robotic surgery market is moderately competitive and consists of several major players. They are engaged in establishing a strategic alliance and collaborating with other companies operating in this global market. Thus, such strategic initiatives undertaken by market participants are projected to foster the industry's market growth over the study period. Some of the key players operating in the market are, Stryker, Accuray Incorporated, Medtronic, Lem Surgical Ag, Zimmer Biomet among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Technological Advancements And Entry Of New Market Players

- 4.2.2 Rising Preference For Minimally Invasive Surgeries

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Processes And High Cost Of Devices

- 4.4 Industry Attractiveness- Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 System

- 5.1.1.1 Surgical Robot

- 5.1.1.2 Navigation System

- 5.1.2 Consumables And Accessories

- 5.1.3 Software And Services

- 5.1.1 System

- 5.2 By Application

- 5.2.1 Fusion Surgery

- 5.2.2 Non-fusion Surgery

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Stryker

- 6.1.2 Accuray Incorporated

- 6.1.3 Medtronic

- 6.1.4 Lem Surgical Ag

- 6.1.5 Brainlab Ag

- 6.1.6 Globus Medical, Inc.

- 6.1.7 Zimmer Biomet

- 6.1.8 Curexo, Inc

- 6.1.9 Point Robotics Medtech Inc.

- 6.1.10 Beijing Tinavi Medical Technologies Co., Ltd.

- 6.1.11 Nanjing Perlove Medical Equipment Co., Ltd.