|

시장보고서

상품코드

1685777

유럽의 종자 처리 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Europe Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

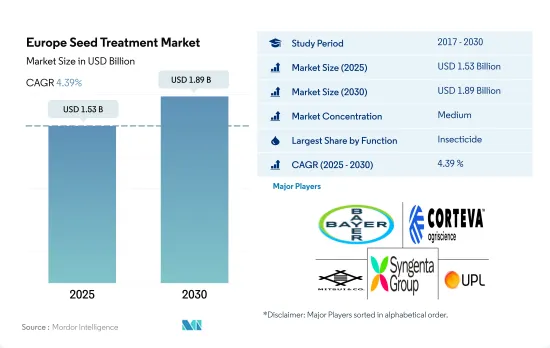

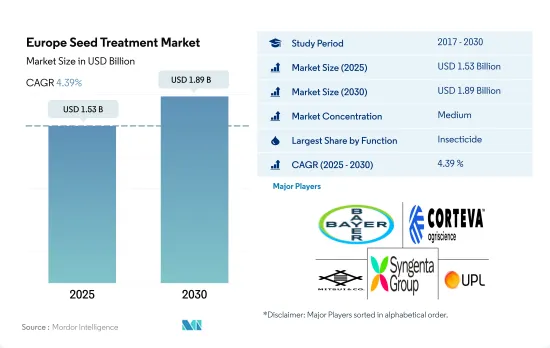

유럽의 종자 처리 시장 규모는 2025년 15억 3,000만 달러로 추정되고, 2030년에는 18억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 4.39%로 성장헐 것으로 예상됩니다.

종자는 토양 매개 박테리아의 영향을 받기 쉽기 때문에 살균제가 유럽 종자 처리 시장을 독점했습니다.

- 종자 처리란, 살균제, 살충제, 또는 양쪽 모두를 조합하여 종자에 살포함으로써, 종자를 소독하고, 종자를 매개하는 병원체나 토양을 매개하는 병원체로부터 종자를 보호하는 것을 가리킵니다. 종자 처리는 발아, 묘목, 균주의 활력, 묘목, 총 수율을 향상시켜, 작물이 유전적 잠재 능력을 최대한으로 발휘할 수 있도록 합니다.

- 파종 후 첫 4-6주간은 묘목이 발아되어 체질이 형성되기 때문에 새로운 식물의 일생에 있어서 중요한 시기입니다.

- 살균제는 2024년 유럽 씨앗 처리 시장의 46.9%를 차지하고 있습니다. 유럽에서 발견되는 가장 흔한 질병을 유발하는 곰팡이균에는 푸사륨속, 셉토리아속, 피레노포라속, 우스틸라고속, 틸레티아속, 보트리티스속이 있습니다. 비슷하게, 리족토니아 솔라니, 파이토프로라속, 피시움속, 버티실륨속, 고무버섯속이 유럽의 가장 흔한 토양 전염성 진균입니다.

- 유럽의 종자 처리 시장은 곡물 작물이 지배적이며, 2024년 시장 점유율의 59.8%를 차지합니다. 종자 처리는 이러한 병원체로부터 종자를 보호하고 발아나 초기 성장 단계에서의 감염을 막는데 도움이 됩니다.

- 유럽의 종자 처리 보증 체계(ESTA)와 같은 방식은 종자 처리와 그 결과 얻은 치료된 종자가 입법기관이나 업계에 의해 정의된 요건을 충족하는 것을 보증하는 품질 보증 시스템이며, 시장의 성장을 뒷받침하고 있습니다.

유럽 종자 처리 보증 제도와 같은 제도가 종자 처리 시장을 견인

- 유럽에서 한해살이 작물은 겨울 작물과 봄 작물, 여름 작물로 세분화됩니다. 겨울 작물은 가을에 파종되어 다음 해의 여름에 수확됩니다. 봄 작물과 여름 작물은 같은 해에 씨를 뿌리고 수확합니다, 밀, 유채, 호밀, 라이밀이 일반적인 겨울 작물이고, 옥수수, 해바라기, 쌀, 콩, 감자, 사탕무는 여름 작물입니다. 보리는 겨울용과 봄용이 모두 있습니다.

- 유럽에서의 종자 처리제의 소비는 곡물이 압도적으로 많아, 시장 매출의 약 59.8%를 차지해 2024년에는 약 8억 7,800만 달러에 달했습니다. 예측 기간 종료시에는 11억 3,000만 달러에 이를 것으로 예측되고 있습니다.

- 유럽 국가 중 스페인은 2024년 유럽 종자 처리 시장의 12.9% 시장 점유율을 차지하고 있습니다.

- 게다가 유럽의 종자치료보증제도(ESTA)와 같은 일부 제도는 종자치료와 그 결과 얻은 처리종자가 입법자와 산업계에 의해 정의된 요건을 충족하고 있음을 보증하는 품질보증제도이며, 시장 성장을 촉진하고 있습니다. ESTA는 프랑스(PQP)와 독일(SeedGuard)의 국가 품질 보증 제도와 호환성을 갖도록 설계되어 있습니다.

유럽 종자 처리 시장 동향

팜 투 포크 전략과 종자와 토양을 매개하는 질병을 방제하기위한 다른 옵션의 채택이 증가하고 종자 처리제의 헥타르 당 소비량이 감소하고 있습니다.

- 농업은 유럽 경제에 크게 기여하고 있지만, 잡초 만연, 해충, 진균병 등 매년 작물 생산에 큰 손실을 초래하는 몇 가지 과제에 직면하고 있습니다. 유럽 농업은 2022년 농지 1헥타르 당 619.3g의 종자 처리제를 사용했습니다. 이 종자 처리제는 작물의 생육 초기에 발생하는 해충이나 질병으로부터 작물을 지키기 위해서 특별히 설계되고 있어, 농가는 수확량을 늘려, 이 지역에 있어서의 식량 수요의 증대에 대응할 수 있습니다.

- 수년간, 이 지역에서는 1헥타르당 종자 처리제의 사용량이 대폭 감소하고 있습니다. 이 전략의 주요 목표는 비료와 농약의 사용을 절반으로 줄이고 유기농업을 25% 늘리는 것입니다.

- 옥수수는 프랑스, 루마니아, 독일, 헝가리, 이탈리아 등의 유럽 국가에서 재배되는 중요한 농작물입니다. 옥수수의 유전자 변형 품종 도입에 의해 종자 처리제의 사용량은 대폭 감소해, 그 결과, 약제 살포의 필요성도 저하했습니다. 그 결과, 유럽의 옥수수 재배에서는 종자 처리는 일반적이 아니게 되고 있습니다.

시펠메트린, 메탈락실, 아조시스트로빈, 아바멕틴, 에마멕틴벤조산염 기반의 농약 종자 처리는 병해충으로부터 작물을 보호하는데 중요한 역할을 합니다.

- 시페르메트린, 메탈락실, 아조시스트로빈, 아바멕틴, 에마멕틴 벤조산염 기반 농약은 작물을 병해충으로부터 보호하는데 중요한 역할을 합니다. 이 농약은 표적을 좁힌 보호를 제공해, 잎면 살포나 토양 살포의 농약에 비해 소량이 필요하고, 코스트 삭감에 연결됩니다.

- 2022년, 시페르메트린의 가격은 1톤당 2만 1,100달러였습니다.

- 중요한 아실알라닌계 살균제인 메탈락실은 극히 중요합니다.

- 아조시스트로빈은 2022년 톤당 4,600달러로 종자 처리용 살균제로 사용됩니다. 수많은 종자 전염성 및 토양 전염성 병원균에 효과적입니다.

- 2022년, 아바멕틴의 가격은 톤당 8,800달러였습니다. 위험을 줄일 수 있습니다. 이 널리 사용되는 농약은 곤충과 진드기를 포함한 다양한 해충을 효과적으로 제거하여 농업과 원예에 중요한 역할을 합니다.

유럽 종자 처리 산업 개요

유럽 종자 처리 시장은 적당히 통합되어 있으며 상위 5개 기업에서 58.33%를 차지합니다. 이 시장 주요 기업은 Bayer AG, Corteva Agriscience, Mitsui & Co. Ltd (Certis Belchim), Syngenta Group, UPL Limited가 있습니다(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 우크라이나

- 영국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 기능

- 살균제

- 살충제

- 살선충제

- 작물 유형

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 지방 종자

- 잔디 및 관상용

- 생산국

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 우크라이나

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Albaugh LLC

- Bayer AG

- Corteva Agriscience

- Mitsui & Co. Ltd(Certis Belchim)

- PI Industries

- Syngenta Group

- UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Seed Treatment Market size is estimated at 1.53 billion USD in 2025, and is expected to reach 1.89 billion USD by 2030, growing at a CAGR of 4.39% during the forecast period (2025-2030).

Fungicides dominated the European seed treatment market as seeds are more susceptible to soil-borne fungi

- Seed treatment refers to the application of fungicide, insecticide, or a combination of both to seeds to disinfect them and protect them from seed-borne or soil-borne pathogenic organisms. Seed treatment can improve germination, seedling emergence, plant vigor, stand establishment, and total yield, helping ensure the crop is on its way to reaching its full genetic potential.

- The first four to six weeks after sowing is a critical period in the life of a new plant as seedlings emerge and develop their physical makeup. Sowing treated seeds helps protect the germination and establishment stages when emerging seedlings are most vulnerable to attack from invasive insect pests and disease pathogens.

- Fungicides accounted for 46.9% of the European seed treatment market in 2024. The most common disease-causing fungi found in Europe are Fusarium spp., Septoria spp., Pyrenophora spp., Ustilago spp., Tilletia spp., and Botrytis spp. Similarly, Rhizoctonia solani, Phytophthora spp., Pythium spp., Verticillium spp., and Sclerotinia spp. are the most common soil-borne fungi.

- The European seed treatment market is dominated by cereal and grain crops, accounting for 59.8% of the market share in 2024. Cereal crops are susceptible to various seed-borne diseases caused by fungi, bacteria, and viruses. Seed treatment helps protect the seeds from these pathogens, preventing infection during germination and early growth stages. Common seed-borne diseases in cereals include Fusarium, smuts, bunts, and seedling blights.

- Schemes like the European Seed Treatment Assurance Scheme (ESTA), a quality assurance system to ensure that seed treatment and the resulting treated seeds meet requirements defined by legislators and the industry, are boosting the market's growth.

Schemes like the European Seed Treatment Assurance Scheme drive the seed treatment market

- In Europe, annual crops can be subdivided into winter crops and spring and summer crops. Winter crops are sown in autumn and harvested in the summer of the following year. Spring and summer crops are sown and harvested in the same year. In the European Union, wheat, rapeseed, rye, and triticale are typically winter crops, whereas maize, sunflowers, rice, soybeans, potatoes, and sugar beet are summer crops. Barley is common in both its winter and spring varieties.

- Grains and cereals dominated the consumption of seed treatment chemicals in Europe, accounting for about 59.8% of the market value, which was valued at about USD 878.0 million in 2024. It is anticipated to reach USD 1.13 billion by the end of the forecast period. The area under grains and cereals is showing an increasing trend, which was 119.2 million hectares in 2022 to 133.5 million hectares by 2030.

- Among the European countries, Spain accounted for a market share of 12.9% of the European seed treatment market in 2024. The area under cultivation is anticipated to grow from 12.7 million hectares in 2022 to 14.0 million hectares by 2030. This will further drive the country's seed treatment market and it is anticipated to register a CAGR of 3.7% during the forecast period.

- Moreover, a few schemes like the European Seed Treatment Assurance Scheme (ESTA), a quality assurance system to ensure that seed treatment and the resulting treated seed meet requirements defined by legislators and industry are boosting the market's growth. The ESTA has been designed to be compatible with the national quality assurance systems in France (PQP) and Germany (SeedGuard). This will further drive the market and is anticipated to grow at a value CAGR of 4.4% during the forecast period.

Europe Seed Treatment Market Trends

Growing adoption of farm-to-fork strategy and other alternatives for controlling seed and soil-borne diseases is reducing the per hectare consumption of seed treatments

- Agriculture is a major contributor to the European economy, but it faces several challenges, such as weed infestation, insect pests, and fungal diseases, which cause significant losses in crop production every year. To address these issues, the European agricultural industry employed an average of 619.3 grams of seed treatment chemicals per hectare of farmland in 2022. These seed treatment chemicals are specifically designed to protect crops from early crop growth pests and diseases, allowing farmers to increase their yields and meet the growing demand for food in the region.

- Over the years, there has been a significant decrease in the usage of seed treatments per hectare in the region. In 2022, the consumption of seed treatments per hectare was reduced by a substantial 33.0 grams compared to 2017. This decline can be mainly attributed to the increasing adoption of the farm-to-fork strategy in European countries. The primary goal of this strategy is to reduce the use of fertilizers and pesticides by half and increase organic farming by 25%. The widespread adoption of this strategy has led to a significant impact on the application of seed treatments to control soil-borne and seed-borne diseases. Farmers are now actively seeking alternative methods to control these diseases.

- Maize is a crucial field crop cultivated in several European countries such as France, Romania, Germany, Hungary, and Italy. These countries have more than a million hectares of farmland dedicated to maize cultivation. The introduction of genetically modified varieties of maize has led to a significant decrease in the use of seed treatment chemicals, resulting in a lower need for their application. As a result, seed treatment is becoming less common in European maize cultivation.

Cypermethrin, metalaxyl, azoxystrobin, abamectin, and emamectin benzoate-based pesticide seed treatments play an important role in protecting crops from pests and diseases

- Cypermethrin, metalaxyl, azoxystrobin, abamectin, and emamectin benzoate-based pesticides play an essential role in protecting crops from pests and diseases. Farmers are becoming more aware of the advantages of using seed treatment pesticides. These chemicals provide targeted protection, requiring lower quantities compared to foliar or soil-applied pesticides, which can lead to cost savings.

- In 2022, cypermethrin was priced at USD 21.1 thousand per metric ton. This synthetic pyrethroid is used as an insecticide by farmers for seed treatment before planting, providing protection against insect, pest, and bird attacks. Cypermethrin serves as a highly effective insecticide seed treatment to mitigate bulb flies and wireworms.

- Metalaxyl, a significant acyl-alanine fungicide, holds crucial importance. Effective against oomycetes such as Pythium, Phytophthora, and various downy mildews, it is commonly applied in crops like corn, peas, sorghum, and sunflower. In 2022, its price amounted to USD 4.5 thousand per metric ton.

- Azoxystrobin, which was priced at USD 4.6 thousand per metric ton in 2022, is used as a seed treatment fungicide. It is effective against numerous seed-borne and soil-borne pathogens, which cause seed decay, seedling blight, and damping-off. Azoxystrobin mainly targets diseases such as Pythium, Fusarium, white mold, brown spot, and Phomopsis.

- In 2022, abamectin was priced at USD 8.8 thousand per metric ton. By employing abamectin seed treatment, plants receive protection right from the start, mitigating the risk of early pest damage during critical early growth stages. This widely used pesticide plays a significant role in agriculture and horticulture by effectively controlling various pests, including insects and mites.

Europe Seed Treatment Industry Overview

The Europe Seed Treatment Market is moderately consolidated, with the top five companies occupying 58.33%. The major players in this market are Bayer AG, Corteva Agriscience, Mitsui & Co. Ltd (Certis Belchim), Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Ukraine

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Ukraine

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Albaugh LLC

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 Mitsui & Co. Ltd (Certis Belchim)

- 6.4.5 PI Industries

- 6.4.6 Syngenta Group

- 6.4.7 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms