|

시장보고서

상품코드

1906930

압력 센서 산업 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Pressure Sensors Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

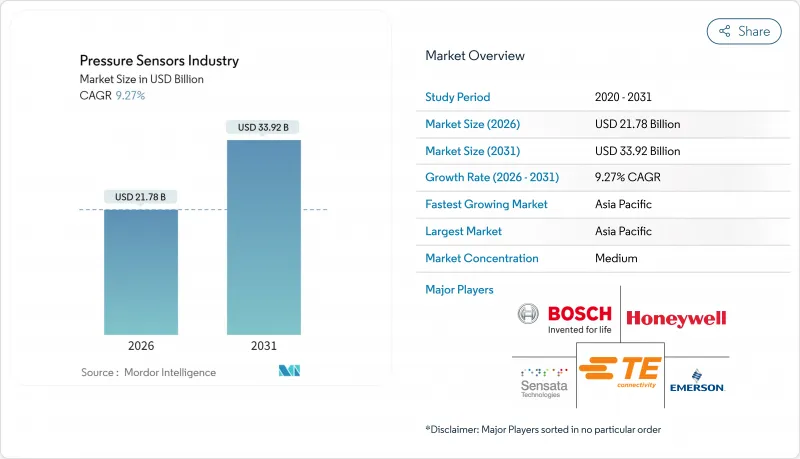

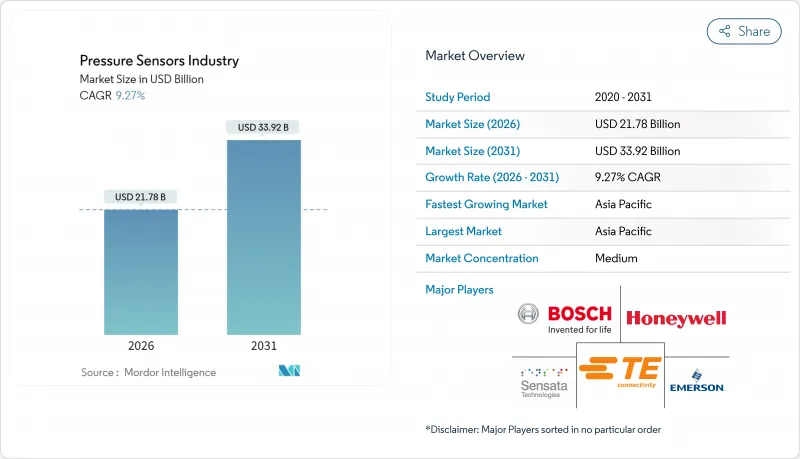

압력 센서 시장은 2025년 199억 3,000만 달러로 평가되었고, 2026년 217억 8,000만 달러에서 2031년까지 339억 2,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 9.27%를 나타낼 전망입니다.

안전성과 효율성을 위해 정밀한 압력 모니터링이 필요한 전기화 파워트레인 제어, 스마트 공장 개조, 일회용 의료 기기에서 강력한 수요가 발생하고 있습니다. 아시아태평양 지역의 전기화 의무화는 xEV 배터리 열 관리 시스템에 고정밀 기압 센서 채택을 가속화하고 있으며, 유럽과 북미 전역의 인더스트리 4.0 업그레이드는 설치 비용을 절감하는 무선 노드를 선호하고 있습니다. 의료 기기 소형화, 특히 심혈관 카테터 분야의 진전은 멸균 기준을 충족하는 일회용 MEMS 설계에 상당한 기회를 열어주고 있습니다. 동시에 LNG 운반선 함대와 같은 가혹한 환경 탐사 분야에서는 175°C 이상의 공정 라인을 견딜 수 있는 실리콘 카바이드 및 광학 기술에 대한 프리미엄 수요가 발생하고 있습니다. 경쟁 강도가 높아지고 있습니다. 기존 업체들은 마진을 방어하기 위해 엣지에 AI 엔진을 내장하는 반면, 중국 화이트라벨 MEMS 파운드리 업체들은 생산량을 확대하며 평균 판매 가격을 낮추고 있습니다.

세계의 압력 센서 산업의 동향 및 인사이트

xEV 파워트레인 제어 시스템의 급속한 전동화가 고정밀 기압 센싱을 주도

전기차는 정밀 기압 센서를 활용해 셀 팽창 감지 및 열 관리로 열폭주 사고를 방지하며, 이는 OEM당 최대 3,000달러의 손실을 초래할 수 있습니다. 센서 공급사들은 실리콘 카바이드 트랙션 인버터의 시장 점유율이 2027년까지 50%에 달할 전망에 따라 175°C 이상 작동 가능한 내구성 설계로 전환 중입니다. 중국, 일본, 한국은 기가팩토리 생산 능력과 정부 보조금이 맞물려 채택을 가속화하며 자동차 수요가 가장 강세입니다.

스마트 공장 개조 확대가 무선 센서 노드 수요 촉진

유럽 및 북미 제조업체들은 기존 장비에 LoRaWAN 및 NB-IoT 압력 노드를 추가해 예측 유지보수를 구현하고 있으며, 저전력 광역 연결은 2030년까지 35억 개를 넘어설 것으로 전망됩니다. WIKA 계측기 시설과 같은 조립 라인에서는 이제 단일 자동화 셀에 10,000개 이상의 센서 변종이 통합됩니다. 개조 프로젝트는 고가의 배관 설치 비용을 피하기 위해 배터리 구동 노드를 우선시하며, 이는 무선 채택률 12.8% CAGR의 핵심 요인입니다.

중국 화이트라벨 MEMS 파운드리 업체들의 ASP 침식

MEMSensing과 같은 기업들은 2024년 28.8%-36.85%의 매출 성장을 기록했음에도 여전히 적자를 내고 있어, 글로벌 기존 업체들의 마진을 압박하는 공격적인 가격 정책을 부각시켰습니다. 서구 공급업체들은 고온 실리콘 카바이드 및 AI 지원 패키지로 전환하며 대응하고 있습니다.

부문 분석

유선 장치는 엔진 제어 장치 및 수술실과 같은 전력 공급이 풍부한 환경에서 결정론적 데이터 전달이 가능해 2025년 기준 71.32%의 매출을 유지했습니다. 그러나 공장이 인더스트리 4.0으로 전환함에 따라 무선 노드가 12.61%의 연평균 성장률(CAGR)로 추월할 전망입니다. 스마트 제어 개조 키트는 설치 비용을 40% 절감하면서 압력 용기의 예측적 정지를 가능하게 합니다. 파워오버이더넷(PoE) 업그레이드는 단일 회선으로 전력과 데이터를 다중화하여 유선 센서의 경쟁력을 유지하고 있습니다. 무선 노드는 에너지 하베스팅과 엣지 컴퓨팅을 활용하여 회전축이나 밀폐된 챔버 등 기존에는 접근 불가능했던 위치에도 설치가 가능해졌습니다.

절대압 센서 설계는 매니폴드 압력, 기상 기록, 드론 고도 측정에 진공 기준 측정이 필요하기 때문에 2025년 45.58%의 점유율을 유지했습니다. 차압 센서는 HVAC 개조 및 클린룸 여과 모니터링 수요로 10.23%의 연평균 성장률을 기록할 전망입니다. 최근 습식 식각 실리콘 제조 기술로 감도가 5.07mV/V/MPa(0.67% FS 선형성)까지 향상되었다. 게이지 센서는 유압 시스템의 핵심 장치로 남아 있으나 중반 단일 자릿수 성장에 그칠 것으로 예상됩니다.

지역별 분석

아시아태평양 지역의 35.62% 점유율 주도권은 중국의 MEMS 팹과 인도의 TPMS 의무화 정책에서 비롯됩니다. 국도 확장 사업과 5,293개 전기차 충전소가 차량당 센서 탑재량을 촉진하고 있습니다. 현지 생산사들이 기술 격차를 좁혀가고 있으며, 주요 업체들은 국내 공급사들이 자동차 인식 스택에 AI를 통합하고 있다고 지적합니다. 유럽은 산업 자동화 유산을 활용합니다. 인피니언의 50억 유로 규모 드레스덴 스마트 파워 팹은 전략적 반도체 자립을 강조합니다. 북미는 항공우주 및 의료 부문에서 두각을 나타내며, DARPA 지원 연구가 센싱 기술의 한계를 넓히고 있습니다. 중동 및 아프리카는 해저 계측 장비가 필요한 LNG 프로젝트로 12.08%의 가장 빠른 연평균 성장률(CAGR)을 기록하며, 무선 전개의 기반이 되는 스마트 시티 인프라가 이를 보완합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- xEV 파워트레인 제어 시스템의 급속한 전기화로 인한 고정밀 기압 센싱 수요 증가(아시아)

- 스마트 공장 개수 확대가 무선 센서 노드 수요를 주도(유럽 및 북미)

- 인도 및 ASEAN의 이륜차용 타이어 공압 감시 장치 의무화 도입

- 정밀 열역학적 압력 제어가 필요한 5G mmWave 무선 통신 장비의 가속화된 도입

- 외래 심혈관 클리닉에서 일회용 MEMS 압력 카테터 채택(미국)

- LNG 운반선 함대 확대로 가혹한 환경의 해저 압력 계측 수요 증가(중동)

- 시장 성장 억제요인

- 중국의 화이트라벨 MEMS 파운드리 업체로 인한 ASP 하락

- 통합 비용 증가를 초래하는 분산된 무선 프로토콜 환경

- 175℃를 넘는 프로세스 라인의 광학식 압력 칩 신뢰성에 관한 우려

- 대량 압저항 웨이퍼 부족에 대한 공급망 노출

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 매크로 동향이 시장에 미치는 영향

- 투자 분석

제5장 시장 규모와 성장 예측

- 센서 유형별

- 유선

- 무선

- 제품 유형별

- 절대압

- 차동형

- 게이지

- 기술별

- 압전 저항 소자

- 전자기

- 용량성

- 공진형 고체

- 광학

- 기타 압력 센서

- 용도별

- 자동차

- 의료

- 소비자용 전자 기기

- 산업

- 항공우주 및 방위

- 식품, 음료

- HVAC

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd

- All Sensors Corporation

- Bosch Sensortec GmbH

- Endress Hauser AG

- TE Connectivity

- Honeywell International Inc.

- Schneider Electric SE

- Kistler Group

- Rockwell Automation Inc.

- Emerson Electric Co.

- Sensata Technologies Inc.

- Siemens AG

- Yokogawa Electric Corp.

- Infineon Technologies AG

- STMicroelectronics NV

- Sensirion AG

- NXP Semiconductors NV

- Texas Instruments Inc.

- Omron Corporation

- Murata Manufacturing Co., Ltd.

- Amphenol(SSI Technologies)

- BD Sensors GmbH

- Keller AG fur Druckmesstechnik

제7장 시장 기회와 장래의 전망

HBR 26.02.04The pressure sensors market was valued at USD 19.93 billion in 2025 and estimated to grow from USD 21.78 billion in 2026 to reach USD 33.92 billion by 2031, at a CAGR of 9.27% during the forecast period (2026-2031).

Strong demand stems from electrified power-train control, smart-factory retrofits, and disposable medical devices that require precise pressure monitoring for safety and efficiency. Electrification mandates in Asia-Pacific are accelerating adoption of high-accuracy barometric sensors in xEV battery-thermal systems, while Industry 4.0 upgrades across Europe and North America favor wireless nodes that cut installation cost. Medical device miniaturization, especially in cardiovascular catheters, is opening a sizeable opportunity for single-use MEMS designs that meet sterilization standards. At the same time, harsh-environment exploration-such as LNG carrier fleets-creates premium demand for silicon-carbide and optical technologies capable of surviving >175 °C process lines. Competitive intensity is rising: incumbents embed AI engines at the edge to defend margins, whereas Chinese white-label MEMS foundries scale volume and depress average selling prices.

Global Pressure Sensors Industry Trends and Insights

Rapid electrification of xEV power-train control systems driving high-accuracy barometric sensing

Electric vehicles use precision barometric sensors to detect cell swelling and manage heat, avoiding thermal runaway events that can cost OEMs up to USD 3,000 per vehicle. Sensor suppliers are hardening designs for >175 °C operation because silicon-carbide traction inverters will reach 50% penetration by 2027. Automotive demand is strongest in China, Japan, and South Korea where gigafactory capacity and government subsidies intersect to accelerate adoption.

Expansion of smart-factory retrofits boosting wireless sensor node demand

European and North American manufacturers are layering LoRaWAN and NB-IoT pressure nodes onto legacy equipment to enable predictive maintenance; low-power wide-area connections are forecast to exceed 3.5 billion by 2030. Assembly lines such as WIKA's gauge facility now incorporate more than 10,000 sensor variants in a single automated cell. Retrofit projects prioritize battery-powered nodes to avoid expensive conduit runs, a key factor behind the 12.8% CAGR in wireless uptake.

ASP erosion from Chinese white-label MEMS foundries

Firms such as MEMSensing posted 28.8%-36.85% revenue growth in 2024 while still running at a loss, underscoring aggressive pricing tactics that compress margins for global incumbents. Western vendors answer by pivoting toward high-temperature silicon-carbide and AI-enabled packages.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory tyre-pressure monitoring adoption waves in India & ASEAN two-wheelers

- Accelerated rollout of 5G mmWave radios requiring precision thermo-mechanical pressure control

- Fragmented wireless protocol landscape inflating integration cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wired devices retained 71.32% revenue in 2025 due to deterministic data delivery in power-rich settings such as engine control units and surgical theaters. However, wireless nodes will outpace with a 12.61% CAGR as factories retrofit to Industry 4.0. Smart Control retrofit kits cut installation expense by 40% while enabling predictive shutdowns for pressure vessels. Power-over-Ethernet upgrades are keeping wired sensors relevant by multiplexing power and data on a single line. Wireless nodes leverage energy harvesting and edge compute, allowing placement on rotating shafts or sealed chambers once considered unreachable.

Absolute designs held 45.58% share in 2025 because manifold pressure, weather logging, and drone altimetry require vacuum-referenced readings. Differential units will see a 10.23% CAGR thanks to HVAC retrofits and filtration monitoring in cleanrooms. Recent wet-etch silicon fabrication pushed sensitivity to 5.07 mV/V/MPa with 0.67% FS linearity. Gauge units remain staple devices in hydraulics but exhibit only mid-single-digit growth.

The Pressure Sensors Market Report is Segmented by Type of Sensor (Wired, Wireless), Product Type (Absolute, Differential, Gauge), Technology (Piezoresistive, Electromagnetic, Optical, Capacitive, Resonant Solid-State, and More), Application (Automotive, Medical, Industrial, Aerospace and Defense, HVAC, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 35.62% leadership stems from China's MEMS fabs and India's TPMS mandates. The National Highways expansion and 5,293 EV charging stations catalyze sensor content per vehicle. Local producers are closing the technology gap; Major players notes domestic suppliers are integrating AI into automotive perception stacks. Europe leverages its industrial automation heritage; Infineon's EUR 5 billion Dresden Smart Power Fab underscores strategic semiconductor self-reliance. North America excels in aerospace and medical segments, with DARPA-funded research pushing sensing frontiers. The Middle East & Africa posts the fastest 12.08% CAGR on LNG projects needing subsea instrumentation, complemented by smart-city infrastructure that seeds wireless deployments.

- ABB Ltd

- All Sensors Corporation

- Bosch Sensortec GmbH

- Endress+Hauser AG

- TE Connectivity

- Honeywell International Inc.

- Schneider Electric SE

- Kistler Group

- Rockwell Automation Inc.

- Emerson Electric Co.

- Sensata Technologies Inc.

- Siemens AG

- Yokogawa Electric Corp.

- Infineon Technologies AG

- STMicroelectronics N.V.

- Sensirion AG

- NXP Semiconductors N.V.

- Texas Instruments Inc.

- Omron Corporation

- Murata Manufacturing Co., Ltd.

- Amphenol (S S I Technologies)

- BD Sensors GmbH

- Keller AG fur Druckmesstechnik

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid electrification of xEV power-train control systems driving high-accuracy barometric sensing (Asia)

- 4.2.2 Expansion of smart factory retrofits boosting wireless sensor node demand (Europe and NA)

- 4.2.3 Mandatory tyre-pressure monitoring adoption waves in India and ASEAN two-wheelers

- 4.2.4 Accelerated rollout of 5G mmWave radios requiring precision thermo-mechanical pressure control

- 4.2.5 Adoption of disposable MEMS pressure catheters in outpatient cardiovascular clinics (US)

- 4.2.6 LNG carrier fleet build-up elevating harsh-environment subsea pressure instrumentation (Middle East)

- 4.3 Market Restraints

- 4.3.1 ASP erosion from Chinese white-label MEMS foundries

- 4.3.2 Fragmented wireless protocol landscape inflating integration cost

- 4.3.3 Reliability concerns in optical pressure chips beyond 175 degree C process lines

- 4.3.4 Supply-chain exposure to bulk piezoresistive wafer shortages

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macro Trends on the Market

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type of Sensor

- 5.1.1 Wired

- 5.1.2 Wireless

- 5.2 By Product Type

- 5.2.1 Absolute

- 5.2.2 Differential

- 5.2.3 Gauge

- 5.3 By Technology

- 5.3.1 Piezoresistive

- 5.3.2 Electromagnetic

- 5.3.3 Capacitive

- 5.3.4 Resonant Solid-State

- 5.3.5 Optical

- 5.3.6 Other Pressure Sensors

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Medical

- 5.4.3 Consumer Electronics

- 5.4.4 Industrial

- 5.4.5 Aerospace and Defense

- 5.4.6 Food and Beverage

- 5.4.7 HVAC

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global- and Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 All Sensors Corporation

- 6.4.3 Bosch Sensortec GmbH

- 6.4.4 Endress+Hauser AG

- 6.4.5 TE Connectivity

- 6.4.6 Honeywell International Inc.

- 6.4.7 Schneider Electric SE

- 6.4.8 Kistler Group

- 6.4.9 Rockwell Automation Inc.

- 6.4.10 Emerson Electric Co.

- 6.4.11 Sensata Technologies Inc.

- 6.4.12 Siemens AG

- 6.4.13 Yokogawa Electric Corp.

- 6.4.14 Infineon Technologies AG

- 6.4.15 STMicroelectronics N.V.

- 6.4.16 Sensirion AG

- 6.4.17 NXP Semiconductors N.V.

- 6.4.18 Texas Instruments Inc.

- 6.4.19 Omron Corporation

- 6.4.20 Murata Manufacturing Co., Ltd.

- 6.4.21 Amphenol (S S I Technologies)

- 6.4.22 BD Sensors GmbH

- 6.4.23 Keller AG fur Druckmesstechnik

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment