|

시장보고서

상품코드

1685842

군용기용 아비오닉스 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 통계 및 성장 예측Military Aircraft Avionics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

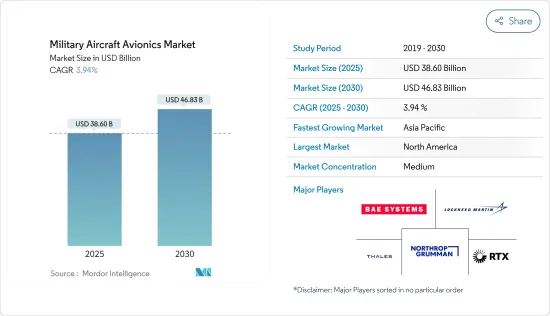

군용기용 아비오닉스 시장 규모는 2025년에 386억 달러로 추정되며, 예측 기간(2025-2030년) 동안 CAGR 3.94%로 성장하여 2030년에는 468억 3,000만 달러에 달할 것으로 예측됩니다.

지정학적 긴장과 국경 분쟁으로 세계의 일부 국가는 새로운 군용기, 헬리콥터 및 드론 조달을 서두르고 있으며, 이는 군사비의 대폭적인 상승으로 이어지고 있습니다. 공중전 능력을 강화하기 위해 최신예 장비로 전투기 현대화에 투자하고 있습니다.

첨단 아비오닉스의 도입으로 인해 기존 군용기의 구형 아비오닉스 시스템을 대체할 필요성이 발생합니다. 신형 아비오닉스 시스템은 새로운 전장의 조건에 맞춰 항공기를 지원합니다. 따라서 적보다 뒤쳐지지 않도록 방위군은 군용기의 아비오닉스 현대화를 계획하고 있습니다.

각국의 UAV에 대한 수요 증가는 고가의 유인 항공기에 대한 잠재적인 손해나 위험을 방지하기 위한 목적으로 적대공역 상공에 UAV를 배치할 필요성이 높아지고 있는 것이 배경에 있습니다. UAV는 임무 유효성의 장점 뿐만 아니라 전투 목표의 포착이나 수색 및 구조 활동도 실시할 수 있습니다. 항공기와 비교하여 UAV의 조달 비용이 낮기 때문에 신흥 국가의 UAV 취득이 증가하고 있습니다. 비대칭적인 위협과 복잡한 작전 환경을 특징으로 하는 현대 전쟁의 성격 변화로 인해 고도로 적응 가능하고 유연한 플랫폼의 필요성이 높아지고 있습니다.

군용기용 아비오닉스 시장 동향

예측 기간 동안 비행 제어 시스템 분야가 시장을 독점

군용 항공기 비행 제어 시스템(FCS)은 데이터 수집 시스템, 오토 파일럿, 비행 기록 장치, 액티브 인셉터 시스템, 항공기 관리 컴퓨터 등 조종석 비행 제어를 위한 하드웨어 및 소프트웨어 시스템으로 구성됩니다. 시스템은 플라이 바이 와이어(FBW) 기술을 기반으로 개발되고 있습니다. 다양한 지역에서 지정학적 긴장이 높아지고 있기 때문에 국방군은 전투 능력을 강화할 필요성을 체감하고 있습니다.

또한 항공기 OEM은 아비오닉스 OEM과 제휴하여 신세대 항공기에 첨단 비행 제어 시스템을 개발 및 탑재하고 있습니다. 예를 들어 2023년 1월 프랑스는 Thales와 Sabena Technics에 프랑스 공군과 우주군의 C N-235 군용 수송기의 업그레이드 계약을 발주했습니다. 업그레이드가 완료되면 CN-235 함대는 2040년 경 운용이 가능할 전망입니다. Arcfield Canada는 CF-18의 아비오닉스 서비스 지원 계약을 1억 5,700만 달러에 수주했습니다.

예측 기간 중 북미가 최대 시장 점유율을 차지할 전망

북미는 이 시장에서 지배적인 지역 기업으로서 대두할 것으로 예상됩니다. 미국에서는 최근 몇 년간 세계적인 분쟁 증가, 지정학적 긴장 증가, 테러리즘, 미국의 잠재적 적대세력의 능력 향상 등의 다양한 요인에 의해 군용기용 아비오닉스 수요가 대폭 증가하고 있습니다.

미 정부는 방위능력을 강화하기 위해 기술 플랫폼에 대규모 투자를 시행하고 있습니다. 예를 틀면, 2023년 미 군사방위비는 9,160억 달러로 증가하였으며 2022년과 비교해서 2.3% 증가했습니다. 첨단 무기에 대한 투자 증가는 러시아와 중국의 미국에 대한 위협이 증가하고 있기 때문입니다. 이러한 군사비 증액을 통해 미 국방부(US DoD)는 미국의 지역 방위력 현대화와 역량 확대를 위해 노력하고 있습니다.

예를 들어 2024년 2월 미국 육군은 Triumph Group에 CH-47 Chinook 헬리콥터 T55 엔진의 EMC32T 유압 미터링 어셈블리(HMA) 연료 제어 업그레이드 계약을 발주했습니다. 해당 계약을 통해 HMA를 오버홀하고 최신 규격에 적합하게 업그레이드합니다. 마찬가지로 2024년 3월, 해군 항공 시스템 사령부는 보잉사에 신형 제트 전투기 F/A-18 슈퍼 호넷 폭격기 17기, 센서, 아비오닉스의 제조 계약을 14억 달러에 발주했습니다. 호넷은 능동형 전자주사식 위상배열(AESA) 레이더, 대형 조종석 디스플레이, 그리고 공동 헬멧 탑재형 큐잉 시스템을 특징으로 하고 있습니다.

군용기용 아비오닉스 산업 개요

군용기용 아비오닉스 시장은 반고정적이며, 여러 회사가 시장 점유율의 대부분을 차지하고 있습니다.

Thales는 NH90, AH-1Z Viper, T129, UH-1Y Venom, Tiger, Rooivalk 헬리콥터와 같은 회전익 항공기 프로그램을 지원하는 유명한 헤드업 디스플레이(HUD) 제공업체입니다. BAE Systems PLC는 F-35 라이트닝 II 전투기의 액티브 인셉터 시스템, 전자전 스위트, 차량 관리 컴퓨터, 식별, 통신, 그리고 네비게이션 시스템용 전자 부품을 제공합니다. 주요 기업은 R&D에 투자하고 새로운 시장을 얻기 위해 첨단 제품을 개발하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 서브시스템

- 비행 제어 시스템

- 통신 시스템

- 네비게이션 시스템

- 모니터링 시스템

- 기타 서브시스템

- 항공기 유형

- 고정익 전투기

- 고정익 비전투기

- 헬리콥터

- 무인항공기(UAV)

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이스라엘

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- L3 Harris Technologies Inc.

- RTX Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Thales

- BAE Systems PLC

- Honeywell International Inc.

- Elbit Systems Ltd

- Cobham Limited

- Garmin Ltd

- Moog Inc.

제7장 시장 기회와 미래 동향

CSM 25.04.22The Military Aircraft Avionics Market size is estimated at USD 38.60 billion in 2025, and is expected to reach USD 46.83 billion by 2030, at a CAGR of 3.94% during the forecast period (2025-2030).

Due to geopolitical tensions and border disputes, several countries worldwide are expediting their procurement of new military aircraft, helicopters, and drones, leading to a significant rise in military spending. Numerous nations are investing in modernizing their fleets with state-of-the-art equipment to bolster their aerial capabilities. These investments in the procurement and modernization of military aircraft are anticipated to drive market growth in the future.

The introduction of advanced avionics generates the need to replace old avionics systems in conventional military aircraft. These new avionics suites support the aircraft in meeting the new battlefield requirements, such as electronic warfare defense and long-distance target detection and tracking. Therefore, to stay abreast of adversaries, the defense forces plan to modernize the avionics in military aircraft. Various countries are procuring next-generation military aircraft to expand their fleets.

Various nations' rising demand for UAVs is driven by the increasing necessity to deploy them over hostile airspace, aiming to prevent any potential damage or danger to expensive manned aircraft. Besides their effectiveness in intelligence, surveillance, and reconnaissance (ISR) missions, UAVs can carry out combat target acquisition and search and rescue operations. The rising demand for UAVs is primarily motivated by the safety of crew members involved in non-combat missions. Additionally, the lower procurement cost of UAVs compared to traditional aircraft used for similar purposes has led to their increased acquisition by developing countries. However, challenges in certifications and integration of new hardware in advanced avionics systems hamper market growth. The changing nature of modern warfare, characterized by asymmetric threats and complex operational environments, necessitates the need for highly adaptable and flexible platforms. Such developments may create market opportunities in the future.

Military Aircraft Avionics Market Trends

The Flight Control Systems Segment to Dominate the Market During the Forecast Period

A military aircraft's flight control system (FCS) consists of hardware and software systems for cockpit flight controls, such as data acquisition systems, autopilot, flight recorders, active inceptor systems, and aircraft management computers. Currently, the flight control systems in military aircraft are developed based on fly-by-wire (FBW) technology. The rising geopolitical tensions across various regions have compelled defense forces to enhance their combat capabilities. Many countries have increased their defense budgets to strengthen their military capabilities, driving the demand for military aircraft and UAVs.

Additionally, aircraft OEMs have partnered with avionics OEMs to develop and equip advanced flight control systems in new-generation aircraft. Also, key players are focusing on integrating next-generation technologies such as big data analytics and artificial intelligence (AI) into computers to enhance the autonomous operations of human-crewed and uncrewed aircraft. For instance, in January 2023, France granted Thales and Sabena Technics a contract to upgrade the CN-235 military transport fleet of the French Air and Space Force. Once the upgrade is done, the CN-235 fleet will be operational through 2040. Similarly, in March 2024, Canada's Department of National Defence (DND) awarded Arcfield Canada a contract to provide avionics in-service support for the CF-18 fleet for USD 157 million. Such developments are expected to accelerate the market's growth during the forecast period.

North America Expected to Exhibit the Largest Market Share During the Forecast Period

North America is expected to emerge as the dominant regional player in the market. The demand for military aircraft avionics significantly increased in the United States in recent years due to various factors such as the rise of global conflicts, growing geopolitical tensions, terrorism, and the increasing capabilities of potential adversaries of the United States.

The US government has invested heavily in technological platforms to enhance its defense capabilities. For instance, in 2023, the US military defense expenditure rose to USD 916 billion, a growth of 2.3% compared to 2022. Rising investments in advanced weaponry are due to the increasing threat to the country from Russia and China on the battlefield. With this increased military expenditure, the US Department of Defense (US DoD) is working to modernize and expand the country's regional defense forces capabilities.

For instance, in February 2024, the US Army awarded Triumph Group a contract to upgrade the EMC32T Hydraulic Metering Assembly (HMA) fuel control on the T55 engines for the CH-47 Chinook helicopter fleet. Triumph will overhaul more than 100 EMC32T HMAs each year from 2024 to 2028 to ensure they meet the latest standards. Similarly, in March 2024, the Naval Air Systems Command awarded Boeing a contract to build 17 new F/A-18 Super Hornet jet fighter bombers, sensors, and avionics for USD 1.4 billion. The Super Hornet features an active electronically scanned array (AESA) radar, large cockpit displays, and a joint helmet-mounted cueing system. Such investments by countries in North America to enhance their aerial capabilities are anticipated to propel the growth of the market over the coming years.

Military Aircraft Avionics Industry Overview

The market for military aircraft avionics is semi-consolidated, with only a few players accounting for most of the market share. RTX Corporation, Lockheed Martin Corporation, Thales, BAE Systems PLC, and Northrop Grumman Corporation are some of the prominent players in the market. The key players enter long-term contracts with aircraft OEMs to provide avionic systems.

Thales is a prominent head-up display (HUD) provider that supports rotary-wing aircraft programs such as NH90, AH-1Z Viper, T129, UH-1Y Venom, Tiger, and Rooivalk helicopters. BAE Systems PLC provides active inceptor systems, electronic warfare suite, vehicle management computers, and electronic components for identification, communication, and navigation systems in the F-35 Lightning II fighter aircraft. The key players invest in research and development and develop advanced products to capture new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Subsystem

- 5.1.1 Flight Control System

- 5.1.2 Communication System

- 5.1.3 Navigation System

- 5.1.4 Monitoring System

- 5.1.5 Other Subsystems

- 5.2 Aircraft Type

- 5.2.1 Fixed-wing Combat Aircraft

- 5.2.2 Fixed-wing Non-Combat Aircraft

- 5.2.3 Helicopters

- 5.2.4 Unmanned Aerial Vehicles (UAVs)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 L3 Harris Technologies Inc.

- 6.2.2 RTX Corporation

- 6.2.3 Lockheed Martin Corporation

- 6.2.4 Northrop Grumman Corporation

- 6.2.5 Thales

- 6.2.6 BAE Systems PLC

- 6.2.7 Honeywell International Inc.

- 6.2.8 Elbit Systems Ltd

- 6.2.9 Cobham Limited

- 6.2.10 Garmin Ltd

- 6.2.11 Moog Inc.