|

시장보고서

상품코드

1685890

아프리카의 생물촉진제 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Africa Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

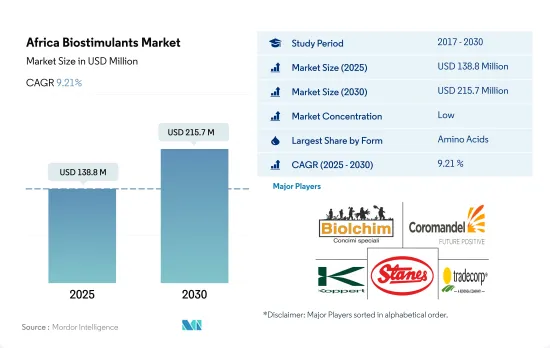

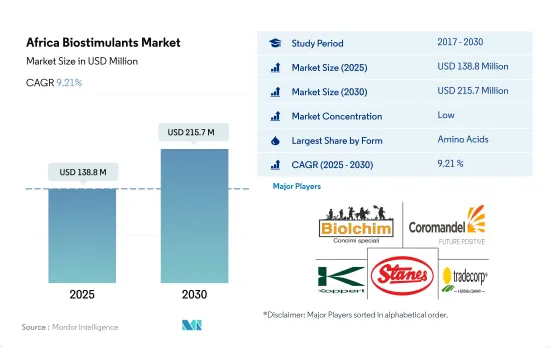

아프리카의 생물촉진제 시장 규모는 2025년에 1억 3,880만 달러, 2030년에는 2억 1,570만 달러에 이를 것으로 예측되며, 예측 기간(2025년-2030년) CAGR은 9.21%를 나타낼 전망입니다.

- 아미노산 기반 생물촉진제는 아프리카 시장을 독점하며, 2022년에는 3,530만 달러로 평가되었습니다. 생물학적 및 생물학적 스트레스에 대한 작물의 회복력을 향상시키고, 특히 질소와 인에 관하여 영양분의 흡수와 이용을 촉진하고, 농약이나 비료 등의 다른 농업 투입물의 효율을 증폭하는 능력이 있기 때문에 널리 사용되고 있습니다.

- 후민산 기반의 생물촉진제는 스트레스 내성의 향상, 양분 흡수량 증가, 화학 투입의 전체적인 삭감 등의 이점이 있어, 또한 관개나 토양 살포에 의한 시용이 용이하기 때문에 시장을 견인할 가능성이 있어 시장 가치는 2029년까지 약 78.5% 증가했습니다.

- 부식산 기반 생물촉진제는 토양, 이탄, 석탄 및 기타 화석 광상에 포함된 부식물질에서 유래하는 유기 토양 개량제의 일종으로 토양 건강과 식물 성장을 가속할 것으로 알려져 있습니다. 부식산을 풍부하게 포함하고 있습니다.이 생물촉진제는 2022년의 아프리카의 생물촉진제 시장의 금액 베이스로 23.4%를 차지해, 2위 시장 점유율을 차지하고 있습니다.

- 해초 추출물 기반 생물촉진제는 많은 해안 지역에서 풍부하게 이용 가능하며 농업에서 화학 비료의 필요성을 줄일 수 있기 때문에 아프리카 시장 점유율을 향상시킬 수 있습니다. 이러한 요인은 예측 기간 동안 해초 기반의 생물촉진제 수요를 촉진할 가능성이 있습니다.

- 2023년부터 2029년 사이에 다른 생물촉진제보다 급속하게 성장할 것으로 예측되고 있습니다.

- 아프리카는 다양한 농업 시스템으로 알려져 있으며, 지역 전체에서 다양한 작물이 재배되고 있습니다. 농업은 아프리카 경제에서 중요한 역할을 하고 있으며, 유기농업은 2021년에는 약 12만 헥타르의 유기농 작물 재배 면적을 가질 정도로 성장했습니다. 옥수수, 쌀, 수수와 같은 곡물은 이 지역에서 가장 널리 재배되는 작물 중 하나입니다.

- 아프리카 농업의 성장 분야 중 하나에 생물촉진제 시장이 있어 2017년부터 2021년에 걸쳐 약 18.7% 상승하여 금액이 대폭 증가했습니다.

- 아프리카의 생물촉진제 시장의 대부분은 아프리카의 다른 지역이 차지하고 있으며, 2022년 시장 매출의 약 81.1%를 차지했습니다. 유기생산자 수가 약 22만명으로 가장 많습니다. 그러나 대부분의 아프리카 국가에서는 유기농업에 관한 법률이 정비되어 있지 않기 때문에 일부 지역에서는 확립된 생물촉진제 시장의 확립이 방해되고 있습니다.

- 해초 기반의 생물촉진제는 시장 매출의 43.8%를 차지하고 2022년에는 약 340만 달러가 되었습니다.

- 아프리카에서의 생물촉진제 수요는 국내외 유기농 제품에 대한 소비자의 관심이 높아짐에 따라 향후 수년간 증가할 것으로 예상됩니다. 농부들은 화학 물질 투입에 대한 의존도가 높다는 단점과 생물촉진제를 사용하는 경제적 이점에 대해 더 많은 정보를 얻을 수 있습니다.

아프리카 생물촉진제 시장 동향

이 지역의 유기 부문에는 834,000명의 유기 생산자가 있으며, 튀니지 쪽이 유기농지가 많습니다.

- 2022년 아프리카의 유기농지면적은 120만 헥타르를 넘어 세계의 유기농지면적의 9%를 차지했습니다.

- 2020년, 아프리카는 2019년보다 149,000헥타르 많은 유기 재배지를 보고해, 약 834,000명의 생산자의 존재에 수반해, 전년 대비 7.7% 증가를 기록했습니다. 에티오피아의 유기 생산자 수가 가장 많았다(약 22만명).

- 아프리카에서는 환금작물이 유기농지에서 차지하는 비율이 크고 유기농지면적의 63.2%를 차지하는 81만 7,400헥타르로 되어 있습니다. 유기농지 전체의 약 25.6%, 합계 33만 1,200헥타르에 이릅니다.

- 유기농지면적이 큰 아프리카 국가에는 그 밖의 아프리카 부문, 이집트, 남아프리카가 포함됩니다. 타르에서 아프리카의 유기농업 총면적의 95.0%를 차지하고, 이집트가 4만5,100헥타르로 3.5%, 남아프리카가 1만2,600헥타르로 1.0%의 점유율을 차지합니다.

- 아프리카에서는 2017년부터 2022년 사이에 유기농업의 작부면적이 6.9% 증가했습니다.

1인당 유기농 제품에 대한 지출은 이집트, 남아프리카, 나이지리아 국가가 우세

- 아프리카의 1인당 소득은 수년에 걸쳐 지속적으로 증가하고 있으며, 사람들은 영양가가 높은 식품에 더 많은 지출을 하게 되었습니다. 아프리카에서는 유기농 식품과 식음료가 더 많은 선반에 늘어서 있습니다. 유기농 인증을 받은 농산물의 국내 소비량은 비교적 적기 때문에 유기농 제품의 대부분은 수출용으로 생산되고 있습니다.

- 아프리카에서는 특히 이집트, 남아프리카, 나이지리아에서 유기 제품의 소비가 크게 증가하고 있습니다. 2021년 유기농 제품의 1인당 소비는 이집트 55.5달러, 남아프리카 7.1달러였습니다. 유기농 생산자 수가 가장 많은 나라는 에티오피아(거의 222,000명), 탄자니아(거의 149,000명), 우간다(139,000명 이상)였습니다.

- 아프리카에서 일반적으로 소비되는 유기농 제품에는 신선한 야채와 과일이 포함됩니다. 아프리카에서는 유기농업을 정책, 국가개선보급시스템, 마케팅, 밸류체인 개척의 주류로 삼기 위한 많은 노력이 이루어져 왔습니다. 이러한 모든 요인들이 소비자들의 관심을 끌고 있습니다.

- 과일 주스를 중심으로 한 음료의 1인당 소비량 증가, 건강 의식의 높아짐, 화학 성분을 포함하지 않는 유기 음료 및 식품으로의 소비자의 변화에 따라, 아프리카의 유기 식품 시장 수요는 2023년부터 2029년에 걸쳐 확대될 것으로 예상됩니다.

- 그러나 저소득층이 많아 유기 기준과 현지 시장 인증을 위한 기타 인프라가 갖추어지지 않은 것이 이 지역의 유기 시장 성장의 주요 저해 요인이 되고 있습니다.

아프리카 생물촉진제 산업 개요

아프리카의 생물촉진제 시장은 세분화되어 있으며, 상위 5개사에서 18.64%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Biolchim SPA, Coromandel International Ltd, Koppert Biological Systems Inc., T. Stanes and Company Limited and Trade Corporation International(sorted alphabetically).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 유기 재배 면적

- 1인당 유기농 제품에 지출

- 규제 프레임워크

- 이집트

- 나이지리아

- 남아프리카

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 형태

- 아미노산

- 풀보산

- 후민산

- 단백질 가수분해물

- 해초 추출물

- 기타 생물촉진제

- 작물 유형

- 환금작물

- 원예작물

- 밭작물

- 생산국

- 이집트

- 나이지리아

- 남아프리카

- 기타 아프리카

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일.

- Atlantica Agricola

- Biolchim SPA

- Coromandel International Ltd

- Haifa Group

- Humic Growth Solutions Inc.

- Koppert Biological Systems Inc.

- Microbial Biological Fertilizers International

- T. Stanes and Company Limited

- Trade Corporation International

- UPL

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Africa Biostimulants Market size is estimated at 138.8 million USD in 2025, and is expected to reach 215.7 million USD by 2030, growing at a CAGR of 9.21% during the forecast period (2025-2030).

- Amino acid-based biostimulants dominate the African market, valued at USD 35.3 million in 2022. Amino acid-based biostimulants are widely used because of their ability to enhance seed germination and seedling growth, improve crop resilience to various biotic and abiotic stresses, boost nutrient uptake and utilization, especially with regard to nitrogen and phosphorus, and amplify the efficiency of other agricultural inputs such as pesticides and fertilizers.

- The benefits of humic acid-based biostimulants, such as increased stress tolerance, increased nutrient uptake, and an overall reduction in chemical inputs, as well as their ease of application via fertigation or soil application methods, may drive the market, with the market value expected to grow by about 78.5% to USD 49.6 million by 2029.

- Humic acid-based biostimulants, which are a type of organic soil amendment derived from humic substances found in soil, peat, coal, and other fossil deposits, are known to enhance soil health and plant growth. They are rich in humic acids. These biostimulants account for the second-largest market share, representing 23.4% of the African biostimulant market by value in 2022.

- Seaweed extract-based biostimulants can potentially improve their market share in the African region due to their abundant availability in many coastal areas and their ability to decrease the need for chemical fertilizers in agriculture. These factors may drive the demand for seaweed-based biostimulants during the forecast period. Seaweed extract-based biostimulants accounted for about USD 23.1 million in 2022.

- Humic and fulvic acid-based biostimulants are anticipated to grow faster than other biostimulants between 2023 and 2029.

- Africa is known for its diverse agricultural systems, with a wide range of crops grown across the region. Agriculture plays a vital role in the African economy, and organic farming gained traction, with approximately 120 thousand hectares of organic crop area in 2021. Cereal crops, such as maize, wheat, and corn, are among the most widely grown crops in the region.

- One area of growth in African agriculture is the biostimulants market, which saw a significant increase in value, rising by approximately 18.7% from 2017 to 2021. This growth is expected to continue, with the market value projected to increase by 67.8%.

- The majority of the African biostimulants market is dominated by the Rest of African region, accounting for about 81.1% of the market value in 2022. Tunisia is the top organic producer in terms of area, and Ethiopia has the highest number of organic producers, with approximately 220,000 in 2020. However, the lack of legislation for organic farming in most African countries has hampered the establishment of a well-established biostimulant market in some areas.

- Seaweed-based biostimulants make up 43.8% of the market value, valued at about USD 3.4 million in 2022. The use of seaweed extract-based biostimulants is prevalent in Nigeria.

- The demand for biostimulants in Africa is expected to rise in the coming years, driven by increasing consumer interest in organic products, both domestically and internationally. Farmers are becoming more informed about the drawbacks of heavy reliance on chemical inputs and the economic benefits of using biostimulants. With these factors in play, the biostimulants market in Africa is poised for significant growth, providing opportunities for both farmers and businesses in the region.

Africa Biostimulants Market Trends

8,34,000 organic producers are in the region's organic sector with Tunisia is having more organic land

- In 2022, the area of organic agricultural land in the African region amounted to over 1.2 million hectares, representing 9.0% of the global organic agricultural area.

- In 2020, Africa reported 149,000 hectares more in organic cultivation land than in 2019, recording a 7.7% increase Y-o-Y in line with the presence of nearly 834,000 producers. Tunisia had the largest amount of organic land (more than 290,000 hectares in 2020), whereas Ethiopia had the highest number of organic producers (almost 220,000). The island states of Sao Tome and Principe have the most significant amount of land committed to organic farming in the region, with 20.7% of their agricultural area dedicated to organic crops.

- In the African region, cash crops account for a significant share of organic agricultural land, amounting to 63.2% of the total organic acreage with 817.4 thousand hectares. Row crops hold the second-largest share of organic acreage in Africa, which amounts to about 25.6% of the total organic acreage, totaling 331.2 thousand hectares. Horticultural crops account for 11.2% of the total organic acreage in Africa, with 144.9 thousand hectares in 2022.

- The African countries with significant organic agricultural acreage include the Rest of Africa regional segment, Egypt, and South Africa. In 2022, the Rest of Africa segment accounted for 95.0% of the total organic agricultural acreage in Africa, with 1.2 million hectares, Egypt accounted for a 3.5% share with 45.1 thousand hectares, and South Africa accounted for a 1.0% share with 12.6 thousand hectares.

- Organic agricultural acreage rose by 6.9% between 2017 and 2022 in Africa. It is anticipated to increase by about 52.2% and reach USD 2.0 million by 2029.

Per capita spending on organic product predominant in Egypt, South Africa, and Nigeria countries

- Africa's per capita income has consistently increased throughout the years, encouraging people to spend more money on nutritious food. Organic foods and beverages are gaining more shelf space in the African region. Since the domestic consumption of certified organic produce is relatively small, most organic goods are produced for export.

- In Africa, consumption of organic products has increased significantly, especially in Egypt, South Africa, and Nigeria. In 2021, the per capita consumption of organic products was USD 55.5 in Egypt, followed by South Africa with USD 7.1. The countries with the highest number of organic producers were Ethiopia (almost 222,000), Tanzania (nearly 149,000), and Uganda (over 139,000).

- In the African region, commonly consumed organic products include fresh vegetables and fruits. In Africa, significant efforts have been made to mainstream organic agriculture into policy, national extension systems, marketing, and value chain development. All these factors have gained the attention of consumers.

- With the increasing per capita consumption of beverages, primarily fruit juices, growing health awareness, and consumers shifting toward organic drinks and food that do not contain chemical ingredients, the demand for the African organic food market is expected to grow between 2023 and 2029.

- However, low-income levels and a lack of organic standards and other infrastructure for local market certification are the major restraining factors for the growth of the organic market in the region.

Africa Biostimulants Industry Overview

The Africa Biostimulants Market is fragmented, with the top five companies occupying 18.64%. The major players in this market are Biolchim SPA, Coromandel International Ltd, Koppert Biological Systems Inc., T. Stanes and Company Limited and Trade Corporation International (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Nigeria

- 4.3.3 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Egypt

- 5.3.2 Nigeria

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Atlantica Agricola

- 6.4.2 Biolchim SPA

- 6.4.3 Coromandel International Ltd

- 6.4.4 Haifa Group

- 6.4.5 Humic Growth Solutions Inc.

- 6.4.6 Koppert Biological Systems Inc.

- 6.4.7 Microbial Biological Fertilizers International

- 6.4.8 T. Stanes and Company Limited

- 6.4.9 Trade Corporation International

- 6.4.10 UPL

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms