|

시장보고서

상품코드

1685898

예방 백신 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Preventive Vaccines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

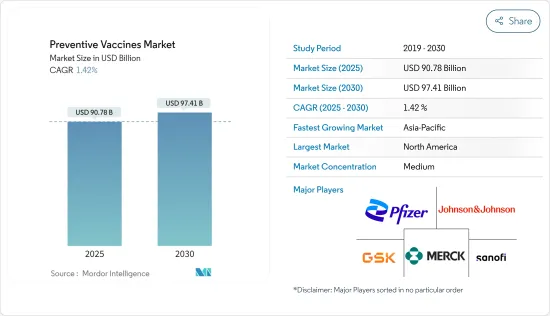

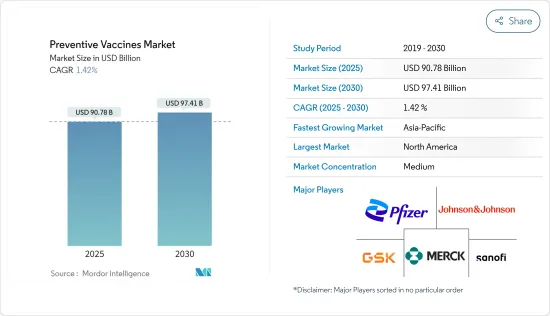

예방 백신 시장 규모는 2025년에 907억 8,000만 달러, 2030년에는 974억 1,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 1.42%를 나타낼 전망입니다.

전염병 확산, 백신 개발 혁신 기술, 정부 및 국제기구의 자금 제공 증가, 예방접종 프로그램에 대한 정부의 관심 증가 등의 요인이 시장 성장을 가속하고 있습니다.

감염증 발생 건수 증가는 예측 기간 중에 예방 백신 수요를 촉진할 것으로 예상되는 주요 요인입니다.2022년에는 전 세계적으로 약 1,060만명이 결핵을 앓았고, 이 중 남성 580만명, 여성 350만명, 소아 130만명이었습니다. 2022년 10만명당 2.5명에서 2023년에는 2.9명으로 2024년 3월에 15% 상승했습니다.

이와 같이 사람들 사이에서 결핵의 부담이 증가하고 있기 때문에 그 예방의 필요성이 높아지고 있으며, 이것이 예측기간 중 시장의 성장을 가속할 것으로 예측되고 있습니다. 하지만 C형 만성 간염 바이러스에 감염되어 있어 매년 약 150만명이 새롭게 감염되고 있습니다.

백신 기술의 급속한 진보는 유전자 공학, 백신 전달 기술, 단백질체학의 도입에 의해 촉진되고 있습니다.2024년 1월 중국 국가약품감독관리국은 CSPC 제약 그룹의 호흡기 세포융합 바이러스(RSV) 후보 백신에 대한 인체 임상 시험 개시를 승인했습니다. 이는 예방 백신 제품 개발 증가로 이어져 시장 성장을 뒷받침할 것으로 예상됩니다.

감염증의 만연을 막기 위한 예방접종 프로그램을 조직하는 정부의 대처가 활발해지고, 백신 접종의 필요성이 높아지고 있는 것이, 예측 기간중 시장의 성장을 높일 것으로 예상됩니다. 프로그램을 시작했습니다. 또한 정부는 대상 연령대에 대한 예방 접종을 적극적으로 추진하고 있습니다.

예방 백신 시장 동향

간염분야는 예측기간 동안 크게 성장할 것으로 예상

간염은 간의 염증을 특징으로 하며, 바이러스, 알코올, 약물 등 다양한 감염원으로부터 발생하는 가능성이 있습니다.

간염 환자 증가는 효과적인 백신 접종 솔루션에 대한 수요가 증가함에 따라 예방 백신 시장의 성장을 가속화할 것으로 보입니다. 주제이기 때문에 공중 보건에 대한 노력과 개인 의식이 모두 백신 개발과 유통에 대한 더 큰 투자로 이어지고 있습니다. 전 세계적으로 3억 400만 명이 만성바이러스성 B형 간염 및 C형 간염으로 진단되었으며, 2022년에는 이러한 만성 바이러스성 간염주의 신규 감염이 220만 건 발생했습니다. 효과적인 백신 접종 솔루션에 대한 수요가 증가함에 따라 백신의 개발과 배포가 더욱 중요해지고 있습니다.

예방 백신 시장의 추진에는 백신 접종 프로그램의 추진, 조사 자금 제공, 공중 보건 정책의 실시 등, 정부의 대처가 중요한 역할을 하고 있습니다. 일반 시민의 접근을 향상시키기 위해 예방 접종 캠페인을 실시하고, 보조금을 지급하거나, 예방 접종 가이드 라인을 책정하는 경우가 많습니다. Gavi는 에볼라, 일상적인 다가 뇌수막염, 인간 광견병 및 B형 간염 출생 시 접종에 대한 예방 조치를 목표로 하는 새로운 예방 접종 이니셔티브를 발표했습니다. Gavi는 저소득국가에 대한 지원을 확대하고 다가 수막염균 결합형 백신이나 B형 간염 출생 용량 백신과 함께 노출 후 예방을 위한 인간 광견병 백신의 정기 투여를 촉진하고 있습니다.

따라서 A형 간염, B형 간염, C형 간염의 부담이 증가와 간염 예방 백신을 뒷받침하는 정부의 이니셔티브이 증가 등의 요인으로, 이 부문은 예측 기간 중에 성장할 것으로 예상됩니다.

예측기간 중 북미가 큰 시장 점유율을 차지할 전망

북미의 예방 백신 시장은 전염병의 유행 증가, 백신 수요 증가, 전염병이 발생하기 쉬운 노인 인구 증가, 주요 시장 기업 존재 등의 요인으로 인해 예측 기간 동안 성장할 것으로 예상됩니다.

COVID-19와 같은 감염증의 부담 증가는 백신 수요를 대폭 증가시켜 예방백신 시장을 견인하고 있습니다. 백신 유통의 개선, 백신 접종의 의무화로 연결됩니다.

같은 출처에 따르면 미국은 2024년 8월까지 국내에서 7억 1,181만 회의 백신이 접종되었습니다.

예방 접종 프로그램의 실행에 정부가 주력하게 된 것도 시장의 성장에 기여하고 있습니다.2023년 12월 온타리오 주민 및 기타 캐나다인들은 보편적 인플루엔자 예방 접종 프로그램(UIIP)에 따라 무료 독감 백신을 이용했습니다. 또한 2023년 2월 캐나다 정부의 예방 접종 프로그램에서는 아이들은 2, 4, 18개월에 폴리오 백신을 접종하고, 그 후 4세와 6세 사이에 부스터 접종을 받아야 한다고 권고했습니다. 따라서 정부 주도의 예방접종 프로그램은 백신에 대한 접근을 확대하고, 국민의 참여를 촉진하고, 백신 개발에 대한 투자를 촉진함으로써 예방 백신 시장을 견인하고 있으며, 북미에서 시장 개척의 원동력이 되고 있습니다.

또한 국내 예방백신 개발을 가속시키기 위한 정부와 국제기관의 자금개척도 시장 성장을 뒷받침할 것으로 예상됩니다. 따라서 간염에 대한 정부 자금 증가는 연구 지원, 생산 능력 강화, 예방 접종 프로그램의 확대로 예방 백신 시장을 추진하고 있습니다.

제휴, 확대, 상시 등 다양한 사업 전략을 채용하는 기업의 주목도가 높아지고 있기 때문에 이 시장에서는 예방 백신의 입수 기회가 창출될 것으로 예상됩니다., 2023년 10월, 화이자는 PENBRAYA에 대한 미국 식품 의약국(FDA)의 승인을 받았으며, 청소년과 청소년 성인에서 수막염균 감염의 가장 흔한 다섯 혈청군에 대한 최초의 유일한 백신이 되었습니다.

또한 2023년 8월 화이자는 ABRYSVO의 미국 FDA 승인을 받았습니다. 특이한 이용 사례에 대한 것이었습니다. 이것은 출생시부터 생후 6개월까지의 유아를 RSV에 의한 하기도 질환(LRTD) 및 중증 LRTD로부터 보호하기 위한 어머니용 백신으로서 미국 최초로 유일한 승인이었습니다.

그러므로 전염병 증가율, 예방접종 프로그램 및 캠페인 증가, 예방 백신 개발을 위한 정부 자금 증가, 기업 활동 활성화 등의 요인으로 인해 예측 기간 동안 시장이 성장할 것으로 예상됩니다.

예방 백신 산업 개요

예방 백신 시장은 세분화되어 있으며, 여러 주요 기업이 진입하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 감염증의 유행 확대

- 백신 개발에 있어서의 혁신적 기술

- 정부 및 국제기구로부터의 자금 제공 증가

- 예방 접종 프로그램에 대한 정부의 관심 증가

- 시장 성장 억제요인

- 부작용의 위험

- 높은 백신 개발 비용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자, 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 백신 유형별

- 생백신, 약독화 백신

- 불활성화 백신

- 서브 유닛 백신

- 톡소이드 백신

- mRNA 백신

- 기타 백신

- 질환 유형별

- 폐렴구균

- 폴리오바이러스

- 간염

- 인플루엔자

- 홍역, 오타후쿠카제, 풍진(MMR)

- COVID-19

- 기타 질환

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- AstraZeneca PLC

- Emergent BioSolutions Inc.

- Daiichi Sankyo Company Limited

- GSK plc

- Johnson & Johnson Services, Inc.

- Merck & Co.

- Novavax Inc.

- Pfizer Inc.

- Sanofi

- Takeda Pharmaceutical Co. Ltd

제7장 시장 기회와 앞으로의 동향

SHW 25.04.23The Preventive Vaccines Market size is estimated at USD 90.78 billion in 2025, and is expected to reach USD 97.41 billion by 2030, at a CAGR of 1.42% during the forecast period (2025-2030).

Factors such as the growing prevalence of infectious diseases, innovative technology in vaccine development, increased funding from government and international organizations, and the increasing government focus on immunization programs are boosting the market's growth.

The rising incidences of infectious diseases are the key factor expected to drive the demand for preventive vaccines over the forecast period. For instance, according to the World Health Organization data published in November 2023, tuberculosis was the second most deadly infectious disease globally, following COVID-19. In 2022, an estimated 10.6 million individuals globally contracted tuberculosis (TB), comprising 5.8 million men, 3.5 million women, and 1.3 million children. Additionally, per the Centers for Disease Control and Prevention (CDC), the US TB rate climbed by 15% in March 2024, from 2.5 per 100,000 individuals in 2022 to 2.9 in 2023.

Thus, the rising burden of tuberculosis among the population increases the need for its prevention, which, in turn, is anticipated to propel the market's growth over the forecast period. Additionally, according to data published by the World Health Organization (WHO) in July 2023, globally, an estimated 58 million people had chronic hepatitis C virus, and about 1.5 million new infections occur annually. According to the same source, the hepatitis C virus is a blood-borne pathogen, and the most common form of the disease is exposure to small amounts of blood. Thus, the increasing burden of hepatitis is propelling the growth of the market.

The rapid advancements in vaccine technology are fueled by the introduction of genetic engineering, vaccine-delivering technology, and proteomics. For instance, in January 2024, the National Medical Products Administration of China granted regulatory approval for CSPC Pharmaceutical Group's candidate vaccine for the respiratory syncytial virus (RSV) to commence human clinical trials. This is expected to increase the development of preventive vaccine products, bolstering the market's growth.

Rising government initiatives in organizing immunization programs to prevent the spread of infectious diseases and the need for vaccination are expected to increase the market's growth over the forecast period. For instance, in February 2024, the Government of India initiated a vaccination program targeting girls aged 9 to 14 aimed at preventing cervical cancer. Furthermore, the government is actively promoting this vaccination among the eligible age group. Therefore, owing to these factors, the market is expected to grow over the forecast period. However, the risk of adverse effects and the high cost of vaccine development will likely impede the market's growth over the forecast period.

Preventive Vaccines Market Trends

The Hepatitis Segment is Expected to Witness Significant Growth Over the Forecast Period

Hepatitis, characterized by liver inflammation, can arise from various sources, including viruses, alcohol, and drugs. The predominant strains are hepatitis A, B, and C, each stemming from distinct viruses. Common symptoms encompass jaundice, fatigue, and abdominal discomfort. Treatment strategies hinge on the underlying cause and the condition's severity.

The rise in hepatitis cases is likely to drive the growth of the preventive vaccines market due to increasing demand for effective vaccination solutions. As hepatitis remains a significant global health issue, especially in areas with high infection rates, both public health initiatives and individual awareness are leading to more substantial investment in vaccine development and distribution. For instance, according to the World Health Organization data updated in 2024, in 2022, 304 million individuals globally were diagnosed with chronic viral hepatitis B and C. Further, 2.2 million new infections of these chronic viral hepatitis strains occurred in 2022. Therefore, as the demand for effective vaccination solutions increases to combat the rising number of hepatitis cases, there is a stronger emphasis on developing and distributing vaccines. This heightened focus on prevention and public health drives investment and innovation in the segment.

Government initiatives play a crucial role in driving the preventive vaccines market by promoting vaccination programs, funding research, and implementing public health policies. Governments often launch vaccination campaigns, provide subsidies, and establish immunization guidelines to enhance public access to vaccines. For instance, in June 2024, Gavi unveiled new vaccination initiatives targeting preventive measures against Ebola, routine multivalent meningitis, human rabies, and the hepatitis B birth dose. As per the same source, Gavi is extending its support to lower-income nations, facilitating the routine administration of the human rabies vaccine for post-exposure prophylaxis alongside the multivalent meningococcal conjugate and hepatitis B birth dose vaccines.

Therefore, the segment is expected to grow over the forecast period due to factors such as the rising burden of hepatitis A, B, and C and increasing government initiatives to boost the preventive vaccines for hepatitis.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

The preventive vaccines market in North America is expected to grow over the forecast period owing to factors such as the rising prevalence of infectious diseases, increasing demand for vaccines, growing geriatric population prone to develop infectious diseases, and the presence of key market players.

The rising burden of infectious diseases, such as COVID-19, drives the preventive vaccines market by significantly increasing vaccine demand. The urgent need to control widespread outbreaks accelerates vaccine development and broadens the range of available vaccines. This heightened demand leads to more significant investment in research, improved vaccine distribution, and the implementation of vaccination mandates. For instance, according to data published by the World Health Organization (WHO) in August 2024, about 7.6 million confirmed cases of COVID-19 were reported in Mexico. In addition, 222.23 million vaccine doses had been administered in the country by August 2024.

According to the same source, 711.81 million vaccine doses had been administered in the country by August 2024 in the United States. Therefore, the outbreak of infectious diseases like COVID-19 stimulates the preventive vaccines market by boosting demand, accelerating development, and expanding vaccine availability, which is expected to fuel the market's growth over the forecast period.

Increasing government focus on organizing immunization programs also contributes to the market's growth. For instance, in December 2023, Ontarians and other Canadians accessed free influenza vaccines under the Universal Influenza Immunization Program (UIIP). Ontario residents aged six months and older who work or attend school qualified for the influenza vaccine. Additionally, in February 2023, the Canadian government's immunization program advised that children should receive the polio vaccine at 2, 4, and 18 months, followed by a booster dose between the ages of 4 and 6. An extra dose of IPV can be given at six months, alongside DTap and Hib, for convenience. Therefore, government-led immunization programs drive the preventive vaccines market by expanding vaccine access, increasing public participation, and fostering investment in vaccine development, which will drive market growth in North America.

Growing funding from government and international organizations to accelerate the development of preventive vaccines in the country is also expected to boost the market's growth. For instance, according to the National Institute of Health, in March 2024, the US government allocated USD 364 million to combat hepatitis in 2023, following a USD 359 million investment in 2022. Therefore, increasing government funding for hepatitis propels the preventive vaccines market by supporting research, enhancing production capabilities, and expanding vaccination programs. Such investments foster broader vaccine availability and accessibility, ultimately strengthening global efforts to control and prevent hepatitis.

The rising focus of companies on adopting various business strategies, such as collaboration, expansion, and launches, is expected to create opportunities for the availability of preventive vaccines in the market. This is anticipated to fuel the market's growth over the forecast period. For instance, in October 2023, Pfizer received US Food and Drug Administration (FDA) approval for PENBRAYA, making it the first and only vaccine against the five most common serogroups of meningococcal disease in adolescents and young adults.

In addition, in August 2023, Pfizer received US FDA approval for ABRYSVO. This approval was for a specific use case: immunization of pregnant women between 32 and 36 weeks of gestation to protect their newborns from respiratory syncytial virus (RSV). It was the first and only US approval for a maternal vaccine to help protect infants at birth through six months of life from lower respiratory tract disease (LRTD) and severe LRTD due to RSV.

Therefore, the market is expected to grow over the forecast period due to factors such as the high incidences of infectious diseases, increasing immunization programs and campaigns, growing government funding for developing preventive vaccines, and increasing company activities.

Preventive Vaccines Industry Overview

The preventive vaccines market is fragmented and consists of several major players. A few of the major players currently dominating the market in terms of market share include GSK PLC, Johnson & Johnson Services Inc., Merck & Co., Pfizer Inc., and Sanofi.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Infectious Diseases

- 4.2.2 Innovative Technology in Vaccine Development

- 4.2.3 Increased Funding from Government and International Organizations

- 4.2.4 Increasing Government Focus on Immunization Programs

- 4.3 Market Restraints

- 4.3.1 Risk of Adverse Effects

- 4.3.2 High Cost of Vaccine Development

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Vaccine Type

- 5.1.1 Live/Attenuated Vaccines

- 5.1.2 Inactivated Vaccines

- 5.1.3 Subunit Vaccines

- 5.1.4 Toxoid Vaccines

- 5.1.5 mRNA Vaccines

- 5.1.6 Other Vaccine Types

- 5.2 By Disease Type

- 5.2.1 Pneumococcal

- 5.2.2 Poliovirus

- 5.2.3 Hepatitis

- 5.2.4 Influenza

- 5.2.5 Measles, Mumps, and Rubella (MMR)

- 5.2.6 COVID-19

- 5.2.7 Other Disease Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AstraZeneca PLC

- 6.1.2 Emergent BioSolutions Inc.

- 6.1.3 Daiichi Sankyo Company Limited

- 6.1.4 GSK plc

- 6.1.5 Johnson & Johnson Services, Inc.

- 6.1.6 Merck & Co.

- 6.1.7 Novavax Inc.

- 6.1.8 Pfizer Inc.

- 6.1.9 Sanofi

- 6.1.10 Takeda Pharmaceutical Co. Ltd