|

시장보고서

상품코드

1686538

아시아태평양의 작물 보호 화학제품 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Asia Pacific Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

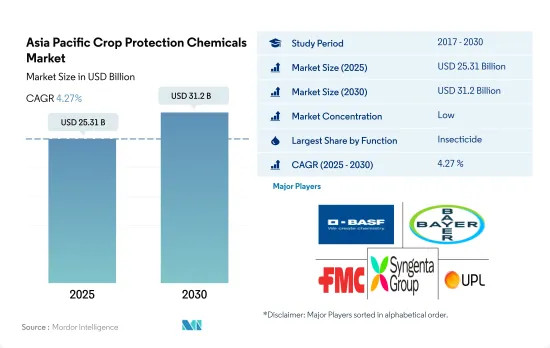

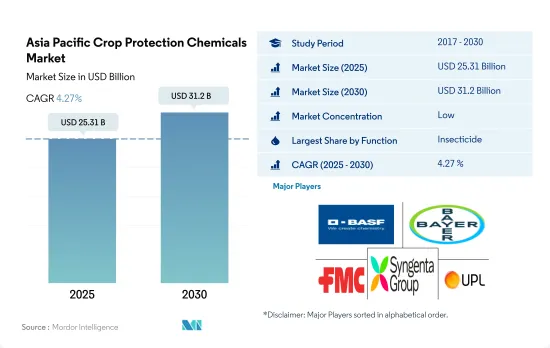

아시아태평양의 작물 보호 화학제품 시장 규모는 2025년에 253억 1,000만 달러, 2030년에는 312억 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 4.27%를 보일 것으로 예상됩니다.

해충과 잡초의 공격 증가로 인한 아시아태평양 시장에서 살충제와 제초제의 이점

- 아시아태평양의 농업은 다양성이 풍부하며 많은 국가의 경제에서 중요한 역할을 수행합니다. 이 지역은 열대에서 온대까지 폭넓은 기후를 가지고 있으며, 쌀, 콩, 밀, 다양한 과일 및 채소 재배로 유명합니다. 2022년 아시아태평양은 세계 작물 보호 화학 시장에서 금액 기준으로 24.7%의 점유율을 차지했습니다.

- 보다 양호한 수율을 달성하기 위한 작물 보호 화학물질의 사용은 이 지역의 인구 증가로 인한 식용 작물 수요 증가에 의해 장려됩니다. 동시에, 기술의 진보는 농업의 방식을 바꾸고 해충 방제의 새로운 기술은 작물과 농가에게 큰 이익을 가져다줍니다.

- 살충제는 아시아태평양의 작물 보호 화학 시장에서 50.8%로 가장 높은 점유율을 차지하고 있습니다. 벼는 많은 지역에서 재배되는 주요 작물입니다. 그러나 다양한 해충의 피해를 받기 쉽고, 그로 인해 수확량에 영향을 미칩니다.

- 제초제는 2022년 금액 기준으로 28.5%로 2위 점유율을 차지했습니다. 주식 작물, 상업 작물, 원예 작물에서 잡초의 해는이 지역의 농업 생산성에 큰 과제를 초래합니다. 이 지역의 경제 성장에는 과실산업이 크게 공헌하고 있기 때문에 과실잡초는 큰 경제적 손해를 초래합니다. Amaranthus retroflexus(Redroot pigweed)와 Echinochloa crus-galli(Barnyard grass)는 지역 과일 나무 산업에서 가장 흔한 잡초입니다.

- 식량 안보에 대한 관심 증가와 다양한 시장 개척으로 농가는 작물에 대한 해충의 영향을 최소화하면서 효율적이고 지속 가능한 식량 생산을 실시했습니다. 이것이 시장을 견인하고 있으며, 예측 기간 중(2023-2029년)의 CAGR은 4.5%를 나타낼 것으로 예측되고 있습니다.

해충, 질병, 잡초로부터 농작물을 보호하기 위한 작물 보호 화학물질 소비 증가로 시장은 성장하고 있다.

- 2022년 아시아태평양은 세계 살충제 시장에서 금액 기준으로 24.7% 시장 점유율을 차지했습니다. 이 지역의 살충제 분야는 매우 중요하며 끊임없이 진화하고 있습니다. 여러 국가에서 생산적이고 지속 가능한 농업 관행을 촉진하는 데 중요한 역할을 수행하고 있습니다. 지난 일정 기간 동안 아시아태평양의 살충제 시장은 일관된 성장을 이루었고 CAGR은 5.5%였습니다.

- 중국과 인도를 비롯한 아시아태평양 국가에서는 다양한 농업 경관을 위해 작물 보호 화학제품의 사용량이 증가하고 있으며 병해충에 약한 작물도 있습니다. 집약적인 작물 재배와 단일 재배의 보급도 병해충의 번식에 호조건을 부여하고 있습니다. 많은 인구를 유지하기 위해 식량 안보 확보가 최우선 과제가 되고, 작물의 수율을 지키고, 병해충에 의한 손실을 최소한으로 억제할 필요성이 높아져, 그 결과, 작물 보호 화학제품에의 의존도가 높아지고 있습니다.

- 또한 현대적 접근법의 도입과 경작지 확대로 농업 확대도 시장의 성장을 가져옵니다. 이 지역의 농지 면적은 2019년 6억 2,450만 ha에서 2022년 6억 6,220만 ha로 확대됐습니다. 농업 활동이 확대됨에 따라 해충으로부터 작물을 보호하는 효율적인 솔루션에 대한 수요도 확대되고 있습니다.

- 예측 기간 중(2023-2029년) 태국은 금액 기준으로 CAGR 6.8%로 이 지역에서 가장 빠른 성장률을 보일 것으로 예측되고 있습니다. 이 급성장은 해충 위협 증가와 작물 손실 증가로 인한 농민들의 작물 보호 화학물질 사용 증가가 예상되기 때문입니다.

아시아태평양의 작물 보호 화학제품 시장 동향

해충 증가로 작물 보호 화학제품 사용량 증가

- 아시아태평양의 2022년 작물 보호 화학물질의 평균 소비량은 농지 1헥타르당 2.9kg이었습니다. 살균제는 화학작물 보호 화학물질 중 가장 많이 사용되었으며 평균 소비량은 헥타르당 10.6kg에 달했습니다. 이것은 곰팡이 병원체가 농업 생산에 큰 위협을 초래하여 살균제의 필요성이 증가하고 있음을 보여줍니다. 벼 볶음병의 원인균은 MBI-D 살균제에 대한 내성을 획득하고 있으며, 살균제 살포의 필요성이 높아지고 있습니다.

- 살균제의 다음은 제초제로, 2022년의 1헥타르당의 살포량은 10.4kg에 달했습니다. 헥타르당 제초제 사용량 증가는 농업 인구 고령화, 노동력 부족, 농지 확대 등 다양한 요인에 기인합니다. 이러한 요인은 수작업 제초에서 벼와 콩과 같은 중요한 작물에서 효과적인 잡초 관리를 위해 제초제 사용으로의 전환을 촉진합니다. 또한 잡초가 기존 제초제에 대한 내성을 획득하고 있기 때문에 잡초 관리는 매우 어려워지고, 그 결과 제초제의 살포량이 증가하고 있습니다.

- 살충제는 아시아태평양 국가에서는 작물 보호 화학제품 중에서 세 번째로 살포량이 많아 2022년 1헥타르당 살포량은 8kg이 됩니다. 지구 온난화와 기후 변화는 다양한 메커니즘으로 해충을 증가시킴으로써 농업 생산에 다양한 과제를 야기하고 있습니다. 예를 들어 벼의 주요 해충인 히메토비운카(Nilaparvata lugens)는 아시아의 일부에서 기온 상승에 반응하여 개체수가 증가하고 분포가 확대되는 것으로 관찰되고 있습니다. 마찬가지로, 살선충제와 살연체 동물제의 사용은 농부들 사이의 장점에 대한 인식이 높아지고 필요성이 증가함에 따라 증가하고 있습니다.

시펠메트린의 가용성과 수요가 제한되어 아시아태평양 시장에서 유효 성분의 가격이 상승하고 있습니다.

- 시펠메트린은 비늘눈, 칼집목, 쌍방목, 반선목 등 폭넓은 해충에 유효한 합성 피레스로이드계 살충제로서 이 지역에서 주로 사용되고 있습니다. 인도, 중국, 베트남과 같은 국가에서는 다양한 작물의 해충 방제에 주로 시펠 메트린이 사용됩니다. 특히 중국과 베트남은 시펠메트린의 주요 수입국입니다. 2022년 현재 유효성분 가격은 1톤당 21,037.7달러로 상승했으며 2017년 이후 21.1%의 현저한 상승을 반영하고 있습니다. 이 가격 상승은 사탕수수, 면화, 과일, 야채 등의 작물에서 시펠메트린 수요 증가로 인한 것입니다.

- 아트라진은 이 지역에서 널리 이용되는 제초제로서 중요한 위치를 차지하고 있으며, 트리아진 클래스의 염소계 제초제로 분류됩니다. 아틀라진은 콩나물, 옥수수, 사탕수수, 잔디와 같은 작물의 1학년 활엽 잡초와 벼과 잡초를 효과적으로 방제합니다. 이 활성 성분의 가격은 다양한 작물에 대한 광범위한 적용으로 전년 대비 일관된 성장을 보여줍니다. 2022년 최신 기록에서 가격은 1톤당 13,817.2달러로 2017년부터 29.8%의 상당한 상승세를 보였습니다.

- Mancozeb은 접촉 살균제이며, 곡물, 과일, 야채, 콩류와 같은 광범위한 균류 병해를 효과적으로 표적으로 하는 다목적 응용 분야로 알려져 있습니다. 이 활성 성분의 가격은 현재 1톤당 7,776.9달러이며 아시아태평양 국가에서 널리 사용되는 주요 살균제 활성 성분 중 하나입니다.

- 유효 성분의 가격은 원료 비용의 상승, 수입 관세, 물류비의 상승으로 해마다 상승하고 있습니다.

아시아태평양 작물 보호 화학제품 산업 개요

아시아태평양의 작물보호화학 시장은 세분화되어 상위 5개사에서 33.97%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. BASF SE, Bayer AG, FMC Corporation, Syngenta Group and UPL Limited(sorted alphabetically).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 작물 보호 화학제품 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 미얀마

- 파키스탄

- 필리핀

- 태국

- 베트남

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 기능

- 살균제

- 제초제

- 살충제

- 살연체 동물제

- 살선충제

- 사용 모드

- 약제 살포

- 잎면 살포

- 훈증

- 종자 처리

- 토양처리

- 작물 유형

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 유량씨

- 잔디 및 관상용

- 국가

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 미얀마

- 파키스탄

- 필리핀

- 태국

- 베트남

- 기타 아시아태평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Rainbow Agro

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Asia Pacific Crop Protection Chemicals Market size is estimated at 25.31 billion USD in 2025, and is expected to reach 31.2 billion USD by 2030, growing at a CAGR of 4.27% during the forecast period (2025-2030).

Dominance of insecticides and herbicides in the Asia-Pacific market due to a rise in pest and weed attacks

- Agriculture in Asia-Pacific is diverse and plays a significant role in the economies of many countries. The region has a wide range of climates, from tropical to temperate, and is known for the cultivation of rice, soybeans, wheat, and various fruits and vegetables. In 2022, Asia-Pacific occupied a share of 24.7% by value of the global crop protection chemicals market.

- The use of pesticides in order to achieve better yields is encouraged by the increasing demand for food crops due to population growth in the region. At the same time, technological advancements have changed the way farming is done, and new technologies in pest control are benefiting crops and farmers a great deal.

- Insecticides occupied the highest share of 50.8% in the Asia-Pacific crop protection chemicals market. Rice is the major crop cultivated across many regional countries. However, it is also susceptible to various pests, which have led to severe damage to the crop and, subsequently, its yield.

- Herbicides occupied the second-largest share of 28.5% by value in 2022. Weed attacks in staple, commercial, and horticultural crops pose a significant challenge to the region's agricultural productivity. As there is a significant contribution by the fruit industry to the region's economic growth, fruit weeds cause substantial economic damage. Amaranthus retroflexus (Redroot pigweed) and Echinochloa crus-galli (Barnyard grass) are the most common weeds in the regional fruit industry.

- Increased concerns for food security and various market developments have facilitated the efficient and sustainable production of food by farmers while minimizing the impact of pests on their crops. This has driven the market, which is anticipated to register a CAGR of 4.5% during the forecast period (2023-2029).

The market is growing due to the rising consumption of pesticides to protect crops from pests, diseases, and weeds

- In 2022, Asia-Pacific held a market share of 24.7% by value of the global insecticide market. The pesticide segment in the region is of great importance and is constantly evolving. It plays a vital role in promoting productive and sustainable agricultural practices in multiple countries. During the historical period, the pesticide market in Asia-Pacific experienced consistent growth, with a CAGR of 5.5%.

- Asia-Pacific countries like China and India, along with other countries, experience increased pesticide usage due to their varied agricultural landscape, making some crops more vulnerable to pests and diseases. The prevalence of intensive cropping practices and monocultures also contributes to the favorable conditions for pests to thrive. With substantial populations to sustain, ensuring food security becomes a top priority, leading to a heightened need to protect crop yields and minimize losses caused by pests, thus resulting in a greater reliance on pesticides.

- The market is also experiencing growth due to the expansion of agriculture, with the adoption of modern practices and the expansion of cultivated land. The region's agricultural land area grew from 624.5 million ha in 2019 to 662.2 million ha in 2022. As agricultural activities expand, the demand for efficient solutions to protect crops from pests is also growing.

- During the forecast period (2023-2029), Thailand is projected to exhibit the fastest growth rate in the region, with a CAGR of 6.8% by value. This rapid growth can be attributed to the anticipated increase in the usage of pesticides by farmers in the country due to the rising threat of pests and increasing crop losses.

Asia Pacific Crop Protection Chemicals Market Trends

Increasing pest proliferation is leading to higher application of pesticides

- The average consumption of crop protection chemicals in Asia-Pacific was 2.9 kg per hectare of agricultural land in 2022. Fungicides were the highest used among all chemical pesticides, with average consumption amounting to 10.6 kg per hectare. This indicates the significant threat posed on agricultural production by fungal pathogens, resulting in a higher need for fungicides. Fungus-causing rice blast in paddy has developed resistance to MBI-D fungicides, leading to a higher need for fungicidal applications.

- Fungicides are followed by herbicides, with a per hectare application rate of 10.4 kg per hectare in 2022. The increase in herbicide usage per hectare can be attributed to various factors, including an aging farming population, labor shortages, and the expansion of agricultural land. These factors have prompted a transition from manual weeding practices to the utilization of herbicides for effective weed management in significant crops like rice and soybeans. Weeds are also becoming very tough to manage as they are developing resistance to existing herbicides, leading to higher dosages of application.

- Insecticides are the third most applied among pesticides in Asia-Pacific countries, with a per hectare application rate of 8 kg in the year 2022. Global warming and climate change are posing various challenges to agricultural production, even by increasing the pest population through various mechanisms. For instance, the brown planthopper (Nilaparvata lugens), a major pest of rice, has been observed to increase in population and expand its distribution in response to rising temperatures in parts of Asia. Similarly, the usage of nematicides and molluscicides has been increasing amid growing awareness among farmers of their benefits, along with the increasing need.

Limited availability and demand for cypermethrin have increased the price of active ingredients in the Asia-Pacific market

- Cypermethrin is the dominant insecticide used in the region, being a synthetic pyrethroid effective against a wide range of insect pests such as Lepidoptera, Coleoptera, Diptera, and Hemiptera. Countries like India, China, and Vietnam primarily rely on cypermethrin for pest control in various crops. Notably, China and Vietnam are the major importers of cypermethrin. As of 2022, the price of the active ingredient had risen to USD 21,037.7 per metric ton, reflecting a notable increase of 21.1% since 2017. This surge in price can be attributed to the growing demand for cypermethrin in crops like sugarcane, cotton, fruits, and vegetables.

- Atrazine holds a prominent position as a widely utilized herbicide in the region, classified as a chlorinated herbicide of the triazine class. It serves as both a pre- and post-emergence herbicide, effectively controlling annual broadleaf weeds and grasses in crops like soybeans, maize, sugarcane, and turf grasses. The active ingredient's price has experienced consistent year-on-year growth due to its extensive application across various crops. As of the latest recording in 2022, the price stood at USD 13,817.2 per metric ton, marking a significant increase of 29.8% since 2017.

- Mancozeb is a contact fungicide known for its versatile application modes, effectively targeting a wide array of fungal diseases in cereal crops, fruits, vegetables, and pulses. The price of the active ingredient currently stands at USD 7,776.9 per metric ton, making it one of the principal fungicide active ingredients extensively utilized in the Asia-Pacific countries.

- The prices of active ingredients are experiencing annual increases due to the rise in raw material costs, import tariffs, and escalating logistics expenses.

Asia Pacific Crop Protection Chemicals Industry Overview

The Asia Pacific Crop Protection Chemicals Market is fragmented, with the top five companies occupying 33.97%. The major players in this market are BASF SE, Bayer AG, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 China

- 5.4.3 India

- 5.4.4 Indonesia

- 5.4.5 Japan

- 5.4.6 Myanmar

- 5.4.7 Pakistan

- 5.4.8 Philippines

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록