|

시장보고서

상품코드

1687074

중국의 엔지니어링 플라스틱 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)China Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

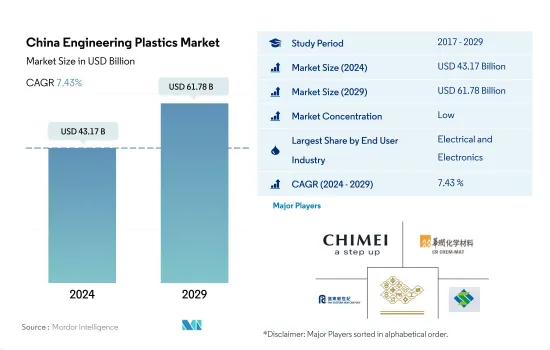

중국의 엔지니어링 플라스틱 시장 규모는 2024년에 431억 7,000만 달러에 달했습니다. 2029년에는 617억 8,000만 달러에 이를 것으로 예상되고, 예측 기간 중(2024-2029년)의 CAGR은 7.43%를 나타낼 것으로 전망됩니다.

포장 부문은 전기 및 전자산업에 수량 점유율을 빼앗깁니다.

- 엔지니어링 플라스틱의 용도는 항공우주 산업의 인테리어 벽 패널과 도어에서 단단하고 부드러운 포장까지 다양합니다. 아시아태평양의 엔지니어링 플라스틱 시장은 포장, 전기 및 전자, 자동차 산업이 견인하고 있습니다. 2022년 엔지니어링 플라스틱 시장의 수량 구성비는 포장용 전기전자산업이 약 39.65%, 전자산업이 약 35.86%였습니다.

- 2020년 중국의 엔지니어링 플라스틱 소비량은 전 세계 공급망 혼란으로 인해 수량 기준으로 전년 대비 2.88% 감소했습니다. 그러나 2021년에는 소비가 회복되었고, 2022년에는 수량으로 2.35% 증가해 안정된 성장을 이어갔습니다.

- 음료, 식수, 퍼스널케어, 가정용 케어 제품 등의 포장에 사용되는 플라스틱 병의 대량 생산으로, 이 나라에서는 포장 산업이 가장 대량의 엔지니어링 플라스틱을 소비하고 있습니다. 중국은 세계 최대의 전자상거래 시장이며, 그 점유율은 거의 50%에 달할 전망입니다. 이 나라의 전자상거래 시장 매출은 2023년 1조 4,000억 달러에서 2027년 약 2조 3,000억 달러에 이를 것으로 예측됩니다. 2022년 수지 소비량은 709만톤이었고 2029년에는 960만톤에 이를 것으로 추정됩니다. 이러한 모든 요인이 업계 소비를 밀어 올리고 예측 기간 중 CAGR은 금액 기준으로 6.47%를 나타낼 것으로 전망됩니다.

- 자동차는 중국의 엔지니어링 플라스틱 시장에서 가장 급성장하는 최종 사용자 산업이며, 예측 기간 중 CAGR은 금액 기준으로 9.40%를 나타낼 것으로 예상됩니다. 이는 폴리카보네이트, 폴리아미드, 불소 수지 등의 경량 엔지니어링 플라스틱 복합재료가 고온에서의 사용, 화학적 불활성, 내마모성, 안정된 성능을 보장하는 비용출성 등의 장점을 갖추고 있기 때문에 자동차 부품에 사용되는 수요가 증가하고 있는 것과 일치하고 있습니다.

중국의 엔지니어링 플라스틱 시장 동향

중국은 세계의 전자기기 제조 허브로 계속

- 중국은 2020년부터 2021년에 걸쳐 전기 및 전자산업의 수익이 14.5% 증가했습니다. 이 중 전기통신기기 제조업체의 생산고는 1-4월기에 전년 동기 대비 8.6% 증가를 기록했지만 휴대전화의 생산고는 전년 대비 10.9% 감소했습니다. 컴퓨터·제조업체의 생산고는 전년대비 3.9%의 성장을 기록했습니다.

- COVID-19 팬데믹 관련 혼란으로 인해 2020년 노트북과 태블릿형 컴퓨터의 생산고는 각각 31.1%와 24.5% 감소했습니다.

- 그러나 같은 기간 동안 전자와 게임에 대한 수요가 증가함에 따라 전기 및 전자 제품에 대한 수요가 증가했습니다. 2021년 중국 전자제조기업의 총이익은 전년 대비 38.9% 증가한 8,283억 위안에 달했고, 동기간 최고 성장률을 기록했습니다. 2018년 감소를 경험한 후 업계의 이익은 2019년부터 2021년까지 급속히 증가했습니다.

- 중국은 국내 산업에서 사용되는 전자기기의 85%를 국내에서 제조하고 있으며, 방위기기와 첨단기기에서 국내 제조의 필수 전자부품 비율은 30%에서 85%로 상승했습니다. 중국은 여전히 소비자용 전자기기의 중요한 세계적 제조 거점이며, 세계 주요 전자기기 제조업체가 제조 거점과 R&D 센터를 설립하도록 유치하고 있습니다. 이러한 개발은 2022년의 전자기기 생산을 밀어 올려, 이 나라의 세계 생산은 제1위가 되었습니다. 이러한 요인은 예측기간 동안 전기 및 전자산업의 생산을 촉진할 것으로 예상됩니다.

중국의 엔지니어링 플라스틱 산업의 개요

중국의 엔지니어링 플라스틱 시장은 단편화되어 상위 5개사에서 31.57%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. CHIMEI, China Resources(Holdings), Far Eastern New Century Corporation, Formosa Plastics Group and Sanfame Group(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 포장

- 수출입 동향

- 가격 동향

- 재활용 동향

- 폴리아미드(PA) 재활용 동향

- 폴리카보네이트(PC) 재활용 동향

- 폴리에틸렌 테레프탈레이트(PET) 재활용 동향

- 스티렌 공중합체(ABS 및 SAN) 재활용 동향

- 규제 프레임워크

- 중국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 산업 및 기계

- 포장

- 기타 최종 사용자 산업

- 수지 유형

- 플루오로폴리머

- 하위 수지 유형별

- 에틸렌테트라플루오로에틸렌(ETFE)

- 불소화 에틸렌-프로필렌(FEP)

- 폴리테트라플루오로에틸렌(PTFE)

- 폴리비닐플루오라이드(PVF)

- 폴리비닐리덴 플루오라이드(PVDF)

- 기타 하위 수지 유형

- 액정 폴리머(LCP)

- 폴리아미드(PA)

- 하위 수지 유형별

- 아라미드

- 폴리아미드(PA) 6

- 폴리아미드(PA) 66

- 폴리프탈아미드

- 폴리부틸렌 테레프탈레이트(PBT)

- 폴리카보네이트(PC)

- 폴리에테르 에테르 케톤(PEEK)

- 폴리에틸렌 테레프탈레이트(PET)

- 폴리이미드(PI)

- 폴리메틸 메타크릴레이트(PMMA)

- 폴리옥시메틸렌(POM)

- 스티렌 공중합체(ABS와 SAN)

- 플루오로폴리머

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Chang Chun Group

- CHIMEI

- China Petroleum & Chemical Corporation

- China Resources(Holdings) Co.,Ltd.

- Covestro AG

- Dongyue Group

- Far Eastern New Century Corporation

- Formosa Plastics Group

- Henan Energy Group Co., Ltd.

- Highsun Holding Group

- Jilin Joinature Polymer Co., Ltd.

- PetroChina Company Limited

- Sanfame Group

- Shenzhen Wote Advanced Materials Co.,Ltd.

- Zhejiang Hengyi Group Co., Ltd.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The China Engineering Plastics Market size is estimated at 43.17 billion USD in 2024, and is expected to reach 61.78 billion USD by 2029, growing at a CAGR of 7.43% during the forecast period (2024-2029).

Packaging to lose its market share by volume to the electrical and electronics industry

- Engineering plastics have applications ranging from interior wall panels and doors in the aerospace industry to rigid and flexible packaging. The Asia-Pacific engineering plastics market is led by the packaging, electrical and electronics, and automotive industries. The packaging electrical and electronics industries accounted for around 39.65% and 35.86%, respectively, of the engineering plastics market by volume in 2022.

- In 2020, China's engineering plastics consumption fell by 2.88% by volume over the previous year due to disruptions in the global supply chain. However, consumption recovered in 2021 and continued to grow steadily, increasing by 2.35% in volume in 2022.

- The packaging industry consumes the highest amounts of engineering plastics in the country due to the large-scale production of plastic bottles used in the packaging of beverages, drinking water, personal care, and household care products, among others. China is the largest e-commerce market globally, with its share amounting to almost 50%. The country's e-commerce market is projected to reach a revenue of around USD 2.3 trillion in 2027 from USD 1.4 trillion in 2023. In 2022, the industry consumed 7.09 million tons of resin, which is expected to reach 9.6 million tons by 2029. All these factors boost the industry's consumption, which is expected to record a CAGR of 6.47%, by value, during the forecast period.

- Automotive is the fastest-growing end-user industry of the Chinese engineering plastics market, expected to record a CAGR of 9.40% by revenue during the forecast period. This is in line with the industry's increasing demand for lightweight engineering plastic composites, such as polycarbonate, polyamide, and fluoropolymer, for use in vehicle components due to their benefits such as high-temperature use, chemical inertness, resistance to abrasion, and non-leaching capabilities that ensure consistent performance.

China Engineering Plastics Market Trends

China to remain a global electronics manufacturing hub

- China witnessed a 14.5% increase in the revenue of its electrical and electronics industry from 2020 to 2021. Of these, the output of telecom equipment manufacturers registered a Y-o-Y gain of 8.6% in the first four months, while mobile phone output shrank by 10.9% from the previous year. The output of computer manufacturers registered a 3.9% growth in 2020 from the previous year.

- The output of laptops and tablet computers dropped by 31.1% and 24.5%, respectively, in 2020 due to the COVID-19 pandemic-related disruptions.

- However, during the same period, the demand for electrical and electronic products increased owing to the rising demand for electronics and gaming. In 2021, the total profit of Chinese electronic manufacturing enterprises grew by 38.9% over the previous year, reaching CNY 828.3 billion, recording the highest growth rate in the given period. After experiencing a decrease in 2018, the industry's profits rose quickly from 2019 to 2021.

- China domestically manufactures 85% of the electronics used in its defense industry, and the ratio of domestically manufactured essential electronic parts in defense and high-tech equipment rose from 30% to 85%. China remains an important global manufacturing base for consumer electronics, attracting the world's major electronic producers to establish manufacturing bases and research and development centers. Such developments boosted electronics production in 2022, ranking the country first in terms of global production. Such factors are expected to drive production in the electrical and electronics industry during the forecast period.

China Engineering Plastics Industry Overview

The China Engineering Plastics Market is fragmented, with the top five companies occupying 31.57%. The major players in this market are CHIMEI, China Resources (Holdings) Co.,Ltd., Far Eastern New Century Corporation, Formosa Plastics Group and Sanfame Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 China

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Chang Chun Group

- 6.4.2 CHIMEI

- 6.4.3 China Petroleum & Chemical Corporation

- 6.4.4 China Resources (Holdings) Co.,Ltd.

- 6.4.5 Covestro AG

- 6.4.6 Dongyue Group

- 6.4.7 Far Eastern New Century Corporation

- 6.4.8 Formosa Plastics Group

- 6.4.9 Henan Energy Group Co., Ltd.

- 6.4.10 Highsun Holding Group

- 6.4.11 Jilin Joinature Polymer Co., Ltd.

- 6.4.12 PetroChina Company Limited

- 6.4.13 Sanfame Group

- 6.4.14 Shenzhen Wote Advanced Materials Co.,Ltd.

- 6.4.15 Zhejiang Hengyi Group Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms