|

시장보고서

상품코드

1907289

판지 포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Paperboard Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

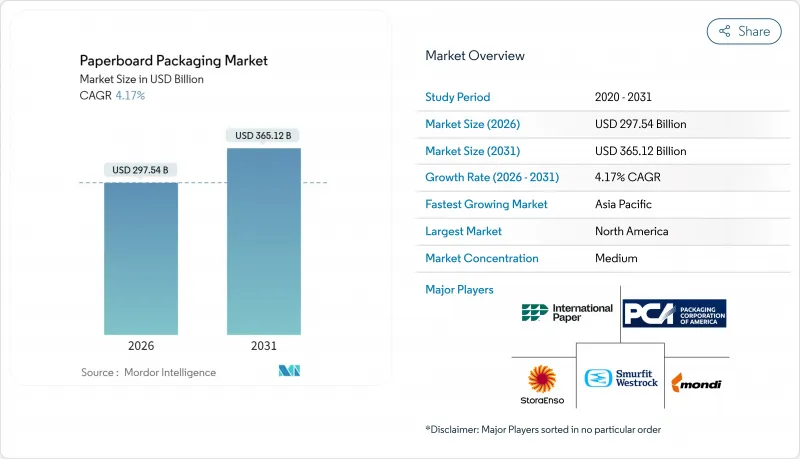

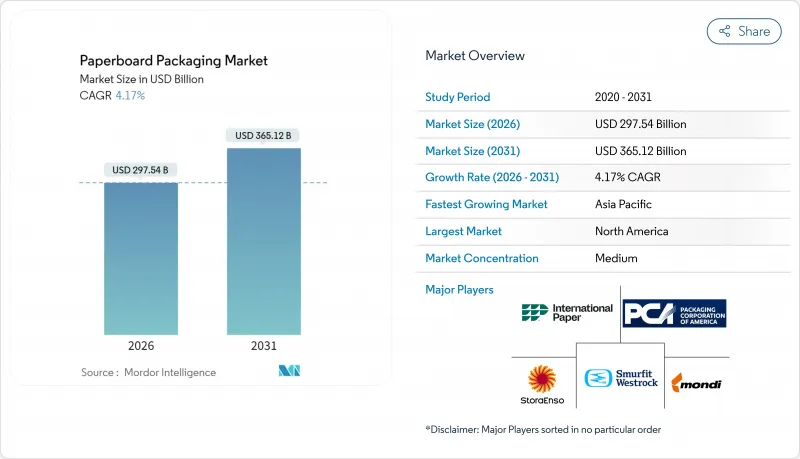

판지 포장 시장은 2025년 2,856억 3,000만 달러에서 2026년에는 2,975억 4,000만 달러로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 CAGR 4.17%로 성장할 것으로 예상되며, 2031년에는 3,651억 2,000달러에 이를 전망입니다.

전자상거래 물량 증가, 플라스틱보다 섬유를 선호하는 규제 추세, 경량화 및 디지털 변환 기술의 지속적인 개선이 종합적으로 시장 확장을 주도하고 있습니다. 재생 섬유의 우수한 비용 대비 성능은 소매업체의 순환형 공급망 구축 노력과 시너지를 발휘하여 원자재 가격 변동에도 불구하고 수요를 유지하고 있습니다. 골판지 포장은 물류 네트워크의 핵심으로 자리매김한 반면, 접이식 카톤은 프리미엄 소비재 분야에서 점유율을 확대하고 있습니다. 시장 참여자들은 에너지 및 회수 종이 가격 변동성 증가에 대응하기 위해 저비용 임업 지역의 수직 통합 및 펄프 생산 능력 확장에 투자하고 있습니다.

세계의 판지 포장 시장 동향 및 인사이트

전자상거래의 급증이 골판지 운송 수요를 주도

온라인 소매 시장 침투는 다중 접점을 견딜 수 있는 더 강력하고 치수 최적화된 운송 용기를 요구합니다. 박스 제조사들은 고성능 플루트 프로파일과 SKU 기하학에 맞춰 포장재를 설계하는 실시간 디자인 도구를 결합하여 급증하는 주문을 확보했습니다. 2025년 초 미국 포장 회사(Packaging Corporation of America)의 톤당 70달러 가격 인상은 수요-공급 균형이 긴축되었음을 보여주었다. 소비자 직거래(D2C) 모델은 외부 포장재의 브랜딩 공간 필요성을 더욱 강화하여, 변환업체들이 고화질 디지털 인쇄 모듈을 통합하도록 유도하고 있습니다. 위치 및 충격 모니터링을 지원하는 스마트 라벨 기술이 이제 골판지 라이너에 적용되어 보호 기능을 넘어선 가치를 창출하고 있습니다.

플라스틱 대체 규정이 섬유 포장을 뒷받침

유럽연합(EU)의 '포장재 및 포장 폐기물 규정'은 2030년까지 90% 재생률을 의무화하여 다층 플라스틱에서 재생 가능한 섬유 포맷으로의 전환을 가속화하고 있습니다. 북미 주들은 생산자 책임 확대(EPR) 체계를 도입 중이며, 여러 아시아태평양 시장들도 유사한 법안을 마련 중입니다. 생산자들은 분산형 차단 코팅과 PFAS 무첨가 방유 화학 기술을 통해 식품 안전성을 유지하면서 재펄프화 가능성을 확보하고 있습니다. 브랜드 소유자들은 이러한 솔루션을 활용해 대중의 지속가능성 약속을 이행하고 다가올 플라스틱 세금을 회피합니다.

산림 파괴와 섬유 조달에 대한 감시 강화

유럽연합 삼림 파괴 방지 규정 시행으로 제지 공장들은 2020년 12월 이후 삼림 파괴가 없는 것으로 검증된 구획까지 목재의 출처를 추적해야 하며, 이는 감사 비용을 증가시키고 규정 미준수 공급망에 수입 금지 조치를 초래합니다. 다국적 기업들은 동일한 규정을 전 세계적으로 확대 적용해 규정 준수를 효과적으로 글로벌화하고 있습니다. 소규모 가공업체들은 불균형적인 행정적 부담에 직면하여 인증 풀링 또는 플랜테이션 소유주와의 수직적 파트너십으로 전환하고 있습니다. 인증 목재에 지불되는 프리미엄은 특정 등급의 손익분기점을 높여, 관리연쇄(CoC) 시스템이 성숙할 때까지 마진을 압박합니다.

부문 분석

재생 섬유는 광범위한 도로변 수거 네트워크와 성숙한 탈잉크 기술에 힘입어 2025년 판지 포장 시장의 72.10% 점유율을 차지했습니다. 이 부문은 순환성 목표와 연계된 규제 크레딧으로 인해 신규 등급을 앞지르며 6.65%의 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. 브랜드 소유자들이 대량 SKU에 대해 최소한의 소비 후 재생 함량을 의무화함에 따라 재생 등급의 판지 포장 시장 규모는 확대될 것으로 예상됩니다. 화장품 선물 상자나 의약품 블리스터 카드처럼 완벽한 시각적 품질이나 높은 습윤 강도가 필수적인 분야에서는 신규 섬유가 여전히 중요합니다.

저비용 플랜테이션 임업에 대한 지속적인 투자가 재생 원료의 주도적 위치를 공고히 합니다. 수자노의 신규 브라질 유칼립투스 단지는 연간 255만 톤의 고휘도 펄프를 공급하며, 이는 회수된 원료와 완벽하게 혼합되어 전 세계 제지 공장의 평균 원료 비용을 낮춥니다. FSC 및 PEFC 인증은 재생 시트를 더욱 차별화하여, 변환업체가 환경 의식이 높은 소비자에게 호소하는 탄소 중립 주장을 추가할 수 있게 합니다. 이러한 공급 안정성과 브랜드 영향력은 재생 섬유를 판지 포장 시장의 최전선에 위치시킵니다.

골판지 상자는 옴니채널 소매와 연계된 배송 빈도 급증에 힘입어 2025년 매출 점유율 42.10%를 기록했습니다. 내장된 방습 기능과 내충격성 마이크로 플루트는 자동 분류 시스템을 최소한의 손상으로 통과할 수 있게 하여 필수성을 강화합니다. 폴딩 카톤은 톤수 기준 규모는 작지만, 고급 그래픽 구현 능력이 프리미엄 식품 및 개인용품 포장과 부합하며 가장 빠른 5.55% CAGR을 약속합니다. 폴딩 카톤의 판지 포장 시장 규모는 선명한 인쇄와 향상된 재생성을 결합한 선반 준비형 포장 수요와 함께 확대될 전망입니다.

혁신 측면에서는 그라이프(Greif)의 엔비로랩(EnviroRAP™)이 라미네이트 메일러를 대체하면서도 가정용 재생성을 유지하는 단일 소재 포장 방식을 선보입니다. 디지털 골판지 제조기의 병행 발전으로 변환업체는 인쇄 속도로 가변 데이터를 인쇄할 수 있어 지역별 명절 테마나 인플루언서 협업을 지원합니다. 이러한 유연성은 골판지 솔루션을 판지 포장 시장 내에서 차별화하며 유통의 주력 솔루션으로서의 선도적 위치를 유지합니다.

지역별 분석

북미는 통합된 재생 섬유 네트워크와 주 차원의 플라스틱 감축 의무화 정책으로 인해 2025년 매출 점유율 38.55%를 기록하며 우위를 점했습니다. 이러한 정책은 변환 업체들이 가정용 재생 솔루션으로 전환하도록 유도하고 있습니다. 패키징 코퍼레이션 오브 아메리카(PCA)의 18억 달러 규모 컨테이너보드 인수 거래는 지역 생산 역량을 강화하며 규모의 경제를 활용하는 산업 통합을 입증합니다. 소매업체의 당일 배송 서비스는 적정 크기의 골판지 운송용기 수요를 추가로 촉진하여, 에너지 비용 상승이라는 역풍에도 불구하고 판지 포장 시장이 중간 단일자리 수 성장률을 유지하는 데 기여합니다.

아시아태평양 지역은 도시 가구의 포장된 필수품 및 간편식 구매 증가로 2031년까지 연평균 6.78% 성장률을 기록하며 가장 빠르게 확장되는 시장입니다. 중국 수출 주문은 섬유 기반 운송용 포장재를 점점 더 요구하는 반면, 베트남 현지 산업은 2026년까지 35억 달러 규모의 포장 수익을 목표로 합니다. 지역 정부들은 새로운 폐기물 지침에 순환경제 조항을 포함시켜 재생 시트 수입업체에 관세 혜택을 부여하고 있습니다. 이러한 정책적 수단과 저비용 노동력, 확대되는 온라인 소매가 결합되어 아시아태평양 지역을 판지 포장 시장의 성장 동력으로 만들고 있습니다.

유럽은 재생성과 조달 기준을 강화하는 PPWR(플라스틱 포장재 규정) 및 EUDR(유럽 플라스틱 폐기물 규정)과 같은 규제를 바탕으로 소재 혁신을 지속하고 있습니다. 사피(Sappi)의 5억 유로(5억 8,773만 달러) 규모 기계 업그레이드는 경량 코팅 용량 증대를 가져왔으며, 몬디(Mondi)의 인수 행보는 소비재 클러스터 전반에 걸친 접이식 카톤 시장 점유율 확대를 이끌었다. 높은 회수율과 소비자의 친환경 라벨 수용성은 견고한 기반을 유지하지만, 부진한 거시적 수요는 생산량 증가를 억제하고 있습니다. 그럼에도 엄격한 규정 준수 장벽은 판지 포장 시장 내 기존 업체들에게 유리한 경쟁 우위를 형성합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전자상거래 급증으로 인한 골판지 운송 수요 증가

- 플라스틱 대체 규제로 인한 섬유 포장재 선호

- 경량화 기술에 의한 물류 비용 절감

- 아시아태평양 포장 식품 및 음료의 급속한 성장

- AI 기반 주문형 맞춤 인쇄

- 라틴아메리카 유칼립투스 펄프 붐으로 인한 원목 섬유 원가 하락

- 시장 성장 억제요인

- 산림 파괴 및 섬유 원료 조달에 대한 감시 강화

- 재생지 및 에너지 비용의 변동성

- 브랜드 소유자에 의한 지속가능성에 관한 공약 후퇴

- 유연성 있는 플라스틱 파우치 시장 점유율 잠식

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체 제품 및 서비스의 위협

- 경쟁 기업간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

- 기술의 전망

- 규제 상황

제5장 시장 규모와 성장 예측

- 원재료별

- 버진 섬유

- 재생 섬유

- 제품 유형별

- 접이식 카톤

- 골판지 상자

- 경질 박스

- 기타 제품 유형

- 포장 형태별

- 1차 포장

- 2차 포장

- 운송/전자상거래 배송

- 최종 사용자 업계별

- 식품

- 음료

- 헬스케어

- 퍼스널케어 및 화장품

- 가정용품

- 전기 및 전자 기기

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 베트남

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향과 발전

- 시장 점유율 분석

- 기업 프로파일

- International Paper Company

- Smurfit WestRock

- Mondi plc

- Packaging Corporation of America

- Stora Enso Oyj

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Rengo Co., Ltd.

- Metsa Board Oyj

- Graphic Packaging Holding Company

- Cascades Inc.

- Sonoco Products Company

- Nine Dragons Paper(Holdings) Ltd.

- Georgia-Pacific LLC

- Klabin SA

- Sappi Limited

- Mayr-Melnhof Karton AG

- Huhtamaki Oyj

- Visy Industries Holdings Pty Ltd.

- Seaboard Folding Box Company Inc.

- Clearwater Paper Corporation

- ITC Limited

제7장 시장 기회와 장래의 전망

HBR 26.02.04The Paperboard Packaging market is expected to grow from USD 285.63 billion in 2025 to USD 297.54 billion in 2026 and is forecast to reach USD 365.12 billion by 2031 at 4.17% CAGR over 2026-2031.

Rising e-commerce volumes, regulatory momentum favoring fiber over plastic, and continuous improvements in lightweighting and digital converting technologies collectively propel expansion. Recycled fiber's strong cost-to-performance profile complements retailer commitments to circular supply chains, sustaining demand despite raw-material cost swings. Corrugated formats remain the backbone of fulfillment networks, while folding cartons gain ground in premium consumer categories. Market participants counter mounting energy and recovered-paper price volatility by investing in vertical integration and pulp capacity in low-cost forestry regions.

Global Paperboard Packaging Market Trends and Insights

E-commerce Surge Boosting Corrugated-Shipping Demand

Online retail penetration requires stronger, dimension-optimized shipping containers that withstand multiple touchpoints. Box producers captured surging orders by pairing high-performance flute profiles with real-time design tools that tailor packaging to SKU geometry. Packaging Corporation of America's USD 70-per-ton price increase in early 2025 illustrated a tight demand-supply balance. Direct-to-consumer models further reinforce the need for branding space on outer packs, incentivizing converters to integrate high-graphics digital print modules. Smart-label technologies supporting location and shock monitoring now ship on corrugated liners, creating value beyond protection.

Plastic-Substitution Regulations Favor Fiber Packaging

The European Union's Packaging and Packaging Waste Regulation mandates 90% recyclability by 2030, accelerating the shift from multilayer plastics toward recyclable fiber formats. North American states replicate extended-producer-responsibility frameworks, while several Asia-Pacific markets draft similar statutes. Producers respond with dispersion-based barrier coatings and PFAS-free grease-proof chemistries that safeguard food while maintaining repulpability. Brand owners leverage these solutions to meet public sustainability pledges and evade upcoming plastic taxes.

Deforestation and Fiber-Sourcing Scrutiny

Implementation of the European Union Deforestation Regulation compels mills to trace wood back to plots verified as deforestation-free after December 2020, adding auditing costs and exposing non-compliant supply chains to import bans. Multinationals extend the same protocols worldwide, effectively globalizing compliance. Smaller converters face disproportionate administrative burdens, nudging them toward certification pooling or vertical partnerships with plantation owners. Premiums paid for certified logs increase the break-even point for certain grades, compressing margins until chain-of-custody systems mature.

Other drivers and restraints analyzed in the detailed report include:

- Light-Weighting Innovations Lowering Logistics Cost

- Rapid Growth of Packaged F&B in Asia-Pacific

- Volatile Recovered-Paper and Energy Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fiber secured a 72.10% share of the paperboard packaging market in 2025, underpinned by extensive curbside collection networks and maturing de-inking technologies. This segment is also projected to clock a 6.65% CAGR, outpacing virgin grades due to regulatory credits linked to circularity goals. The paperboard packaging market size for recycled grades is forecast to widen as brand owners mandate minimum post-consumer content for high-volume SKUs. Virgin fiber retains relevance where impeccable visual quality or high wet-strength is mandatory, such as cosmetics gift boxes and pharmaceutical blister cards.

Continuous investments in low-cost plantation forestry bolster recycled leadership. Suzano's new Brazilian eucalyptus complex provides 2.55 million t/year of high-brightness pulp that blends seamlessly with recovered streams, lowering average furnish costs for global mills. Certification through FSC and PEFC further differentiates recycled sheets, enabling converters to add carbon-neutral claims that resonate with eco-conscious consumers. Resulting supply security and branding leverage keep recycled fiber at the forefront of the paperboard packaging market.

Corrugated boxes captured 42.10% revenue share in 2025, propelled by shipment frequency spikes tied to omnichannel retail. Embedded moisture barriers and crush-resistant micro-flutes allow these boxes to traverse automated sortation systems with minimal damage, reinforcing their indispensability. Folding cartons, though smaller in tonnage, promise the fastest 5.55% CAGR, as high-graphics capabilities align with premium food and personal-care placement. The paperboard packaging market size for folding cartons is projected to expand alongside demand for shelf-ready packs that combine vivid print with easier recyclability.

On the innovation front, Greif's EnviroRAP(TM) showcases mono-material wrap formats that replace laminated mailers while retaining curbside recyclability. Parallel progress in digital corrugators lets converters print variable data at press speed, supporting localized holiday themes or influencer collaborations. Such flexibility differentiates corrugated solutions within the paperboard packaging market and sustains their lead as the workhorse of distribution.

The Paperboard Packaging Market Report is Segmented by Raw Material Source (Virgin Fibre, and Recycled Fibre), Product Type (Folding Cartons, Corrugated Boxes, and More), Packaging Format (Primary Packaging, Secondary Packaging, and More), End-User Industry (Food, Beverage, Healthcare, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.55% revenue share in 2025, buoyed by integrated recovered-fiber networks and state-level plastic-reduction mandates that steer converters toward curbside-recyclable solutions. Packaging Corporation of America's USD 1.8 billion containerboard acquisition bolsters regional capacity, evidencing consolidation that harnesses scale efficiencies. Retailers' same-day delivery services further stimulate demand for right-sized corrugated shippers, helping the paperboard packaging market sustain mid-single-digit growth despite energy-cost headwinds.

Asia-Pacific represents the fastest-expanding arena, clocking a 6.78% CAGR through 2031 as urban households buy more packaged staples and quick-service meals. China's export orders increasingly specify fiber-based transit wraps, while Vietnam's local industry eyes USD 3.5 billion in packaging revenue by 2026. Regional governments embed circular-economy clauses in new waste directives, granting tariff concessions to importers of recycled sheets. These policy levers, coupled with low-cost labor and expanding online retail, turn Asia-Pacific into the growth engine of the paperboard packaging market.

Europe sustains material innovations underpinned by regulations such as the PPWR and the EUDR, which tighten recyclability and sourcing standards. Sappi's EUR 500 million(USD 587.73 million) machine upgrade enhances lightweight coated capacity, while Mondi's acquisition spree widens folding-carton footprints across consumer-goods clusters. High recovery rates and consumer receptiveness to eco-labels maintain a robust baseline, although sluggish macro demand tempers tonnage growth. Still, stringent compliance hurdles create a moat that favors established players inside the paperboard packaging market.

- International Paper Company

- Smurfit WestRock

- Mondi plc

- Packaging Corporation of America

- Stora Enso Oyj

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Rengo Co., Ltd.

- Metsa Board Oyj

- Graphic Packaging Holding Company

- Cascades Inc.

- Sonoco Products Company

- Nine Dragons Paper (Holdings) Ltd.

- Georgia-Pacific LLC

- Klabin S.A.

- Sappi Limited

- Mayr-Melnhof Karton AG

- Huhtamaki Oyj

- Visy Industries Holdings Pty Ltd.

- Seaboard Folding Box Company Inc.

- Clearwater Paper Corporation

- ITC Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce surge boosting corrugated-shipping demand

- 4.2.2 Plastic-substitution regulations favor fibre packaging

- 4.2.3 Light-weighting innovations lowering logistics cost

- 4.2.4 Rapid growth of packaged F&B in Asia-Pacific

- 4.2.5 AI-enabled on-demand custom printing

- 4.2.6 LatAm eucalyptus pulp boom lowering virgin-fibre cost

- 4.3 Market Restraints

- 4.3.1 Deforestation and fibre-sourcing scrutiny

- 4.3.2 Volatile recovered-paper and energy costs

- 4.3.3 Brand-owner pull-back on sustainability pledges

- 4.3.4 Flexible plastic pouches eroding share

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competitive Rivalry

- 4.6 The Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Regulatory Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Raw Material Source

- 5.1.1 Virgin Fibre

- 5.1.2 Recycled Fibre

- 5.2 By Product Type

- 5.2.1 Folding Cartons

- 5.2.2 Corrugated Boxes

- 5.2.3 Rigid Boxes

- 5.2.4 Other Product types

- 5.3 By Packaging Format

- 5.3.1 Primary Packaging

- 5.3.2 Secondary Packaging

- 5.3.3 Transit / E-commerce Shipping

- 5.4 By End-user Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Household Care

- 5.4.6 Electrical and Electronics

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Vietnam

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit WestRock

- 6.4.3 Mondi plc

- 6.4.4 Packaging Corporation of America

- 6.4.5 Stora Enso Oyj

- 6.4.6 Oji Holdings Corporation

- 6.4.7 Nippon Paper Industries Co., Ltd.

- 6.4.8 Rengo Co., Ltd.

- 6.4.9 Metsa Board Oyj

- 6.4.10 Graphic Packaging Holding Company

- 6.4.11 Cascades Inc.

- 6.4.12 Sonoco Products Company

- 6.4.13 Nine Dragons Paper (Holdings) Ltd.

- 6.4.14 Georgia-Pacific LLC

- 6.4.15 Klabin S.A.

- 6.4.16 Sappi Limited

- 6.4.17 Mayr-Melnhof Karton AG

- 6.4.18 Huhtamaki Oyj

- 6.4.19 Visy Industries Holdings Pty Ltd.

- 6.4.20 Seaboard Folding Box Company Inc.

- 6.4.21 Clearwater Paper Corporation

- 6.4.22 ITC Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment