|

시장보고서

상품코드

1687161

유럽의 금속캔 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

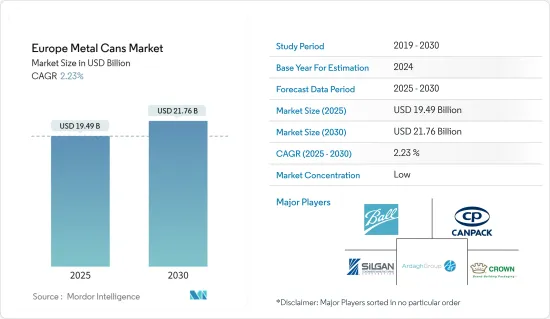

유럽의 금속캔 시장 규모는 2025년에 194억 9,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 2.23%로 성장할 전망이며, 2030년에는 217억 6,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 식음료 부문의 견조한 유럽 수요가 금속캔 시장을 견인합니다. 탄산음료, 맥주, 에너지음료, 수프, 채소와 같은 캔 식품 포장에 널리 이용되는 금속캔은 보존기간 연장, 빛과 공기로부터의 보호, 운송의 용이함 등의 이점을 자랑합니다다. 편리한 조리된 식품 및 음료의 인기가 높아지는 가운데, 이 부문의 꾸준한 성장은 여전히 강력합니다.

- 지속가능한 포장에 대한 수요가 높아지면서 시장 확대의 원동력이 되고 있습니다. 알루미늄 캔은 재활용성이 높고 플라스틱 폐기물을 억제하려는 소비자와 규제 당국의 움직임에 공감하고 있습니다. 알루미늄 캔의 재활용률이 세계에서 가장 높은 나라 중 하나인 유럽에서는 알루미늄 캔은 환경 기준의 유지를 목표로 하는 기업에 있어서 최선의 선택지가 되고 있습니다. 게다가 포장 폐기물이나 지속 가능성에 관한 유럽의 엄격한 규제는, 기업을 에코 프렌들리 솔루션으로 향하게 해, 금속캔 시장을 강화하고 있습니다.

- 지속가능성 뿐만 아니라 고급포장에 대한 축족도 현저합니다. 브랜드는 그 실용성과 마케팅 툴로서 금속캔을 활용하고 있습니다. 인쇄와 디자인의 진보 덕분에 브랜드는 선반에서 주목받는 시각적으로 인상적인 캔을 만들 수 있습니다. 이것은 특히 음료 부문에서 현저하며, 눈길을 끄는 캔은 제품의 시인성을 높여 브랜드의 ID 확인을 전달합니다. 덧붙여, 건강 지향이 강한, 레디투 드링크 음료의 동향이 높아지고 있는 것도, 금속캔의 수요를 높이고 있습니다.

- Ardagh Group, Ball Corporation, Crown Holdings와 같은 유럽 제조업체들은 금속캔 생산과 유통을 독점하고 있습니다. 이들 기업은 주로 알루미늄과 철강 등의 원료를 세계 공급업체로부터 조달하고 완제품을 국제시장에서 거래하고 있습니다. 유럽은 주로 음료 산업으로부터의 수요에 의해 금속캔의 수출입의 중요한 허브가 되고 있습니다.

- 그러나 유럽의 금속캔 시장은 불안정한 원료 가격이나 페트병이나 카톤과 같은 대체품과의 엄격한 경쟁 등의 과제에 임하고 있습니다. 알루미늄 제조에는 에너지 집약적인 성질이 있기 때문에 환경에 대한 우려가 있습니다. 유럽의 강력한 재활용 인프라와 지속 가능하고 편리한 고급 포장에 대한 꾸준한 수요는 시장의 지속적인 성장에 좋은 징조입니다.

유럽의 금속캔 시장 동향

알코올 음료가 큰 성장률을 기록

- 유럽에서는 소비자의 편의성과 휴대성에 대한 선호도가 높아짐에 따라 알코올 음료 부문에서 금속캔 수요가 꾸준히 증가하고 있습니다. 캔은 유리병보다 가볍고 내구성이 있기 때문에 운송 및 보관이 용이합니다. 이 이점은 야외 이벤트나 축제, 도시 지역에서의 외출 소비에 큰 의미를 가지고 있습니다. 소비자, 특히 젊은 층이 편리성을 우선시하는 가운데, 맥주, 사이다, 레디투 드링크 칵테일 등, 캔에 든 알코올 음료의 시장은 계속 확대되고 있습니다. 금속캔은 이러한 제품에 실용적인 포장 솔루션을 제공해, 유럽의 알코올 음료 시장 전체에서의 채용을 촉진하고 있습니다.

- 지속가능성에 대한 우려는 유럽의 금속캔 수요에 크게 영향을 미치고 있습니다. 환경 문제에 대한 소비자의 의식은 친환경 포장을 선호하는 경향을 강화하고 있습니다. 알루미늄 캔은 재활용이 가능하며, 이 지역은 세계적으로 가장 높은 알루미늄 재활용률을 유지하고 있습니다. 유럽 정부가 플라스틱 포장이나 폐기물 관리에 관한 규제를 강화하는 가운데, 알코올 음료 브랜드는 지속가능한 솔루션으로서 금속캔을 채용하고 있습니다. 이 변화는 친환경 제품과 포장을 원하는 소비자의 요구와 일치하며 금속캔은 생산자 및 소비자에게 유리합니다.

- 유럽에서 프리미엄화의 동향은 알코올 음료 시장에서 금속캔 수요 증가에 기여하고 있습니다. 크래프트 맥주, 하드 셀처, 고급 레디투 드링크 칵테일의 성장으로 제조사는 세련된 디자인의 고품질 알루미늄 캔을 사용하게 되었습니다. 인쇄 및 가식 기술의 향상으로 선명하고 맞춤형 포장이 가능해져 브랜드 인지도와 제품의 차별화가 높아졌습니다. 소비자가 프리미엄한 체험을 요구하는 가운데, 브랜드는 금속캔을 사용해 품질과 혁신성을 어필해, 유럽 시장의 성장을 지탱하고 있습니다.

- 유럽에서의 건강 지향 음료의 출현은 금속캔 수요에 영향을 미칩니다. 하드 셀처, 기능성 음료, 무알코올 맥주 등 저알코올, 저칼로리, 무알코올 음료가 인기를 누리고 있습니다. 그 편리성과 경량의 특성 때문에, 이러한 음료에는 금속 캔 포장이 자주 사용되고 있습니다. 건강 동향이 유럽의 알코올 음료 시장에 영향을 계속 주는 가운데, 금속캔은 이러한 신흥 제품의 효과적인 포장 솔루션으로서 기능해, 이 지역에서의 시장 존재감을 높이고 있습니다.

- 독일의 맥주 수량은 2024년 3월의 533만 6,340헥타르에서 2024년 5월에는 676만 8,340헥타르로 증가해, 포장 시장에서의 금속캔 수요를 견인하고 있습니다. 맥주 시장의 성장, 특히 봄과 여름에는 편리성, 내구성, 지속 가능성을 제공하는 포장 솔루션에 대한 요구가 높아집니다. 금속캔, 특히 알루미늄캔은 경량인 점, 재활용 가능한 점, 음료의 품질을 유지하는 능력이 있기 때문에 맥주 포장에 선호되고 있습니다.

- 독일의 맥주 수량 증가는 금속캔 수요를 지원하는 시장 동향과 일치합니다. 휴대하기 편리한 음료 포장에 대한 소비자의 기호는, 제조사와 소비자에게 있어서 캔을 효율적이고 비용대비 효과가 높은 선택사항으로 하고 있습니다. 야외 이벤트나 축제에서의 맥주 판매 증가에는 운송이나 취급 중에 제품의 무결성을 보증하는 포장 솔루션이 필요합니다. 금속캔은 이러한 요건을 효과적으로 충족시키기 때문에 독일의 맥주 제조업체나 공급업체에 있어서 주요한 선택사항이 되고 있습니다.

큰 시장 점유율을 차지하는 영국

- 영국의 금속캔 포장 시장은 계속 확대되고 있으며, 특히 음료 부문에서는 맥주, 청량 음료, 에너지 음료, 레이디 투 음료 칵테일이 성장하고 있습니다. 알루미늄 캔은 경량 특성, 재활용성, 제품 보존 능력으로 인해 많은 브랜드에서 주요 포장 옵션으로 부상해 왔습니다. 이러한 특성은, 휴대가 가능하고 친환경 포장을 요구하는 영국의 소비자의 기호와 일치하고 있습니다.

- 지속 가능한 포장에 대한 소비자 수요는 영국에서 금속캔을 채택하는 데 큰 영향을 미쳤습니다. 플라스틱 폐기물 삭감을 대상으로 한 환경 규제의 실시에 의해, 알루미늄 캔은 실행 가능한 대체품으로서 자리매김하고 있습니다. 캔의 무한한 재활용 가능성은 영국의 순환 경제 목표를 뒷받침하고 있습니다. 플라스틱 포장세나 확대 생산자 책임(EPR) 스킴을 포함한 정부의 시책이, 기업에 금속캔 포장의 채용을 재촉했습니다. 영국의 2050년까지의 순 제로 배출량 목표는 유리나 플라스틱 대체품보다 금속캔과 같은 지속가능한 포장 옵션의 시장 잠재력을 강화하고 있습니다.

- 건강과 웰빙 동향도 영국의 금속캔 포장의 상승에 영향을 미치고 있습니다. 소비자는, 저알코올, 저칼로리, 기능성 음료(하드 셀처, 콤부차, 피트니스 음료등)를 요구하게 되어 있습니다. 이러한 제품은 캔에 든 것이 많아, 소비자는 이것을 편리하고 환경을 배려하고 있다고 인식하고 있습니다. 캔의 경량성과 재활용 가능성은 지속 가능성을 지원하면서 액티브한 라이프 스타일을 보완하는 제품을 찾는 건강 지향적인 사람들에게 어필합니다. 포장은 음료의 신선도와 탄산을 유지하며, 이것은 하드 셀처나 수제 맥주와 같은 제품에 특히 중요합니다.

- 영국에서는 크래프트 맥주 운동과 알코올 음료의 프리미엄화가 고품질의 금속캔 포장에 대한 수요를 높이고 있습니다. 수제 맥주 양조장과 부티크 제조업체는 그 실용성과 혁신적인 디자인과 브랜딩을 어필하는 능력을 위해 캔을 선택하고 있습니다. 금속캔은, 디자인에 민감한 소비자에게 어필하는 선명한 커스텀 그래픽이나 상세한 아트 워크를 가능하게 합니다. 알루미늄 캔은 빛과 산소의 노출로부터 보호함으로써 수제 맥주의 품질을 유지합니다. 이러한 제품의 보존성과 디자인성의 조합에 의해, 캔은 프리미엄 음료에 선호되는 포장의 선택사항으로서 확립되어 영국에 있어서의 금속캔 시장의 성장을 지지하고 있습니다.

- 영국에서는 레드 Bull(5억 1,073만 달러), Monster(4억 4,453만 달러), Lucozade(2억 8,507만 달러) 등 주요 에너지 음료 브랜드의 소매 매출이 높기 때문에 금속캔 포장 수요가 높아지고 있습니다. 이러한 기업이 금속 캔을 선택하는 이유는, 그 편리성, 휴대성, 제품의 신선도와 탄산을 유지하는 능력이며, 외출중에서의 소비라고 하는 소비자의 기호에 맞습니다. 알루미늄 캔의 재활용 가능성도 환경 의식이 높은 소비자를 끌어들이고 있습니다. Prime이나 EuroShopper와 같은 프리미엄 브랜드와 밸류 브랜드 모두 제품의 체재를 갖추고 지속 가능성 요건을 충족시키기 위해 금속캔 포장을 채택하고 있으며, 이는 에너지 드링크 시장에서 금속캔 수요의 지속적인 성장을 보여주고 있습니다.

- 영국의 금속캔 포장 동향은 지속가능성, 편리성, 보다 건강한 음료를 요구하는 소비자 수요, 알코올 음료의 프리미엄화 등 다양한 요인의 수렴에 의해 초래되고 있습니다. 알루미늄 캔은 재활용 가능하고 효율적이며 소비자 친화적인 솔루션이기 때문에 그 인기는 다양한 음료 카테고리에서 계속 상승할 것으로 생각됩니다. 소비자의 기호가 보다 친환경적이고 편리한 포장으로 전환됨에 따라 영국의 금속캔 시장은 디자인, 기능성, 지속가능성의 혁신에 힘입어 지속적인 성장을 이룰 태세가 갖추어져 있습니다.

유럽의 금속캔 산업 개요

유럽의 금속캔 시장은 부문화되어 있으며, 여러 기업이 이 지역에서 사업을 전개하고 있습니다. 주요 기업은 Ball Corporation, Ardagh Group SA, Crown Holdings, Inc. 등입니다. 이들 기업은 다양한 전략적 대처를 통해 시장 점유율을 다투고 있습니다. M&A는 기업이 지리적 위상과 생산 능력을 확대하는 데 도움이 됩니다.

각 회사는 협력 관계를 통해 공급망 네트워크를 강화하고 시장에서의 지위를 높이고 있습니다. 제품의 혁신은 기업이 소비자의 진화하는 수요에 대응하고 시장에서의 경쟁 우위성을 유지할 수 있게 합니다. 또, 기업은 경쟁사와의 차별화를 도모하기 위해, 지속 가능성에의 대처나 기술의 진보에도 주력하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력-Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 거시 경제 요인이 시장에 미치는 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 금속 포장의 높은 재활용률

- 지속가능성에 대한 중요성 증가 및 금속캔의 높은 재활용성 부각

- 시장의 과제

- 대체 포장 솔루션의 존재

제6장 시장 세분화

- 재료 유형별

- 알루미늄

- 스틸

- 유형별

- 식품캔

- 야채

- 과일

- 반려동물 식품

- 스프 및 조미료

- 기타 식품캔(베이비 푸드, 유제품, 과일 및 야채 주스, 수산물, 고기 및 닭고기캔)

- 음료캔

- 알코올 음료

- 비알코올

- 에어로졸 캔

- 퍼스널케어 및 화장품

- 가정용 및 재택 치료

- 기타 에어로졸 캔

- 기타 캔

- 식품캔

- 국가별

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 폴란드

제7장 경쟁 구도

- 기업 프로파일

- Ball Corporation

- Ardagh Group

- Crown Holdings, Inc.

- Silgan Holdings Inc.

- CAN-PACK SA

- Massilly Holding SAS

- Tecnocap Group

- Tata Europe Ltd

- ASA Group

- Eurobox Metal Packaging

제8장 투자 분석

제9장 시장 전망

AJY 25.05.02The Europe Metal Cans Market size is estimated at USD 19.49 billion in 2025, and is expected to reach USD 21.76 billion by 2030, at a CAGR of 2.23% during the forecast period (2025-2030).

Key Highlights

- The food and beverage sector's robust European demand propels the metal cans market. Widely utilized for packaging carbonated drinks, beer, energy drinks, and canned foods like soups and vegetables, metal cans boast advantages such as extended shelf life, protection from light and air, and transport ease. With the rising popularity of convenient ready-to-eat meals and beverages, this sector's steady growth is still strong.

- A surging demand for sustainable packaging is driving the market's expansion. Aluminum cans, being highly recyclable, resonate with the mounting consumer and regulatory push to curb plastic waste. Europe, boasting one of the world's highest recycling rates for aluminum cans, positions these cans as the top choice for companies aiming to uphold environmental standards. Furthermore, stringent European regulations on packaging waste and sustainability are nudging businesses towards eco-friendly solutions, bolstering the metal cans market.

- Beyond sustainability, there's a notable pivot towards premium packaging. Brands are leveraging metal cans for their practicality and as a marketing tool. Thanks to advancements in printing and design, brands can craft visually striking cans that capture attention on shelves. This is particularly evident in the beverage sector, where eye-catching cans enhance product visibility and convey brand identity. Additionally, the rising trend of health-conscious, ready-to-drink beverages amplifies the demand for metal cans.

- European manufacturers, including Ardagh Group, Ball Corporation, and Crown Holdings, dominate the production and distribution of metal cans. These companies source raw materials from global suppliers, primarily aluminum and steel, and trade their finished products in international markets. Europe is a significant hub for importing and exporting metal cans, mainly driven by demand from the beverage industry.

- However, the European metal cans market grapples with challenges, including volatile raw material prices and stiff competition from alternatives like plastic bottles and cartons. The energy-intensive nature of aluminum manufacturing raises environmental concerns. Nevertheless, Europe's strong recycling infrastructure and a persistent demand for sustainable, convenient, and premium packaging bodes well for the market's continued growth.

Europe Metal Cans Market Trends

Alcoholic Beverages to Register Significant Growth Rate

- In Europe, the demand for metal cans in the alcoholic beverage sector has increased steadily due to consumers' growing preference for convenience and portability. Cans are lighter and more durable than glass bottles, making them easier to transport and store. This advantage is significant for outdoor events, festivals, and on-the-go consumption in urban areas. As consumers, particularly younger demographics, prioritize convenience, the market for canned alcoholic beverages, including beer, cider, and ready-to-drink cocktails, continues to expand. Metal cans provide a practical packaging solution for these products, driving their adoption across the European alcoholic beverage market.

- Sustainability concerns significantly influence the demand for metal cans in Europe. Consumer awareness of environmental issues has increased the preference for eco-friendly packaging. Aluminum cans are recyclable, and the region maintains one of the highest aluminum recycling rates globally. As European governments implement stricter regulations on plastic packaging and waste management, alcoholic beverage brands are adopting metal cans as a sustainable solution. This shift aligns with consumer demand for environmentally responsible products and packaging, making metal cans advantageous for producers and consumers.

- The premiumization trend in Europe contributes to the increased demand for metal cans in the alcoholic beverage market. The growth of craft beers, hard seltzers, and premium ready-to-drink cocktails has prompted manufacturers to use high-quality aluminum cans with refined designs. Printing and decoration technology improvements enable vibrant and customized packaging that enhances brand visibility and product differentiation. As consumers seek premium experiences, brands use metal cans to demonstrate quality and innovation, supporting European market growth.

- The emergence of health-conscious drinking in Europe affects metal can demand. Low-alcohol, low-calorie, and alcohol-free beverages, including hard seltzers, functional drinks, and alcohol-free beers, have gained popularity. Due to their convenience and lightweight properties, these beverages frequently use metal can packaging. As health trends continue to influence the European alcoholic beverage market, metal cans serve as an effective packaging solution for these emerging products, increasing their market presence in the region.

- The beer sales volume in Germany increased from 5,336.34 thousand hectoliters in March 2024 to 6,768.34 thousand hectoliters in May 2024, driving the demand for metal cans in the packaging market. The beer market growth, particularly during the spring and summer, increases the requirement for packaging solutions that provide convenience, durability, and sustainability. Metal cans, specifically aluminum cans, are preferred for beer packaging due to their lightweight nature, recyclability, and ability to preserve beverage quality.

- The increasing beer sales volumes in Germany correspond with market trends supporting metal can demand. Consumer preferences for portable and convenient beverage packaging make cans an efficient and cost-effective option for manufacturers and consumers. The increase in beer sales during outdoor events and festivals requires packaging solutions that ensure product integrity during transport and handling. Metal cans effectively meet these requirements, making them a primary choice for beer producers and suppliers in Germany.

United Kingdom to Hold Significant Market Share

- The metal can packaging market in the UK continues to expand, particularly in the beverage sector, with growth across beer, soft drinks, energy drinks, and ready-to-drink cocktails. Aluminum cans have emerged as a primary packaging option for many brands due to their lightweight properties, recyclability, and product preservation capabilities. These characteristics align with UK consumer preferences for portable and environmentally responsible packaging.

- Consumer demand for sustainable packaging has significantly influenced the adoption of metal cans in the UK. Implementing environmental regulations targeting plastic waste reduction has positioned aluminum cans as a viable alternative. The infinite recyclability of cans supports the UK's circular economy objectives. Government policies, including the Plastic Packaging Tax and Extended Producer Responsibility (EPR) schemes, have encouraged companies to adopt metal can packaging. The UK's net zero emissions target by 2050 reinforces the market potential for sustainable packaging options like metal cans over glass and plastic alternatives.

- Health and wellness trends have also influenced the rise of metal can packaging in the UK. Consumers increasingly seek low-alcohol, low-calorie, and functional beverages like hard seltzers, kombucha, and fitness-focused drinks. These products are often packaged in cans, which consumers perceive as convenient and environmentally responsible. The lightweight nature of cans, combined with their recyclability, appeals to health-conscious individuals seeking products that complement their active lifestyles while supporting sustainability. The packaging maintains beverage freshness and carbonation, which is particularly important for products like hard seltzers and craft beers.

- The craft beer movement and premiumization of alcoholic beverages in the UK have increased demand for high-quality metal can packaging. Craft breweries and boutique producers select cans for their practicality and capacity to showcase innovative designs and branding. Metal cans enable vibrant, custom graphics and detailed artwork that appeal to design-conscious consumers. Aluminum cans preserve craft beer quality by protecting against light and oxygen exposure. This combination of product preservation and design capabilities has established cans as a preferred packaging choice for premium beverages, supporting metal can market growth in the UK.

- The high retail sales revenue of major energy drink brands in the UK, including Red Bull (USD 510.73 million), Monster (USD 444.53 million), and Lucozade (USD 285.07 million), drives the demand for metal can packaging. These companies choose metal cans for their convenience, portability, and ability to maintain product freshness and carbonation, which suits consumer preferences for on-the-go consumption. The recyclability of aluminum cans also attracts environmentally conscious consumers. Both premium and value brands, such as Prime and Euro Shopper, are adopting metal can packaging to improve product presentation and meet sustainability requirements, indicating continued growth in metal can demand within the energy drink market.

- The metal can packaging trend in the UK is driven by a convergence of factors, including sustainability, convenience, consumer demand for healthier drinks, and the premiumization of alcoholic beverages. With aluminum cans offering a recyclable, efficient, and consumer-friendly solution, their popularity is likely to continue rising across various beverage categories. As consumer preferences shift toward more eco-conscious and convenient packaging, the metal can market in the UK is poised for sustained growth, fueled by design, functionality, and sustainability innovations.

Europe Metal Cans Industry Overview

The European metal cans market is fragmented, with multiple companies operating in the region. Major players include Ball Corporation, Ardagh Group S.A., Crown Holdings, Inc., and Silgan Holdings Inc. These companies compete for market share through various strategic initiatives. Mergers and acquisitions help companies expand their geographical presence and production capabilities.

Companies strengthen their supply chain networks and enhance their market position through collaborations. Product innovations enable companies to meet evolving consumer demands and maintain competitive advantages in the market. Companies also focus on sustainability initiatives and technological advancements to differentiate themselves from competitors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of Macro-economic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Sustainability Gains Importance, Metal Cans Shine with Their High Recyclability

- 5.2 Market Challenge

- 5.2.1 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By Type

- 6.2.1 Food Cans

- 6.2.1.1 Vegetables

- 6.2.1.2 Fruits

- 6.2.1.3 Pet Food

- 6.2.1.4 Soups and Condiments

- 6.2.1.5 Other Food Cans (Baby Food, Dairy, Fruit/Vegetable Juices, Seafood, and Meat and Poultry Cans)

- 6.2.2 Beverage Cans

- 6.2.2.1 Alcoholic

- 6.2.2.2 Non-Alcoholic

- 6.2.3 Aerosol Cans

- 6.2.3.1 Personal care and Cosmetics

- 6.2.3.2 Household and Homecare

- 6.2.3.3 Other Aerosol Cans

- 6.2.4 Other Cans

- 6.2.1 Food Cans

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Spain

- 6.3.5 Italy

- 6.3.6 Poland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ball Corporation

- 7.1.2 Ardagh Group

- 7.1.3 Crown Holdings, Inc.

- 7.1.4 Silgan Holdings Inc.

- 7.1.5 CAN-PACK SA

- 7.1.6 Massilly Holding SAS

- 7.1.7 Tecnocap Group

- 7.1.8 Tata Europe Ltd

- 7.1.9 ASA Group

- 7.1.10 Eurobox Metal Packaging