|

시장보고서

상품코드

1687180

인도네시아의 작물 보호 화학제품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Indonesia Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

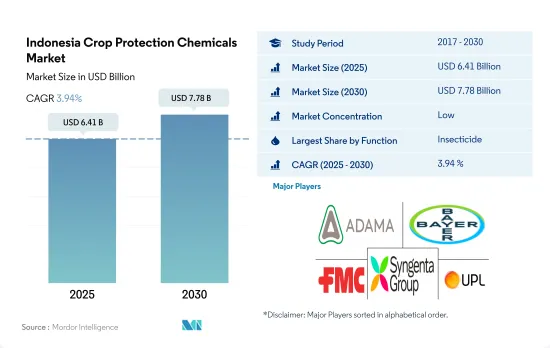

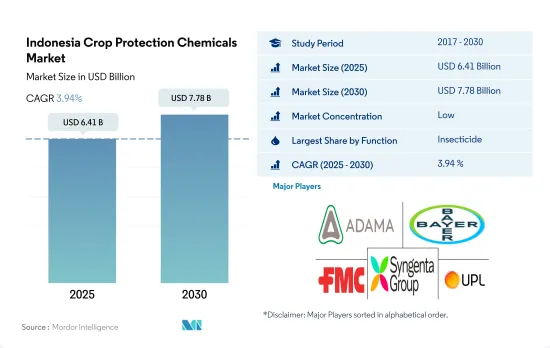

인도네시아의 작물 보호 화학제품 시장 규모는 2025년에 64억 1,000만 달러로 추정되고, 2030년에는 77억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년) 중 CAGR 3.94%로 성장할 것으로 예측됩니다.

살충제가 인도네시아 작물 보호 화학제품 시장을 독점

- 천연 자원과 적절한 기후 조건이 풍부한 인도네시아는 아시아에서 가장 중요한 농업 시장 중 하나입니다. 특히 식량안보를 달성하기 위한 주요 수단으로 수확량이 중시됨에 따라 작물 보호 화학제품에 대한 수요가 자극받고 있습니다. 인도네시아의 작물 보호 화학제품 시장은 꾸준히 성장하여 역사적 기간(2017-2022년)에 금액으로 22억 달러 증가했습니다.

- 농지의 확대 및 농업 기술의 진보에 의해 작물 보호 화학제품은 점점 일반적으로 되고 있습니다. 인도네시아는 세계 최대의 팜유 생산국이며, 커피 생산에서는 제4위입니다. 쌀 생산에 있어서 작물 보호 화학제품의 사용량은 여전히 높습니다.

- 살충제는 2022년에 금액 기준으로 74.4%의 최대 점유율을 차지했습니다. 농업 종사자는 다양한 등록 농약군을 이용할 수 있도록 해야 하며, 이를 통해 포장에서의 그룹 간 로테이션이 가능해집니다. 2021년 2월까지 인도네시아에는 1,059개의 살충제 브랜드가 등록되어 있으며 80가지의 유효 성분으로 구성되어 있습니다. 인도네시아에서 등록된 유효성분의 90% 이상이 피레트로이드, 유기인산염, 아벨멕틴, 밀베마이신의 조합으로 구성되어 있습니다.

- 농업은 경제에서 중요한 역할을 하기 때문에 정부는 GDP를 밀어 올리기 위해 인도네시아에서 정밀 농업산업을 추진하고 있습니다. 이 움직임은 이 나라의 작물 보호 화학품 시장에 좋은 영향을 주고 있습니다. 해충의 만연 증가 및 농업 종사자의 의식 고조에 더해 새로운 농법의 채택과 식품의 안전성 및 품질을 유지하는 수요로 인해 이 나라의 작물 보호 화학제품 시장은 예측 기간인 2023-2029년 CAGR 4.1%를 기록할 것으로 예측됩니다.

인도네시아의 작물 보호 화학제품 시장 동향

제초제 내성 잡초 증가에 의해 헥타르당 제초제 소비량이 증가

- 인도네시아는 저명한 농업국이며, 비옥한 토지와 열대성 기후라는 다종다양한 작물의 재배에 유리한 조건이 갖추어져 있는 것이 특징입니다. 그러나 이 나라의 농업 부문은 잡초의 만연, 해충, 균류병 등 수많은 과제에 직면해 있습니다. 이러한 문제에 대처하고 농작물 생산을 강화하기 위해 인도네시아 농업 종사자들은 농작물 손실을 억제하는 수단으로 농약 제품에 크게 의존하고 있습니다.

- 헥타르당 제초제 소비량은 과거 조사 기간 동안 2.7%라는 상당한 성장을 보였습니다. 이 급증은 주로 주요 작물에서 관찰되는 잡초의 만연 심화에 기인하고 있습니다. 안타깝게도, 이러한 침입 잡초는 특정 작물이나 그와 관련된 환경에 따라 다르지만, 10%에서 경이적인 60%에 이르는 연간 수확량의 대폭적인 손실을 일으키고 있습니다. 이러한 유해한 손실과 싸우기 위해 농업 종사자들은 점점 제초제를 주요 방제 방법으로 삼도록 되어 있습니다. 그러나 작물에 대한 제초제의 지속적인 살포로 잡초는 이러한 약제에 대한 내성을 획득하고 있습니다. 그 결과 제초제 소비량이 증가하고 헥타르당 살포량이 증가하여 인도네시아 농업 종사자들이 직면하고 있는 과제를 악화시키고 있습니다.

- 살균제, 살충제, 기타 농약 제품의 1헥타르당 소비량은 큰 변화 없이 비교적 안정되어 있습니다. 그러나 농업 활동의 확대로 국내의 헥타르당 농약 사용량은 전체적으로 증가하고 있습니다. 이러한 증가 경향은 농약의 최대 잔류 사용량에 제한을 두는 규제가 없는 것에 기인하고 있습니다. 그 결과, 헥타르당 농약 소비량은 증가하는 경향이 있습니다.

농약 제조업체는 유효 성분 가격의 상승을 소비자에게 전가하여 농약 가격이 상승할 수 있습니다.

- 유효성분의 가격은 농약의 생산비용에 직접 영향을 줍니다. 유효성분의 가격이 상승하면 농약 제조업체는 그 비용 증가를 소비자에게 전가하고, 결과적으로 농약 가격이 상승할 가능성이 있습니다.

- 시페르메트린은 2022년에 1톤당 2만 900달러로 평가되었습니다. 시페르메트린은 합성 피레트로이드계 살충제로 대규모 업무용 농업 용도로 사용되며, 저용량으로도 살포 직후부터 곤충을 구제하는 데 매우 효과적입니다. 또한 반점옥충, 핑크볼웜, 얼리스팟볼러, 애벌레 등 곤충에 의한 병해 방제에도 효과적입니다. 시페르메트린을 대체할 수 있는 약제의 입수 가능 여부는 가격 설정에 영향을 미칩니다.

- 아틀라진은 가격이 크게 상승했으며 2022년에는 1톤당 9,900달러로 평가되었습니다. 아틀라진은 농작물 발생 전과 발생 후 활엽 잡초와 벼과 잡초 방제에 사용되며 밭농사 옥수수, 스위트콘, 수수, 사탕수수에 사용이 가장 많습니다. 아틀라진은 잡초를 관리함으로써 작물 생산량을 최대 6% 증가시킬 수 있을 것으로 예측되고 있습니다. 이러한 요인 때문에, 이 유효 성분의 가격은 최근, 수요의 증가에 수반해 상승하고 있을 가능성이 있습니다. 제초제 사용에 관한 농업 종사자의 결정은 유효 성분의 가격에 영향을 받을 수 있습니다. 가격이 상승하면 농업 종사자는 대체 제초제 사용을 검토하게 될 가능성이 있습니다.

- 2022년, 만코제브 화학 살균제의 가격은 1톤당 약 7,700달러로 평가되고 있습니다. 만코제브는 접촉 살균제로 과실, 채소, 견과류, 밭작물 등 폭넓은 작물을 보호하는 능력을 가지고 있습니다. 또한 전문 잔디 관리에도 자주 이용되고 있습니다. 그 다용도성과 유효성 때문에 농업 종사자나 기타 전문가에게 있어서 농작물을 보호하기 위한 귀중한 도구가 되고 있습니다.

인도네시아의 작물 보호 화학제품 산업 개요

인도네시아의 작물 보호 화학제품 시장은 세분화되어 있으며 상위 5개 기업에서 1.67%를 차지하고 있습니다. 이 시장의 주요 기업은 ADAMA Agricultural Solutions Ltd, Bayer AG, FMC Corporation, Syngenta Group, UPL limited 등입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사의 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 인도네시아

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 기능별

- 살균제

- 제초제

- 살충제

- 연체동물 구제제

- 살선충제

- 적용 모드별

- 약제 살포

- 엽면 살포

- 훈증

- 종자 처리

- 토양처리

- 작물 유형별

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 지방종자

- 잔디 및 관상용

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- PT BIoTis Agrindo

- Syngenta Group

- UPL limited

- Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Indonesia Crop Protection Chemicals Market size is estimated at 6.41 billion USD in 2025, and is expected to reach 7.78 billion USD by 2030, growing at a CAGR of 3.94% during the forecast period (2025-2030).

Insecticides dominate the Indonesian crop protection chemicals market

- Given its natural resources and the right climatic conditions, Indonesia is one of the most important agricultural markets in Asia. In particular, demand for crop protection chemicals has been stimulated by a greater emphasis on yield as the primary instrument of achieving food security. The Indonesian crop protection chemicals market grew steadily, increasing by USD 2.2 billion in value during the historical period (2017-2022).

- Crop protection chemicals have become increasingly common in this country due to the expansion of agricultural land and advancements in farming techniques. Indonesia is the largest producer of palm oil globally and ranks fourth in coffee production. The use of crop protection chemicals in rice production remains high.

- Insecticides held the largest share of 74.4% by value in 2022. Farmers must have access to a diverse range of registered pesticide groups, which enables them to rotate among the groups in the field. Until February 2021, there were 1,059 insecticide brands registered in Indonesia, consisting of 80 different active ingredients. More than 90% of active ingredients registered in Indonesia consist of a combination of pyrethroids, organophosphates, avermectins, and milbemycins.

- The government is promoting the precision agriculture industry in Indonesia to boost its GDP, as agriculture plays a significant role in the economy. This move has had a positive impact on the crop protection chemicals market in the country. Owing to the increase in pest infestations and rise in awareness among farmers, coupled with the adoption of new farming practices and a demand to maintain food safety and quality, the crop protection chemicals market in the country is anticipated to record a CAGR of 4.1% during the forecast period (2023-2029).

Indonesia Crop Protection Chemicals Market Trends

Increased number of herbicide-resistant weed species has increased the herbicide consumption per hectare

- Indonesia stands out as a prominent agricultural country, distinguished by its abundance of fertile land and tropical climate, both of which create advantageous conditions for cultivating a wide variety of crops. However, the agricultural sector in the country faces numerous challenges, including weed infestation, insect pests, and fungal diseases. To address these issues and bolster crop production, Indonesian farmers are heavily relying on pesticide products as a means of controlling crop losses.

- The per hectare consumption of herbicides has witnessed a significant 2.7% increase during the historical period. This surge is primarily attributed to the escalating weed infestation observed in major crops. Disturbingly, these invasive weeds are causing substantial annual yield losses, ranging from 10% to a staggering 60%, depending on the specific crop and its associated environment. In order to combat these detrimental losses, farmers have increasingly turned to herbicides as their primary method of control. However, the continuous application of herbicides on crops has led the weeds to develop resistance against these chemical agents. This consequence has resulted in increased consumption of herbicides and an elevated application rate per hectare, exacerbating the challenge faced by Indonesian farmers.

- The per hectare consumption of fungicides, insecticides, and other pesticide products remains relatively stable without any significant changes. However, the overall usage of pesticides per hectare in the country is increasing due to the expansion of agricultural activities. This upward trend can be attributed to a lack of regulations that set limits on the maximum residual use of pesticides. As a result, the consumption of pesticides per hectare is on the rise.

Pesticide manufacturers may pass on the increase in active ingredient prices to consumers, resulting in higher pesticide prices

- The price of active ingredients directly affects the cost of producing pesticides. When the price of active ingredients rises, pesticide manufacturers may pass on these increased costs to consumers, resulting in higher pesticide prices.

- Cypermethrin was valued at USD 20.9 thousand per metric ton in 2022. It is a synthetic pyrethroid used as an insecticide in large-scale commercial agricultural applications and is very effective in controlling the insects immediately after application, even at lower doses. It is also effective in controlling diseases by insects such as spotted ball worms, pink ball worms, early spot borers, and hairy caterpillars. The availability of alternatives to cypermethrin can impact its pricing.

- Atrazine witnessed a significant increase in its price, valued at USD 9.9 thousand per metric ton in 2022. It is used to stop pre- and post-emergence broadleaf and grassy weeds in crops, with the highest use on field corn, sweet corn, sorghum, and sugarcane. It is projected that atrazine can raise crop production by up to 6% by managing weeds. Due to these factors, the prices of this active ingredient may have gone up in recent years in line with the rising demand. Farmers' decisions on herbicide usage can be affected by active ingredient prices. Higher prices may lead farmers to explore alternative herbicide applications.

- As of 2022, the price of mancozeb chemical fungicide was valued at approximately USD 7.7 thousand per metric ton. It is a contact fungicide that has the ability to provide protection for a wide range of crops, including fruits, vegetables, nuts, and field crops. It is also commonly utilized in professional turf management. Its versatility and effectiveness make it a valuable tool for farmers and other professionals to protect crops.

Indonesia Crop Protection Chemicals Industry Overview

The Indonesia Crop Protection Chemicals Market is fragmented, with the top five companies occupying 1.67%. The major players in this market are ADAMA Agricultural Solutions Ltd, Bayer AG, FMC Corporation, Syngenta Group and UPL limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Indonesia

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 PT Biotis Agrindo

- 6.4.8 Syngenta Group

- 6.4.9 UPL limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms