|

시장보고서

상품코드

1851545

음료 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Beverage Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

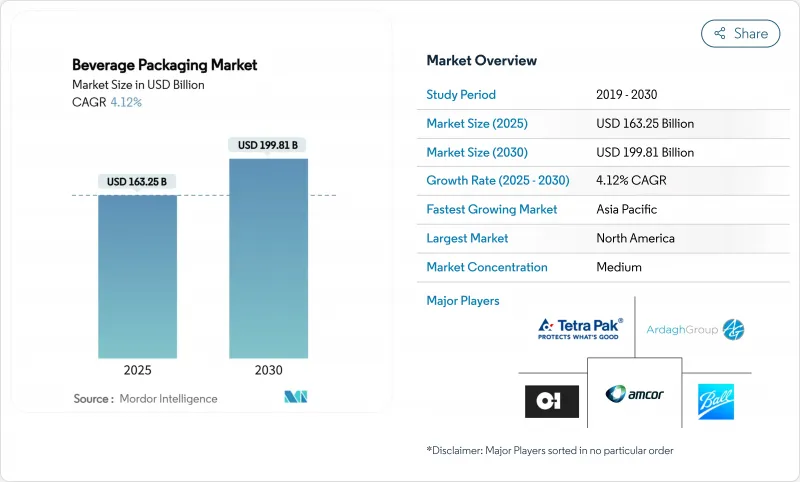

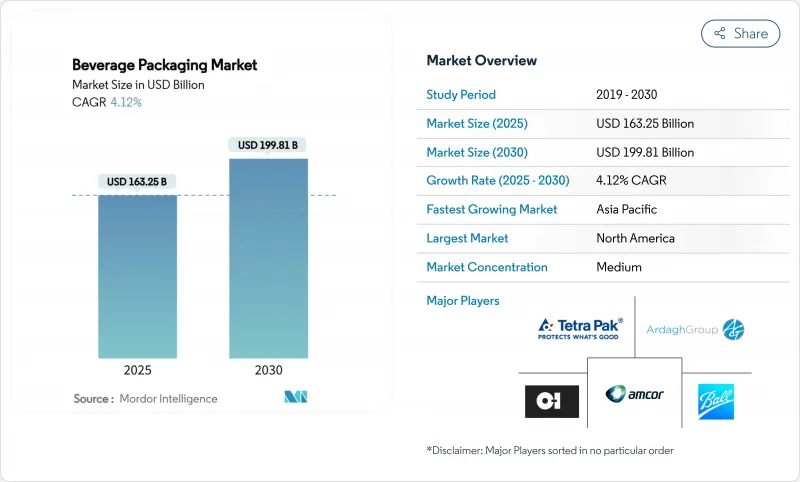

음료 포장 시장의 2025년 시장 규모는 1,632억 5,000만 달러에 달하고, CAGR 4.12%를 나타내, 2030년에는 1,998억 1,000만 달러에 이를 것으로 예상되고 있습니다.

성장을 뒷받침하는 것은 재활용 함량의 기준치를 표준화하는 세계적인 규제의 수렴이며, 프리미엄 음료의 발매와 알루미늄캔의 생산 능력 증강의 파도가 병행하는 수요 엔진이 되고 있습니다. 재생 재료의 의무화, 버진 수지의 비용 상승, 소비자의 취향의 저 임팩트 포맷으로의 변화를 잘 극복할 수 있는 패키징 공급자가 점유율을 획득하고 있습니다. 폐쇄 루프 재활용, 디지털 워터마크 및 전자상거래 지원 멀티팩에 대한 전략적 투자는 리더 기업과 후발 기업을 차별화하고 있습니다. 분쟁 중인 암코와 베리 세계의 합병으로 대표되는 통합은 경쟁 기반의 재구축을 계속하고 멀티포맷 포트폴리오를 보유한 기업들에게 규모의 이점을 제공합니다.

세계의 음료 포장 시장 동향과 인사이트

RTD 음료 프리미엄화

프리미엄 RTD의 출시로 브랜드는 상품화된 플라스틱에서 유리나 정교한 알루미늄으로 업그레이드를 촉구하고 있습니다. 영국에서는 2024년에 168억 파운드(212억 달러) 규모의 증류주 부문이 2023년에 50개 이상의 증류소를 신설했으며 RTD 증류주는 2030년까지 연률 16.2% 확대할 것으로 예측되고 있습니다. 미국 소비자의 92%가 유리를 품질과 끝없는 재활용 가능성을 연상하고 있으며, 유리 공급업체는 프리미엄 단서를 활용합니다. 브랜드 소유자는 투명도가 높은 용기에 스마트 클로저와 QR 코드가 있는 라벨을 조합하여 출처 데이터, 로열티 혜택, 인증된 재활용 방법을 제공합니다. 음료 포장 시장은 프리미엄 SKU의 리터당 포장 비용이 증가하고 주류 탄산 음료의 수량 침체를 상쇄함으로써 이익을 얻고 있습니다.

알루미늄캔의 생산능력 확대 급증

알루미늄의 무한한 재활용 가능성과 70% 이상의 폐쇄 루프 회수율은 세계적인 생산 능력 경쟁에 박차를 가하고 있습니다. 볼사는 플로리다 주 라인을 증설하고 2024년에는 오리건주 공장에 착공했습니다. 노벨리스는 2031년까지 연률 4%의 캔판 수요 성장이 예상되므로 아다그와의 장기 공급 계약에 따라 앨라배마주에 60만 톤의 압연 공장을 건설 중입니다. 따라서 음료 포장 시장에서 종합 금속 공급업체는 비용 경쟁력과 지속가능성 메시징 우위를 확보하고 맥주와 발포수 플라스틱에 압력을 가하고 있습니다.

불안정한 처녀 수지 가격

원유 가격의 변동과 정유소의 운영 중단으로 인해 2025년 초에 PTA와 MEG 비용이 상승했으며 중국과 유럽의 폴리에스터 병 칩 제조업체는 재고 균형을 조정하기 위해 생산 능력을 중단할 수밖에 없었습니다. 수지의 스팟 계약을 맺고 있는 패키징 컨버터는 마진의 압축을 목격하고, 선도 계약이나 기계 리사이클에의 통합을 촉구했습니다. 따라서 음료 포장 시장은 재활용 가능한 원료의 주식을 보유한 공급업체에 기울어 고객을 변동으로부터 보호하고 있습니다.

부문 분석

플라스틱은 2024년 매출의 42%를 차지하며, 정착된 공급망과 비용 우위를 보여주었습니다. 그러나 재활용 함량 지령과 보증금 수익의 확대는 PET의 이점에 도전하고 있습니다. 플라스틱 음료 포장 시장 규모는 전체 CAGR 4.12%에 머물 것으로 예상되며, 현재 진행중인 경량화와 화학 재활용 프로젝트에도 불구하고 그 점유율은 축소되고 있습니다. 판지의 CAGR 6.65%는 소재 중 가장 높으며, 알루미늄 캔에 의한 금속 컴백은 재생 가능하거나 무한히 재활용 가능한 기재를 요구하는 규제의 움직임과 소비자의 뒷받침을 보여줍니다. 그래픽 패키징 인터내셔널의 Boardio 판지 캐니스터와 EnviroClip 캐리어의 출시는 한때 수축 필름으로 관리되었던 탄산 음료의 멀티팩을 목표로 하고 있습니다. 통합형 공장은 국내 섬유 공급과 75%의 재활용률을 활용하여 버진 수지의 변동에 대응하고 있습니다.

음료 포장 산업은 물류 배출량이 증가함에도 불구하고 유리가 프레스티지 소재로 재포지셔닝되는 것을 목표로 하고 있습니다. OI Glass는 하이브리드 퍼니스와 경량 병을 갖춘 영국 알로아 공장의 현대화에 1억 5,000만 달러를 투자하여 2030년까지 25%의 CO2 삭감을 목표로 하고 있습니다. 알루미늄의 폐쇄 루프 비율은 70%를 넘었으며 노벨리스 공장은 장기 수요에 대한 자신감을 보여줍니다. 이러한 변화를 종합하면, 2030년까지는 다양한 소재가 혼재하게 되어, 인구 증가에 따라 절대 톤수가 증가해도, 플라스틱 시장 점유율은 음료 포장의 포인트를 잃게 됩니다.

병은 탄산음료, 물, 유제품 대체품, 알코올 음료 등 범용성이 높기 때문에 2024년 매출의 38%를 차지했습니다. 병으로 인한 음료 포장 시장 규모는 포맷 다양화 가운데 2030년까지 3.7%로 완만하게 성장할 것으로 예측됩니다. 테더 캡에 대한 대응과 고급 배리어 코팅(플라즈마 및 산화 규소 등)이 더욱 경량화를 가져옵니다. 그러나, 파우치는 CAGR 7.23%로 대폭적인 성장을 이룹니다. 이는 리터당 재료 중량이 60-80% 낮아 전자상거래에 적합하기 때문입니다.

멀티팩 와인과 칵테일 파우치는 낙하 테스트를 견디고, 운송 비용을 절감하며, 커브사이드 프로그램에서 허용되는 단일 소재 라미네이트를 활용합니다. 카톤은 무균 유제품, 주스 및 현재 식물 유래 라떼에 서비스를 계속 제공하고 있으며, 25%의 에너지 절감을 실현한 테트라팩의 UHT 충전 라인에 밀려 있습니다. 캔은 크래프트 맥주, 에너지 음료, 스파클링 워터를 통해 관련성을 유지하며, 그 급속 냉각 특성이 브랜드 충성도를 지원하고 있습니다. 맥주통은 판매량의 3% 미만으로 틈새 존재에 그치고 있지만, 스테인레스 스틸의 재사용 사이클은 25년 이상으로, 폐기물 제로의 이야기와 일치하고 있습니다.

지역 분석

북미는 1인당 음료 섭취량이 많아 프리미엄화의 여지가 있기 때문에 2024년 매출의 27%를 차지했습니다. 크라운 홀딩스는 버지니아와 네바다의 새로운 캔 라인에 의해 밀려 올라 2024년 북미 수량 성장률 5%를 나타냈습니다. 그러나 테더 캡과 확대 생산자 책임료에 대한 주 수준의 법률은 다각적인 다국적 기업에 유리한 컴플라이언스 복잡성을 창출합니다. 캐나다의 2030년까지의 rPET 조화 목표는 지역의 재생 이용 인프라를 장려하고 음료 포장 시장에서 순환 대응 공급업체를 더욱 강화합니다. 아시아태평양에서 경량 병을 수입하면 경쟁 압력이 발생하고 국내 컨버터가 비용면에서 어려움을 겪습니다.

아시아태평양은 도시화와 가처분 소득 상승에 힘입어 2030년까지 연평균 복합 성장률(CAGR)이 5.61%를 나타낼 것으로 예상됩니다. 중국에서는 2023년 첫 10개월 동안 음료 생산량이 2.7% 증가했으며 맥주 생산량은 22% 급증했습니다. 인도에서는 2025년 4월부터 rPET를 30% 사용하는 것이 의무화되어 재생원료 수요와 위반한 경우의 벌칙적인 과세가 모두 도입됩니다. 자사에서 재활용을 실시하는 다국적 기업(필리핀의 코카콜라의 PETValue 시설 등)이 발판을 굳히는 한편, 소규모의 컨버터는 투입 원료 부족에 직면합니다. 일본의 가산업자는 「빨리 먹을 수 있는」건강 음료에 중점을 두어 휴대용 영양제로서의 무균 파우치의 보급을 촉진하고 있습니다.

유럽에서는 2025년 2월에 PPWR이 시행되어 2028년까지 모든 포장재를 재활용 가능하게 하는 것, 2030년까지 PET병에 30%의 rPET를 사용하는 것이 의무화되는 등, 엄격한 규제가 리더십을 발휘하고 있습니다. 이 때문에 유럽권 음료 포장 시장은 모노 머티리얼 슬리브나 수성 잉크 등 재활용 가능한 디자인 프로토콜에 축족을 두고 있습니다. 식품용 rPET의 수급 불균형은 프리미엄의 상승을 유지하고 충전업자와 재활용업체의 제휴를 촉진합니다. ESG의 제약 속에서 유리의 생산 능력이 합리화되어 산지 와인과 프리미엄 스피릿공급이 긴축되어 가치 유지를 지원하고 있습니다. 소매업체가 회원국 전체에서 플라스틱 삭감 로드맵에 종사하는 가운데 유연한 종이 기반 솔루션이 지지를 모으고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- RTD 음료의 프리미엄화

- 알루미늄 캔 생산 능력 확장의 급증

- PET 경량화와 테더 캡 규제

- 전자상거래 멀티팩(주로 알코올)의 성장

- 순환을 위한 전자 워터마크의 상승

- 농축음료와 「가정용 소다」의 에코시스템

- 시장 성장 억제요인

- 불안정한 처녀 수지 가격

- 재생 PET 플레이크 공급 병목

- 반단독 사용 플라스틱 정책의 가속

- 유리의 설비투자를 억제하는 투자자의 ESG정사

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력/소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시 경제 동향의 평가

제5장 시장 규모와 성장 예측

- 재료 유형별

- 플라스틱

- 금속

- 유리

- 판지

- 제품 유형별

- 병

- 캔

- 파우치

- 카톤

- 맥주통

- 포장 형태별

- 무균 포장

- 고온 충전

- 저온 충전/탄산 음료

- 레토르트 포장

- 상온 보관 가능

- 냉장 유통

- 음료 유형별

- 탄산 음료

- 알코올 음료

- 생수

- 우유

- 과일 및 야채 주스

- 에너지 드링크

- 식물성 음료

- 기타 음료 유형

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 오스트리아

- 폴란드

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Ball Corporation

- Tetra Laval International SA

- OI Glass Inc.

- Crown Holdings Inc.

- Ardagh Group SA

- Ardagh Metal Packaging SA

- Verallia SA

- Vidrala SA

- Vetropack Holding Ltd.

- Silgan Holdings Inc.

- Berry Global Group Inc.

- Mondi plc

- Sonoco Products Company

- CCL Industries Inc.

- Smurfit Kappa Group plc

- CANPACK SA

- Huhtamaki Oyj

- Toyo Seikan Group Holdings Ltd.

- Nampak Ltd.

- Krones AG

- Guala Closures Group

제7장 시장 기회와 향후 전망

KTH 25.11.21The beverage packaging market was valued at USD 163.25 billion in 2025 and is forecast to expand at a 4.12% CAGR, reaching USD 199.81 billion by 2030.

Growth is propelled by converging global regulations that standardize recycled-content thresholds, while premium ready-to-drink launches and a wave of aluminum-can capacity additions provide parallel demand engines. Packaging suppliers able to navigate recycled-material mandates, cost inflation for virgin resin, and shifting consumer preferences toward low-impact formats are capturing share. Strategic investments in closed-loop recycling, digital watermarking, and e-commerce-ready multipacks are differentiating leaders from laggards. Consolidation-exemplified by the pending Amcor-Berry Global merger-continues to reshape the competitive baseline, creating scale benefits for firms with multi-format portfolios.

Global Beverage Packaging Market Trends and Insights

Premiumisation in Ready-to-Drink Beverages

Premium RTD launches are prompting brands to upgrade from commoditized plastics to glass and sleek aluminum, enabling higher shelf price points while still meeting recycled-content requirements. In the United Kingdom, a spirits sector worth GBP 16.8 billion (USD 21.2 billion) in 2024 recorded more than 50 new distilleries during 2023, and RTD spirits are projected to expand 16.2% per year to 2030. Glass suppliers are capitalizing on premium cues, with 92% of US consumers associating glass with quality and infinite recyclability. Brand owners are pairing high-clarity containers with smart closures and QR-coded labels that unlock provenance data, loyalty rewards, and authenticated recycling instructions. The beverage packaging market benefits as premium SKUs carry higher packaging spend per liter, offsetting volume softness in mainstream carbonates.

Surge in Aluminium-Can Capacity Expansions

Aluminum's infinite recyclability and closed-loop recovery rates above 70% have spurred a global capacity race. Ball Corporation added a Florida line and broke ground on an Oregon plant in 2024. Novelis is building a 600,000-tonne rolling mill in Alabama under long-term supply agreements with Ardagh to accommodate forecast 4% annual can-sheet demand growth through 2031. The beverage packaging market therefore sees integrated metal suppliers gaining cost leverage and sustainability messaging advantages, pressuring plastics in beer and sparkling water.

Volatile Virgin-Resin Prices

Crude oil swings and refinery outages pushed PTA and MEG costs higher in early 2025, forcing polyester bottle-chip producers in China and Europe to idle capacity to re-balance inventories. Packaging converters on spot resin contracts saw margin compression, encouraging forward contracts or integration into mechanical recycling. The beverage packaging market therefore tilts toward suppliers holding equity stakes in recycle-ready feedstock, shielding customers from volatility.

Other drivers and restraints analyzed in the detailed report include:

- PET Lightweighting and Tethered-Cap Regulations

- Growth of E-commerce Multipacks

- Supply Bottlenecks for Recycled PET Flakes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic retained 42% of 2024 revenue, underlining entrenched supply chains and cost advantages. Yet recycled-content directives and deposit-return expansion are challenging PET's dominance. The beverage packaging market size for plastic is projected to advance only at the overall 4.12% CAGR, tempering its share despite ongoing lightweighting and chemical-recycling projects. Paperboard's 6.65% CAGR-highest among materials-and metal's comeback via aluminum cans illustrate regulatory pull and consumer push toward renewable or infinitely recyclable substrates. Graphic Packaging International's launch of Boardio paperboard canisters and EnviroClip carriers targets carbonated soft drink multipacks once controlled by shrink-film. Integrated mills leverage domestic fiber supply and 75% recycling rates, cushioning them against virgin-resin volatility.

The beverage packaging industry is also witnessing glass repositioned as a prestige material notwithstanding higher logistics emissions. O-I Glass committed USD 150 million to modernize its Alloa, UK plant with hybrid furnaces and lightweight bottles, aiming for a 25% CO2 cut by 2030. Aluminum enjoys a closed-loop rate above 70%, and Novelis' forthcoming mill signals confidence in long-term demand. Collectively, these shifts suggest a diversified material mix by 2030, with plastics losing points of beverage packaging market share even as absolute tonnage rises in line with population growth.

Bottles accounted for 38% of 2024 revenue thanks to versatility across carbonates, water, dairy alternates, and alcohol. The beverage packaging market size attributed to bottles is projected to grow modestly at 3.7% to 2030 amid format diversification. Tethered-cap compliance and advanced barrier coatings (e.g., plasma or silicon oxide) are unlocking incremental weight savings. However, pouches are set to capture outsized gains via a 7.23% CAGR, reflecting 60-80% lower material weight per liter and suitability for e-commerce.

Multipack wine and cocktail pouches withstand drop tests, reduce shipping costs, and utilize mono-material laminates increasingly accepted in curbside programs. Cartons continue to service aseptic dairy, juice, and now plant-based lattes, propelled by Tetra Pak's UHT filling lines with energy cuts of 25%. Cans sustain relevance through craft beer, energy drinks, and sparkling water, and their rapid chilling characteristics underpin brand loyalty. Beer kegs remain a niche at under 3% of volume, but stainless-steel re-use cycles of 25+ years align with zero-waste narratives.

The Beverage Packaging Market Report is Segmented by Material Type (Plastic, Metal, Glass, and Paperboard), Product Type (Bottles, Cans, Pouches, Cartons, and Beer Kegs), Packaging Format (Aseptic, Hot-Fill, Cold-Fill/Carbonated, Retortable, and More), Beverage Type (Carbonated Drinks, Alcoholic Beverages, Bottled Water, Milk, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 27% of 2024 revenue due to to high per-capita beverage intake and premiumization headroom. Crown Holdings registered 5% North American volume growth in 2024, boosted by new Virginia and Nevada can lines. Yet state-level legislation on tethered caps and expanded-producer-responsibility fees creates compliance complexity that favors diversified multinationals. Canada's harmonized rPET targets to 2030 incent regional reclamation infrastructure, further bolstering circular-ready suppliers within the beverage packaging market. Competitive pressures arise from Asia-Pacific imports of lightweight bottles, challenging domestic converters on cost.

Asia-Pacific is forecast to post a 5.61% CAGR through 2030, underpinned by urbanization and rising disposable incomes. China recorded 2.7% output growth in beverages across the first ten months of 2023 while beer production jumped 22%. India's rPET mandate at 30% from April 2025 introduces both demand for recycled feedstock and punitive taxes for non-compliance. Multinationals with in-house recycling (e.g., Coca-Cola's PETValue facility in the Philippines) gain a foothold, whereas small converters face input scarcity. Japanese processors focus on "ready-to-eat" and healthy beverages, encouraging aseptic pouch uptake for portable nutrition.

Europe commands stringent regulatory leadership with the PPWR effective February 2025 mandating all packaging be recyclable by 2028 and 30% rPET in PET bottles by 2030. The beverage packaging market in the bloc therefore pivots toward design-for-recycling protocols such as monomaterial sleeves and water-based inks. Supply-demand imbalances in food-grade rPET keep premiums elevated, encouraging partnerships between fillers and recyclers. Glass capacity rationalization amid ESG constraints tightens supply for regional wine and premium spirits, supporting value retention. Flexible paper-based solutions gain traction as retailers commit to plastic reduction roadmaps across member states.

- Amcor plc

- Ball Corporation

- Tetra Laval International SA

- O-I Glass Inc.

- Crown Holdings Inc.

- Ardagh Group S.A.

- Ardagh Metal Packaging S.A.

- Verallia S.A.

- Vidrala S.A.

- Vetropack Holding Ltd.

- Silgan Holdings Inc.

- Berry Global Group Inc.

- Mondi plc

- Sonoco Products Company

- CCL Industries Inc.

- Smurfit Kappa Group plc

- CANPACK S.A.

- Huhtamaki Oyj

- Toyo Seikan Group Holdings Ltd.

- Nampak Ltd.

- Krones AG

- Guala Closures Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumisation in ready-to-drink (RTD) beverages

- 4.2.2 Surge in aluminium-can capacity expansions

- 4.2.3 PET lightweighting and tethered-cap regulations

- 4.2.4 Growth of e-commerce multipacks (mainly alcohol)

- 4.2.5 Rise of digital watermarks for circularity (under-radar)

- 4.2.6 Beverage concentrates and "soda-at-home" ecosystems (under-radar)

- 4.3 Market Restraints

- 4.3.1 Volatile virgin-resin prices

- 4.3.2 Supply bottlenecks for recycled PET flakes

- 4.3.3 Anti-single-use plastics policy acceleration (under-radar)

- 4.3.4 Investor ESG scrutiny curbing cap-ex in glass (under-radar)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.2 Metal

- 5.1.3 Glass

- 5.1.4 Paperboard

- 5.2 By Product Type

- 5.2.1 Bottles

- 5.2.2 Cans

- 5.2.3 Pouches

- 5.2.4 Cartons

- 5.2.5 Beer Kegs

- 5.3 By Packaging Format

- 5.3.1 Aseptic

- 5.3.2 Hot-Fill

- 5.3.3 Cold-Fill/Carbonated

- 5.3.4 Retortable

- 5.3.5 Shelf-Stable Ambient

- 5.3.6 Chilled Distribution

- 5.4 By Beverage Type

- 5.4.1 Carbonated Drinks

- 5.4.2 Alcoholic Beverages

- 5.4.3 Bottled Water

- 5.4.4 Milk

- 5.4.5 Fruit and Vegetable Juices

- 5.4.6 Energy Drinks

- 5.4.7 Plant-based Drinks

- 5.4.8 Other Beverage Types

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Austria

- 5.5.2.7 Poland

- 5.5.2.8 Russia

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Ball Corporation

- 6.4.3 Tetra Laval International SA

- 6.4.4 O-I Glass Inc.

- 6.4.5 Crown Holdings Inc.

- 6.4.6 Ardagh Group S.A.

- 6.4.7 Ardagh Metal Packaging S.A.

- 6.4.8 Verallia S.A.

- 6.4.9 Vidrala S.A.

- 6.4.10 Vetropack Holding Ltd.

- 6.4.11 Silgan Holdings Inc.

- 6.4.12 Berry Global Group Inc.

- 6.4.13 Mondi plc

- 6.4.14 Sonoco Products Company

- 6.4.15 CCL Industries Inc.

- 6.4.16 Smurfit Kappa Group plc

- 6.4.17 CANPACK S.A.

- 6.4.18 Huhtamaki Oyj

- 6.4.19 Toyo Seikan Group Holdings Ltd.

- 6.4.20 Nampak Ltd.

- 6.4.21 Krones AG

- 6.4.22 Guala Closures Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment