|

시장보고서

상품코드

1687239

미국의 전기자동차(EV) 충전 설비 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)US Electric Vehicle (EV) Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

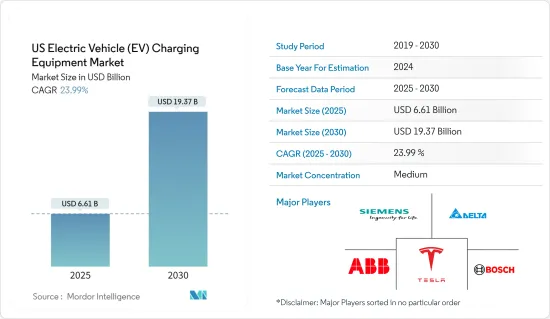

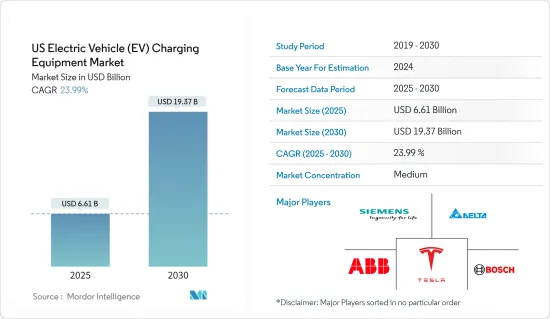

미국의 전기자동차(EV) 충전 설비 시장 규모는 2025년에 66억 1,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 23.99%로 성장할 전망이며, 2030년에는 193억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 국내에서의 전기자동차의 보급 확대나 전기자동차 인프라의 개발 등의 요인이, 예측 기간 중 충전 설비 시장을 견인할 것으로 전망됩니다.

- 한편, 충전소의 설치에 수반하는 높은 설치 비용 및 유지관리 비용이 예측 기간 중 시장 성장에 방해가 될 것으로 예상됩니다.

- EV에 대한 투자 증가 및 EV 충전 설비의 기술 진보는 예측 기간 중 미국의 전기자동차 충전 설비 시장에 큰 비즈니스 기회를 가져올 것으로 기대되고 있습니다.

미국의 전기자동차(EV) 충전 설비 시장 동향

이 나라에서 전기자동차의 보급 확대

- 전기자동차는 친환경성과 비용 효율성이 점점 더 높아지고 있습니다. 그러나 EV 소유자에게 있어 주요 우려 사항 중 하나는 충전 스테이션의 이용 가능성입니다. 전기자동차 이용이 증가함에 따라 그 요구를 충족시키기 위해 더 많은 충전 설비 및 인프라가 필요합니다.

- 전기자동차의 보급이 진행됨에 따라 충전 장치와 관련 인프라의 요구가 확대되고 있습니다. 수요를 충족시키기 위해 정부와 회사는 주차장, 쇼핑몰, 고속도로와 같은 공공 장소에 충전소을 설치하기 위해 노력하고 있습니다. 또한 전기자동차 소유자의 대부분은 개인 사용을 위해 집에 충전 설비를 설치합니다.

- 국제에너지기구(IEA)에 따르면 미국에서는 2022년 전기차 판매량이 2021년 대비 55% 증가하여 배터리 전기자동차(BEV)가 견인했습니다. BEV의 판매 대수는 70% 증가해 약 80만 대에 달하였고, 2019-2020년 침체된 뒤 2년 연속 견조한 성장을 확인했습니다. PHEV의 판매 대수도 15% 증가에 그쳤던 것이 증가했습니다.

- 미국 에너지성 과학국에 따르면 2023년 12월 중 미국에서 판매된 플러그인 차량은 총 14만 1,055대(BEV 10만 928대, PHEV 4만 127대)로 2022년 12월 판매 대수에서 42.4% 증가했습니다. 또한 2023년 12월 미국에서 판매된 HEV는 11만 7,690대(승용차 3만 1,825대, LT 8만 5,865대)로 2022년 12월 대비 70.3% 증가했습니다. 전기자동차의 총 재고는 2022년에 300만 대가 되었고, 2021년 대비 36% 이상 증가하여 세계 전체의 10%를 차지했습니다.

- 2023년 2월, 바이덴 초당파 인프라법 하에, 국가는 전기자동차 충전에 75억 달러, 청정 수송에 100억 달러, 전기자동차 배터리 부품, 중요 미네랄, 재료에 70억 달러 이상을 투자할 계획을 발표했습니다.

- 게다가 자동차 제조업체와 배터리 제조업체는 37개의 EV 배터리 전용 제조 시설에 500억 달러 이상을 투입할 계획입니다. 총 설비용량으로는 654GWh의 생산이 가능하며, 이는 2030년까지 연간 약 1,000만 대의 소형차를 지원해 전기차의 제조와 판매를 뒷받침하기에 충분한 용량입니다. 이러한 투자는 모두 미국 전역에서 EV의 보급을 뒷받침할 것으로 전망니다. 그 결과 예측 기간 동안 EV 충전 설비 및 인프라 요구가 높아지게 됩니다.

- 따라서 이 나라에서의 전기차의 보급과 투자 증가는 EV 충전 설비 수요를 계속 가속화하고 예측 기간 유망한 시장을 유지할 것으로 예상됩니다.

시장을 독점하는 배터리 전기자동차.

- 배터리 전기자동차(BEV)는 일반적으로 전기 모터를 탑재한 전기자동차라고도 합니다. 이 차량은 전기 모터에 전력을 공급하기 위해 대형 트랙션 배터리 팩을 사용합니다. EV는 벽의 콘센트 또는 전기자동차 공급설비(EVSE)라고 불리는 충전 설비에 접속해야 합니다.

- BEV는 완전한 전기자동차이며, 통상, 내연 기관(ICE), 연료 탱크, 배기관을 포함하지 않습니다. 추진력은 전기에만 의존하고 있습니다. 차량의 에너지는 배터리 팩으로부터 공급되어 그리드로부터 충전됩니다. BEV는 제로 에미션 차량으로 기존 가솔린 차량에 의한 유해한 테일파이프 배출이나 대기오염 위험은 없습니다.

- 미국에서는 배터리 전기자동차(BEV)의 보급이 가속화되어 자동차 산업에 변화를 가져오고 있습니다. 기술의 진보, 정부의 지원, 환경 문제에 대한 관심의 증가로 BEV는 기후 변화라는 과제에 대처하고 화석 연료에 대한 의존을 줄이는 유망한 솔루션으로 떠올랐습니다.

- 최근 미국에서는 배터리 전기자동차의 채용이 크게 증가했습니다. 배터리 기술의 향상, 항속 거리의 연장, 충전 인프라의 급증에 의해 최초의 진입 장벽을 극복할 수 있었습니다. Tesla, Chevrolet, Nissan, Ford와 같은 자동차 제조업체들은 광범위한 소비자들에게 호소하는 저렴한 모델을 제공하고 BEV의 보급에 큰 역할을 했습니다.

- 2022년 미국에서는 99만 대의 전기차가 신규 등록되어 그 중 약 80%가 BEV였습니다. 국제에너지기구(IEA)에 따르면 미국에서 배터리 전기자동차(BEV) 판매량은 2021년 대비 40% 증가했습니다.

- 미국 에너지부에 따르면 공개적으로 이용 가능한 전기자동차 충전 포인트(레벨 1, 레벨 2, DC 급속)의 수는 2022년 14만 3,729에서 2023년 17만 5,547로 증가했습니다. 2023년 충전 포인트 수 17만 5,547곳 중 약 13만 7,795곳이 저속 충전 포인트였고, 나머지 3만 7,752곳이 급속 충전 포인트였습니다. 국내에서는 최근 몇 년 동안 일반적으로 사용 가능한 급속 충전 포인트의 비율이 크게 증가하고 있습니다. 예측 기간 동안에도 동일한 경향이 지속될 것으로 예상됩니다.

- 기술이 계속 진화하는 동안 미국의 배터리 전기자동차의 미래는 유망합니다. 자동차 제조업체는 미국 정부와 함께 배터리 효율 향상, 비용 절감, 차량 전체의 성능 향상을 위한 연구 개발에 많은 투자를 하고 있습니다.

- 예를 들어, 2022년 3분기에는 이 나라가 EV와 배터리 제조에 약 2,100억 달러를 투자했습니다. Tesla는 2022-2024년 미국과 독일에 매년 60억-80억 달러를 투자하는 등 투자 증가가 전망되고 있습니다. 게다가 자동차 및 배터리 제조업체도 국내 37개 EV 배터리 제조 시설에 540억 달러의 지출을 계획하고 있습니다. 이러한 시설에서는 2030년까지 연간 654기가와트(GWh)의 EV 배터리용량이 생산될 전망입니다. 이러한 시나리오는 BEV 제조 산업에 긍정적인 영향을 미칠 것으로 예상됩니다.

- 게다가 자율주행 기술과 차량 투 그리드의 통합의 출현은 BEV가 운송 부문에 혁명을 일으킬 확률을 더욱 높이고 있습니다. 이것에 의해 배터리 전기자동차용 충전 장치 수요가 높아지고 있습니다

미국의 전기자동차(EV) 충전 설비 산업 개요

미국의 전기자동차(EV) 충전 설비 시장은 반분단되어 있습니다. 이 시장의 주요 기업으로는 ABB Ltd, Robert Bosch GmbH, Delta Electronics Inc., Siemens AG, Tesla Inc. 등이 있습니다.(순부동)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 시장 규모 및 수요 예측2029년)

- 최근 동향 및 개발

- 정부의 규제 및 시책

- 시장 역학

- 성장 촉진요인

- 전기차 보급 및 관련 투자 증가

- 정부의 지원 시책 및 이니셔티브

- 성장 억제요인

- 전기자동차 충전 설비 설치에 걸리는 고비용

- 성장 촉진요인

- 공급망 분석

- PESTLE 분석

제5장 시장 세분화

- 차종별

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 자동차(PHEV)

- 하이브리드 전기자동차(HEV)

- 용도별

- 가정용 충전

- 직장 충전

- 공공 충전

- 충전 유형별

- AC 충전(레벨 1 및 레벨 2)

- DC 충전

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 주요 기업의 전략

- 기업 프로파일

- ABB Ltd.

- Robert Bosch GmbH

- ChargePoint Inc.

- Enphase Energy, Inc.

- Delta Electronics Inc.

- Powercharge

- Siemens AG

- Tesla Inc.

- KOSTAL Automobil Elektrik GmbH & Co. KG.

- Webasto SE

- 시장 랭킹 분석

제7장 시장 기회 및 향후 동향

- EV 충전기의 기술 진보

The US Electric Vehicle Charging Equipment Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 19.37 billion by 2030, at a CAGR of 23.99% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors like the growing adoption of electric vehicles in the country and the development of electric vehicle infrastructure are expected to drive the charging equipment market during the forecast period.

- On the other hand, high installation costs associated with setting up charging stations and maintenance costs are expected to hinder the market's growth during the forecast period.

- Nevertheless, increasing investments in EVs and technological advancements in EV charging Equipment are expected to provide significant opportunities for the US electric vehicle (EV) charging equipment market during the forecast period.

US Electric Vehicle (EV) Charging Equipment Market Trends

Increasing Adoption of Electric Vehicles in the Country

- Electric vehicles (EVs) became increasingly popular due to their eco-friendly nature and cost-effective benefits. However, one of the main concerns for EV owners is the availability of charging stations. As the usage of electric vehicles increases, more charging equipment and infrastructures are required to fulfill the need.

- As the adoption of electric vehicles increases, the need for charging devices and relevant infrastructure is expanding. To meet the demand, the government and companies work on installing more charging stations in public areas such as parking lots, malls, and highways. Many electric vehicle owners also install charging stations in their homes for personal use.

- According to the International Energy Agency (IEA), in the United States, electric car sales increased by 55% in 2022 relative to 2021, led by battery electric vehicles (BEV). Sales of BEVs increased by 70%, reaching nearly 800,000 and confirming a second consecutive year of solid growth after the 2019-2020 dip. Sales of PHEVs also grew, albeit by only 15%.

- According to the United States Department of Energy Office of Science, a total of 141,055 plug-in vehicles (100,928 BEVs and 40,127 PHEVs) were sold during December 2023 in the United States, up 42.4% from the sales in December 2022. Also, In December 2023, 117,690 HEVs (31,825 cars and 85,865 LTs) were sold in the United States, up 70.3% from the sales in December 2022. The total stock of electric cars stood at 3 million in 2022, recording more than a 36% increase compared to 2021, accounting for 10% of the global total.

- In February 2023, Under Biden's Bipartisan Infrastructure Law, the country announced its plan to invest USD 7.5 billion in electric vehicle charging, USD 10 billion in clean transportation, and over USD 7 billion in electric vehicle (EV) battery components, critical minerals, and materials.

- Furthermore, the automakers and battery makers plan to spend over USD 50 billion across 37 dedicated EV battery manufacturing facilities. At total capacity, the facilities could produce 654 GWh in capacity, which is enough to support about 10 million light-duty vehicles annually by 2030 to support their electric vehicle manufacturing and sales. All these investments are likely to boost the adoption of EVs across the United States. It, in turn, is driving the need for EV charging devices and infrastructures over the forecast period.

- Hence, the increasing adoption of electric vehicles (EVs) and investments in the country are expected to continue accelerating the demand for EV charging equipment and hold a promising market over the forecast period.

Battery Electric Vehicles to Dominate the market.

- Battery electric vehicles (BEVs) are also commonly referred to as electric vehicles with an electric motor. The vehicle uses a large traction battery pack to power the electric motor. The EV must be plugged into a wall outlet or charging equipment called electric vehicle supply equipment (EVSE).

- BEVs are fully electric vehicles and typically do not include an internal combustion engine (ICE), fuel tank, or exhaust pipe. They rely only on electricity for propulsion. The vehicle's energy comes from the battery pack, which is recharged from the grid. BEVs are zero-emission vehicles, as they do not generate any harmful tailpipe emissions or air pollution hazards caused by traditional gasoline-powered vehicles.

- The United States is transforming the automotive industry as battery electric vehicles (BEVs) gain momentum and popularity. With technological advancements, government support, and increasing environmental concerns, BEVs emerged as a promising solution to address the challenges of climate change and reduce reliance on fossil fuels.

- In recent years, the adoption of battery-electric vehicles in the United States grew significantly. Improved battery technology, extended driving ranges, and a surge in charging infrastructure helped overcome the initial entry barriers. Automakers like Tesla, Chevrolet, Nissan, and Ford played instrumental roles in popularizing BEVs, offering affordable models that appeal to a broader range of consumers.

- In 2022, the United States registered 990,000 new electric cars, of which about 80% were BEVs, and witnessed a rise of 70% compared to 2021. According to the International Energy Agency (IEA), battery electric vehicle (BEV) sales increased by 40% in the United States relative to 2021.

- According to the United States Department of Energy, the number of publicly available electric vehicle charging points (Level 1, Level 2, and DC Fast) grew from 143,729 in 2022 to 175,547 in 2023. Of the 175,547 charging points in 2023, around 137,795 were slow charging points, and the rest 37,752 were fast charging points. The share of publicly available fast charging points witnessed significant growth in the country in recent years. It is expected to continue the same trend during the forecast period.

- As technology continues to evolve, the future of battery-electric vehicles in the United States looks promising. Automakers, along with the United States government, are investing heavily in research and development to improve battery efficiency, reduce costs, and enhance overall vehicle performance.

- For instance, in Q3 2022, the country invested nearly USD 210 billion in EV and battery manufacturing. The investment is expected to increase, with Tesla including USD 6-8 billion annually in the United States and Germany between 2022 and 2024. Further, automakers and battery makers also planned to spend USD 54 billion across 37 EV battery manufacturing facilities across the country. These facilities are expected to produce 654 gigawatt hours (GWh) of EV battery capacity annually by 2030. Such a scenario is expected with a positive impact on the BEV manufacturing industry.

- Moreover, the emergence of autonomous driving technology and vehicle-to-grid integration further adds to the potential of BEVs to revolutionize the transportation sector. It is thereby driving the demand for charging equipment for battery electric vehicles.

US Electric Vehicle (EV) Charging Equipment Industry Overview

The US electric vehicle (EV) charging equipment market is semi-fragmented. Some of the key players in the market (not in any particular order) include ABB Ltd, Robert Bosch GmbH, Delta Electronics Inc., Siemens AG, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles and Related Investments

- 4.5.1.2 Supportive Government Policies And Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Cost Of Setting Up Ev Charging Stations

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Battery Electric Vehicle (BEV)

- 5.1.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.1.3 Hybrid Electric Vehicle (HEV)

- 5.2 Application

- 5.2.1 Home Charging

- 5.2.2 Workplace Charging

- 5.2.3 Public Charging

- 5.3 Charging Type

- 5.3.1 AC Charging (Level 1 and Level 2)

- 5.3.2 DC Charging

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd.

- 6.3.2 Robert Bosch GmbH

- 6.3.3 ChargePoint Inc.

- 6.3.4 Enphase Energy, Inc.

- 6.3.5 Delta Electronics Inc.

- 6.3.6 Powercharge

- 6.3.7 Siemens AG

- 6.3.8 Tesla Inc.

- 6.3.9 KOSTAL Automobil Elektrik GmbH & Co. KG.

- 6.3.10 Webasto SE

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in the EV Charging Equipment