|

시장보고서

상품코드

1850311

애플리케이션 딜리버리 컨트롤러(ADC) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Application Delivery Controllers (ADC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

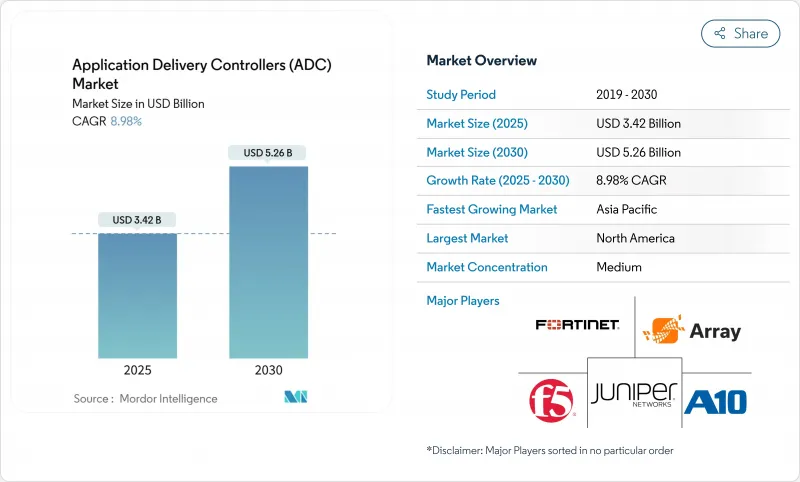

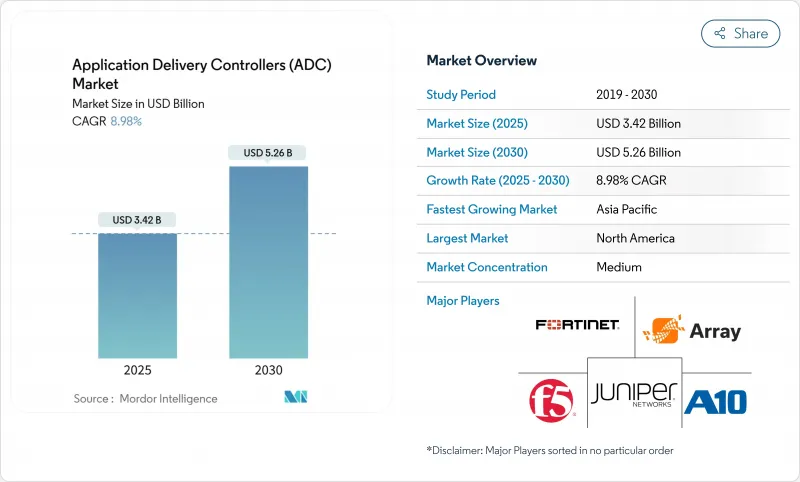

ADC(애플리케이션 딜리버리 컨트롤러) 시장 규모는 2025년에 34억 2,000만 달러로 평가되었고 2030년에 52억 6,000만 달러에 이를 것으로 예측되며, CAGR은 8.98%를 나타낼 전망입니다.

클라우드 네이티브 아키텍처로의 급속한 전환, 증가하는 동서 방향 데이터센터 트래픽, 지속되는 멀티클라우드 전략으로 인해 지능적이고 보안 인식형 트래픽 관리 플랫폼에 대한 수요가 높게 유지되고 있습니다. 벤더들은 이제 고급 레이어 7 보안, API 보호, AI 지원 분석을 단일 제품으로 묶어 제공함으로써 기업이 위험을 통제하면서 사용자 경험을 개선할 수 있도록 합니다. 하드웨어 어플라이언스는 여전히 성능이 중요한 워크로드에서 우위를 점하고 있지만, 조직들이 민첩성과 사용량 기반 경제성을 우선시함에 따라 가상 및 클라우드 관리형 폼 팩터의 성장 속도가 더 빨라지고 있습니다. 지역별로는 북미가 성숙한 IT 인프라와 규제적 호재를 활용해 주도권을 유지하는 반면, 아시아태평양 지역의 5G 구축과 디지털 이니셔티브가 가장 가파른 성장 곡선을 만들어내고 있습니다.

세계의 애플리케이션 딜리버리 컨트롤러(ADC) 시장 동향 및 인사이트

클라우드 네이티브 및 마이크로 서비스 아키텍처로 이동

기업 워크로드의 절반 이상이 이미 컨테이너화되거나 서버리스 구성 요소로 실행되면서, 애플리케이션 딜리버리 컨트롤러 시장은 쿠버네티스 클러스터 및 서비스 메시 내부에 위치하는 경량 API 중심 폼 팩터로 전환되고 있습니다. 이러한 마이크로 게이트웨이는 세분화된 트래픽 제어, 상호 TLS 종단 처리, 현대 애플리케이션의 일시적 특성에 부합하는 자동 확장 기능을 제공합니다. 벤더들은 동서 방향 서비스 호출로 인해 발생한 보안 취약점을 해소하기 위해 스키마 인식 API 방화벽과 분산 속도 제한기를 내장하고 있습니다. CIO들이 플랫폼 엔지니어링을 추진함에 따라 선언형 “코드 기반 ADC(ADC-as-code)”는 GitOps 파이프라인과 원활하게 통합되어 개발(Dev)과 네트워크 운영(NetOps) 간의 작업 이관을 줄입니다.

급증하는 동서 방향 데이터센터 트래픽

가상 서버 밀도 증가는 내부 흐름을 급증시켜 기존 남북(북-남) 패턴을 능가하며 지연 시간에 민감한 마이크로 트랜잭션을 증가시켰습니다. 분산형 ADC 인스턴스는 이제 워크로드 포드에 더 가깝게 배치되어 병목 현상 없이 광범위한 텔레메트리 및 인라인 복호화를 제공합니다. 금융 거래소, 통신사, 게임 제공업체는 수천 개의 경량 프록시를 전개하여 레이어-7 정책을 집합적으로 적용하면서도 버스트성 리소스 풀에 적응합니다.

복잡한 레이어-7 정책 구성이 IT 운영에 부담

기업 팀은 수백 개의 이질적인 애플리케이션에 직면하며, 각각 맞춤형 라우팅, 리라이팅 또는 WAF 로직을 요구합니다. 멀티클라우드 환경 전반에 걸쳐 정확성을 유지하는 것은 부족한 DevSecOps 인력을 압박하며 광범위한 ADC 전개를 지연시킬 수 있습니다. 벤더들은 의도 기반 템플릿, AI 지원 규칙 생성, 시각적 종속성 맵으로 대응하지만 기술 격차는 지속됩니다.

부문 분석

하드웨어 어플라이언스는 2024년 애플리케이션 딜리버리 컨트롤러 시장의 59%를 차지했으며, 이는 전용 SSL 오프로드 칩과 결정론적 처리량에 의해 뒷받침되었습니다. 그러나 가상화 부문은 DevOps 팀이 ADC 이미지를 CI/CD 파이프라인에 직접 통합함으로써 랙 공간을 줄이고 전개 기간을 단축함에 따라 14.6%의 연평균 성장률(CAGR)로 확장되고 있습니다. 가상 솔루션용 애플리케이션 딜리버리 컨트롤러 시장 규모는 컨테이너 채택과 함께 급증할 것으로 예상되며, 이는 미션 크리티컬 계층에서 하드웨어의 지배력에 도전장을 내밀고 있습니다.

성숙한 벤더들은 어플라이언스 오버헤드를 제거하면서도 기존 정책 엔진을 계승하는 컨테이너 네이티브 프록시를 출시하며 대응하고 있습니다. 비용 투명성과 클라우드 마켓플레이스 결제는 애자일 팀에게 매력적이어서, 전통적 기업 내부에서도 소프트웨어의 점유율 증가를 이끌고 있습니다. TLS 1.3 및 QUIC 채택이 증가함에 따라 코드 수준의 민첩성은 소프트웨어 형태로의 선택을 더욱 촉진할 것이나, 금융 및 통신 코어의 초고 TPS 게이트웨이에는 하드웨어가 지속될 전망입니다.

2024년 애플리케이션 딜리버리 컨트롤러 시장 규모에서 온프레미스 인스턴스는 여전히 64%를 차지하며, 데이터 주권 규제를 준수해야 하는 산업 분야에서 선호됩니다. 통합 위협 분석 모듈과 사용량 기반 용량 라이선싱은 이제 포크리프트 교체 없이도 레거시 환경을 갱신합니다.

반대로 클라우드 관리형 모델은 플랫폼 팀이 패치, 확장 및 원격 측정 기능을 벤더 운영 제어 플레인에 오프로드함에 따라 15.2%의 CAGR로 상승합니다. 다중 지역 전개가 몇 시간 내에 완료되고, 통합 API 정책 적용으로 사이트 수준의 드리프트가 제거되어 디지털 네이티브 기업들이 선호하는 경로가 되고 있습니다. 애플리케이션 딜리버리 컨트롤러 시장은 단일 콘솔에서 하드웨어, 가상, SaaS 엔드포인트를 구성하는 하이브리드 대시보드를 통해 이러한 모드를 계속 혼합하고 있습니다.

애플리케이션 딜리버리 컨트롤러(ADC) 시장은 유형(하드웨어 기반 ADC, 가상/소프트웨어 ADC), 전개(온프레미스, 클라우드 관리/호스팅), 구성 요소(솔루션(제어, 가속, 보안), 서비스(통합, 관리, 교육), 기업 규모(대기업, 중소기업), 최종 사용자 업종(IT 및 통신, BFSI 등), 지역별로 세분화됩니다. 시장 전망은 가치(USD) 기준으로 제공됩니다.

지역 분석

북미는 하이퍼스케일러 생태계와 통합 보안 요구사항을 강화하는 엄격한 데이터 개인정보 보호 규제의 영향으로 2024년 애플리케이션 딜리버리 컨트롤러 시장의 34%를 유지했습니다. F5가 수백 개의 시트릭스 넷스케일러 환경을 대체했다는 보도와 같은 통합 움직임은 성숙한 고객 계정 내에서의 이탈을 보여줍니다.

아시아태평양 지역은 5G 도입과 인더스트리 4.0 의제가 공장 및 스마트 시티 전반에 걸쳐 저지연, 멀티 테넌트 ADC 패브릭에 대한 수요를 촉진함에 따라 가장 가파른 12.8%의 CAGR을 기록합니다. 중국과 인도의 정부 클라우드 프로그램은 주권 클라우드 내에 ADC 기능을 내장하여 현지 벤더와의 협력을 촉진하고 있습니다.

유럽은 온프레미스와 클라우드 도입을 균형 있게 추진하며, 은행 및 핀테크 업그레이드에 영향을 미치는 DORA(데이터 보호 규정) 준수 기한이 이를 강화하고 있습니다. 규제 당국의 데이터 거주지(residence)에 대한 집중은 정책 기반 위치 제한(location fencing) 수요를 촉진합니다.

중동 및 아프리카 지역은 3조 7,000억 달러 규모의 메가 프로젝트 건설, IoT 기반 유틸리티, 전국적 디지털 정부 포털 구축을 위해 ADC를 활용합니다. 하이브리드 모델은 성능 요구와 제한된 지역 데이터센터 공간을 동시에 충족시킵니다.

남미의 금융 서비스 현대화와 소매 전자상거래가 점진적 도입을 촉진하며, 경제 변동성 속 자본 제약을 회피하기 위해 클라우드 기반 ADC가 선호됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 클라우드 네이티브 및 마이크로서비스 아키텍처로 전환

- 데이터센터 내 동서 방향 트래픽의 기하급수적 증가

- 북미 및 EU에서의 보안 디지털 뱅킹에 관한 규제 요건

- 아시아에서 5G 전개의 확대가 엣지 ADC 채택 촉진

- 세계 2000대 기업 간 멀티클라우드와 하이브리드 IT 전략 대두

- 시장 성장 억제요인

- 복잡한 레이어-7 정책 구성으로 인한 IT 운영 부담

- 고급 ADC 라이선싱 모델 비용 상승

- 기본 부하 분산 기능의 상품화

- 숙련된 NetOps 및 DevSecOps 인력 부족

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 업계에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 유형별

- 하드웨어 기반 ADC

- 가상/소프트웨어 ADC

- 전개별

- 온프레미스

- 클라우드 관리/호스트

- 컴포넌트별

- 솔루션(제어, 가속, 보안)

- 서비스(통합, 관리, 교육)

- 기업 규모별

- 대기업

- 중소기업

- 최종 사용자별

- IT 및 통신

- BFSI

- 소매업 및 전자상거래

- 헬스케어 및 생명과학

- 정부 및 공공 부문

- 제조업 및 인더스트리 4.0

- 미디어 및 엔터테인먼트

- 에너지 및 유틸리티

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 페루

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 전략적 개발

- 벤더 포지셔닝 분석

- 기업 프로파일

- F5 Networks Inc.

- NetScaler(Citrix Systems)

- Fortinet Inc.

- A10 Networks Inc.

- Array Networks Inc.

- Radware Ltd.

- Akamai Technologies Inc.

- Cisco Systems Inc.

- Barracuda Networks Inc.

- HAProxy Technologies LLC

- Kemp Technologies(Progress Software)

- Loadbalancer.org Inc.

- Cloudflare Inc.

- Dell Technologies Inc.

- Amazon Web Services(ALB/NLB)

- Microsoft Azure(Application Gateway)

- Alibaba Cloud(Global Server Load Balancer)

- Piolink Inc.

- Sangfor Technologies Inc.

- NGINX Inc.(F5)

제7장 시장 기회와 장래의 전망

HBR 25.11.19The application delivery controllers market size stands at USD 3.42 billion in 2025 and is set to reach USD 5.26 billion by 2030, expanding at an 8.98% CAGR.

Rapid migration to cloud-native architectures, rising east-west data-center traffic, and persistent multi-cloud strategies keep demand high for intelligent, security-aware traffic-management platforms. Vendors now bundle advanced Layer-7 security, API protection, and AI-assisted analytics into single offerings, allowing enterprises to improve user experience while containing risk. Hardware appliances still dominate performance-critical workloads, yet virtual and cloud-managed form factors are scaling faster as organizations prioritize agility and consumption-based economics. Regionally, North America leverages mature IT estates and regulatory tailwinds to hold leadership, while Asia-Pacific's 5G build-outs and digital initiatives create the steepest growth curve.

Global Application Delivery Controllers (ADC) Market Trends and Insights

Shift Toward Cloud-Native And Microservices Architecture

More than half of enterprise workloads already run as containerized or serverless components, forcing the application delivery controllers market to pivot toward lightweight, API-centric form factors that sit inside Kubernetes clusters and service meshes. These micro-gateways inject granular traffic steering, mutual-TLS termination, and automated scaling hooks that match the ephemeral nature of modern applications . Vendors are embedding schema-aware API firewalls and distributed rate-limiters to close security gaps opened by east-west service calls. As CIOs push for platform engineering, declarative "ADC-as-code" integrates seamlessly with GitOps pipelines, reducing hand-offs between Dev and NetOps.

Exponential East-West Data-Center Traffic Growth

Virtual server density has multiplied internal flows, outpacing traditional north-south patterns and elevating latency-sensitive micro-transactions. Distributed ADC instances now sit closer to workload pods, providing pervasive telemetry and inline decryption without introducing bottlenecks . Financial exchanges, telcos, and gaming providers deploy thousands of lightweight proxies that collectively enforce Layer-7 policies yet adapt to bursty resource pools.

Complex Layer-7 Policy Configuration Burdens IT Ops

Enterprise teams confront hundreds of heterogeneous applications, each demanding bespoke routing, rewrite, or WAF logic. Maintaining accuracy across multi-cloud estates strains scarce DevSecOps talent and can stall broader ADC roll-outs. Vendors answer with intent-based templates, AI-assisted rule creation, and visual dependency maps, yet skill gaps persist.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Secure Digital Banking

- Growing 5G Roll-outs Driving Edge ADC Adoption

- Cost Inflation of Advanced ADC Licensing Models

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware appliances represented 59% of the application delivery controllers market in 2024, supported by specialized SSL offload chips and deterministic throughput. Yet the virtual segment is scaling at 14.6% CAGR as DevOps teams embed ADC images directly into CI/CD pipelines, reducing rack footprint and accelerating rollout windows. The application delivery controllers market size for virtual solutions is forecast to surge alongside container adoption, challenging hardware's grip on mission-critical tiers.

Mature vendors hedge by releasing container-native proxies that inherit their policy engines while shedding appliance overhead. Cost transparency plus cloud marketplace billing appeal to agile teams, driving incremental share gains for software even inside traditional enterprises. As TLS 1.3 and QUIC adoption climb, code-level agility will further tilt decisions toward software form factors, though hardware will persist for ultra-high TPS gateways in finance and telecom cores.

On-premise instances still command 64% of the application delivery controllers market size in 2024, favored by sectors bound to data-sovereignty mandates. Integrated threat analytics modules and pay-as-you-grow capacity licensing now refresh legacy estates without forklift replacements .

Conversely, the cloud-managed model rises at 15.2% CAGR as platform teams offload patching, scaling, and telemetry to vendor-operated control planes. Multi-region rollouts complete in hours, and unified API policy enforcement eliminates site-level drift, making it the preferred path for digital-native firms. The application delivery controllers market continues to blend these modes through hybrid dashboards that configure hardware, virtual, and SaaS endpoints from a single console.

Application Delivery Controllers (ADC) Market is Segmented by Type (Hardware-Based ADC, Virtual/Software ADC), Deployment (On-Premise, Cloud-Managed/Hosted), Component (Solutions (Control, Acceleration, Security), Services (Integration, Managed, Training)), Enterprise Size (Large Enterprises, Smes), End-User Vertical (IT and Telecom, BFSI, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 34% of the application delivery controllers market in 2024, buoyed by hyperscaler ecosystems and stringent data-privacy regulations that elevate integrated security requirements. Consolidation plays, such as F5's reported displacement of hundreds of Citrix NetScaler estates, demonstrate churn within mature accounts.

Asia-Pacific delivers the steepest 12.8% CAGR as 5G rollouts and Industry 4.0 agendas spur demand for low-latency, multi-tenant ADC fabrics across factories and smart cities. Government cloud programs in China and India embed ADC functionality inside sovereign clouds, driving local vendor partnerships.

Europe balances on-prem and cloud adoption, reinforced by DORA compliance deadlines influencing bank and fintech upgrades. Regulators' focus on data residency fuels demand for policy-driven location fencing.

Middle East and Africa tap ADCs to underpin USD 3.7 trillion in megaproject construction, IoT-enabled utilities, and nationwide digital-government portals. Hybrid models satisfy both performance needs and limited regional data-center footprints.

South America's financial-services modernization and retail e-commerce spur incremental uptake, with cloud-based ADCs preferred to circumvent capital constraints amid economic volatility.

- F5 Networks Inc.

- NetScaler (Citrix Systems)

- Fortinet Inc.

- A10 Networks Inc.

- Array Networks Inc.

- Radware Ltd.

- Akamai Technologies Inc.

- Cisco Systems Inc.

- Barracuda Networks Inc.

- HAProxy Technologies LLC

- Kemp Technologies (Progress Software)

- Loadbalancer.org Inc.

- Cloudflare Inc.

- Dell Technologies Inc.

- Amazon Web Services (ALB / NLB)

- Microsoft Azure (Application Gateway)

- Alibaba Cloud (Global Server Load Balancer)

- Piolink Inc.

- Sangfor Technologies Inc.

- NGINX Inc. (F5)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Cloud-Native and Microservices Architecture

- 4.2.2 Exponential East-West Data-Center Traffic Growth

- 4.2.3 Regulatory Mandates for Secure Digital Banking in North America and EU

- 4.2.4 Growing 5G Roll-outs Driving Edge ADC Adoption in Asia

- 4.2.5 Rising Multi-Cloud and Hybrid IT Strategies among Global 2000

- 4.3 Market Restraints

- 4.3.1 Complex Layer-7 Policy Configuration Burdens IT Ops

- 4.3.2 Cost Inflation of Advanced ADC Licensing Models

- 4.3.3 Commoditization of Basic Load-Balancing Features

- 4.3.4 Shortage of Skilled NetOps and DevSecOps Talent

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of Macroeconomic Factors Impact on the Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware-Based ADC

- 5.1.2 Virtual/Software ADC

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud-Managed/Hosted

- 5.3 By Component

- 5.3.1 Solutions (Control, Acceleration, Security)

- 5.3.2 Services (Integration, Managed, Training)

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-user Vertical

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Retail and E-commerce

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Government and Public Sector

- 5.5.6 Manufacturing and Industrial 4.0

- 5.5.7 Media and Entertainment

- 5.5.8 Energy and Utilities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Peru

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 F5 Networks Inc.

- 6.3.2 NetScaler (Citrix Systems)

- 6.3.3 Fortinet Inc.

- 6.3.4 A10 Networks Inc.

- 6.3.5 Array Networks Inc.

- 6.3.6 Radware Ltd.

- 6.3.7 Akamai Technologies Inc.

- 6.3.8 Cisco Systems Inc.

- 6.3.9 Barracuda Networks Inc.

- 6.3.10 HAProxy Technologies LLC

- 6.3.11 Kemp Technologies (Progress Software)

- 6.3.12 Loadbalancer.org Inc.

- 6.3.13 Cloudflare Inc.

- 6.3.14 Dell Technologies Inc.

- 6.3.15 Amazon Web Services (ALB / NLB)

- 6.3.16 Microsoft Azure (Application Gateway)

- 6.3.17 Alibaba Cloud (Global Server Load Balancer)

- 6.3.18 Piolink Inc.

- 6.3.19 Sangfor Technologies Inc.

- 6.3.20 NGINX Inc. (F5)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment