|

시장보고서

상품코드

1687467

골판지 포장 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Corrugated Board Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

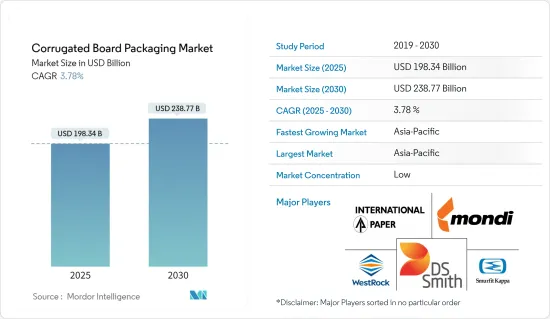

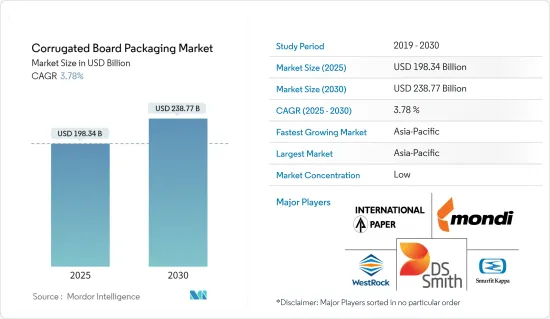

세계의 골판지 포장 시장 규모는 2025년 1,983억 4,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 3.78%로, 2030년에는 2,387억 7,000만 달러에 달할 것으로 예측되고 있습니다.

가혹한 취급에 대한 견고한 보호 기능을 가진 골판지는 선정된 패키지로 등장했습니다. 그 내구성, 다용도성, 안정성에 의해 골판지는 소매 섹터의 정평이 되고 있어, E-Commerce의 세계의 매출 급증에 수반해, 그 채용은 점점 강해지고 있습니다.

주요 하이라이트

- 방습성뿐만 아니라 장시간의 운송에도 견디는 골판지 포장에 주목하는 기업이 늘고 있습니다. 이 동향은 기업이 2차 포장이나 3차 포장에 골판지를 채용함으로써 현저해지고 있습니다. 수요의 급증은 주로 빵과 고기 제품과 같은 가공 식품과 부패하기 쉬운 식품에 의해 발생하며, 이들은 일회용 포장이 필요합니다. 게다가, 사람들의 라이프 스타일이 바빠지면서 편의점에 대한 욕구가 커지고 있습니다.

- 펄프 및 종이로 만든 골판지는 플라스틱으로 만든 것보다 재활용성이 우수합니다. 프루팅 가공이 베풀어진 골판지는 충격 흡수재로서 기능해, 외부로부터의 충격으로부터 내용물을 지킵니다. 골판지는 큰 압력을 견딜 수 있으며, 층상으로 다양한 두께의 플루트가 필수 불가결한 완충재가 됩니다. 전자상거래 부문은 최근 골판지의 압도적인 소비자로 부상했습니다. Amazon을 비롯한 대기업은 골판지를 1차 포장에 이용하는 한편, 개별 상품에는 플라스틱을 사용하고 있습니다.

- 이 시장에도 도전과 한계가 있습니다. 골판지에는 플라스틱이나 나무 상자와 같은 내구성이 없기 때문에 중량물이나 극단적인 압력에는 적합하지 않습니다. 일반적으로 장기적이고 재사용 가능한 투자보다는 단기 사용에 더 적합합니다.

- 골판지는 범용성이 있기 때문에 상자 등 다양한 형태로 성형할 수 있습니다. 지속가능성에 대한 관심이 높아짐에 따라 골판지는 점차적으로 연질 플라스틱 가방을 대체합니다. 게다가 다양한 인쇄 기술을 지원하기 때문에 기업에게는 매력적인 마케팅 도구이며, 여분의 마케팅 비용을 들이지 않고 모바일 광고 타워로서 효과적으로 역할을 합니다.

- 종이 및 재활용 소재와 같은 원료의 가용성과 가격 변동은 생산 및 가격 전략에 영향을 줄 수 있습니다. 종이 포장 산업은 산림 파괴로 인한 문제, 공급망 취약성, 환경 문제, 규제 문제, 지속 가능한 혁신의 긴급 추진에 힘쓰고 있습니다.

골판지 포장 시장 동향

가공 식품 부문이 큰 시장 점유율을 차지할 전망

- 골판지는 가공 식품 업계에서 인기있는 포장 옵션입니다. 상자의 크기와 모양에는 여러 가지가 있습니다. 고객은 잘 알려진 용기로 간식을 즐길 수 있습니다. 골판지로 포장 된 시리얼, 크래커 및 기타 스낵 과자의 소비는 몇 세대에 걸쳐 있습니다.

- 골판지 포장은 제품에서 습기를 멀리하고 장시간 배송을 견딜 수 있기 때문에 기업은 점점 더 많은 포장을 채택하고 특히 2 차 또는 3 차 포장에서 더 나은 고객 성과를 제공합니다. 빵, 고기 제품 및 기타 신선품과 같은 가공 식품은 이러한 포장재를 한 번만 사용해야 하므로 수요가 증가하고 있습니다.

- 2023년 9월 Jamestown Container가 발표한 바에 따르면, 골판지 식품 포장은 기존 소재를 대체하는 친환경 소재로 간주됩니다. 그 범용성은 신선한 식품, 구운 과자, 냉동·통조림 등 다양한 식품에 이릅니다. 골판지 포장의 높은 맞춤화를 통해 기업은 독특하고 시각적으로 매력적인 디자인을 만들 수 있습니다. 여기에는 브랜드 로고, 제품 세부사항 및 기타 브랜딩 요소를 상자에 직접 인쇄하고 브랜드 인지도를 높이고 제품 프레젠테이션을 향상시키는 것도 포함됩니다.

- 골판지 포장은 많은 식품에서 플라스틱 포장을 대체하는 효과적인 옵션이되고 있습니다. 고속 인터넷 서비스에 대한 액세스가 향상되고 전자 소매 및 전자상거래 채널이 등장하여 고객은 다양한 유형의 가공 식품을 온라인에서 더 쉽게 주문할 수 있습니다. 게다가 까다로운 절약과 편의성이 많은 소비자를 끌어당기고 있으며 예측기간을 통해 이 분야의 성장에 박차를 가하고 있습니다. 여기에는 치즈, 기성품 수프, 생선 통조림 등이 포함됩니다. 골판지 상자 포장은 재활용 소재와 퇴비화 소재에서보다 간단하게 만들 수 있습니다.

- 밀레니얼 세대를 비롯한 소비자들은 식품 포장, 생산, 폐기물이 환경에 미치는 영향에 대해 더 강하게 인식하고 있습니다. Stora Enso의 조사에 따르면, 밀레니얼 세대의 59%가 밸류체인 전반에 걸쳐 지속 가능한 포장이어야 한다고 생각합니다. 지속 가능한 포장 제품에 대한 수요는 가공 식품 포장의 주요 촉진요인이며 골판지 포장 시장의 성장에 긍정적인 영향을 미칩니다.

- 브라질의 종이 펄프 제조업체인 Suzanne와 유럽의 중요한 엔지니어링, 설계, 자문 서비스 회사인 AFRY에 따르면, 종이 및 판지의 세계 소비량은 2022년에는 4억 1,500만 톤이 될 것으로 예상되고 있습니다. 소비량은 향후 10년간 더 증가하고 2032년에는 4억 7,600만 톤에 달할 것으로 보입니다. 세계의 종이 및 판지 생산의 대부분은 패키징으로 소비되고 있습니다.

아시아태평양이 큰 점유율을 차지할 전망

- 아시아태평양 골판지 포장 시장은 도시화하는 인구와 환경 친화적 인 포장에 대한 의식이 높아짐에 따라 성장합니다. 주요 산업 동향은 골판지 생산 능력 증가와 기술의 진보를 포함합니다. 그러나 엄격한 규제 및 제품 품질에 대한 우려가 이러한 성장을 방해할 수 있습니다.

- 아시아 골판지 포장 시장의 성장 가속은 지속가능한 포장에 대한 수요 급증, 전자상거래 부문의 활황, 전자 및 개인 관리 제품에 대한 수요 증가, 경제 개척에 따른 1인당 소득 상승으로 추진되고 있습니다.

- 1인당 소득 상승과 인구동태 변화가 중국의 골판지 포장 부문을 형성하고 새로운 포장 재료와 포장 공정이 필요합니다. Alibaba와 같은 전자상거래 대기업이 골판지 시장을 견인하는 태세를 갖추고 있습니다. 국제무역국은 중국이 세계 전자상거래 시장을 독점하고 있으며 거래 총액의 약 50%를 차지하고 있다고 보고했습니다. 온라인 소매 거래는 2024년까지 3조 5,600억 달러에 달할 것으로 예측되고 있으며, 이 붐은 지속 가능한 패키징 솔루션에 대한 수요를 증폭시켜 골판지 패키지의 매출을 밀어올릴 것으로 보입니다.

- 인도, 중국, 일본 등의 국가에서는 음식, IT전자, 가전제품 등 골판지에 크게 의존하는 산업이 소비업그레이드의 동향을 경험하고 있습니다. 이러한 주요 최종 사용자 산업의 변화는 중·고급 골판지 시장을 밀어올릴 것으로 예상됩니다.

- 게다가, 골판지 포장 시장의 성장은 아시아태평양 국가에서 원재료의 가용성, 일회용 플라스틱을 억제하는 정부 규제 및 이들 국가에서 최종 사용 산업 증가로 인해 박차를 받고 있습니다.

골판지 포장 산업 개요

골판지 포장 시장은 단편화되어 있으며 Mondi Group, DS Smith PLC, WestRock Company, Smurfit Kappa Group과 같은 기업과 그 외에도 많은 기업이 있습니다. 이러한 기업들은 지속 가능성을 지원하기 위해 친환경 포장 제품을 혁신하고 출시하고 있습니다. 또한 다양한 최종 사용자 산업에 맞는 맞춤형 골판지 상자 디자인을 선보이며 새로운 기회를 포착하고 있습니다. 또한 골판지 포장 분야에서 주요 업체들이 포트폴리오를 강화하면서 파트너십과 인수가 활발하게 이루어지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 친환경 소재의 채용 확대와 골판지의 디지털 인쇄의 진화

- 전자상거래 분야의 왕성한 수요

- 시장 성장 억제요인

- 리터너블 포장과 재사용 가능 포장 증가

제6장 시장 세분화

- 최종 사용자 산업별

- 가공식품

- 신선식품 및 청과

- 음료

- 퍼스널케어와 하우스 홀드 케어

- 전자상거래

- 기타 최종 사용자 산업(전기 및 전자, 헬스케어, 공업, 섬유, 유리 및 세라믹)

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 폴란드

- 아시아

- 중국

- 인도

- 일본

- 한국

- 인도네시아

- 태국

- 호주 및 뉴질랜드

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 북미

제7장 경쟁 구도

- 기업 프로파일

- International Paper Company

- Mondi Group

- DS Smith PLC

- WestRock Company

- Smurfit Kappa Group

- Stora Enso Oyj

- Sealed Air Corporation

- Asia Pulp & Paper(APP) Sinar Mas

- Napco National

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings Limited

- Oji Holdings Corporation

제8장 투자 분석

제9장 시장 전망

JHS 25.04.01The Corrugated Board Packaging Market size is estimated at USD 198.34 billion in 2025, and is expected to reach USD 238.77 billion by 2030, at a CAGR of 3.78% during the forecast period (2025-2030).

With its robust protection against harsh handling, the corrugated board has emerged as the packaging of choice. Its durability, versatility, and stability make it a staple in the retail sector, and with the global surge in e-commerce sales, its adoption is only intensifying.

Key Highlights

- Businesses increasingly turn to corrugated board packaging, not only for its moisture protection but also for its resilience during extended transportation. This trend is significantly pronounced as companies adopt it for secondary and tertiary packaging. The surge in demand is primarily driven by processed and perishable foods, like bread and meat products, which necessitate single-use packaging. Additionally, as people's lifestyles grow busier, the appetite for convenience foods rises.

- Crafted from pulp and paper, corrugated boards boast a recyclability edge over their plastic counterparts. The fluting medium acts as a shock absorber, safeguarding contents from external impacts. These boards can endure significant pressure, and their layered and varied-thickness flutes provide essential cushioning. The e-commerce sector has recently emerged as a dominant consumer of corrugated boards. Major players, including Amazon, utilize these boards for primary packaging while reserving plastic for individual items.

- The market also has challenges and limitations. The corrugated board lacks the durability of plastic or wooden boxes, making them less suitable for heavy items or extreme pressures. Typically, it's favored for short-term use rather than as long-term, reusable investments.

- Their versatility allows corrugated boards to be molded into various shapes, including boxes. As sustainability concerns mount, they're gradually replacing flexible plastic bags. Furthermore, their compatibility with diverse printing techniques makes them an attractive marketing tool for companies, effectively serving as mobile billboards without incurring extra marketing costs.

- Variations in the availability and pricing of raw materials, such as paper and recycled content, can influence production and pricing strategies. The paper packaging industry grapples with challenges stemming from deforestation, encompassing supply chain vulnerabilities, environmental issues, regulatory challenges, and an urgent push for sustainable innovations.

Corrugated Board Packaging Market Trends

Processed Food Segment Expected to Occupy Significant Market Share

- The corrugated board is a popular packaging choice in the processed food industry. There are many different sizes and shapes of boxes. Customers are given a well-known container to enjoy their snacking in. The consumption of cereal, crackers, and other snack foods packaged in corrugated boards spans several generations.

- The corrugated board packaging keeps moisture away from products and can withstand long shipping times, companies are increasingly adopting this packaging to offer better customer outcomes, especially for secondary or tertiary packaging. Processed foods, such as bread, meat products, and other perishable items, need these packaging materials to be used just once, thus driving the demand.

- According to Jamestown Container in September 2023, corrugated food packaging is increasingly considered an eco-friendly alternative to conventional materials. Its versatility spans various food products, including fresh produce, baked goods, and frozen and canned items. The high customizability of corrugated packaging allows businesses to craft distinctive and visually appealing designs. This includes printing brand logos, product details, and other branding elements directly onto the boxes, enhancing brand recognition, and elevating product presentation.

- Corrugated board packaging is becoming a viable alternative to plastic packaging for many food products. Due to the rising accessibility of high-speed internet services and the rise of e-retail and e-commerce channels has been sparked, making it more straightforward for customers to order various kinds of processed food goods online. In addition, the generous savings and convenience it offers draw more consumers, adding to the segment's growth throughout the forecast period. These include cheese, ready-made soups, and canned fish, among others. Corrugated box packaging can be created more simply from recycled or composted materials.

- Consumers, such as millennials, are becoming more aware of the environmental impact of food packaging, production, and waste. According to a Stora Enso survey, 59% of millennials think packaging should be sustainable throughout the value chain. Demand for sustainable packaging products is a key driver in processed food packaging, positively impacting corrugated board packaging market growth.

- According to Suzanne, a Brazilian pulp and paper producer, and AFRY, a critical European engineering, design, and advisory services firm, the global consumption of paper and paperboard was expected to be 415 million tonnes in 2022. Consumption will rise further over the next decade, reaching 476 million tonnes by 2032. Packaging consumes the majority of worldwide paper and paperboard production.

Asia Pacific is Expected to Hold a Significant Share

- Asia Pacific's corrugated board packaging market is set to grow, driven by an urbanizing population and heightened awareness of eco-friendly packaging. Key industry trends include increased containerboard capacity and technological advancements. However, stringent regulations and product quality concerns could hinder this growth.

- Accelerated growth in Asia's corrugated board packaging market is fueled by a surge in demand for sustainable packaging, a booming e-commerce sector, heightened demand for electronics and personal care products, and rising per capita income amid economic development.

- Rising per capita income and shifting demographics shape China's corrugated board packaging sector, necessitating new packaging materials and processes. E-commerce giants like Alibaba are poised to drive the corrugated packaging market. The International Trade Administration reported that China dominates the global e-commerce landscape, accounting for about 50% of total transactions. With projections of online retail transactions hitting USD 3.56 trillion by 2024, this boom is set to amplify the demand for sustainable packaging solutions, bolstering sales of corrugated board packaging.

- In countries like India, China, and Japan, industries such as food and beverage, IT electronics, and home appliances, which heavily rely on corrugated boxes, are experiencing a trend of consumption upgrading. This shift in leading end-user industries is anticipated to boost the market for mid to high-end corrugated cartons.

- Additionally, the growth of the corrugated board packaging market is spurred by the availability of raw materials in Asia Pacific nations, government regulations curbing single-use plastics, and a rising number of end-use industries across these countries.

Corrugated Board Packaging Industry Overview

The corrugated board packaging market is fragmented, with numerous players such as Mondi Group, DS Smith PLC, WestRock Company, Smurfit Kappa Group, and more offering diverse solutions. These companies are innovating and rolling out eco-friendly packaging products to support sustainability. Additionally, they're unveiling tailored corrugated box designs catering to various end-user industries, seizing emerging opportunities. Furthermore, the market is seeing a flurry of partnerships and acquisitions as key players bolster their portfolios in the corrugated board packaging arena.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Eco-friendly Materials and Evolution of Digital Print for Corrugated Boards

- 5.1.2 Strong Demand from the E-commerce Sector

- 5.2 Market Restraint

- 5.2.1 Increasing Usage of Returnable and Reusable Packaging

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Processed Foods

- 6.1.2 Fresh Food and Produce

- 6.1.3 Beverages

- 6.1.4 Personal and Household Care

- 6.1.5 E-commerce

- 6.1.6 Other End-user Industries (Electrical & Electronics, Healthcare, Industrial, Textile, Glass & Ceramics)

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Spain

- 6.2.2.6 Poland

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 South Korea

- 6.2.3.5 Indonesia

- 6.2.3.6 Thailand

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.5.2 Argentina

- 6.2.5.3 Mexico

- 6.2.6 Middle East and Africa

- 6.2.6.1 Saudi Arabia

- 6.2.6.2 South Africa

- 6.2.6.3 United Arab Emirates

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Paper Company

- 7.1.2 Mondi Group

- 7.1.3 DS Smith PLC

- 7.1.4 WestRock Company

- 7.1.5 Smurfit Kappa Group

- 7.1.6 Stora Enso Oyj

- 7.1.7 Sealed Air Corporation

- 7.1.8 Asia Pulp & Paper (APP) Sinar Mas

- 7.1.9 Napco National

- 7.1.10 Georgia-Pacific LLC

- 7.1.11 Nine Dragons Paper Holdings Limited

- 7.1.12 Oji Holdings Corporation