|

시장보고서

상품코드

1851037

자율형 항공기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Autonomous Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

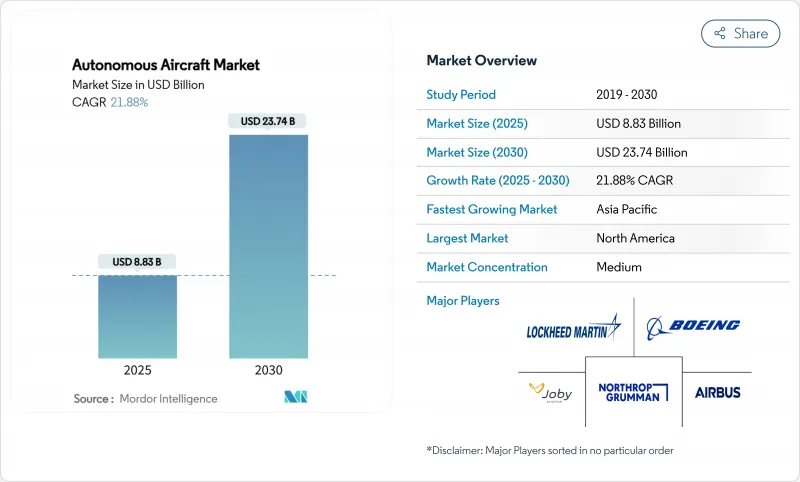

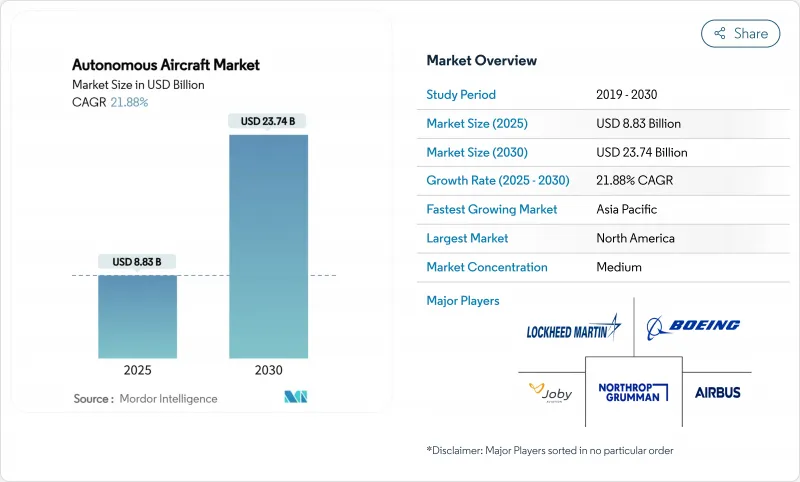

자율형 항공기 시장 규모는 2025년 88억 3,000만 달러, 2030년 237억 4,000만 달러에 이를 것으로 예상되며, CAGR은 21.88%를 나타낼 전망입니다.

국방 근대화, 도시 이동 계획, 물류 자동화의 파도가 항공 경제를 재구성하고 점차 자기 관리 플랫폼에 대한 수요를 높이고 있습니다. 고정 날개 기계 구성이 현재 주류를 차지하고 있지만 항공사와 군가 다목적 중거리 솔루션을 선호하고 있음을 반영하여 하이브리드 고정 날개 VTOL 기계가 성장 곡선을 이끌고 있습니다. 방위기관에 의한 공동 전투기나 ISR 무인기에 대한 급속한 투자는 기술의 준비 태세를 가속시킵니다. 동시에 도심항공모빌리티(UAM) 프로그램은 시선을 넘어선 코리도와 버티포트의 건설을 촉진합니다. AI 통합의 심화는 완전한 자율 운용을 가능하게 해, 화물, 여객, 특수 임무의 각 이용 사례로 대응 가능한 범위를 넓힙니다. 기존의 터빈 엔진은 여전히 주요 추진 기반이지만 지속가능성 의무화가 강화됨에 따라 수소 연료전지와 첨단 전기 시스템에 자본이 모여 있습니다.

세계의 자율형 항공기 시장 동향과 인사이트

AI 구동 비행 제어 시스템의 진보

실시간 머신러닝 알고리즘은 파일럿 개입 없이 전술적 조종, 장애물 회피, 루트 최적화를 유도합니다. 서브의 자율형 그리펜 E의 시험에서는 전투기 레벨의 AI가 순간의 판단을 실행해, 룰 베이스의 자동화로부터 적응적인지에의 이행을 검증하고 있습니다. 2024년 6월에 발표된 FAA의 AI 안전 보증 로드맵은 정적으로 훈련된 AI와 지속적으로 학습하는 AI의 인증 단계를 간략히 설명하고 민간 항공기를 위한 진도의 길을 명확히 했습니다. 미국 공군의 공동 전투기와 같은 밀리초 단위의 판단 루프를 요구하는 전투 프로그램은 입증된 아키텍처를 상용 시스템에 파급시켜 화물 오퍼레이터나 신흥의 에어택시 플릿이 내비게이션, 센스 앤 아보이드, 헬스 모니터링 기능을 위한 강화된 AI 스택을 계승하는 것을 계승합니다.

도시 지역의 항공 이동성 급성장 및 eVTOL 채택

대도시 계획 담당자는 3차원 이동성을 혼잡 완화와 지역 연결성의 테코로 간주하게 되어 있습니다. 버티컬 에어로스페이스는 2028년까지 VX4 인증을 취득하기 위해 하니웰에서 10억 달러의 어비오닉스 주문을 확약했으며, 이는 공급망에 대한 신뢰의 증거입니다. 일본 최초의 eVTOL 노선은 2028년 오사카 박람회를 목표로 하고 있으며, 스카이 드라이브는 300대 이상의 임시 수주를 획득하여 선진 항공모빌리티에 대한 국가의 우선순위를 일치시키고 있습니다. 도시 에어포트와 같은 버티포트 개발업체가 에너지, 유지보수, 항공 교통 서비스를 번들로 제공하는 200곳을 계획하고 있기 때문에 네트워크 효과가 증폭되고 있습니다. 규제 장애물이 완화됩니다. EASA가 VTOL 패키지를 발표하고 FAA의 파워 드리프트 최종 규칙이 파일럿 면허를 명확히 함에 따라 활주로가 없는 항공기는 확장된 서비스로 향하고 있습니다. 개선된 배터리와 인증된 자율성은 시간을 절약하여 할인된 운임을 정당화할 수 있는 20-100마일의 도시 간 이동을 위한 비즈니스 사례를 지원합니다.

인증 및 공역 통합의 규제 복잡성

전통적인 항공 규칙은 탑승자를 태울 수 없는 항공기에 맞추기 위해 고생하고 있습니다. FAA는 2026년까지 종합적인 BVLOS 규정을 발표하는 것을 목표로 하고 있으며, 현재 면제에 근거한 운항을 일상적인 상업 레인으로 확대합니다. EASA의 인증 카테고리는 유인기와 유사한 형식 증명 및 운항 승인을 요구하며, 자율화 프로그램을 몇 년의 타임라인으로 연장합니다. 국경을 넘는 루트는 하모나이제이션이 아직 부분적이기 때문에 복잡성을 늘리고 제조자는 병행하여 허가를 추구하게 됩니다. 항공 교통 통합은 또한 기존의 ATC와 원활하게 인터페이스해야 하는 무인 교통 관리 시스템에 달려 있습니다. 자원에 제약이 있는 신흥기업은 인증 취득까지의 긴 길의 자금 반복에 고생하는 경우가 많고, 경쟁 우위는 기존의 항공우주 프라임에 기울입니다.

부문 분석

2024년 자율형 항공기 시장의 51.08%를 고정익기가 차지해 장거리 ISR이나 화물 미션에 있어서의 공력 효율과 항속 거리의 우위성이 강조되었습니다. General Atomics사의 MQ-20 Avenger의 업그레이드는 레거시 기체에 완전한 자율성을 갖게 하는 개조가 가능함을 증명해, 능력을 향상시키면서 라이프 사이클 비용을 낮게 억제할 수 있습니다. 그러나 하이브리드 고정익 VTOL 시스템의 CAGR은 26.89%로 함대 계획자가 순항 성능을 유지하면서 활주로에 의존하지 않는 운용을 원한다는 것을 보여줍니다. 도시 네트워크가 수직 상승하면서 200노트의 순항 속도를 유지하는 항공기를 요구하고 있기 때문에 하이브리드 VTOL 플랫폼과 관련된 자율형 항공기 시장 규모가 급격히 확대되고 있습니다.

하이브리드 VTOL의 성장은 보잉의 MQ-25 스팅레이와 같은 방위 보급 개념에서 비롯됩니다. 회전익기는 응급구명과 소화활동 등 호버링을 많이 사용하는 작업에서 틈새 역할을 담당하고 있지만, 틸트 로터와 틸트 윙 아키텍처는 현재 도달범위를 확대하면서 비슷한 수직 방향의 민첩성을 제공합니다. 설계를 결합하여 광대한 활주로와 밀집한 도시 중심부의 갭을 메우고, 인프라의 제약을 완화하고, 미션 세트를 확대할 수 있습니다.

2024년에는 자율성이 높다고 분류되는 플랫폼이 액티브 납품기의 68.45%를 차지했으며, 규제 당국과 운영자가 급격한 도약보다 단계적인 기능 업그레이드를 선호한다는 것을 반영했습니다. AeroVironment 사의 ARK와 같은 개장 가능한 키트는 기존 플릿에 고급 자율성을 추가하여 운영자가 새로운 유형의 인증을 받지 않고 이점을 수확할 수 있도록 합니다. 완전 자율 시스템은 AI 신뢰성, 센서 퓨전 및 클라우드 연결이 수렴함에 따라 CAGR 27.75%를 나타낼 전망입니다.

완전 자율형 선박의 자율형 항공기 시장 규모는 모니터링된 운영 데이터를 통해 규제 당국의 신뢰가 높아짐에 따라 확대됩니다. 옵션으로 탑승자를 태우는 설계를 채용하는 군사 프로그램은 지각 스택에 실세계의 스트레스 테스트를 제공하여 기술의 성숙을 가속화합니다. 민간에서는 Joby Aviation이 Xwing의 자율성 부문을 인수함에 따라 여객 서비스를 위한 턴키 AI 비행 데크에 자본이 모여 있는 것이 부각되었습니다. 예측기간 동안 인간에 의한 온더 루프 거버넌스는 점차 예외만의 개입으로 이행하여 운항비용 절감과 24시간 365일 가동 확대가 진행될 것으로 보입니다.

지역 분석

북미는 2024년 세계 매출의 37.23%를 차지했습니다. 미국 방총성이 전투기와 고고도 ISR 무인기의 공동 개발에 자금을 제공하는 것이 국내 수요를 뒷받침하는 한편 FAA의 규제 주도가 세계 인증 경로를 형성합니다. 보잉, 록히드 마틴, 노스롭 그라만과 같은 대기업은 AI 벤처기업과 제휴해 파일럿리스 전투기나 택배 드론을 개발해 대학에서 실리콘 밸리의 연구소에 이르는 인재 파이프라인을 충실히 하고 있습니다. 캐나다는 아비오닉스와 복합재 제조로 공급을 강화하고, 멕시코는 국경을 넘은 프로그램에 공급하는 비용 효율적인 조립 라인을 보유하고 있습니다. 자율형 항공기 시장 규모는 명확한 BVLOS의 틀에 따라 방위 예산과 도시 이동성 조종사가 성숙함에 따라 더욱 확대될 것으로 보입니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 24.37%로 가장 급성장하고 있는 분야입니다. 중국의 저고도 경제계획은 2025년까지 1조 5,000억 위안의 항공 생산을 목표로 하고 있으며, EHang사의 허페이 공장과 같은 eVTOL 생산 거점에 보조금을 투입하고 있습니다. 일본에서는 2028년 오사카 박람회에 맞추어 상업용 에어택시의 취항을 목표로 하고 있으며, 버티포트의 조닝이나 자율 비행 시험에 관한 관민 협조에 스포트라이트가 적용되고 있습니다. 한국 인천을 중심으로 하는 버티포트 그리드와 호주 전동 에어택시의 실현 가능성 연구는 지역 실험을 확대합니다. 인도의 방위 연구개발 장려책과 위성 연결성의 향상은 원격지에서의 자율형 ISR과 화물 운송의 기회를 개방하는 것으로, 동남아시아는 군도적인 지형 중의 의료 보급을 위한 드론에 주목하고 있습니다.

유럽은 엄격한 안전문화와 지속가능성 요청의 균형을 유지하면서 전략적 발판을 유지하고 있습니다. EASA의 점진적인 VTOL 규정은 독일, 프랑스, 영국의 도시 계획자들에게 세계적인 벤치마크를 정의하고 신뢰성을 뒷받침하며, 각각 볼로콥터와 버티컬 에어로스페이스의 eVTOL 프로토타입을 받아들입니다. 지역 펀드는 수소 추진과 재활용이 가능한 구조를 대상으로 하며 유럽의 OEM은 에코 중심 입찰로 우위를 차지할 수 있습니다. 이탈리아의 전국적인 버티포트 코리도 계획과 스웨덴의 자율적인 스웜 시험은 유럽 대륙의 민간과 군사의 이중 추진력을 반영합니다. 이 대륙의 성장은 APAC보다 느리지만, 정책적 영향력과 탄소 목표는이 대륙을 중요한 참고 시장으로 자리 매김하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- AI에 의한 비행 제어 시스템의 진보

- 도심항공모빌리티(UAM)와 eVTOL의 급속한 보급

- 자율형화물 드론에 의한 물류의 비용 절감 인센티브

- ISR과 전투 자동화에 대한 군사 투자 증가

- BVLOS 에어코리도와 무인교통관리(UTM)의 전개

- 비행 인증을 받은 자율형 어비오닉스와 센서 스위트의 가용성 증가

- 시장 성장 억제요인

- 인증과 공역 통합에 있어서 규제의 복잡성

- 배터리 기술의 한계와 높은 자본 비용

- 사이버 위협이나 시스템 탈취에 대한 취약성 증가

- AI 처리 장치에 영향을 미치는 반도체 공급의 혼란

- 밸류체인 분석

- 기술의 전망

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력/소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 항공기 유형별

- 고정익

- 회전익

- 하이브리드(고정익 VTOL)

- 자율성 수준별

- 점진적 자율성

- 완전 자율성

- 용도별

- 화물 항공기

- 여객 항공기

- 특수 임무/ISR

- 항공 택시/UAM

- 추진 유형별

- 기존 터빈

- 전기

- 하이브리드 전기

- 수소 연료전지

- 구성 요소별

- 비행 제어 컴퓨터

- 센서 및 내비게이션

- 통신 및 데이터 링크

- 소프트웨어 및 AI 알고리즘

- 추진 시스템

- 기체 및 구조

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Northrop Grumman Corporation

- The Boeing Company

- Lockheed Martin Corporation

- RTX Corporation

- Elbit Systems Ltd.

- AeroVironment, Inc.

- Saab AB

- BAE Systems plc

- Airbus SE

- Textron Inc.

- Israel Aerospace Industries Ltd.

- General Atomics

- Joby Aviation, Inc.

- Volocopter Technologies GmbH

- Guangzhou EHang Intelligent Technology Co. Ltd.

- Archer Aviation Inc.

- Wisk Aero LLC

- Kratos Defense & Security Solutions Inc.

- Kaman Corporation

제7장 시장 기회와 향후 전망

KTH 25.11.11The autonomous aircraft market size stands at USD 8.83 billion in 2025 and is projected to reach USD 23.74 billion by 2030, equating to a vigorous 21.88% CAGR.

A wave of defense modernization, urban mobility plans, and logistics automation is reshaping aviation economics and elevating demand for progressively self-directed platforms. Fixed-wing configurations command present dominance, yet hybrid fixed-wing VTOL aircraft lead the growth curve, reflecting airlines' and militaries' preference for versatile mid-range solutions. Rapid investments by defense agencies in collaborative combat aircraft and ISR drones accelerate technology readiness. At the same time, urban air mobility (UAM) programs foster beyond-visual-line-of-sight corridors and vertiport construction. Deepening AI integration helps unlock fully autonomous operations and widens the addressable envelope across cargo, passenger, and special-mission use cases. Conventional turbine engines remain the primary propulsion base, but hydrogen fuel-cell and advanced electric systems draw rising capital as sustainability mandates tighten.

Global Autonomous Aircraft Market Trends and Insights

Advancements in AI-Driven Flight Control Systems

Real-time machine-learning algorithms guide tactical maneuvers, obstacle avoidance, and route optimization without pilot intervention. Saab's autonomous Gripen E trials illustrate fighter-grade AI executing split-second decisions, validating moves from rule-based automation to adaptive cognition. The FAA's AI Safety Assurance Roadmap, released in June 2024, outlines certification tiers for statically trained and continuously learning AI, clearing a progression path for civil fleets. Combat programs demanding millisecond decision loops, such as the US Air Force's collaborative combat aircraft, spill proven architectures into commercial systems, enabling cargo operators and emerging air-taxi fleets to inherit hardened AI stacks for navigation, sense-and-avoid, and health-monitoring functions.

Rapid Growth in Urban Air Mobility and eVTOL Adoption

Metropolitan planners increasingly view three-dimensional mobility as a lever for congestion relief and regional connectivity. Vertical Aerospace committed USD 1 billion of Honeywell avionics orders to certify the VX4 by 2028, a signal of supply-chain confidence. Japan's first eVTOL routes target the 2028 Osaka Expo, with SkyDrive capturing over 300 provisional orders, aligning national priorities for advanced air mobility. Network effects amplify as vertiport developers such as Urban-Air Port plan 200 sites that bundle energy, maintenance, and air-traffic services. Regulatory hurdles ease: EASA released its VTOL package, and the FAA's powered-lift final rule clarifies pilot licensing, paving the runway-free aircraft toward scaled service. Improved batteries and certified autonomy underpin business cases for 20-100-mile urban hops where time savings justify premium fares.

Regulatory Complexity in Certification and Airspace Integration

Legacy aviation rules struggle to fit aircraft with no onboard crew. The FAA aims to publish comprehensive BVLOS regulations by 2026, extending present waiver-based operations into routine commercial lanes. EASA's certified category demands type certificates and air operator approvals similar to manned fleets, stretching autonomous programs to multi-year timelines. Cross-border routes magnify complexity because harmonization remains partial, pushing manufacturers to chase parallel approvals. Air-traffic integration further hinges on unmanned-traffic-management systems that must interface seamlessly with conventional ATC. Resource-constrained startups often struggle to fund long certification paths, tilting competitive advantage toward incumbent aerospace primes.

Other drivers and restraints analyzed in the detailed report include:

- Cost Reduction Incentives for Logistics via Autonomous Cargo Drones

- Increased Military Investments in ISR and Combat Autonomy

- Limitations in Battery Technology and High Capital Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed-wing models accounted for 51.08% of the autonomous aircraft market 2024, underscoring their aerodynamic efficiency and range advantages for long-haul ISR and cargo missions. General Atomics' MQ-20 Avenger upgrade proves that legacy airframes can be retrofitted with full autonomy, keeping lifecycle costs low while enhancing capability. Hybrid fixed-wing VTOL systems, however, register a 26.89% CAGR, indicating fleet planners' appetite for runway-independent operations that preserve cruise performance. The autonomous aircraft market size attached to hybrid VTOL platforms will broaden sharply as urban networks demand aircraft that lift vertically yet sustain 200-knot cruise.

Hybrid VTOL growth also springs from defense refueling concepts such as Boeing's MQ-25 Stingray, which proves carrier compatibility without deck-space penalties. Rotary-wing craft hold niche roles for hover-intensive tasks like medevac and firefighting, but tilt-rotor and tilt-wing architectures now offer similar vertical dexterity with extended reach. Combining designs bridges the gap between sprawling runways and tightly packed city cores, easing infrastructure constraints and expanding mission sets.

In 2024, platforms classed as increasingly autonomous made up 68.45% of active deliveries, reflecting regulators' and operators' preference for step-wise feature upgrades over radical leaps. Retrofittable kits such as AeroVironment's ARK add advanced autonomy to existing fleets, enabling operators to harvest benefits without new-type certification. Fully autonomous systems-still a smaller slice-are growing at 27.75% CAGR as AI reliability, sensor fusion, and cloud connectivity converge.

The autonomous aircraft market size for fully autonomous craft will expand as regulatory confidence builds through supervised operations data. Military programs embracing optionally crewed designs provide real-world stress tests for perception stacks, accelerating tech maturity. On the civil side, Joby Aviation's takeover of Xwing's autonomy division highlights capital gravitating toward turnkey AI flight decks aimed at passenger services. Over the forecast period, human-on-the-loop governance will gradually yield to exception-only intervention, cutting operating costs and extending 24/7 utilization.

The Autonomous Aircraft Market Report is Segmented by Aircraft Type (Fixed-Wing, Rotary-Wing, and Hybrid (VTOL)), Autonomy Level (Increasingly Autonomous, and Fully Autonomous), Application (Cargo Aircraft, and More), Propulsion Type (Conventional Turbine, Electric, and More), Component (Flight Control Computers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 37.23% of global revenue in 2024. Pentagon funding for collaborative combat aircraft and high-altitude ISR drones underpins domestic demand, while the FAA's regulatory leadership shapes global certification pathways. Major primes-Boeing, Lockheed Martin, Northrop Grumman-pair with AI start-ups to field pilotless fighters and delivery drones, enriching a talent pipeline spanning universities to Silicon Valley labs. Canada bolsters supply with avionics and composite manufacturing, and Mexico hosts cost-effective assembly lines that feed cross-border programs. The autonomous aircraft market size will continue to compound as defense appropriations and urban mobility pilots mature under clarified BVLOS frameworks.

Asia-Pacific is the fastest-growing arena at 24.37% CAGR through 2030. China's low-altitude economy plan, which targets 1.5 trillion yuan aviation output by 2025, funnels subsidies into eVTOL production bases such as EHang's Hefei plant. Japan aims for commercial air-taxi launches coinciding with the 2028 Osaka Expo, spotlighting public-private coordination on vertiport zoning and autonomous flight-testing. South Korea's Incheon-centered vertiport grid and Australia's electric air-taxi feasibility studies widen regional experimentation. India's defense R&D incentives and increasing satellite connectivity open opportunities for autonomous ISR and cargo operations in remote terrain, while Southeast Asia eyes drones for medical resupply amid archipelagic geography.

Europe maintains a strategic foothold, balancing a stringent safety culture with sustainability imperatives. EASA's phased VTOL regulations define global benchmarks and anchor confidence for city planners across Germany, France, and the United Kingdom, each hosting eVTOL prototypes from Volocopter and Vertical Aerospace. Regional funds target hydrogen propulsion and recyclable structures, giving European OEMs an edge in eco-centric tenders. Italy's plan for nationwide vertiport corridors and Sweden's autonomous swarm trials echo the continent's dual civilian-military thrust. Although the continent grows more slowly than APAC, its policy influence and carbon targets position it as a key reference market.

- Northrop Grumman Corporation

- The Boeing Company

- Lockheed Martin Corporation

- RTX Corporation

- Elbit Systems Ltd.

- AeroVironment, Inc.

- Saab AB

- BAE Systems plc

- Airbus SE

- Textron Inc.

- Israel Aerospace Industries Ltd.

- General Atomics

- Joby Aviation, Inc.

- Volocopter Technologies GmbH

- Guangzhou EHang Intelligent Technology Co. Ltd.

- Archer Aviation Inc.

- Wisk Aero LLC

- Kratos Defense & Security Solutions Inc.

- Kaman Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancements in AI-driven flight control systems

- 4.2.2 Rapid growth in Urban Air Mobility (UAM) and eVTOL adoption

- 4.2.3 Cost reduction incentives for logistics via autonomous cargo drones

- 4.2.4 Increased military investments in ISR and combat autonomy

- 4.2.5 Deployment of BVLOS air corridors and Unmanned Traffic Management (UTM)

- 4.2.6 Increased availability of flight-certified autonomous avionics and sensor suites

- 4.3 Market Restraints

- 4.3.1 Regulatory complexity in certification and airspace integration

- 4.3.2 Limitations in battery technology and high capital costs

- 4.3.3 Heightened vulnerability to cyber threats and system hijacking

- 4.3.4 Semiconductor supply disruptions affecting AI processing units

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Fixed-wing

- 5.1.2 Rotary-wing

- 5.1.3 Hybrid (Fixed-Wing VTOL)

- 5.2 By Autonomy Level

- 5.2.1 Increasingly Autonomous

- 5.2.2 Fully Autonomous

- 5.3 By Application

- 5.3.1 Cargo Aircraft

- 5.3.2 Passenger Aircraft

- 5.3.3 Special Mission/ISR

- 5.3.4 Air Taxi/UAM

- 5.4 By Propulsion Type

- 5.4.1 Conventional Turbine

- 5.4.2 Electric

- 5.4.3 Hybrid-Electric

- 5.4.4 Hydrogen Fuel-cell

- 5.5 By Component

- 5.5.1 Flight Control Computers

- 5.5.2 Sensors and Navigation

- 5.5.3 Communication and Data Links

- 5.5.4 Software and AI Algorithms

- 5.5.5 Propulsion Systems

- 5.5.6 Airframe and Structure

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Italy

- 5.6.2.5 Russia

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Northrop Grumman Corporation

- 6.4.2 The Boeing Company

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 RTX Corporation

- 6.4.5 Elbit Systems Ltd.

- 6.4.6 AeroVironment, Inc.

- 6.4.7 Saab AB

- 6.4.8 BAE Systems plc

- 6.4.9 Airbus SE

- 6.4.10 Textron Inc.

- 6.4.11 Israel Aerospace Industries Ltd.

- 6.4.12 General Atomics

- 6.4.13 Joby Aviation, Inc.

- 6.4.14 Volocopter Technologies GmbH

- 6.4.15 Guangzhou EHang Intelligent Technology Co. Ltd.

- 6.4.16 Archer Aviation Inc.

- 6.4.17 Wisk Aero LLC

- 6.4.18 Kratos Defense & Security Solutions Inc.

- 6.4.19 Kaman Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment