|

시장보고서

상품코드

1687899

북미의 리튬이온 배터리 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Lithium-ion Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

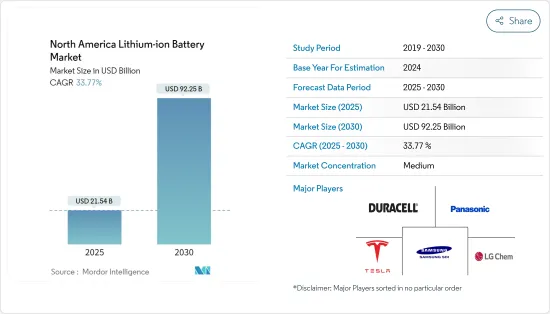

북미의 리튬이온 배터리 시장 규모는 2025년에 215억 4,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 33.77%로 성장할 전망이며, 2030년에는 922억 5,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전기자동차나 하이브리드차의 보급이 진행되어 에너지 저장 시스템 수요가 증가하는 것이 시장을 견인할 것으로 예상됩니다.

- 한편, 원료의 수급 미스매치가 조사 기간 중 시장 성장을 저해할 것으로 예상됩니다.

- 효율과 유지 보수 요구 사항의 개선은 예측 기간 동안 리튬이온 배터리에 큰 비즈니스 기회를 가져올 것으로 예상됩니다.

- 미국은 정부가 예측기간 동안 전기자동차 부문에 대한 투자를 늘리기 때문에 시장을 독점할 것으로 예상됩니다. 그 결과 주로 리튬이온 배터리가 주도하는 배터리 기반 에너지 저장 시스템의 수요가 증가합니다.

북미의 리튬이온 배터리 시장 동향

자동차 배터리가 급성장할 전망

- 리튬이온 배터리 시스템은 주행 거리와 충전 시간에 대한 OEM 요구 사항을 충족하여 플러그인 하이브리드 자동차 및 전기자동차의 성능을 향상시킵니다. 고에너지 밀도, 고속 충전 능력, 고방전 전력으로 리튬이온 배터리는 선호되는 기술이 되고 있습니다. 리튬이온 배터리는 비 에너지와 무게 측면에서 납 기반 트랙션 배터리보다 우수합니다. 그 결과, 리튬이온 배터리는 총 하이브리드 전기자동차 및 전기자동차에 가장 경쟁 옵션입니다.

- 리튬이온 배터리는 전원 공급을 이 배터리에 의존하는 전기자동차의 수명을 연장하고 배터리 교체의 빈도를 줄입니다. 리튬이온 배터리는 납이나 카드뮴과 같은 유해 물질을 포함하지 않기 때문에 다른 배터리에 비해 친환경적이라고 생각됩니다. 따라서 더 깨끗하고 안전한 선택이되었습니다. 게다가 리튬이온 배터리는 고출력을 제공하기 때문에 급 가속과 고속 주행이 필요한 전기자동차에 필수적입니다.

- 또한 전기자동차 배터리 제조 산업에서는 리튬이온 배터리의 각형 셀의 인기가 높아지고 있습니다. 이 셀은 상당히 크고 원통형 셀의 20배에서 100배까지 크기가 있습니다. 이 큰 크기는 각형 셀이 동일한 부피 내에서 더 큰 전력을 공급하고 더 큰 에너지를 저장할 수 있습니다. 한편, 원통형 셀은 케이스에 사용하는 재료가 적기 때문에 출력과 에너지 저장 능력에 한계가 있습니다.

- 또한 전기차 판매량이 증가함에 따라 자동차 부문용 리튬이온 배터리 수요는 예측 기간 동안 크게 증가할 것으로 예상됩니다. 예를 들어 국제 에너지 기관에 따르면 미국과 캐나다에서 전기자동차 판매량은 2021-2022년 54% 이상 증가했습니다.

- 게다가 2022년에는 General Motors와 Ford와 미국 기업이 EV 제조 및 판매의 목표 전략을 발표했습니다. General Motors는 2025년까지 북미에서 30차종의 EV를 제조하고, 100만 대의 배터리 전기자동차(BEV) 생산 능력을 확립하는 것, 게다가 2040년에는 탄소 중립을 실현하는 것을 목표로 내걸고 있습니다. 이에 대해 포드는 2026년까지 판매량의 3분의 1을 완전 전기자동차로, 2030년까지 50%를 완전 전기자동차로 하고, 2030년까지 유럽에서의 판매를 모두 전기자동차로 한다는 목표를 선언했습니다. 북미에서는 리튬이온 배터리의 필요성이 높아질 것으로 예상됩니다.

- 2023년 2월, NanoGraf는 실리콘 음극 개발에서 최신 발전을 이루고 있으며, 다가올 리튬이온 배터리의 에너지 밀도와 출력 밀도를 향상시켰습니다. 이 획기적인 기술은 실리콘 음극과 관련된 문제를 효과적으로 해결합니다.

- 이러한 이유로 전기차로의 이동이 증가함에 따라 예측 기간 동안 북미의 리튬이온 배터리 시장을 견인할 것으로 예상됩니다.

미국이 시장을 독점할 전망

- 미국은 세계 배터리 시장에서 연구 및 혁신의 선구자 중 하나입니다. 또, 1차 배터리, 2차 배터리에 관계없이, 배터리의 최대 소비국의 하나이기도 합니다. 이는 전기자동차의 보급, 소비자용 전자기기 제품에 대한 지출, 소비활동과 제조활동 증가로 인한 것입니다.

- 미국에는 리튬이온 배터리의 제조 인프라가 확립되어 있어 다수의 배터리 제조업체, 배터리 기술에 특화된 연구개발 시설이 있습니다. 이러한 인프라로 인해 미국은 생산 능력과 기술 발전에 대해 경쟁 우위를 가지고 있습니다.

- 예를 들어, 2022년 10월, Honda는 미국에서 리튬이온 배터리를 생산할 계획을 발표하고 이를 수행하는 최신 자동차 회사가 되었습니다. LG Energy Solutions와의 합작 사업으로, Honda는 Honda와 Acura의 브랜드로 전기 자동차용으로 설계된 '파우치형' 배터리를 북미 시장에 공급하는 것을 목표로 하고 있습니다. 44억 달러를 투입하는 공장의 정확한 위치는 밝혀지지 않았지만 합작사업은 규제당국의 승인을 거쳐 올해 말까지 개시될 예정입니다. 건설은 2023년 초에 시작되어 2025년 말까지 선진적인 리튬 이온 배터리 셀의 대량 생산을 달성할 예정입니다.

- 게다가 미국은 정부의 인센티브, 환경 규제, 보다 깨끗한 수송 수단을 요구하는 소비자 수요에 밀려, 전기자동차의 큰 시장을 잡고 있습니다. 전기자동차의 보급이 리튬이온 배터리 수요를 높여, 미국은 이 시장에서 우위에 서 있습니다.

- 새로운 시책에서는 배터리 기술 지원을 위한 2022년도 예산 2억 달러를 포함하여 연방 정부의 지원을 받는 프로젝트는 미국 내에서 제품을 제조해야 한다고 의무화되고 있습니다. 또 DOE의 선진 기술 자동차 제조 대출 프로그램 하에 대출 당국이 발행하는 170억 달러에도 적용됩니다.

- 국제에너지기구(IEA)에 의하면, 이 나라의 전기자동차 판매 대수는 6만 3,000대에 대해 9만 9,000대로, 2022-2021년 57% 이상의 성장률을 기록했습니다.

- 또한 미국 에너지 정보국에 따르면 2022년 시점의 대규모 축배터리의 누적 용량은 약 2만 2,385.1메가와트시(MWh)로 2021년에 비해 약 80% 증가하고 있습니다. 미국에서는 캘리포니아주 독립계통운용기관(CAISO)과 텍사스주전력 신뢰성평의회(ERCOT)가 대규모 축배터리 용량 증설의 대부분을 차지했습니다. 2022년에 CAISO는 7,561.3MWh, 34%의 점유율, ERCOT는 1,684.4MWh, 7.5%의 점유율을 보유하고 있습니다.

- 게다가 국내 EV 제조업체는 수요 증가에 대응하기 위해 추가적인 노력을 하고 있습니다. 미국에서는 2025년까지 13개의 새로운 배터리 셀 기가 공장이 가동될 예정입니다. 이 기가 공장은 Ford Motor Company 및 General Motors와 같은 자동차 제조업체가 전기자동차 제조 및 판매를 지원하기 위해 개발하고 있습니다.

- 그러므로 북미의 리튬이온 배터리 시장에서는 도시화와 개인 소비 증가에 힘입어 이 나라가 지배적인 지위를 차지할 가능성이 높습니다. 리튬이온 배터리로 인한 혜택은 기술적으로 첨단 장비와 자동차에 대한 수요를 높일 것으로 예상됩니다. 이에 따라 배터리 사용량도 증가할 것으로 예상됩니다.

북미의 리튬이온 배터리 산업 개요

북미의 리튬이온 배터리 시장은 세분화되어 있습니다. 이 시장의 주요 기업으로는 Tesla Inc., LG Chem Ltd., Panasonic Corporation, Duracell Inc., Samsung SDI 등이 있습니다.(순부동)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 시장 규모 및 수요 예측(단위 : 달러)(-2029년)

- 세계의 리튬이온 배터리 가격 동향 분석(-2029년)

- 최근 동향 및 개발

- 정부 규제 및 시책

- 시장 역학

- 성장 촉진요인

- 리튬이온 배터리 가격 하락

- 전기자동차 보급 확대

- 성장 억제요인

- 리튬이온 배터리에 관한 안전성에 대한 우려

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 용도별

- 소비자 일렉트로닉스

- 자동차

- 산업용 배터리(동력용, 거치형(텔레콤, UPS, 에너지 저장 시스템(ESS) 등))

- 기타 용도(전동 공구, 방위, 의료기기 등)

- 시장 분석 : 지역별 시장 규모 별 수요 예측(-2028년)

- 미국

- 캐나다

- 기타 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 주요 기업의 전략

- 기업 프로파일

- BYD Company Ltd

- Contemporary Amperex Technology Co. Limited

- EnerSys

- Duracell Inc.

- Clarios(구 Johnson Controls International PLC)

- LG Chem Ltd.

- Panasonic Corporation

- VARTA AG

- Samsung SDI Co. Ltd.

- Sony Corporation

- Tesla Inc.

제7장 시장 기회 및 향후 동향

- 효율 향상 및 유지보수 필요성

The North America Lithium-ion Battery Market size is estimated at USD 21.54 billion in 2025, and is expected to reach USD 92.25 billion by 2030, at a CAGR of 33.77% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the market is expected to be driven by the increasing adoption of electric and hybrid vehicles and the increasing demand for energy storage systems.

- On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market growth during the study period.

- Nevertheless, the improvements in efficiency and maintenance requirements are expected to provide significant opportunities for lithium-ion batteries during the forecast period.

- The United States is expected to dominate the market due to the government's increasing investments in electric vehicle segments in the forecast period. It will result in increased demand for battery-based energy storage systems, primarily led by lithium-ion batteries.

North America Lithium-ion Battery Market Trends

Automotive Batteries Expected to be the Fastest-growing Segment

- Lithium-ion battery systems drive the performance of plug-in hybrid and electric vehicles by meeting OEM requirements for driving range and charging time. Their high energy density, fast recharge capability, and high discharge power make lithium-ion batteries the preferred technology. They outperform lead-based traction batteries in terms of specific energy and weight. As a result, lithium-ion batteries are the most competitive option for total hybrid electric vehicles and electric vehicles.

- Lithium-ion batteries offer a longer lifespan for electric vehicles, which rely on these batteries for power, reducing the frequency of battery replacements. Lithium-ion batteries are considered environmentally friendly compared to other batteries as they do not contain toxic materials like lead or cadmium. It makes them a cleaner and safer choice. Additionally, lithium-ion batteries provide a high power output, which is crucial for electric vehicles that require rapid acceleration and high speeds.

- Moreover, within the electric vehicle battery manufacturing industry, there is a growing popularity of lithium-ion battery prismatic cells. These cells are significantly larger, ranging from 20 to 100 times the size of cylindrical cells. This larger size allows prismatic cells to deliver more power and store greater energy within the same volume. Cylindrical cells, on the other hand, use less material for their casing, which can limit their power and energy storage capabilities.

- Additionally, with the growing sales of electric vehicles, the demand for lithium-ion batteries for the automotive segment is expected to increase significantly during the forecasted period. For instance, according to the International Energy Agency, the sales of electric vehicles in the United States and Canada grew by more than 54% between 2021 and 2022.

- Moreover, in 2022, General Motors & Ford, and American companies announced their targeted strategy to manufacture and sell EVs. General Motors declared its target to manufacture 30 EV models and set up a Battery Electric Vehicle (BEV) production capacity of 1 million units in North America by 2025, plus carbon neutrality in 2040. In comparison, Ford declared its target of One-third of sales to be fully electric by 2026 and 50% by 2030, with all-electric sales in Europe by 2030. It will drive the need for lithium-ion batteries in North America.

- In February 2023, NanoGraf's latest advancement in deploying silicon anodes is positioned to enhance the energy and power densities of forthcoming lithium-ion batteries. This breakthrough technology effectively addresses the challenges associated with silicon anodes.

- Therefore, the increasing shift towards electric vehicles is expected to drive the North America Lithium-ion Battery Market during the forecast period.

The United States Expected to Dominate the Market

- The United States is one of the pioneers in research and innovation in the global battery market. The region also remains one of the largest consumers of batteries, i.e., both primary and secondary battery types. It is owing to increased electric vehicle deployment, spending on consumer electronics, and consumer and manufacturing activities.

- The United States includes a well-established manufacturing infrastructure for lithium-ion batteries, a significant number of battery manufacturers, and research and development facilities focused on battery technologies. This infrastructure gives the United States a competitive edge regarding production capacity and technological advancements.

- For instance, in October 2022, Honda announced its plans to manufacture lithium-ion batteries in the United States, making it the latest car company to do so. In a joint venture with LG Energy Solutions, Honda aims to supply the North American market with "pouch type" batteries designed to power electric vehicles under its Honda and Acura brands. While the exact location of the USD 4.4 billion factory is not disclosed, the joint venture is expected to commence by the end of this year, pending regulatory approval. Construction is planned to begin in early 2023 to achieve mass production of advanced lithium-ion battery cells by the end of 2025.

- Moreover, the United States holds a large market for electric vehicles driven by government incentives, environmental regulations, and consumer demand for cleaner transportation options. The increasing adoption of EVs fuels the demand for lithium-ion batteries, giving the United States an advantage in the market.

- The new policies mandate that projects receiving federal support, including the USD 200 million in the agency's 2022 budget to support battery technology, must manufacture their products within the United States. It also applies to the USD 17 billion issued by the lending authority under DOE's Advanced Technology Vehicles Manufacturing Loan Program.

- According to the International Energy Agency, the country's electric vehicle sales were around 990000 compared to 630000, registering a growth rate of more than 57% between 2022 and 2021.

- Moreover, as of 2022, the cumulative large-scale battery storage capacity was around 22,385.1 megawatt-hours (MWh), which was approximately 80% more than in 2021, as per the United States Energy Information Administration. In the United States, the California Independent System Operator (CAISO) and Electric Reliability Council of Texas (ERCOT) include most of the large-scale battery storage capacity additions. In 2022, CAISO had 7561.3 MWh or 34 % share, and ERCOT had 1684.4 MWh capacity or 7.5% share in the country's overall installed capacity.

- Further, the country's EV manufacturers are undertaking further initiatives to cater to the rising demand. Thirteen new battery cell giga-factories are expected to come online in the United States by 2025. These giga-factories are being developed by various automobile manufacturers, like Ford Motor Company and General Motors Company, to support their electric vehicle manufacturing and sales.

- Therefore, the country is likely the dominant player in the North American lithium-ion battery market, supported by increasing urbanization and consumer spending. These are expected to ramp up the demand for technically advanced devices and vehicles due to the benefits provided by the same. Consecutively, this is expected to boost the usage of batteries.

North America Lithium-ion Battery Industry Overview

The North American lithium-ion battery market is semi-fragmented. Some of the key players in the market (in no particular order) include Tesla Inc., LG Chem Ltd, Panasonic Corporation, Duracell Inc., and Samsung SDI Co. Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Global Lithium-ion Battery Price Trend Analysis, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Declining Lithium-Ion Battery Prices

- 4.6.1.2 Increasing Adoption Of Electric Vehicles

- 4.6.2 Restraints

- 4.6.2.1 Safety Concerns Related To Lithium-Ion Battery

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Consumer Electronics

- 5.1.2 Automotive

- 5.1.3 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.))

- 5.1.4 Other Applications (Power Tools, Defense, Medical Devices, etc.)

- 5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 EnerSys

- 6.3.4 Duracell Inc.

- 6.3.5 Clarios (Formerly Johnson Controls International PLC)

- 6.3.6 LG Chem Ltd.

- 6.3.7 Panasonic Corporation

- 6.3.8 VARTA AG

- 6.3.9 Samsung SDI Co. Ltd.

- 6.3.10 Sony Corporation

- 6.3.11 Tesla Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Improvement In Efficiency And Maintenance Requirements