|

시장보고서

상품코드

1797830

산업용 트랙션 배터리 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Industrial Traction Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

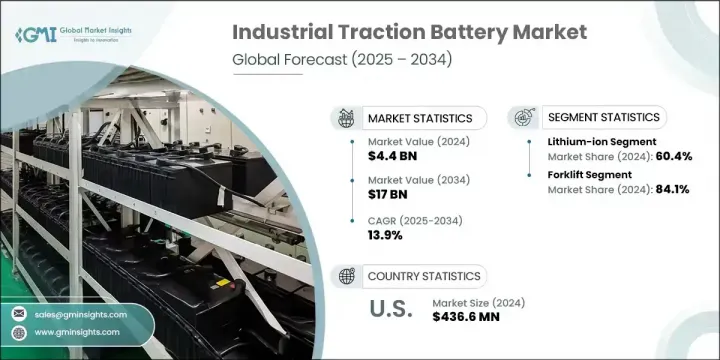

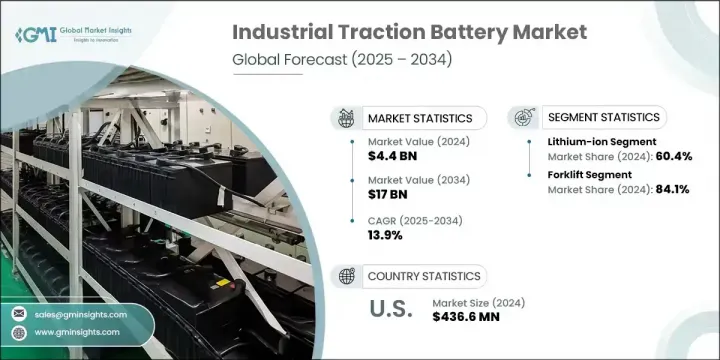

세계의 산업용 트랙션 배터리 시장은 2024년 44억 달러로 평가되었으며 CAGR 13.9%로 성장해 2034년까지 170억 달러에 이를 것으로 추정됩니다.

이 급성장의 주요 요인은 현대 산업 시설 내에서 전동 자재관리 장비, 유틸리티 카트 및 자동화 시스템에 대한 수요가 증가하고 있습니다. 배터리 구동 시스템은 운영 비용이 낮고 배출량을 줄이고 유지 보수 필요성을 최소화함으로써 연료 구동 기계를 빠르게 대체합니다. 창고 관리, 물류 및 제조 업무가 더 높은 효율성과 지속가능성을 추구하는 동안 트랙션 배터리는 이러한 이동을 가능하게 하는 중요한 역할을 수행하고 있습니다. 자동화 및 로봇 공학에 대한 투자 확대는 워크플로우와 안전성을 향상시키는 배터리 구동 산업 자산의 광범위한 사용을 지원합니다.

동시에, 배터리 화학, 특히 리튬 이온 및 커패시터 기술의 급속한 발전은 더 높은 에너지 효율과 더 빠른 충전 사이클을 실현합니다. 이러한 이점을 통해 제조업체는 환경 지침을 준수하면서 가동 중지 시간을 줄이고 처리 능력을 향상시킬 수 있습니다. 전기자동차로의 전환에 재정적 인센티브와 보조금을 제공하는 정부 이니셔티브는 업계 전반에 걸쳐 청정 에너지 기술의 채택을 강화하고 있습니다. 트랙션 배터리 시스템은 현재 가동 시간과 운전 회복력을 극대화하면서 이산화탄소 배출량의 삭감을 목표로 하는 차세대 산업 에코시스템에 필수적입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 44억 달러 |

| 예측 금액 | 170억 달러 |

| CAGR | 13.9% |

리튬 이온 부문은 60.4%의 점유율을 차지하며, 2034년까지 CAGR 15%로 예측됩니다. 이 성장을 뒷받침하고 있는 것은 창고업, 건설업, 생산업에 있어서, 장기적인 효율 향상과 배출 가스 규제에의 준거를 요구하는 만큼, 배터리 구동 기기에의 기호가 높아지고 있는 것입니다. 리튬이온 유닛은 다른 배터리 유형에 비해 에너지 밀도가 뛰어나 수명이 길고 유지보수가 최소한이기 때문에 지지되고 있습니다. 급속 충전 기술과의 호환성과 고부하 용도에의 대응 능력에 의해 연속 운전에 최적인 선택이 되고 있습니다.

철도 분야의 2024년 시장 규모는 5억 8,640만 달러였습니다. 국가 및 지역 당국은 탈탄소화 전략의 일환으로 하이브리드 철도 및 전기 철도 인프라에 대한 투자를 늘리고 있습니다. 도시 지역이 더 깨끗하고 효율적인 대중 교통망을 선호하기 때문에 배터리 구동 지하철과 경편 철도 차량이 눈에 띄게되었습니다. 철도 트랙션 배터리는 추진력을 지원할 뿐만 아니라 보조 시스템에도 전력을 공급하므로 도시 회랑에서 보다 조용하고 배출가스가 없는 수송 수단을 가능하게 합니다.

북미의 산업용 트랙션 배터리는 2034년까지 연평균 복합 성장률(CAGR)이 10%로 예상됩니다. 스마트 제조, 전자상거래, 산업 자동화의 등장이 전동 산업 차량과 이를 지원하는 인프라 수요를 밀어 올리고 있습니다. 배터리 기술의 발전, 특히 충전 시간 단축과 서비스 간격 연장이 이러한 기세를 뒷받침하고 있습니다. 미국과 캐나다 기업들은 규제 요건과 사내 지속가능성 목표를 모두 충족하기 때문에 저 배출 가스 장비로의 전환을 가속화하고 있습니다. 산업 허브는 친환경 의무에 따라 에너지 관련 비용을 장기적으로 최소화하기 위해 배터리 구동 차량을 통합합니다.

이 산업용 트랙션 배터리 시장에서 혁신을 추진하고 있는 주요 기업으로는 ENERSYS, BYD, Flux Power, Sunlight Group, EXIDE INDUSTRIES 등이 있어, 모두 세계경쟁 구도를 적극적으로 형성하고 있습니다. 산업용 트랙션 배터리 시장의 주요 기업은 첨단 배터리 기술, 특히 리튬 이온 및 고체 화학에 대한 장기 전략 투자를 선호합니다. 이러한 기업들은 지역 수요에 대응하고 공급망의 제약을 완화하기 위해 세계 제조 기지를 확대하고 있습니다. 제품의 다양화는 그들의 접근 방식의 중심이며 광범위한 전기 산업 차량에 맞는 모듈식 배터리 시스템에 강력하게 초점을 맞추었습니다. 각 회사는 또한 OEM 및 물류 운영자와 협력하여 성능과 신뢰성을 향상시키는 통합 배터리 솔루션을 공동 개발하고 있습니다. 시장의 리더 기업 여러 회사는 실시간 모니터링, 예측 분석 및 성능 최적화를 위해 텔레매틱스 및 배터리 관리 시스템을 통합하여 디지털 서비스를 강화하고 있습니다. 또한 순환형 경제 모델과 2차 라이프 배터리 프로그램을 추진함으로써 지속가능성 목표와의 무결성을 도모하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인 매핑

- 이해관계자 분석

- 산업 구조의 진화

- 규제 상황

- 세계 안전 기준

- 환경규제와 지속가능성 요건

- 지역에 의한 규제의 차이

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTLE 분석

- 기술의 진화와 혁신의 동향

- 배터리의 화학과 진보의 타임라인

- 에너지 밀도 향상의 궤적

- 배터리 관리 시스템의 진화

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 대시보드

- 전략적 노력

- 주요 파트너십 및 협업

- 주요 M&A 활동

- 제품의 혁신과 발매

- 시장 확대 전략

- 경쟁 벤치마킹

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 화학별, 2021-2034년

- 주요 동향

- 납축전지

- 리튬 이온

- 니켈 베이스

- 기타

제6장 시장 규모와 예측 : 용도별, 2021-2034년

- 주요 동향

- 지게차

- 철도

- 기타

제7장 시장 규모와 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 한국

- 호주

- 인도

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

제8장 기업 프로파일

- Amara Raja Batteries

- Aliant Battery

- BYD

- Camel Group

- East Penn

- EXIDE INDUSTRIES

- ecovolta

- ENERSYS

- Farasis Energy

- Flux Power

- Guoxuan High-tech Power Energy

- HOPPECKE Batteries

- Hitachi Energy

- Mutlu Corporation

- MIDAC

- Sunlight Group

- Sunwoda Electronic

- Toshiba Corporation

The Global Industrial Traction Battery Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 13.9% to reach USD 17 billion by 2034. This surge is largely fueled by the rising demand for electric material handling equipment, utility carts, and automation systems within modern industrial facilities. Battery-powered systems are rapidly replacing fuel-driven machinery due to their lower operational costs, reduced emissions, and minimal maintenance needs. As warehousing, logistics, and manufacturing operations push for greater efficiency and sustainability, traction batteries are playing a crucial role in enabling the shift. Growing investment in automation and robotics is supporting widespread use of battery-powered industrial assets that improve workflow and safety.

At the same time, rapid progress in battery chemistry, particularly in lithium-ion and ultracapacitor technologies, is delivering greater energy efficiency and faster charge cycles. These benefits are allowing manufacturers to cut downtime and increase throughput, while still adhering to environmental guidelines. Government initiatives offering financial incentives and subsidies for electric fleet conversions are reinforcing the adoption of clean-energy technologies across industries. Traction battery systems are now integral to next-gen industrial ecosystems aiming to reduce carbon output while maximizing uptime and operational resilience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $17 Billion |

| CAGR | 13.9% |

The lithium-ion segment held a 60.4% share and is projected to grow at a CAGR of 15% through 2034. This growth is being propelled by a growing preference for battery-powered equipment in warehousing, construction, and production, as organizations seek long-term efficiency gains and compliance with emissions regulations. Lithium-ion units are favored for their superior energy density, longer life span, and minimal maintenance compared to other battery types. Their compatibility with fast-charging technologies and ability to support high-duty applications make them a prime choice for continuous operation.

The rail segment was valued at USD 586.4 million in 2024. National and regional authorities are increasing investments in hybrid and electric rail infrastructure as part of decarbonization strategies. Battery-powered metro and light rail vehicles are becoming more prominent as urban areas prioritize cleaner, more efficient public transport networks. Traction batteries in rail not only support propulsion but also power auxiliary systems, enabling quieter, emission-free transit options in urban corridors.

North America Industrial Traction Battery Market is expected to register a CAGR of 10% through 2034. The rise of smart manufacturing, e-commerce, and industrial automation is pushing demand for electric industrial vehicles and supporting infrastructure. Advancements in battery technologies, particularly those that reduce charging time and extend service intervals, are supporting this momentum. Businesses across the U.S. and Canada are increasingly switching to low-emission equipment to meet both regulatory requirements and internal sustainability goals. Industrial hubs are integrating battery-powered fleets to align with green mandates and minimize energy-related costs over time.

Top players driving innovation in this Industrial Traction Battery Market include ENERSYS, BYD, Flux Power, Sunlight Group, and EXIDE INDUSTRIES, all of which are actively shaping the global competitive landscape. Leading companies in the industrial traction battery market are prioritizing long-term strategic investments in advanced battery technologies, particularly lithium-ion and solid-state chemistries. These players are expanding their global manufacturing footprints to address regional demand and reduce supply chain constraints. Product diversification is central to their approach, with a strong focus on modular battery systems compatible with a wide range of electric industrial vehicles. Companies are also collaborating with OEMs and logistics operators to co-develop integrated battery solutions that enhance performance and reliability. Several market leaders are enhancing their digital offerings by embedding telematics and battery management systems for real-time monitoring, predictive analytics, and performance optimization. Additionally, they are aligning with sustainability targets by promoting circular economy models and second-life battery programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1.1 Value chain mapping

- 3.1.1.2 Stakeholder analysis

- 3.1.1.3 Industry structure evolution

- 3.2 Regulatory landscape

- 3.2.1.1 Global safety standards

- 3.2.1.2 Environmental regulations and sustainability requirements

- 3.2.1.3 Regional regulatory variations

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Technology evolution and innovation trends

- 3.7.1 Battery chemistry and advancement timeline

- 3.7.2 Energy density improvement trajectory

- 3.7.3 Battery management system evolution

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Chemistry, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Lead acid

- 5.3 Lithium-ion

- 5.4 Nickel-based

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Forklift

- 6.3 Railroads

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 Australia

- 7.4.5 India

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Amara Raja Batteries

- 8.2 Aliant Battery

- 8.3 BYD

- 8.4 Camel Group

- 8.5 East Penn

- 8.6 EXIDE INDUSTRIES

- 8.7 ecovolta

- 8.8 ENERSYS

- 8.9 Farasis Energy

- 8.10 Flux Power

- 8.11 Guoxuan High-tech Power Energy

- 8.12 HOPPECKE Batteries

- 8.13 Hitachi Energy

- 8.14 Mutlu Corporation

- 8.15 MIDAC

- 8.16 Sunlight Group

- 8.17 Sunwoda Electronic

- 8.18 Toshiba Corporation