|

시장보고서

상품코드

1687937

프로덕션 프린터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Production Printer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

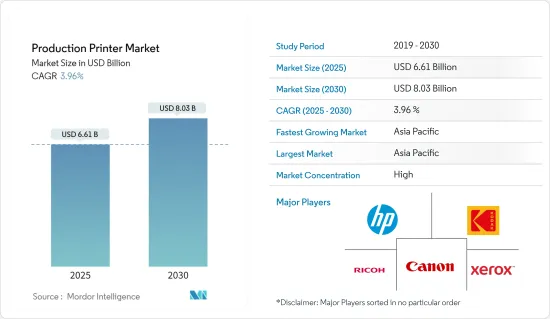

프로덕션 프린터 시장 규모는 2025년에 66억 1,000만 달러에 이르고 예측 기간(2025-2030년)의 CAGR은 3.96%를 나타내 2030년에는 80억 3,000만 달러에 달할 것으로 전망됩니다.

주요 하이라이트

- 포장 용도의 성장이 시장 확대를 견인 : 프로덕션 프린터 시장은 포장 부문을 주요 촉진요인으로 큰 성장을 이루고 있습니다. 2022년 프로덕션 프린터 시장에서 포장 용도 시장 규모는 25억 3,060만 달러를 기록했고, 2023-2028년에 걸쳐 CAGR 4.35%를 나타내 2028년에는 32억 9,720만 달러에 달할 것으로 예측되고 있습니다.

- 전자상거래 붐 : 전자상거래의 상승은 혁신적인 포장 솔루션 수요에 박차를 가하고 있으며, 제품 제조업체는 디지털 인쇄를 이용하여 대상으로 하는 소비자 그룹을 위한 포장을 맞춤화하고 있습니다.

- 종이기 : 디자인, 지속가능성, 디지털 인쇄에 대한 투자로 특히 식품 산업에서는 종이기가 보급되고 있습니다.

- 담배, 의약품, 알코올 포장: 다이나믹한 규제와 위조 방지 대책에 의해 이들 제품에의 고품질 인쇄 수요가 높아지고 있다

- 고성능 잉크젯 프린터가 시장 성장을 가속 : 고성능 잉크젯 프린터는 시장 확대에 매우 중요한 역할을 했으며, 2022년 잉크젯 생산 부문 시장 규모는 50억 8,130만 달러였습니다.

- 지배적인 진출 기업 : Xerox, Canon, Ricoh, HP, Lexmark는 품질과 신뢰성을 높이는 지속적인 기술 혁신으로 잉크젯 프린터 시장을 선도하고 있습니다.

- 최근의 신제품 : 캐논의 ProStream 3,000 시리즈(2023년 2월 발매)는 오프셋 품질의 고속 산업 인쇄를 기재하고 있습니다.

- 시장 세분화와 지역 역학 : 프로덕션 프린터 시장은 유형, 생산 방식, 기술, 지역에 따라 구분됩니다.

- 아시아태평양의 우위성 : 인도, 인도네시아, 베트남의 신흥 시장이 강력한 성장을 보이고 있으며, 이 지역의 전체적인 시장 리더십에 공헌하고 있습니다.

- 미국 시장 동향 : 미국 시장의 2022년 시장 규모는 13억 7,620만 달러로, 상업 인쇄를 지원하는 유리한 시책에 의해 CAGR 3.57%를 나타내 2028년에는 17억 1,390만 달러에 달할 것으로 전망됩니다.

- 경쟁 구도와 기술의 진보 : 프로덕션 프린터 시장은 고도로 통합되어 있으며, Xerox, HP, Ricoh, Canon 등의 대기업이 시장에서 강한 존재감을 보여줍니다.

- Xerox와 HP의 혁신 : Xerox의 포트폴리오에는 IRIDESSE PRODUCTION PRESS와 같은 디지털 인쇄기가 있으며 HP의 Designjet Z6800은 포토 프로덕션에서 선도하고 있습니다.

프로덕션 프린터 시장 동향

흑백 부문이 프로덕션 프린터 시장을 독점

흑백 부문은 2022년에 36억 3,780만 달러로 평가되었으며, 2028년에는 45억 5,910만 달러로 성장할 것으로 예상되며, CAGR은 3.68%를 나타낼 것으로 전망됩니다.

- 비용 효율 : 단색 프린터는 인쇄 속도가 빠르고 운영 비용이 낮기 때문에 대량 출력에 중점을 둔 사무실과 산업에 적합합니다.

- 기술 진보: Canon의 varioPRINT 140 QUARTZ(2024년)와 코니카 미놀타의 bizhub 950i 및 850i(2024년)는 소규모 인쇄 공장에 생산 피크를 수용하고 운영 유연성을 유지하기 위한 도구를 제공합니다.

- 중요한 용도 : 단색 인쇄는 최소한의 비용으로 안정적인 대량 출력을 필요로하는 도서 출판, 사용자 수동, 트랜잭션 양식 등의 부문에 필수적입니다.

아시아태평양 : 프로덕션 프린터 시장 성장 엔진

아시아태평양은 프로덕션 프린터의 최대 시장으로 떠오르고 있으며, 2022년 시장 점유율은 44.9%를 나타냈습니다.

- 중국이 리드 : 중국은 2022년에 53.39%의 점유율을 획득해 이 지역 시장을 독점하는 한편, 인도는 CAGR 4.38%의 예측으로 급성장을 보이고 있습니다.

- 산업의 다양성 : 식품에서 소비자용 전자기기까지 폭넓은 산업이 이 지역의 인쇄 솔루션 수요 증가에 공헌하고 있습니다.

- 혁신 : FUJIFILM Business Innovation Corp.와 같은 기업은 Revoria Press EC1100 및 Revoria Press SC180/SC170과 같은 모델로 기술의 한계를 넓혀 고품질의 생산성 솔루션을 계속 제공합니다.

프로덕션 프린터 시장 개요

세계 진출 기업이 통합 시장을 독점 : 프로덕션 프린터 시장은 제록스, HP, 캐논, 리코 등 선도적인 세계 기업이 시장을 선도하고 있으며, 여전히 통합이 계속되고 있습니다.

높은 진입 장벽 : 신규 진출기업은 프로덕션 프린터 산업에서 선도 기업의 이점과 높은 개발 비용으로 인해 큰 문제에 직면합니다.

엔드 투 엔드 솔루션 : 시장 리더는 하드웨어, 소프트웨어 및 서비스를 통합 한 종합적인 제품을 제공하며 다양한 부문의 광범위한 고객 요구를 충족시킵니다.

혁신과 종합적 솔루션이 리더십을 견인 : 각 회사는 경쟁을 유지하기 위해 특히 고속 잉크젯 기술, 디지털 인쇄, 자동화 등의 기술 혁신에 주력하고 있습니다.

향후 전략 : 주요 기업은 3D 프린팅, AI를 활용한 솔루션, 친환경 기술 등 지속가능성에 대한 시장의 요구에 따라 성장 기회를 모색하고 있습니다.

시장의 미래 성공을 위한 전략 : 기술 혁신 외에도 클라우드 인쇄 및 디지털 서비스 등 새로운 시장 동향을 성공적으로 캡처할 수 있는 기업이 성공을 거둘 것으로 예상됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 이해관계자 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 포장에 있어서 인쇄 용도의 확대가 성장을 견인할 전망

- 고성능 잉크젯 프린터 도입으로 잉크젯 판매 증가

- 시장 성장 억제요인

- 디지털 마케팅과 온라인 독서의 성장

- 프로덕션 프린터 공급망 유통에 있어서 COVID-19의 세계적 영향

제6장 주요 기술 투자

- 클라우드 기술

- 인공지능(AI)

- 사이버 보안

- 디지털 서비스

제7장 시장 세분화

- 유형별

- 흑백

- 컬러

- 생산 방법별

- 컷 피드

- 연속 피드

- 기술별

- 잉크젯

- 토너

- 용도별

- 상업

- 출판

- 포장

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 기타 아시아태평양

- 기타

- 북미

제8장 경쟁 구도

- 기업 프로파일

- Xerox Corporation

- Hewlett-Packard Development Company LP

- Ricoh Company Ltd

- Canon Inc.

- Eastman Kodak Company

- Konica Minolta Inc.

- Miyakoshi Printing Machinery Co. Ltd

- Inca Digital Printers Ltd(Dainippon Screen Mfg. Co. Ltd)

제9장 투자 분석

제10장 시장 기회와 앞으로의 동향

KTH 25.05.12The Production Printer Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 8.03 billion by 2030, at a CAGR of 3.96% during the forecast period (2025-2030).

Key Highlights

- Growth in Packaging Applications Drives Market Expansion: The Production Printer Market is undergoing significant growth, with the packaging sector being a primary driver. In 2022, packaging applications accounted for 43.7% of the market share. The rising demand for customization in product packaging is pushing this growth, as brand owners increasingly focus on using creative packaging to capture consumer attention. In 2022, the market size for packaging applications in the production printer market was valued at USD 2,530.6 million, and it is projected to reach USD 3,297.2 million by 2028, growing at a CAGR of 4.35% from 2023 to 2028.

- E-commerce boom: The rise in e-commerce is fueling demand for innovative packaging solutions, with product manufacturers using digital printing to customize packaging for targeted consumer groups.

- Folding cartons: Investments in design, sustainability, and digital printing have popularized folding cartons, especially within the food industry.

- Tobacco, pharmaceutical, and alcohol packaging: Dynamic regulations and anti-counterfeiting measures are boosting the demand for high-quality printing on these products.

- High-Performance Inkjet Printers Fuel Market Growth: High-performance inkjet printers play a pivotal role in market expansion, with the inkjet production segment valued at USD 5,081.3 million in 2022. By 2028, this segment is expected to grow to USD 6,456.7 million, achieving a CAGR of 3.92%. Inkjet technology is favored due to its speed, customization options, and efficiency in handling modern print production demands.

- Dominant players: Xerox, Canon, Ricoh, HP, and Lexmark lead the inkjet printer market with continuous innovations that enhance quality and reliability.

- Recent launches: Canon's ProStream 3000 series (launched in February 2023) offers high-speed industrial printing with offset quality. Markem-Imaje's new 9750+ inkjet printer (April 2023) allows for advanced coding using both dye and pigment inks.

- Market Segmentation and Regional Dynamics: The Production Printer Market is divided by type, production method, technology, and geography. Continuous feed printers held 95.6% of the market share in 2022, proving to be a cost-effective solution for high-volume printing. Regionally, the Asia-Pacific area dominated the market with a 44.9% share.

- Asia-Pacific dominance: Emerging markets in India, Indonesia, and Vietnam are showing strong growth, contributing to the region's overall market leadership.

- U.S. market trends: The U.S. market was valued at USD 1,376.2 million in 2022, and is expected to grow at a CAGR of 3.57% to reach USD 1,713.9 million by 2028, driven by favorable policies supporting commercial printing.

- Competitive Landscape and Technological Advancements: The production printer market is highly consolidated, with major players like Xerox, HP, Ricoh, and Canon holding a strong market presence.

- Xerox and HP innovations: Xerox's portfolio includes digital presses like the IRIDESSE PRODUCTION PRESS, while HP's Designjet Z6800 leads in photo production. Companies are also investing in cloud technologies and AI-driven solutions to stay competitive.

Production Printer Market Trends

Monochrome Segment Dominates Production Printer Landscape

The monochrome segment, valued at USD 3,637.8 million in 2022, is expected to grow to USD 4,559.1 million by 2028, representing a CAGR of 3.68%. This growth is driven by the cost-efficiency and speed of monochrome printers, which are crucial for high-volume print environments that do not require color printing.

- Cost-efficiency: Monochrome printers offer faster print speeds and lower operational costs, making them the preferred choice for offices and industries focused on high-volume output.

- Technological advancements: Canon's varioPRINT 140 QUARTZ (2024) and Konica Minolta's bizhub 950i and 850i (2024) provide small-scale print shops with the tools to handle production peaks and maintain operational flexibility.

- Critical applications: Monochrome printing is essential for sectors like book publishing, user manuals, and transactional forms, which require consistent high-volume output at minimal cost.

Asia-Pacific: The Growth Engine of Production Printer Market:

The Asia-Pacific region has emerged as the largest market for production printers, with a 44.9% market share in 2022. The region is expected to grow from USD 2,601.9 million in 2022 to USD 3,379.6 million by 2028, with a CAGR of 4.30%.

- China leads the way: China dominates the regional market with a 53.39% share in 2022, while India is showing rapid growth with a projected CAGR of 4.38%.

- Industrial diversity: The wide range of industries, from food to consumer electronics, contributes to the region's growing demand for printing solutions.

- Innovation: Companies like FUJIFILM Business Innovation Corp. continue to push technological boundaries with models like the Revoria Press EC1100 and Revoria Press SC180/SC170, offering high-quality productivity solutions.

Production Printer Market Overview

Global Players Dominate Consolidated Market: The Production Printer Market remains consolidated, with major global players such as Xerox, HP, Canon, and Ricoh leading the space. These companies leverage their extensive product portfolios, innovation capabilities, and financial resources to maintain market dominance.

High entry barriers: New entrants face significant challenges due to the dominance of large players and high development costs in the production printer industry.

End-to-end solutions: Leaders in the market provide comprehensive offerings that integrate hardware, software, and services, addressing a wide range of customer needs across different sectors.

Innovation and Comprehensive Solutions Drive Leadership: Companies are focusing on innovation, particularly in high-speed inkjet technology, digital printing, and automation, to maintain their competitive edge. Canon and HP have consistently demonstrated leadership by offering differentiated products tailored to specific market segments.

Future strategies: Key players are exploring growth opportunities in 3D printing, AI-powered solutions, and eco-friendly technologies, aligning with market demands for sustainability. Expanding into high-growth areas like industrial and packaging printing also offers strategic advantages.

Strategies for Future Success in the Market: In addition to technological innovation, companies that can successfully tap into emerging market trends, such as cloud-based printing and digital services, are expected to thrive. Partnerships, acquisitions, and R&D investments will remain central to expanding market share and technological expertise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Printing Applications in Packaging is Expected to Drive Growth

- 5.1.2 Increasing Inkjet Sales Due to Introduction of High-performance Inkjet Printers

- 5.2 Market Restraints

- 5.2.1 Growth of Digital Marketing and the Practice of Online Reading

- 5.3 Impact of COVID-19 in Supply Chain Distribution of Production Printer Globally

6 KEY TECHNOLOGY INVESTMENTS

- 6.1 Cloud Technology

- 6.2 Artificial Intelligence

- 6.3 Cyber Security

- 6.4 Digital Services

7 MARKET SEGMENTATION

- 7.1 By Type

- 7.1.1 Monochrome

- 7.1.2 Color

- 7.2 By Production Method

- 7.2.1 Cut Fed

- 7.2.2 Continuous Feed

- 7.3 By Technology

- 7.3.1 Inkjet

- 7.3.2 Toner

- 7.4 By Application

- 7.4.1 Commercial

- 7.4.2 Publishing

- 7.4.3 Packaging

- 7.5 By Geography

- 7.5.1 North America

- 7.5.1.1 United States

- 7.5.1.2 Canada

- 7.5.2 Europe

- 7.5.2.1 Germany

- 7.5.2.2 United Kingdom

- 7.5.2.3 France

- 7.5.2.4 Italy

- 7.5.2.5 Rest of Europe

- 7.5.3 Asia-Pacific

- 7.5.3.1 India

- 7.5.3.2 China

- 7.5.3.3 Japan

- 7.5.3.4 Rest of Asia-Pacific

- 7.5.4 Rest of the World

- 7.5.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Xerox Corporation

- 8.1.2 Hewlett-Packard Development Company LP

- 8.1.3 Ricoh Company Ltd

- 8.1.4 Canon Inc.

- 8.1.5 Eastman Kodak Company

- 8.1.6 Konica Minolta Inc.

- 8.1.7 Miyakoshi Printing Machinery Co. Ltd

- 8.1.8 Inca Digital Printers Ltd (Dainippon Screen Mfg. Co. Ltd)