|

시장보고서

상품코드

1689777

지역 난방 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

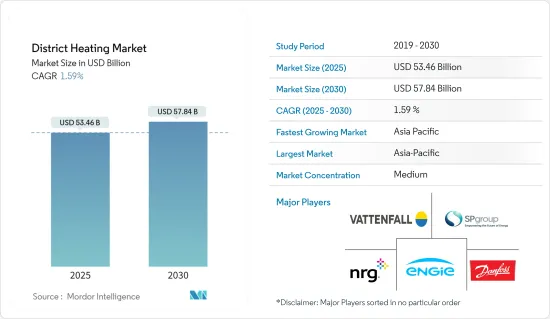

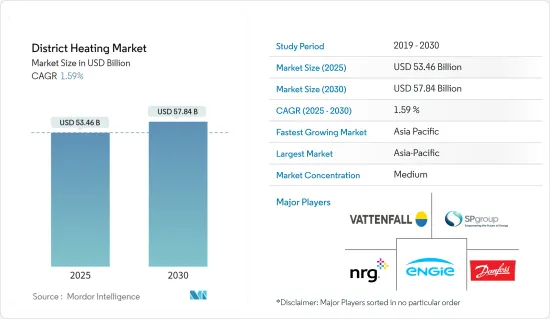

세계의 지역 난방 시장 규모는 2025년 534억 6,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 1.59%로 확대되어, 2030년에는 578억 4,000만 달러에 달할 것으로 예측됩니다.

지역 에너지는 세계 경제가 설정한 적극적인 기후 목표에 힘입어 세계적으로 급성장하는 산업입니다. 초기 평가에 따르면, 이러한 지역 냉난방 회사는 다른 보유 구조를 통해 더 놀라운 성장과 가치 잠재력을 창출하는 사업으로 인식되고 있습니다. 지역 난방 공급에 전동 히트 펌프를 포함함으로써, 더 높은 재생 가능 에너지 레벨을 열 목적으로 활용할 수 있어 에너지 시스템 간의 통합과 균형을 이룰 수 있습니다. 세계적으로 풍력 터빈의 생산 능력이 급증하고 있는 가운데 대형 히트 펌프는 지속적인 녹색 에너지 개발과 2050년까지 화석 연료 탈피에 중요한 역할을 할 것으로 보입니다.

주요 하이라이트

- 지역 난방은 고단열 파이프라인의 배전망을 통해 열에너지를 온수 형태로 건물(주택 및 상업시설)에 공급하는 방법입니다. 산업 공정의 지역 난방으로의 전환은 산업과 공정의 유형에 따라 열부하가 다르기 때문에 산업용 지역 난방의 이용 확대의 가능성은 제한되어 있습니다.

- 그러나 지역 난방으로의 전환은 전기 사용을 11%, 화석 연료 사용을 40% 삭감하고 산업계 전체의 최종 에너지 사용량을 6% 삭감했습니다.

- 산업 공정 전환으로 인해 전 세계의 이산화탄소 배출량을 연간 11만 2,000톤 줄일 수 있습니다. 그러나 주택 및 상업 시장이 큰 점유율을 차지할 것으로 예상됩니다.

- 약 6,000만 명의 EU 시민들이 지역 난방을 이용하고 있으며, 1억 4,000만 명이 적어도 하나의 지역 난방 시스템이 있는 도시에 살고 있습니다. EU와 IEA의 보고에 따르면 DH는 6,000개 지역 냉난방 네트워크를 통해 EU 열 수요의 약 11-12%를 충족합니다.

- 머신러닝을 통해 고객 데이터와 운전 데이터로부터 열 부하를 예측하고, 일기 예보, 공휴일, 평일 등의 데이터와 함께 열 생산을 최적화하고 계획함으로써 열 손실을 줄이고 피크 부하에 대응하는 것입니다. 이 가능성은 누수, 비효율적 인 난방 시스템 또는 단일 부품과 관련된 고장으로 인한 오류를 식별하는 고장 감지에서 지능형 알고리즘으로 확장됩니다.

- 2024년 6월 스웨덴의 SMR 프로젝트 개발 회사인 Karnfull Next는 스웨덴 지역 난방에 SMR을 도입하기 위해 핀란드의 Steady Energy사와 전략적으로 제휴했습니다. 이 제휴는 Karnfull의 독자적인 자금 조달 구조와 공급 모델을 활용하고 Steady Energy의 유명한 지역 난방 원자로를 스웨덴 시장에 도입하는 것을 목표로 합니다.

지역난방시장 동향

주택이 성장을 견인

- 지역 난방은 세계 선진국에서 일반적으로 사용됩니다. 지역 난방은 안전성과 신뢰성 향상, 낮은 배출 가스, 연료 유연성 향상(특히 바이오매스 및 쓰레기와 같은 대체 연료를 사용하는 경우) 등 개별 건물 설비에 비해 몇 가지 장점이 있습니다.

- 지역난방은 단독주택, 집합주택, 고층빌딩, 메가타운십 등에서 널리 이용되고 있습니다. 지역 난방이 필요한 주요 주택용도는 공간 난방과 온수입니다. 지역 난방 시장은 덴마크, 아이슬란드, 독일, 미국 및 기타 EU 국가, 캐나다와 같은 추운 기후 국가에서 확립되었습니다.

- 그러나 신재생에너지원을 동력원으로 하는 지역난방망은 배출량을 크게 줄이고 정부가 배출감소 목표를 달성하는 데 도움이 될 수 있습니다. 다양한 정부가 보조금, 보조금, 에너지세 등의 법적 책임과 인센티브를 마련해 열발전에서의 재생가능에너지 비율을 높이고 있습니다.

- 또한 지역 난방은 이전에는 주로 발전소, 폐기물 발전 시설, 산업 활동의 제품별을 이용했습니다. 그러나 스웨덴은 현재 더 많은 재생 가능 에너지를 통합하고 있습니다. 경쟁에 의해 이 지역 밀착형의 전력은 전국 톱의 가정용 난방 산업에 올라갔습니다.

- BDH에 따르면 2023년 독일에서는 약 79만 500대의 가스 난방 시스템이 판매되었습니다. 이 중 약 9만 4,000대가 기존 저온 기술을 채용하고, 69만 6,500대 이상이 콘덴싱 보일러 기술을 선택하고 있습니다.

아시아태평양이 지역 난방 시장에서 큰 점유율을 차지

- 중국 시장의 성장을 이끌고 있는 주된 이유는 가처분 소득 증가, CO2 배출 우려 증가, 냉난방 시스템의 높은 사용률입니다. 또한 OECD는 인도와 중국의 1인당 GDP가 2060년까지 7배가 될 것으로 예측했습니다.

- 아시아태평양 정부도 현지 기업과 협력하여 가정용 시장을 개척하고 있습니다. 예를 들어, 베이징구 난방 집단은 중국의 주요 난방 회사입니다. 이 회사는 베이징 중앙 정부 및 군, 중국 대사관, 중요한 기업과 조직, 일반 시민에게 난방 솔루션을 제공합니다. 또한 다른 지방에서도 많은 프로젝트가 있습니다.

- 현대 지역 난방 시스템은 대기 오염이 장기적인 경제적 비용과 수십만 명의 조기 사망을 일으키는 동남아시아 국가들에게 특히 중요합니다. 동남아시아의 냉방의 미래는 2040년까지 예상되는 에너지 소비, 피크 전력 수요, CO2 배출량의 성장을 조사했습니다.

- 인도와 호주는 이 지역의 2대 시장입니다. 이 지역 시장은 지역 냉난방 솔루션에 대한 투자가 증가하고 이러한 솔루션을 홍보하기 위해 정부 활동이 활발해짐에 따라 상승하고 있습니다.

- 에너지 위기와 기후 변화에 대응하기 위해 한국 정부는 제로에너지 빌딩을 추진하는 국가계획을 책정하고 최근 동향에서는 이러한 계획을 달성하기 위해 신축 및 기존 건물에 대한 몇 가지 에너지 효율화 정책이 책정되고 있습니다.

지역 난방 산업 개요

지역 난방 시장의 경쟁은 완만하며 많은 세계 기업과 지역 기업이 존재합니다. 이러한 기업들은 전 세계적으로 소비자층을 넓히기 위해 열심히 노력하고 있습니다. 예측기간 동안 경쟁 우위를 확보하기 위해 혁신적 솔루션 개발에 있어서 연구개발비, 전략적 제휴, 기타 유기적 및 무기적 성장 전술도 우선하고 있습니다.

2023년 5월, Vattenfall AB와 Coca-Cola는 스웨덴에서 협업을 발표하고 2040년까지 밸류체인 전반에 걸쳐 넷 제로 방출을 달성하는 야심찬 기후 변화 목표를 세웠습니다. 양사는 전기 수송의 전력 수요를 충족시키기 위해 3개의 충전소을 갖춘 파일럿 프로젝트를 시작했습니다.

2023년 3월, NRG Energy는 Vivint Smart Home의 인수를 완료하고, NRG의 소비자 중시 성장 전략을 가속화하고, 소비자에게 가정의 전력 공급, 보호, 관리를 지능적으로 실시하는 간단하고 커넥티드한 체험을 제공합니다. NRG는 에너지와 가정용 서비스의 교차로에 위치해 있으며, 탁월한 고객 경험을 지원하는 독자적인 엔드 투 엔드 스마트 홈 에코시스템을 제공합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 업계 밸류체인 분석

- 시장에 대한 COVID-19의 영향

- 지역난방이행에 관한 정부의 대처와 프로그램

- 지역난방의 주요 동향과 혁신

제5장 시장 역학

- 시장 성장 촉진요인

- 에너지 효율이 높고 비용 효율적인 난방 시스템에 대한 수요 증가

- 도시화와 산업화의 진전

- 시장 성장 억제요인

- 높은 인프라 비용

제6장 시장 세분화

- 플랜트 유형별

- 보일러

- 열병합발전(CHP)

- 열원별

- 석탄

- 천연가스

- 신재생에너지

- 석유 및 석유제품

- 용도별

- 주택

- 상업 및 공업

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Vattenfall AB

- SP Group

- Danfoss Group

- Engie

- NRG Energy Inc.

- Statkraft AS

- Logstor AS

- Shinryo Corporation

- Vital Energi Ltd

- Gteborg Energi

- Alfa Laval AB

- Ramboll Group AS

- Keppel Corporation Limited

- FVB Energy

제8장 투자 분석

제9장 미래의 기회

JHS 25.04.07The District Heating Market size is estimated at USD 53.46 billion in 2025, and is expected to reach USD 57.84 billion by 2030, at a CAGR of 1.59% during the forecast period (2025-2030).

District energy is a quick-growing industry globally, supported by the aggressive climate objectives set by the global economies. Based on initial assessments, these district heating and cooling companies have been recognized as operations that could produce more extraordinary growth and value potential with an alternative holding structure. By including electrically powered heat pumps in the district heating supply, higher renewable energy levels can be used for thermal purposes, generating integration and balance between energy systems. With a burgeoning global wind turbine capacity, big heat pumps will play a meaningful role in the sustained global green energy development and phasing out fossil fuels by 2050.

Key Highlights

- District heating provides a method of delivering thermal energy to buildings (homes and commercial space) in the form of hot water through a distribution network of highly insulated pipelines. The potential for increased use of industrial district heating is limited because conversions of industrial processes to district heating involve varying heat loads amongst types of industries and processes.

- However, the conversion to district heating serves an 11% reduction in the use of electricity and a 40% reduction in the use of fossil fuels, with a total energy end-use saving of 6% among industries.

- Converting the industrial processes has led to a potential reduction of global carbon dioxide emissions by 112,000 tons per year. However, the residential and commercial markets are expected to hold a significant share.

- Approximately 60 million EU citizens are served by district heating, and an additional 140 million people live in cities with at least one district heating system. According to reports by the EU and the IEA, DH meets around 11-12% of the EU's heat demand via 6,000 district heating and cooling networks.

- With machine learning, the idea is to predict heat loads from customer data and operational data, along with weather forecasts, national holidays, weekdays, etc., to optimize and plan heat production, thereby lowering heat loss and handling peak loads. The potential is extended to intelligent algorithms in fault detection to identify leakages, inefficient heating systems, or errors from failure related to single components.

- In June 2024, Swedish SMR project developer Karnfull Next has strategically partnered with Finnish counterpart Steady Energy to introduce SMRs for district heating in Sweden. The collaboration aims to capitalize on Karnfull's unique financing structures and delivery models to introduce Steady Energy's renowned district heating reactors to the Swedish market.

District Heating Market Trends

Residential to Witness the Growth

- District heating is commonly used in industrialized nations worldwide. It has several advantages over individual building equipment, including improved safety and dependability, lower emissions, and greater fuel flexibility, particularly when utilizing alternative fuels such as biomass or garbage.

- District heating is widely utilized in single-family houses, multi-family dwellings, high-rise buildings, and mega townships. The primary home uses that require district heating are space and water heating. District heating markets are well-established in several cold-climate nations, such as Denmark, Iceland, Germany, the United States, other EU countries, and Canada.

- However, the District heating networks powered by renewable energy sources may significantly reduce emissions and help governments meet their emission reduction objectives. Various governments have established statutory responsibilities and incentives, such as grants, subsidies, and energy taxes, to boost the percentage of renewables in heat generation.

- Moreover, District heating was previously primarily powered by byproducts of power plants, waste-to-energy facilities, and industrial activities. However, Sweden is now incorporating more renewable energy sources into the mix. Due to competition, this localized kind of electricity has risen to the national top home-heating industry.

- According to BDH, in 2023, Germany saw sales of approximately 790,500 gas heating systems. Among these, approximatly 94,000 employed traditional low-temperature technology, with the majority, over 696,500, opting for condensing boiler technology.

Asia-Pacific Holds a Significant Share in the District Heating Market

- The primary reasons driving the market's growth in China are rising disposable income, increased worries about CO2 emissions, and high usage of heating and cooling systems. Moreover, OECD states that projections for India and China's per capita GDP might climb sevenfold by 2060.

- Governments in the Asia-Pacific region are also collaborating with local businesses to develop the home market. For example, the Beijing District Heating Group is a major heating firm in China. The firm provided heating solutions to the central Beijing government and army, Chinese embassies, significant corporations and organizations, and the general people. It also has a large number of projects in other provinces.

- Modern district heating systems are especially important for Southeast Asian countries, where air pollution causes long-term economic expenses and hundreds of thousands of premature fatalities. The Future of Cooling in Southeast Asia investigates the anticipated growth in energy consumption, peak power demand, and CO2 emissions by 2040.

- India and Australia are two of the region's biggest marketplaces. The regional market is rising due to increased investment in district heating and cooling solutions and increased government activities to promote these solutions.

- To respond to energy crises and climate change, the South Korean government established a national plan to promote zero energy buildings, and several energy efficiency policies for new and existing buildings in recent years have been developed to achieve these plans.

District Heating Industry Overview

The district heating market is moderately competitive and has many global and regional players. These companies are working hard to broaden their consumer base globally. To gain a competitive advantage during the predicted term, they also prioritize R&D expenditure in developing innovative solutions, strategic collaborations, and other organic and inorganic growth tactics.

In May 2023, Vattenfall AB and Coca-Cola announced the collaboration in Sweden and have set ambitious climate targets for net zero emissions across their entire value chains by 2040. The companies have initiated a pilot project with three charging stations to meet the need for powering electric transport.

In March 2023, NRG Energy Inc completed its acquisition of Vivint Smart Home, Inc. by accelerating NRG's consumer-focused growth strategy and offering consumers simple, connected experiences to power, protect, and manage their homes intelligently. NRG is at the intersection of energy and home services, with a unique end-to-end smart home ecosystem underpinned by our exceptional customer experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

- 4.5 Government Initiatives and Programs on District Heating Transition

- 4.6 Key Trends and Innovations in District Heating

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Energy-efficient and Cost-effective Heating Systems

- 5.1.2 Rising Urbanization and Industrialization

- 5.2 Market Restraints

- 5.2.1 High Infrastructure Cost

6 MARKET SEGMENTATION

- 6.1 By Plant Type

- 6.1.1 Boiler

- 6.1.2 Combined Heat and Power (CHP)

- 6.2 By Heat Source

- 6.2.1 Coal

- 6.2.2 Natural Gas

- 6.2.3 Renewables

- 6.2.4 Oil and Petroleum Products

- 6.3 By Application

- 6.3.1 Residential

- 6.3.2 Commercial and Industrial

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vattenfall AB

- 7.1.2 SP Group

- 7.1.3 Danfoss Group

- 7.1.4 Engie

- 7.1.5 NRG Energy Inc.

- 7.1.6 Statkraft AS

- 7.1.7 Logstor AS

- 7.1.8 Shinryo Corporation

- 7.1.9 Vital Energi Ltd

- 7.1.10 Gteborg Energi

- 7.1.11 Alfa Laval AB

- 7.1.12 Ramboll Group AS

- 7.1.13 Keppel Corporation Limited

- 7.1.14 FVB Energy