|

시장보고서

상품코드

1689813

환자 중심 헬스케어 앱 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Global Patient-centric Health Care App - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

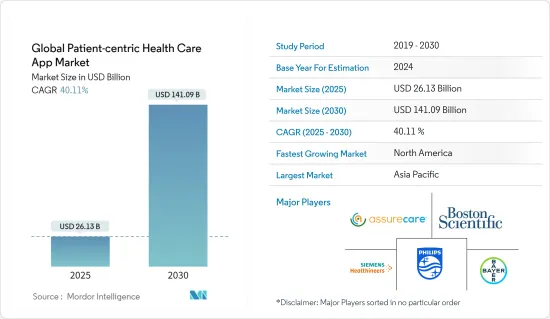

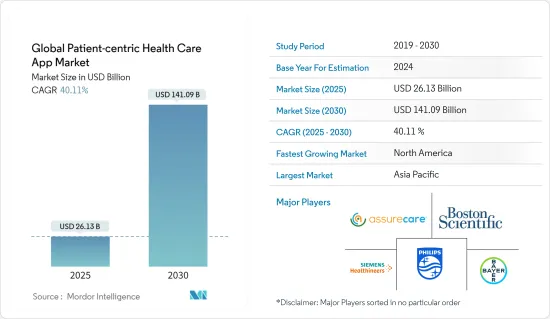

세계의 환자 중심 헬스케어 앱 시장 규모는 2025년 261억 3,000만 달러로 추정되며, 예측 기간(2025-2030년) 중 CAGR 40.11%로 확대되어, 2030년에는 1,410억 9,000만 달러에 달할 것으로 예측됩니다.

COVID-19의 대유행은 의료 산업에 영향을 주었습니다. COVID-19의 유행은 모든 산업 부문의 혼란, 과제, 제한, 변화에 연결되었습니다.

따라서 환자는 당뇨병이나 고혈압 등의 만성 질환을 관리하기 위해 앱을 이용하는 경향이 강해졌으며, COVID-19 관리를 위해 많은 환자 케어 앱이 시작되었습니다.

예를 들어 2020년 12월 Journal of Medical Internet Research에 게재된 Haridimos Kondylakis 등의 조사 연구에 따르면 모바일 앱은 병원 부담 감소, 개인 증상 및 정신 상태 추적, 신뢰할 수있는 정보에 대한 액세스 제공, 새로운 예측 인자 발견 등 유행에 의해 부과된 심각한 과제에 직면하는 의료 전문가, 시민, 의사 결정자에게 있어서 귀중한 툴이라고 생각되어 의료 제공업체와 소비자 모두로부터 산업 전체에서 모바일 헬스 앱의 높은 채용으로 이어졌습니다.

시장 성장을 가속하는 주요 요인은 특히 노인층에서 암, 당뇨병, 류마티스 관절염 등의 만성 질환의 발생률 증가를 포함합니다.

예를 들어 IDF Diabetes Atlas Tenth edition 2021년에 따르면 2021년에는 약 5억 3,700만 명의 성인이 당뇨병을 앓고 있습니다.

2021년 10월에 발표된 세계보건기구(WHO)의 데이터에 따르면 2015-2050년까지 세계의 60세 이상의 인구 비율은 12%에서 22%로 거의 두배로 늘어나 고령자의 80%는 저소득 및 중소득국에 살게 됩니다. 어느 나라도, 의료 사회 시스템이 이 인구 동태의 변화를 최대한 활용할 수 있도록 하는 큰 과제에 직면하고 있습니다. 이것이 시장을 견인할 것으로 예상됩니다. 이와 같이, 노인 증가, 전자 차트 시스템을 유지하기 위한 정부의 이니셔티브의 높아, 투약 미스를 회피하기 위한 기술 기반의 치료에 대한 수요 증가는 예측 기간동안 환자 중심 헬스케어 앱 시장을 견인할 가능성이 높습니다.

환자 중심 헬스케어 앱 시장 동향

전화 기반 앱 하위 부문이 환자 중심 헬스케어 앱 시장에서 큰 시장 점유율을 차지할 전망

예측 기간 동안 환자 중심 헬스케어 앱 시장 전반에 걸쳐 전화 기반 앱이 최대 수익 공유를 차지할 것으로 예측됩니다.

COVID-19 팬데믹 2020 동안 의료, 행복, 사회적 연결의 유지는 노인에게 매우 중요했습니다. Dina M. El-Sherif & MohamedAbouzid가 2022년 6월에 발표한 조사 연구에 따르면, 모바일 애플리케이션은 COVID-19 팬데믹 동안 COVID-19 이외의 관리나 환자에서 중요한 역할을 수행했습니다. 2021년 1월, Dell Technologies는 보건가족 복지부와 Tata Trusts와 공동으로 전국 정부 1차 의료센터(PHC)에서 비감염성 질환을 관리하기 위한 모바일 애플리케이션를 개발했습니다.

세계적으로 스마트폰 사용자의 보급이 진행되고 원격 의료 및 모바일 헬스 서비스에 대한 수요가 높아지는 가운데, 원격 의료 서비스를 제공하는 기업이 모든 이점을 갖춘 용도를 출시하기 때문에 전화 기반의 건강 용도 부문은 예측 기간 동안 성장할 것으로 예상됩니다.

전화 기반 건강 관리 용도의 다른 이점은 대화형, 사용자 친화적인 인터페이스, 진단에서 결제까지의 통합 솔루션, 사용자의 최신 정보를 유지하기위한 정기적인 통지, 제공업체 및 기능에 따라 전화 기반 건강 관리 용도를 인터넷없이 사용할 수 있습니다.

북미가 시장을 독점, 예측기간 동안도 마찬가지로 예측

북미는 예측기간을 통해 환자 중심 헬스케어 앱(PCHA) 시장 전체를 지배할 것으로 예상됩니다.

미국 심장병학회(American College of Cardiology Foundation) 2021에 따르면, 미국에서는 2020년 COVID-19 유방교환시 고혈압성 질환과 허혈성 심장질환으로 인한 사망이 증가하였으며, 미국에서 유행병 시 환자 중심 의료 앱이 질병 관리에 사용되게 되었습니다.

고령자 증가와 만성질환의 부담이 큰 동국은 시장 성장을 뒷받침할 것으로 예상됩니다. 지속적인 모니터링에 대한 요구가 있으며, 환자 중심 헬스케어 앱은 언메트 요구를 충족하기 때문에 예측 기간 동안 성장을 보일 것으로 예상됩니다.

게다가 의료 지출 증가, 건강 의식, 임상 중심의 치료에서 환자 중심 치료로의 시프트가 이 지역 시장을 밀어 올리고 있습니다.

환자 중심 헬스케어 앱 산업 개요

환자 중심 헬스케어 앱 시장의 경쟁은 중간 정도입니다. 시장 포지션을 확대하고 있는 기업도 있습니다. 시장 기업에는 Koninklijke Philips N V, Merck & Co. Inc., Hill-Rom Holdings Inc., Bayer AG, Siemens Healthineers AG 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 만성질환의 유병률 증가와 노인 증가

- 신기술에 의한 액세스의 향상과 유연성

- 시장 성장 억제요인

- 개발 비용의 높이

- 일반 의료 제공업체에 의한 소극적 자세

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 운영 형태별

- 전화 기반

- 웹 기반

- 하이브리드 환자 중심 앱

- 용도별

- 웰니스 관리

- 질병 및 치료 관리

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Boston Scientific Corporation

- Assurecare LLC(IPatient Care)

- Merck & Co. Inc.

- MobileSmith Inc.

- Koninklijke Philips NV

- Pfizer Inc.

- Siemens Healthineers AG

- Novartis AG

- Bayer AG

- Baxter International Inc.(hillrom Services, Inc.)

- athenahealth Inc.

- Allscripts Healthcare Solutions Inc.

- International Business Machines Corporation(IBM)

- Mfine Pvt. Ltd

- Oracle(cerner Corporation)

제7장 시장 기회와 앞으로의 동향

JHS 25.05.07The Global Patient-centric Health Care App Market size is estimated at USD 26.13 billion in 2025, and is expected to reach USD 141.09 billion by 2030, at a CAGR of 40.11% during the forecast period (2025-2030).

The COVID-19 pandemic had an impact on the healthcare industry. The outbreak of COVID-19 led to disruption, challenges, limitations, and changes in every industry sector. The pandemic also impacted the studied market. The outbreak of COVID-19 showed a positive impact on the market, as lockdowns led to the lower availability of doctors in clinical settings.

Thus, patients were more inclined to use apps to manage their chronic conditions, such as diabetes, hypertension, and other chronic diseases. Moreover, there have been a large number of patient care apps launched for COVID-19 management. Nationwide lockdowns resulted in providing healthcare services by the hospitals and clinics, which led to the rise in the use of patient-centric healthcare app that aims toward the management of diseases.

For instance, according to a research study by Haridimos Kondylakis et al., published in the Journal of Medical Internet Research in December 2020, mobile apps were considered to be a valuable tool for health professionals, citizens, and decision-makers in facing critical challenges imposed by the pandemic such as reducing the burden on hospitals, tracking the symptoms and mental health of individuals, providing access to credible information, and discovering new predictors, leading to the high adoption of mobile health apps across the industry both from providers and consumers.

The major factors driving the market growth include the increased incidence of chronic disorders, such as cancers, diabetes, and rheumatoid arthritis, especially in the geriatric population. Treating chronic diseases requires continuous monitoring and evaluation of physiological changes for proper diagnosis and medication.

For instance, as per the IDF Diabetes Atlas Tenth edition 2021, in 2021, about 537 million adults were living with diabetes. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The increasing number of diabetes patients drives them to demand more monitoring apps and drives the market

According to World Health Organization (WHO) data published in October 2021, between 2015 and 2050, the proportion of the global population over 60 years will nearly double from 12% to 22% in 2050, and 80% of older people will be living in low- and middle-income countries. All countries face major challenges in ensuring their health and social systems are ready to make the most of this demographic shift. Thus, healthcare apps come in the role of monitoring vital parameters. This is expected to drive the market. Thus, the growing elderly population, rise in government initiatives to maintain electronic health record systems, and increased demand for technology-based treatment to avoid medication errors are likely to drive the patient-centric healthcare app (PCHA) market over the forecast period.

Patient Centric Healthcare App Market Trends

The Phone-based Apps Sub-segment is Expected to Hold Significant Market Share in the Patient-centric Healthcare App Market

The phone-based apps are expected to account for the largest revenue share in the overall patient-centric healthcare app market over the forecast period.

During the COVID-19 pandemic 2020, the maintenance of healthcare, well-being, and the social connection was crucial for the elderly population. Many mobile health apps were launched after countries relaxed their telehealth regulations to combat the COVID-19 pandemic. Mobile health apps help patients with their health conditions, and physicians deliver the services on their premises. According to the research study published in June 2022 by Dina M. El-Sherif& Mohamed Abouzid, mobile applications played a crucial role during the COVID-19 pandemic in management and patients other than COVID-19. Additionally, in January 2021, in India, Dell Technologies, in collaboration with the Ministry of Health and Family Welfare and Tata Trusts, developed a mobile application to manage non-communicable diseases at the government primary health centers (PHCs) across the country.

With the growing penetration of smartphone users globally and increasing demand for telehealth and mobile health services, the phone-based health application segment is expected to grow over the forecast period as companies offering telehealth services launch their applications with all the benefits.

Other advantages of phone-based health applications include an interactive and user-friendly interface, integrated solutions from consultation to payment, regular notification to keep the user updated, and depending upon the provider and function, phone-based healthcare applications can also be used without the internet. All these factors are collectively expected to boost growth in the studied segment over the forecast period.

North America Dominates the Market and Expected to do the Same in the Forecast Period.

North America is expected to dominate the overall patient-centric healthcare app (PCHA) market throughout the forecast period. The dominance is due to the region's huge target population base with chronic diseases, such as coronary heart diseases, atrial fibrillation, stroke, hypertension, and diabetes.

As per the American College of Cardiology Foundation 2021, deaths from hypertensive diseases and ischemic heart disease in the United States increased during the COVID-19 pandemic in 2020, leading to the increasing use of patient-centric health care apps during the pandemic in the United States in the management of the disease.

The rising geriatric population and the country's high burden of chronic diseases are expected to boost market growth. For instance, Heart disease is the main cause of death in the United States, according to the Centers for Disease Control and Prevention (CDC) September 2020. Around 805,000 Americans experience a heart attack each year. As the number of deaths due to heart diseases is increasing, there is a continuous need for the proper monitoring of cardiac diseases, and patient-centric healthcare apps fulfill the unmet needs; hence it is expected to show growth over the forecast period. Additionally, According to the American Diabetes Federation 2019 report, an estimated 463 million adults live with diabetes worldwide, which is estimated to reach 700 million by 2045.

Furthermore, a rise in healthcare expenditure, health awareness, and a shift from clinical-centric treatment to patient-centric care boost the market in the region. The growing adoption of technology by key healthcare providers in the region is expected to contribute to a significant global market share throughout the forecast period.

Patient Centric Healthcare App Industry Overview

The patient-centric healthcare app market is moderately competitive. Some companies are expanding their market position while others are adopting various strategies, such as mergers and acquisitions, introducing new products, and upgrading technologies, to maintain their market position. Some market players are Koninklijke Philips N V, Merck & Co. Inc., Hill-Rom Holdings Inc., Bayer AG, and Siemens Healthineers AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases and Rising Geriatric Population

- 4.2.2 Enhanced Access and Flexibility with Novel Technologies

- 4.3 Market Restraints

- 4.3.1 The High Cost of Development

- 4.3.2 Reluctance by Regular Healthcare Providers

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Mode of Operation

- 5.1.1 Phone-based

- 5.1.2 Web-based

- 5.1.3 Hybrid Patient-centric Apps

- 5.2 By Application

- 5.2.1 Wellness Management

- 5.2.2 Disease And Treatment Management

- 5.2.3 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Boston Scientific Corporation

- 6.1.2 Assurecare LLC (IPatient Care)

- 6.1.3 Merck & Co. Inc.

- 6.1.4 MobileSmith Inc.

- 6.1.5 Koninklijke Philips NV

- 6.1.6 Pfizer Inc.

- 6.1.7 Siemens Healthineers AG

- 6.1.8 Novartis AG

- 6.1.9 Bayer AG

- 6.1.10 Baxter International Inc. (hillrom Services, Inc.)

- 6.1.11 athenahealth Inc.

- 6.1.12 Allscripts Healthcare Solutions Inc.

- 6.1.13 International Business Machines Corporation (IBM)

- 6.1.14 Mfine Pvt. Ltd

- 6.1.15 Oracle (cerner Corporation)