|

시장보고서

상품코드

1690091

북미의 소형 위성 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)North America Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

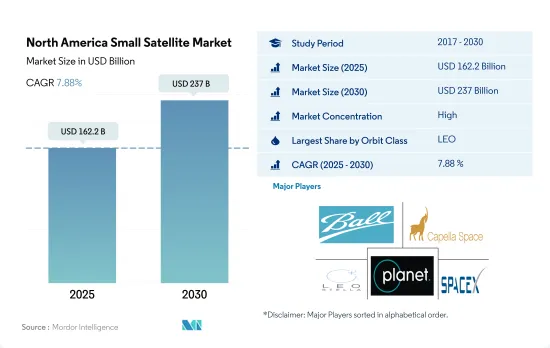

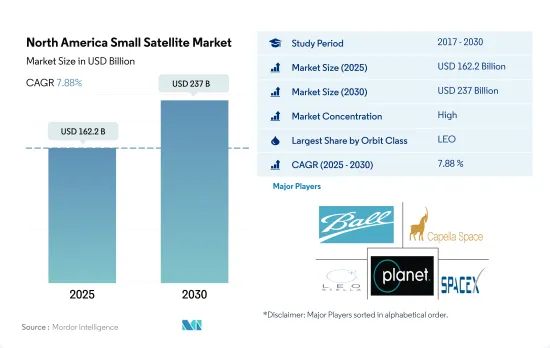

북미의 소형 위성 시장 규모는 2025년에 1,622억 달러에 달할 것으로 추정됩니다. 2030년에는 2,370억 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 7.88%를 나타낼 것으로 전망됩니다.

LEO 위성이 소형 위성 수요를 견인

- 발사할 때 위성과 우주선은 대개 지구를 돌아 다니는 많은 특별한 궤도 중 하나에 배치됩니다. 지구궤도에는 정지궤도(GEO), 중궤도, 저궤도의 3유형가 있습니다. 많은 기상 위성과 통신 위성은 지상에서 가장 먼 지구 높은 궤도에있는 경향이 있습니다. 지구 궤도에 있는 위성에는 특정 지역을 모니터링하도록 설계된 항법 위성 및 특수 위성이 포함됩니다. NASA의 지구 관측 시스템을 포함한 대부분의 과학 위성은 지구 저궤도에 있습니다.

- 소형 위성 시장은 통신, 항법, 지구 관측, 군사 정찰, 과학 미션에 사용되는 LEO 위성 수요 증가에 견인되어 강력한 성장을 이루고 있습니다. 2017년부터 2022년에 걸쳐, 북미만으로 주로 통신 목적으로 약 2,900기의 LEO 소형 위성이 제조·발사되었습니다. 이를 위해 SpaceX, OneWeb, Amazon 등 주요 기업들은 LEO에 수천 개의 위성 발사를 계획하고 있습니다. 지구 관측, 내비게이션, 기상학, 군사통신 등 다양한 분야에서 저궤도에 대한 수요가 높아지면서 이 지역에서는 LEO 위성 발사 수가 증가하고 있습니다.

- MEO 위성과 GEO 위성의 군사 이용은 신호 강도의 향상, 통신·데이터 전송 능력의 향상, 커버 에리어의 확대 등의 이점에 의해 최근 확대되고 있습니다. 예를 들어, 레이세온 테크놀로지스와 보잉사의 밀레니엄 스페이스 시스템즈사는 미국 우주군을 위한 극초음속 미사일을 감지하고 추적하는 MTC(Missile Track Custody) MEO OPIR 페이로드의 최초 프로토타입을 개발하고 있습니다.

북미의 소형 위성 시장 동향

더 나은 연료 사용과 운영 효율의 동향을 볼 수

- 위성의 소형화가 진행되고 있습니다. 소형 위성은 전통적인 위성의 몇 분의 하나의 비용으로 거의 모든 것이 가능하기 때문에 소형 위성 별자리의 구축, 발사 및 운영이 점점 실행 가능 해지고 있습니다. 또한 소형 위성에 대한 의존도도 비약적으로 높아지고 있습니다. 소형 위성은 일반적으로 개발 사이클이 짧고 개발 팀도 소규모이며 발사 비용도 훨씬 낮습니다. 혁명적인 기술의 진보는 전자의 소형화를 촉진하고, 스마트 소재의 발명을 뒷받침하고, 위성 버스의 크기와 질량을 제조업체가 시간이 지남에 따라 줄였습니다.

- 위성은 질량에 따라 분류됩니다. 질량이 500kg 미만인 위성은 소형 위성으로 간주되어 역사적인 기간에 이 지역에서 약 2,900개 이상의 소형 위성이 발사되었습니다. 개발 기간이 짧고 전체 임무 비용을 줄일 수 있기 때문에이 지역에서는 소형 위성에 대한 경향이 커지고 있습니다. 소형 위성은 과학적 및 기술적 성과를 얻는 데 필요한 시간을 크게 단축합니다. 소형 위성의 미션은 유연성이 높고 새로운 기술적 기회와 요구에 대응하기 쉬운 경향이 있습니다. 미국의 소형 위성 산업은 특정 용도에 특화된 소형 위성을 설계 및 제조하기 위한 견고한 프레임워크의 존재에 지원되고 있습니다. 북미의 소형 위성 사업자 수는 상업·군사 우주 분야에서 수요 증가에 의해 2023-2029년에 급증할 것으로 예상됩니다.

다양한 우주 기관의 우주 지출 증가는 북미의 소형 위성 시장에 긍정적인 영향을 미칠 것으로 예상됩니다.

- 북미에서는 우주계획을 위한 정부지출이 2021년 약 1,030억 달러의 기록을 세웠습니다. 이 지역은 세계 최대의 우주 기관인 NASA의 존재로 인해 우주 혁신과 연구의 진원지가 되고 있습니다. 2022년 미국 정부는 우주 프로그램에 약 620억 달러를 지출하고 세계에서 가장 우주 개발비를 던지는 나라가 되었습니다.

- 미국은 인공위성의 개발과 발사에서 세계 유수의 나라입니다. 상업 및 방위용도의 여러 측면에서 헤아릴 수 없기 때문에 위성의 사용은 이 나라에서 크게 받아 들여지고 있습니다. 이 나라에는 상업 및 방어 요구에 부응하기 위해 우주 공간을 돌아 다니는 많은 위성이 있습니다. 2022년 12월, 플래닛 랩은 스페이스 X사의 팔콘 9 로켓을 사용하여 발사 예정인 36대의 슈퍼더브 위성을 제조했다고 발표했습니다. 각 SuperDove 위성의 무게는 약 6kg이며, 이러한 위성에 의해 수집된 데이터는 농업, 정부, 민간 기관 및 기타 산업 조직에 정보 기반 의사 결정을 제공할 것으로 기대됩니다.

- 2022년 11월, NASA는 TROPICS 미션에서 4대의 큐브 서트 발사를 계획하고 있다고 발표했습니다. 이 위성의 무게는 약 5.3kg으로 폭풍우의 강도, 폭풍우 내 및 주변 환경의 온도와 습도의 수평 및 수직 구조의 관측을 신속하게 업데이트하기 위해 개발되었습니다. 수집된 데이터는 과학자들이 이러한 영향력이 큰 폭풍우에 영향을 미치는 과정을 더 잘 이해하는 데 도움이 되며, 궁극적으로 모델링과 예측 개선으로 이어질 것으로 기대됩니다.

북미의 소형 위성 산업 개요

북미의 소형 위성 시장은 상당히 통합되어 있으며 상위 5개사에서 99.57%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Ball Corporation, Capella Space Corp., LeoStella, Planet Labs Inc. and Space Exploration Technologies Corp(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 위성의 질량

- 우주 프로그램에 대한 지출

- 규제 프레임워크

- 캐나다

- 미국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 용도

- 통신

- 지구 관측

- 네비게이션

- 우주 관측

- 기타

- 궤도 등급

- GEO

- LEO

- MEO

- 최종 사용자

- 상업

- 군사 및 정부

- 기타

- 추진 기술

- 전기

- 가스

- 액체 연료

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Ball Corporation

- Capella Space Corp.

- LeoStella

- National Aeronautics and Space Administration(NASA)

- Planet Labs Inc.

- Space Exploration Technologies Corp

- SpaceQuest Ltd

- Spire Global, Inc.

- Swarm Technologies, Inc.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The North America Small Satellite Market size is estimated at 162.2 billion USD in 2025, and is expected to reach 237 billion USD by 2030, growing at a CAGR of 7.88% during the forecast period (2025-2030).

LEO satellites are driving the demand for small satellites

- During launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. There are three types of Earth orbits, namely, geostationary orbit (GEO), medium Earth orbit, and low Earth orbit. Many weather and communication satellites tend to have high Earth orbits farthest from the surface. Satellites in medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- The small satellite market is experiencing strong growth, driven by the increasing demand for LEO satellites, which are used for communication, navigation, Earth observation, military reconnaissance, and scientific missions. Between 2017 and 2022, around 2,900 small LEO satellites were manufactured and launched in North America alone, primarily for communication purposes. This has led companies such as SpaceX, OneWeb, and Amazon to plan the launch of thousands of satellites into LEO. With the rising demand for low Earth orbit from various sectors like Earth observation, navigation, meteorology, and military communications, the region has witnessed an increase in the number of LEO satellite launches.

- The military's use of MEO and GEO satellites has grown in recent years due to their advantages, including increased signal strength, improved communications and data transfer capabilities, and greater coverage area. For instance, Raytheon Technologies' and Boeing's Millennium Space Systems are developing the first prototype Missile Track Custody (MTC) MEO OPIR payloads to detect and track hypersonic missiles for the US Space Force.

North America Small Satellite Market Trends

A trend of using better fuel and operational efficiency has been witnessed

- Satellites are getting smaller nowadays. A small satellite can do almost everything as a conventional satellite at a fraction of the cost, thus making the building, launching, and operation of the small satellite constellations increasingly viable. The reliance on small satellites has also been growing exponentially. Small satellites typically have shorter development cycles, smaller development teams, and cost much lesser for launch. Revolutionary technological advancements facilitated the miniaturization of electronics, which pushed the invention of smart materials, reducing the satellite bus size and mass over time for manufacturers.

- Satellites are classified according to mass. The satellites with a mass of less than 500 kg are considered small satellites, and around 2,900+ small satellites were launched in the region during the historical period. There is a growing trend toward small satellites in the region due to their shorter development time, which can reduce overall mission costs. They have significantly reduced the time required to obtain scientific and technological results. Small spacecraft missions tend to be flexible and more responsive to new technological opportunities or needs. The small satellite industry in the United States is supported by the presence of a robust framework for designing and manufacturing small satellites tailored to serve specific application profiles. The number of small satellite operators in North America is expected to surge during 2023-2029 due to the growing demand in the commercial and military space sectors.

The increasing space expenditures of different space agencies are expected to impact the North American small satellite market positively

- In North America, government expenditure for space programs hit a record of approximately USD 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space in the world.

- The United States is one of the leading countries globally in terms of satellite development and launches. Owing to the immense potential in several aspects of commercial and defense applications, the use of satellites has gained substantial acceptance in the country. The country has many satellites orbiting in space to serve its commercial and defense needs. In December 2022, Planet Labs announced that it had manufactured 36 SuperDove satellites, scheduled for launch using SpaceX's Falcon-9 rocket. Each SuperDove satellite weighs approximately 6 kg, and the data collected by these satellites are expected to provide organizations in agriculture, government, civilian agencies, and other industries to make informed decisions.

- In November 2022, NASA announced that it is planning to launch four CubeSats under the TROPICS mission. These satellites weigh approximately 5.3 kg and are developed to provide rapidly updating observations of storm intensity, as well as the horizontal and vertical structures of temperature and humidity within the storms and in their surrounding environment. The data collected is expected to help scientists better understand the processes that affect these high-impact storms, ultimately leading to improved modeling and prediction.

North America Small Satellite Industry Overview

The North America Small Satellite Market is fairly consolidated, with the top five companies occupying 99.57%. The major players in this market are Ball Corporation, Capella Space Corp., LeoStella, Planet Labs Inc. and Space Exploration Technologies Corp (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ball Corporation

- 6.4.2 Capella Space Corp.

- 6.4.3 LeoStella

- 6.4.4 National Aeronautics and Space Administration (NASA)

- 6.4.5 Planet Labs Inc.

- 6.4.6 Space Exploration Technologies Corp

- 6.4.7 SpaceQuest Ltd

- 6.4.8 Spire Global, Inc.

- 6.4.9 Swarm Technologies, Inc.

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms