|

시장보고서

상품코드

1910864

전력 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

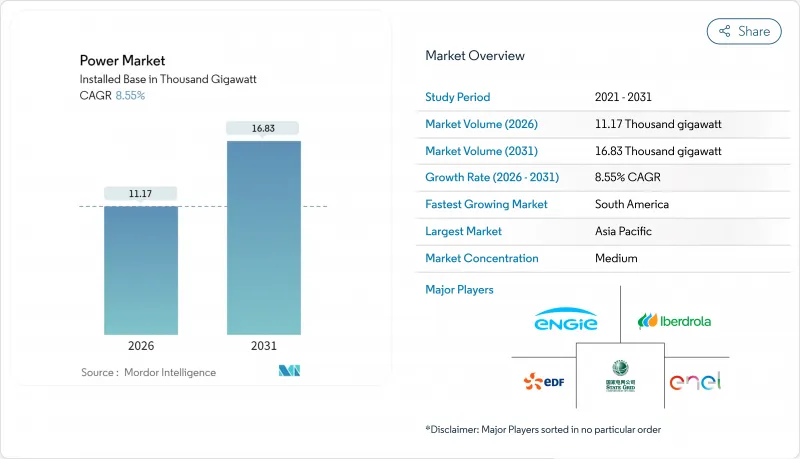

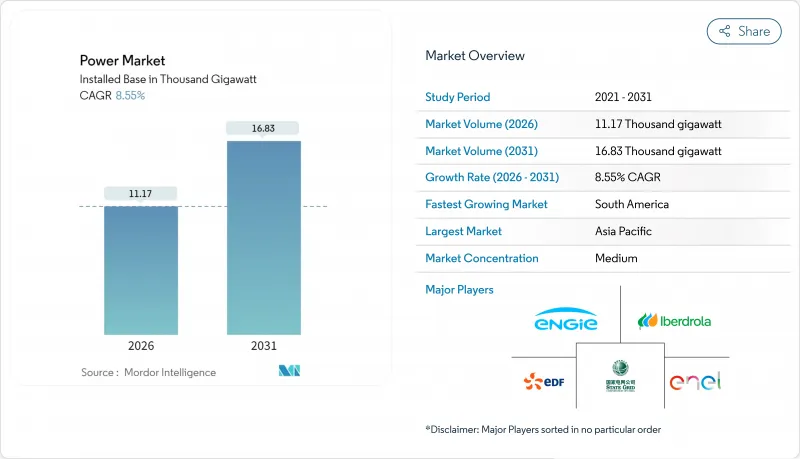

전력 시장은 2025년 1만 290기가와트로 평가되었으며, 2026년 1만 1,170기가와트에서 2031년까지 1만 6,830기가와트에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 8.55%로 예상됩니다.

용량 증가의 배경으로는 데이터센터 확장, 산업의 전기화, 그린 수소의 조기 도입으로 인한 전력 수요의 급증이 있습니다. 신규 용량의 거의 절반을 재생에너지가 차지하면서 배터리 저장 비용의 급격한 저하에 의해 수시간에 걸친 계통 유연성이 실현되는 혜택을 받고 있습니다. 정부 펀드와 연금 기금은 고전압 송전망의 업그레이드에 연간 1,800억 달러를 지속적으로 투입하고 있어 송전 부문에서의 경쟁을 격화시키고 있습니다. 한편, 송전망의 병목이나 허가절차의 지연에 의해 승인된 클린에너지 프로젝트의 23%가 정체될 우려가 있어 발전목표와 인프라 정비 사이에 불일치가 발생하고 있는 것으로 밝혀졌습니다.

세계의 전력 시장의 동향 및 인사이트

폭발적으로 증가하는 데이터센터의 전력 수요

2024년 데이터센터 전력 소비량은 460테라와트(TWh)에 이르렀으며, 아르헨티나의 연간 총 소비량은 세계 전력 소비량의 2%를 차지했습니다. 하이퍼스케일 시설의 평균 연속 전력 소비량은 100-200메가와트(MW)에 이르렀으며, 전력회사는 계통 연계 제도의 재협상과 변전소 업그레이드의 신속화를 요구받고 있습니다. 2024년에는 기술 대기업이 기존 전력 공급 모델을 회피하고 24시간 365일 재생에너지 확보를 도모하는 가운데 기업 바이어에 의한 청정 에너지 계약량은 23.7기가와트에 달했습니다. 버지니아의 '데이터센터 어레이'는 이미 주 내 발전량의 25%를 소비하고 있으며, 규제 당국은 용량 시장 참여 제도를 재검토하고 있습니다(PJM.com). 이러한 집중 부하는 전압 안정성의 리스크를 높여 소매 요금으로 전가되는 프리미엄 용량 계약 가격을 높이고 있습니다. 따라서 세계의 전력 시장은 10년 전에는 일반적이지 않았던 지역 베이스로드의 급증을 축으로 재조정이 진행되고 있습니다.

산업용 열 및 수송의 전기화

2024년에는 신규 철강 생산 능력의 73%를 전기 아크로가 차지했으며, 유럽의 산업용 열원 개보수에서는 40%의 히트 펌프가 천연 가스로 대체되었습니다. 모빌리티 분야에서는 1,410만대의 EV가 85TWh의 순 수요를 추가했지만, 280GWh의 V2G 저장을 제공해 저녁 시간대 피크 감소에 공헌했습니다. 북유럽의 송전망은 이 융합을 실증하고 있습니다. 동기화된 EV 충전 및 산업용 히트 펌프의 사이클은 시간 연동 소비 피크를 발생시키고, 세분화된 요금 신호와 AI 기반 디스패치에 의해 균형을 이룹니다. 알루미늄 정련소와 화학 단지는 저렴하고 안정적으로 공급 가능한 재생에너지를 확보하기 위해 이미 풍력 자원이 풍부한 지역으로 이전을 진행하고 있습니다. 이에 따라 15-20년에 걸친 전력 구입 계약이 체결되어 지역의 송전망 확장을 뒷받침하고 있습니다. 비슷한 움직임이 세계적으로 확산되고 있는 가운데, 세계의 전력 시장에서는 산업용 전력 소비가 15-20% 지속적으로 증가할 것으로 예측되며, 연간 450억 달러 규모의 배전망 강화가 요구되고 있습니다.

송전망의 병목과 허가 지연

송전 제약으로 인해 2024년에는 건설 준비가 완료된 신재생에너지 127GW가 보류되어 3,400억 달러의 투자 지연이 발생했습니다. 미국의 계통 연계 대기 용량은 2,600GW로 치솟아 현행 송전망 용량의 5배에 달하였고, 평균 심사 기간은 5.2년으로 연장되었습니다. 유럽의 크로스보더 송전선은 풍력발전이 활발한 시간대에 95%의 가동률을 나타내며 특히 스페인과 독일에서 47TWh의 출력 억제를 초래했습니다. 정책 수립자는 이에 대해 EU 넷 제로 산업법에 근거해 사전 구역 지정이 끝난 프로젝트의 심사 기간을 12개월로 제한하는 조치를 강구했지만, 지역 주민의 반대에 의해 여전히 초고압 직류 송전 설비(HVDC) 건설은 4건 중 1건이 지연되고 있습니다. 이러한 병목 현상이 해소되지 않으면 자본 선적과 투자자 신뢰의 저하를 초래하여 세계의 전력 시장의 탈탄소화 과정을 방해할 수 있습니다.

부문 분석

재생가능에너지는 2025년 설비용량의 47.95%를 차지하였으며, 2031년까지 연평균 CAGR 13.70%로 확대될 전망입니다. 이는 연간 역대 최고인 태양광 346GW, 풍력 116GW의 신규 도입이 뒷받침하고 있습니다. 해상 풍력은 23.10%의 연평균 복합 성장률(CAGR)로 성장할 전망이며 부유식 구조물에 의해 심해역 사이트를 개발하면서 일본, 한국, 캘리포니아에서의 도입이 가속하고 있습니다. 동시에 원자력발전소의 재가동과 소형모듈로(SMR)의 시험 도입은 산업용 열공급계약을 뒷받침하는 견고한 저탄소전원으로서 초기 단계이지만 전략적인 옵션을 추가합니다. 석탄 및 석유화력발전소는 폐지 또는 개보수가 계속 진행되고 있으며 2024년에는 47GW의 석탄화력발전소가 수소혼소발전으로 전환될 것으로 발표되었지만, 상업적 실현 가능성은 여전히 탄소가격이 톤당 80달러를 넘는 과제에 직면하고 있습니다.

신재생에너지의 보급률 상승에 따라 계획은 유연성 자산으로 중점을 옮깁니다. 2026년부터 2031년까지 세계의 송전망 운영자는 축전지, 양수발전, 수요응답, 송전망 접속설비의 확충에 누계 2조 8,000억 달러의 투자가 필요합니다. 축전지의 통합에 의해 태양광 발전의 주간 과잉 공급이 완화되는 한편, 국경을 넘은 초고압 직류 송전(HVDC) 링크가 잉여 풍력을 부하 중심지로 수송합니다. 이러한 수단이 확대됨에 따라 세계의 전력 시장은 단일 연료의 지배가 아니라 다양한 자원 구성에 의한 탄력성을 통합해 나갈 것입니다. 그러므로 신재생에너지의 급성장은 세계의 전력 시스템 전체에서 자본 배분, 규제 프레임워크 및 시장 가격 형성을 재정의합니다.

본 전력 시장 보고서는 전원별(화력, 원자력, 재생에너지), 최종 사용자별(전력회사, 상업 및 산업, 주택), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 규모와 예측은 설치 용량(GW) 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 44.20%의 용량 점유율로 세계의 전력 시장을 견인했으며 중국(1,411GW)과 인도(425GW)가 핵심을 이루고 있습니다. 중국은 연간 216GW의 신규 재생에너지 설비를 가동시켜 독일의 기존 설비 총량을 웃돌았지만, 동시에 그리드 관성을 확보하기 위해 47GW의 석탄 화력도 추가했습니다. 한편 인도는 태양광 발전의 확대 목표와 병행하여 2026년까지 50GWh의 축전 용량을 목표로 하는 지역별 축전지 입찰을 실시했습니다. 일본과 한국은 수입연료 의존도 감소를 위해 해상 풍력과 선진적 원자력발전에 주력하고 있습니다. 일본은 2040년까지 해상 풍력 45GW 달성을 계획하고, 한국은 12GW 규모의 부유식 태양광 발전의 실증을 진행하고 있습니다. 지역 통합의 과제는 여전히 심각하며, 중국 북서부에서는 송전망의 제약에 의해 재생에너지의 억제율이 8.2%를 넘어, 초고압 직류 송전(HVDC) 라인의 긴급성을 부각하고 있습니다.

남미는 세계의 전력 시장에서 가장 급속히 확대되는 지역으로 부상하여 CAGR 15.10%를 기록했습니다. 칠레의 그린 수소 허브와 아르헨티나 및 브라질의 리튬 전지를 활용한 계통 연계형 축전 수요가 견인 역할을 담당하고 있습니다. 브라질은 195기가와트의 설비 용량을 자랑하며 저비용 풍력 및 수력을 활용하여 광업 및 농업의 탈탄소화를 추진하고 있습니다. 칠레의 아타카마 사막의 태양광 발전 붐은 광업 수요와 수소 수출 터미널 모두에 전력을 공급하여 30달러/MWh 미만의 균등화 발전원가를 달성하고 있습니다. 신재생에너지 외에 아르헨티나의 바카 무에르타 혈암가스는 변동성이 높아지는 발전 설비를 안정화하는 견조한 용량 증가를 뒷받침하고 있습니다. 안데스-태평양 초고압 직류 송전선을 포함한 국경을 넘어선 연계선은 우기와 건기에 수력발전의 최적화를 도모하는 지역간 거래를 실현하고 있습니다.

유럽은 2025년 세계 설비 용량의 22.80%를 유지했으며, 2022년 가스 위기 이후 유연성과 에너지 안보 강화에 주력했습니다. 독일은 17GW의 재생에너지를 도입했고, 주파수 조정은 북유럽의 수력 발전과 프랑스의 원자력 발전 수입에 의존했습니다. 영국은 3.2GW의 해상 풍력을 추가하여 부유식 구조기술에서의 주도적 지위를 확고하게 했습니다. 그러나 성숙한 송전망은 포화 상태에 직면하고 있어 전력 가격이 마이너스가 되는 시간대가 증가하고, 축전의 경제성이 향상되어, 도매 시장에서는 결제 기간을 5분 단위로 재구축하는 움직임이 급속히 진행되고 있습니다. 북미와 중동 및 아프리카는 점유율에서 뒤쳐져 있지만 유망한 성장 지역으로 자리잡고 있습니다. 미국은 2024년 IRA 세제 우대조치에 힘입어 32GW의 재생에너지를 도입했습니다. UAE는 2071년 인터넷 제로 계획에 5.6GW의 태양광 발전을 통합했습니다. 이와 같이 지역분산화가 진행됨으로써 세계의 전력 시장은 특정 지역의 정책과 자원의 충격으로부터 보호됩니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 데이터센터의 전력 수요 급증

- 산업용 열 및 수송의 전기화

- 정부에 의한 청정에너지 보조금 정책의 흐름(IRA, REPowerEU 등)

- 유틸리티 규모 축전지의 급속한 비용 저하

- 국경을 넘은 HVDC 슈퍼 그리드 구축

- 그린 수소 전해 장치의 증설이 베이스로드 수요를 높임

- 억제요인

- 송전망의 병목과 허가 승인의 지연

- 중요 광물의 공급망 변동성

- 포화 상태의 전력망에서 재생에너지의 억제 증가

- 기후 변화에 의한 수력발전의 변동성

- 공급망 분석

- 규제 상황

- 기술 전망(스마트 그리드, BESS, AI를 활용한 디스패치)

- 재생에너지 구성의 개요(2024년)

- 설치가 완료된 발전 용량 전망(GW)

- 발전 전망(TWh)

- 1차 에너지 소비량 동향(Mtoe)

- Porter's Five Forces

- 공급자의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 발전원별

- 화력(석탄, 천연가스, 석유, 디젤)

- 원자력

- 재생에너지(태양광, 풍력, 수력, 지열, 바이오매스 및 폐기물, 조력)

- 최종 사용자별

- 유틸리티

- 상업 및 산업용

- 주택용

- 수송 및 배전 전압 레벨별(정성적 분석)

- 고전압 송전(230kV 이상)

- 송전망(69-161kV)

- 중전압 배전(13.2-34.5 kV)

- 저전압 배전(1kV 이하)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 북유럽 국가

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 합작 사업, 자금 조달, 전력 구입 계약)

- 시장 점유율 분석(주요 기업의 시장 순위 및 점유율)

- 기업 프로파일

- State Grid Corporation of China

- Engie SA

- Enel SpA

- Tokyo Electric Power Co. Holdings

- NTPC Ltd

- Dominion Energy

- China Huaneng Group

- Duke Energy

- E.ON SE

- Siemens Energy

- Hitachi Energy

- Electricite de France(EDF)

- Iberdrola SA

- Korea Electric Power Corp.(KEPCO)

- NextEra Energy

- Southern Company

- Exelon Corporation

- China Three Gorges Corp.

- Orsted A/S

- RWE AG

- General Electric Vernova

- Mitsubishi Electric

제7장 시장 기회 및 미래 전망

CSM 26.02.04The Power Market was valued at 10.29 Thousand gigawatt in 2025 and estimated to grow from 11.17 Thousand gigawatt in 2026 to reach 16.83 Thousand gigawatt by 2031, at a CAGR of 8.55% during the forecast period (2026-2031).

Capacity growth stems from spiraling electricity demand created by data-center build-outs, industrial electrification, and early green-hydrogen uptake. Renewables account for nearly half of all new capacity and benefit from steep battery-storage cost declines that unlock multi-hour grid flexibility. Sovereign wealth and pension funds continue to channel USD 180 billion each year into high-voltage grid upgrades, tightening competition in the transmission segment. At the same time, grid bottlenecks and slow permitting threaten to stall 23% of approved clean-energy projects, exposing a mismatch between generation ambitions and infrastructure readiness.

Global Power Market Trends and Insights

Explosive Data-Center Electricity Demand Surge

Data centers consumed 460 TWh in 2024, equaling Argentina's entire annual load and representing 2% of world electricity. Average hyperscale campuses now draw 100-200 MW of continuous power, forcing utilities to renegotiate interconnection rules and fast-track substation upgrades. Corporate buyers contracted 23.7 GW of clean energy in 2024 as tech giants sidestepped traditional utility supply models to secure 24/7 renewables. Virginia's "data-center alley" already absorbs 25% of statewide generation, prompting regulators to revise capacity-market participation rules [PJM.com]. These concentrated loads heighten voltage-stability risk and drive premium capacity-contract pricing that flows through to retail tariffs. The global power market is therefore recalibrating around localized baseload spikes that were uncommon a decade ago.

Electrification of Industrial Heat & Transport

Electric arc furnaces captured 73% of new steel capacity in 2024, and heat pumps displaced natural gas in 40% of European industrial heating retrofits. On the mobility side, 14.1 million EVs added 85 TWh of net demand yet supplied 280 GWh of vehicle-to-grid storage that helped shave evening peaks. Nordic grids illustrate the convergence: synchronized EV charging and industrial heat-pump cycles create time-bundled consumption spikes that are balanced through granular tariff signals and AI-based dispatch. Aluminum smelters and chemical complexes are already relocating to wind-rich zones to capture cheap, firmed renewable power, locking in 15-20-year offtakes that underpin local transmission expansion. As similar patterns echo worldwide, the global power market anticipates sustained 15-20% rises in industrial consumption that call for USD 45 billion of annual distribution hardening.

Grid Bottlenecks & Permitting Delays

Transmission constraints sidelined 127 GW of shovel-ready renewables in 2024, translating into a USD 340 billion investment backlog. U.S. interconnection queues ballooned to 2,600 GW, five times the present grid capacity, with average study cycles extending 5.2 years. European cross-border lines ran at 95% utilization during windy hours, forcing 47 TWh of curtailment, particularly in Spain and Germany. Policymakers reacted by capping review periods to 12 months for pre-zoned projects under the EU Net-Zero Industry Act, yet community opposition still delays one in four HVDC builds. If unaddressed, these chokepoints could undercut the global power market's decarbonization pathway by deferring capital and eroding investor confidence.

Other drivers and restraints analyzed in the detailed report include:

- Government Clean-Energy Subsidy Waves

- Rapid Cost Decline in Utility-Scale Battery Storage

- Critical-Mineral Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Renewables commanded 47.95% of 2025 installed capacity and are scaling at 13.70% CAGR through 2031, underpinned by a record 346 GW of new solar and 116 GW of wind commissioned during the year. Solar photovoltaics, cheaper than marginal gas in most regions, dominate daytime supply and compress peak-price spreads. Wind plays the complementary role during evening hours, though integration challenges rise as variable output surpasses 30% of national mixes in 15 countries. Offshore wind, growing at a 23.10% CAGR, captures deep-water sites through floating foundations, accelerating uptake in Japan, South Korea, and California. Simultaneously, nuclear restarts and small modular reactor pilots add a nascent but strategic avenue for firm, low-carbon generation that can anchor industrial heat contracts. Coal and oil plants continue to retire or retrofit; 47 GW of coal capacity announced hydrogen co-firing conversions in 2024, though commercial viability remains tied to carbon prices above USD 80 per ton.

High renewable penetration tilts planning toward flexibility assets. Grid operators worldwide will require USD 2.8 trillion in cumulative investment for batteries, pumped-hydro, demand response, and expanded interconnectors over 2026-2031. Battery storage integration softens solar midday oversupply, while cross-border HVDC links move surplus wind to load centers. As these levers scale, the global power market embeds resilience through diversified resource stacks rather than single-fuel dominance. The renewables boom, therefore, redefines capital allocation, regulatory frameworks, and merchant-price formation across global electricity systems.

The Power Market Report is Segmented by Power Source (Thermal, Nuclear, and Renewables) and End-User (Utilities, Commercial and Industrial, and Residential), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Geography Analysis

Asia-Pacific led the global power market with 44.20% capacity share in 2025, anchored by China's 1,411 GW fleet and India's 425 GW. China commissioned 216 GW of new renewables during the year, more than Germany's installed base, yet also added 47 GW of coal to safeguard grid inertia. India, by contrast, balances solar ambition with regional battery tenders that target 50 GWh of storage by 2026. Japan and South Korea lean on offshore wind and advanced nuclear to curb imported-fuel dependence; Japan intends to reach 45 GW of offshore turbines by 2040, while South Korea experiments with 12 GW of floating solar. The region's integration strain remains high, with renewable curtailment surpassing 8.2% in northwest China due to limited transmission, underscoring the urgency of interprovincial HVDC lines.

South America emerged as the fastest-expanding slice of the global power market at 15.10% CAGR, propelled by green-hydrogen hubs in Chile and lithium-driven grid storage demand in Argentina and Brazil. Brazil boasts 195 GW of installed capacity, leveraging low-cost wind and hydro to decarbonize mining and agriculture. Chile's Atacama solar boom supplies both mining loads and hydrogen export terminals, achieving sub-USD 30/MWh levelized costs. Beyond renewables, Argentina's Vaca Muerta shale gas underpins firm capacity additions that stabilize an increasingly variable generation fleet. Cross-border interconnectors, including the Andes-Pacific HVDC, unlock regional trade that optimizes hydropower between wet and dry seasons.

Europe sustained 22.80% of global capacity in 2025, concentrating on flexibility and energy-security upgrades after the 2022 gas crisis. Germany installed 17 GW of renewables while leaning on Nordic hydro and French nuclear imports to balance frequency. The United Kingdom added 3.2 GW of offshore wind, cementing its leadership in floating foundations. Yet mature grids confront rising saturation; negative-price hours proliferate, storage economics improve, and wholesale markets scramble to reconfigure settlement periods to five minutes. North America and the Middle East & Africa lag in share but represent promising growth. The United States installed 32 GW of renewables in 2024, buoyed by IRA tax credits, and the UAE put 5.6 GW of solar into its 2071 net-zero roadmap. Regional diversification, therefore, buffers the global power market against policy or resource shocks in any single geography.

- State Grid Corporation of China

- Engie SA

- Enel SpA

- Tokyo Electric Power Co. Holdings

- NTPC Ltd

- Dominion Energy

- China Huaneng Group

- Duke Energy

- E.ON SE

- Siemens Energy

- Hitachi Energy

- Electricite de France (EDF)

- Iberdrola SA

- Korea Electric Power Corp. (KEPCO)

- NextEra Energy

- Southern Company

- Exelon Corporation

- China Three Gorges Corp.

- Orsted A/S

- RWE AG

- General Electric Vernova

- Mitsubishi Electric

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive data-center electricity demand surge

- 4.2.2 Electrification of industrial heat & transport

- 4.2.3 Government clean-energy subsidy waves (IRA, REPowerEU, etc.)

- 4.2.4 Rapid cost decline in utility-scale battery storage

- 4.2.5 Cross-border HVDC super-grid build-outs

- 4.2.6 Green-hydrogen electrolyzer build-outs raising baseload demand

- 4.3 Market Restraints

- 4.3.1 Grid bottlenecks & permitting delays

- 4.3.2 Critical-mineral supply-chain volatility

- 4.3.3 Rising renewable curtailment in saturated grids

- 4.3.4 Climate-induced hydropower variability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Smart Grids, BESS, AI-enabled Dispatch)

- 4.7 Renewable Energy Mix Snapshot (2024)

- 4.8 Installed Power-Generation Capacity Outlook (GW)

- 4.9 Electricity Generation Outlook (TWh)

- 4.10 Primary Energy Consumption Trend (Mtoe)

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Power-Generation Source

- 5.1.1 Thermal (Coal, Natural Gas, Oil and Diesel)

- 5.1.2 Nuclear

- 5.1.3 Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

- 5.3 By T&D Voltage Level (Qualitative Analysis only)

- 5.3.1 High-Voltage Transmission (Above 230 kV)

- 5.3.2 Sub-Transmission (69 to 161 kV)

- 5.3.3 Medium-Voltage Distribution (13.2 to 34.5 kV)

- 5.3.4 Low-Voltage Distribution (Up to 1 kV)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Malaysia

- 5.4.3.6 Thailand

- 5.4.3.7 Indonesia

- 5.4.3.8 Vietnam

- 5.4.3.9 Australia

- 5.4.3.10 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 State Grid Corporation of China

- 6.4.2 Engie SA

- 6.4.3 Enel SpA

- 6.4.4 Tokyo Electric Power Co. Holdings

- 6.4.5 NTPC Ltd

- 6.4.6 Dominion Energy

- 6.4.7 China Huaneng Group

- 6.4.8 Duke Energy

- 6.4.9 E.ON SE

- 6.4.10 Siemens Energy

- 6.4.11 Hitachi Energy

- 6.4.12 Electricite de France (EDF)

- 6.4.13 Iberdrola SA

- 6.4.14 Korea Electric Power Corp. (KEPCO)

- 6.4.15 NextEra Energy

- 6.4.16 Southern Company

- 6.4.17 Exelon Corporation

- 6.4.18 China Three Gorges Corp.

- 6.4.19 Orsted A/S

- 6.4.20 RWE AG

- 6.4.21 General Electric Vernova

- 6.4.22 Mitsubishi Electric

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment