|

시장보고서

상품코드

1690165

타이어 리트레드 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Tire Retreading - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

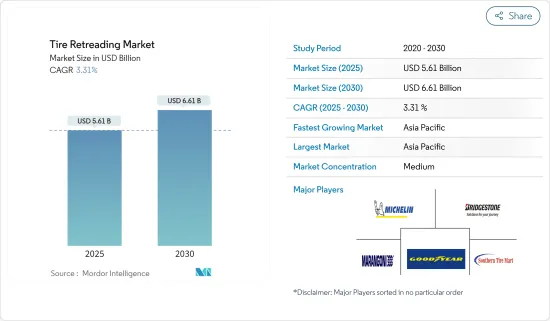

타이어 리트레드 시장 규모는 2025년에 56억 1,000만 달러에 이를 것으로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 3.31%를 나타내고, 2030년에는 66억 1,000만 달러에 달할 것으로 예상됩니다.

2020년 세계 자동차 산업은 COVID-19 팬데믹에 대응하여 시행된 운영 중단으로 인해 큰 문제에 직면했습니다. 이러한 운영 중단으로 인해 상반기에는 타이어 재 트레드를 포함한 제조 활동이 몇 주 동안 중단되어 시장 성장이 방해되었습니다. 그러나 2023년까지 자동차 부문은 힘차게 회복되었고 타이어 리트레드 시장의 향후 몇 년간의 유망한 궤도를 시사했습니다.

중기 예측에 따르면, 타이어 리트레드 시장은 특히 스포츠용 다목적 차량의 새로운 타이어 가격 상승으로 강화됩니다. 이 타이어 가격의 상승은 천연 고무 비용의 상승과 원유 가격의 변동에 의한 점이 큽니다. 게다가 상용차의 세계 보유 대수 증가도 시장 확대에 박차를 가할 것으로 보입니다.

타이어 리트레드 수요가 급증하고 있음을 인정하고, 타이어 제조업체는 이 기술에 깊은 노력을 기울이고 있습니다.

주요 하이라이트

- 2023년 7월, 브리지스톤은 타이어의 재질 재활용을 강화하는 야심찬 계획을 발표했습니다. 이 회사는 "쉽게 재사용 할 수 있는 고무"의 제조에 중점을 두고 폐 타이어를 새로운 타이어로 다시 생산하는 것을 목표로 합니다. 브리지스톤은 재생 가능 자원을 지지해, 마모한 타이어에 새로운 트레드를 장착하는 리트레드나, 폐 타이어를 원료로 재이용하는 케미컬 리사이클 등의 기술을 추진하고 있습니다.

리트레드 타이어는 환경 친화적이며 새로운 타이어보다 비용을 절감할 수 있기 때문에 타이어 리트레드 시장을 견인할 것입니다. 리트레드 타이어는 기존 타이어를 재사용함으로써 매립지를 절약할 뿐만 아니라 이산화탄소 배출을 억제하고 새로운 타이어 생산에 필수적인 자원인 수백만 갤런의 석유를 절약할 수 있습니다.

타이어 리트레드 시장 동향

상용차가 타이어 리트레드 시장에서 가장 큰 부문

타이어 사용률과 마모율이 높기 때문에 상용차 부문은 타이어 리트레드 시장을 선도하고 있습니다. 이 부문에 속하는 트럭, 버스 및 대형 운송 차량은 매일 주행 거리가 길기 때문에 타이어의 열화가 빠릅니다. 함대 운영자의 경우, 리트레드 타이어는 비용 효율적인 대안으로 새 타이어를 구입하는 것에 비해 운전 비용을 크게 줄일 수 있습니다. 타이어 비용이 상용 함대 유지비의 대부분을 차지한다는 점을 감안할 때, 리트레드는 경제적으로 유리한 선택이며, 타이어 수명을 연장하고 안정된 성능을 보장할 수 있습니다.

게다가, 타이어 리트레드의 환경적 측면에서의 이점은 상용차 부문에서의 매력에 매우 중요한 역할을 합니다. 리트레드 타이어는 신품 타이어를 제조하는 것보다 원료와 에너지 소비가 훨씬 적고 탄소 발자국을 줄일 수 있습니다. 함대 운영자는 이러한 환경적 이점을 점점 더 인식하고 있으며 지속 가능한 관행을 채택하기 위해 열심히 기업의 사회적 책임의 이미지를 강화하고 있습니다. 또한 많은 지역의 규제 당국이 환경 친화적인 관행을 추진하고 있기 때문에 리트레드 시장은 상용차에 대한 최적의 선택으로 지지를 모으고 있습니다.

기술의 진보와 리트레드 공정의 신뢰성이 상용차 섹터에서 리트레드 타이어의 채용을 더욱 견고하게 하고 있습니다. 사전 경화 및 금형 경화 프로세스와 같은 최신 기술은 리트레드 타이어가 신품 타이어의 성능과 안전성에 필적할 수 있도록 보장합니다. 이 새로운 신뢰성은 차량의 안전과 성능을 선호하는 함대 운영자의 신뢰를 키우고 있습니다. 고품질의 리트레드 서비스가 널리 이용 가능하며, 리트레드 시설의 견고한 네트워크는 상용차 운영자가 리트레드 타이어를 보다 쉽게 입수할 수 있게 하여 타이어 리트레드 시장에서 이 부문의 리더십을 강화하고 있습니다.

게다가 시장 기업은 할인, 비용 효과적인 정책, 신제품 출시를 전개하고 있으며, 향후 수년간 시장 성장을 가속할 가능성이 높습니다.

콘티넨탈 타이어의 Conti Bharosa 프로그램은 제조 결함에 대한 보증 기간을 5년간 연장하고 있으며, 인도 타이어 제조업체가 제공하는 전통적인 2-3년 보증 기간을 초과합니다. 또한 Conti Bharosa는 표준 하중 적용에 사용되는 타이어에 대한 첫 번째 리트레드 후 제조 결함으로부터 보호하기 위해 타이어의 두 번째 수명에 대한 보증을 제공합니다.

게다가 타이어 리트레드는 중형차 사이에서 급성장하고 있으며, 마지막 마일 딜리버리 서비스와 물류 기업의 도입이 증가하고 있습니다. 예를 들어, UPS와 FedEx와 같은 선도적인 택배 회사는 이미 마일리지 마감에 리트레드 타이어를 활용하고 있습니다. 굿이어는 중형 트럭 운송 부문의 성장을 인정하고 있으며 전략적 비용 절감 수단으로 리트레드에 대한 투자를 강화하고 있습니다.

아시아태평양이 계속 최대 시장을 기록할 전망

중국은 세계 최대의 승용차 보유 대수를 자랑하는 세계 자동차 대국입니다. 이러한 이점은 중국이 승용차와 상용차 생산에 매우 중요한 역할을 한다는 것을 강조할 뿐만 아니라 타이어 리트레드 수요가 급증하고 있음을 보여줍니다. 2023년 중국의 승용차와 상용차의 생산량은 3,016만대로 연간 12%의 견조한 성장세를 보였습니다.

123만대의 상용차를 포함한 총 899만대의 자동차를 등록하는 일본도 타이어 리트레드 분야에서 중요한 선수입니다. 일본의 상용차량의 많음과 기술력의 높이가 프리미엄 리트레드 프로세스의 진보와 보급을 뒷받침하고 있습니다. 일본의 지속가능성에 대한 헌신은 원재료를 절약할 뿐만 아니라 폐기물을 줄이는 타이어 리트레딩의 친환경 이점과 원활하게 연동됩니다. 게다가 일본의 엄격한 규제는 리트레드 타이어가 우수한 안전성과 성능 기준을 유지할 수 있도록 하여 상업 사업자에게 신뢰할 수 있는 경제적인 선택이 되고 있습니다.

인도에서는 운송 및 물류 부문이 상용차에 크게 의존하고 있기 때문에 타이어 리트레드 서비스에 대한 수요가 왕성합니다. 인도의 비용에 민감한 시장을 고려하면, 리트레드 타이어는 전략적 이점으로 부상하고, 함대 운영자는 운영 비용을 크게 줄일 수 있습니다. 또한 인도에서는 인프라 프로젝트가 급증하고 도로망이 확대됨에 따라 상용차 이용이 증가하고 타이어 리트레드 시장의 성장이 더욱 가속화되고 있습니다.

또한 자동차 타이어 시장은 수많은 원재료 공급업체와 정부의 지원 정책에 힘입어 번영하고 있습니다. 일본, 중국, 한국 등의 나라에서는 농업용 차량이 눈에 띄기 때문에 이 분야에서의 자동차용 타이어 수요는 계속 견조합니다.

이러한 모든 역학을 고려하면, 최근 새로운 타이어 리트레드 제조 시설의 완성과 함께, 타이어 리트레드 시장은 앞으로 몇 년 동안 유망한 궤도를 탈 것으로 예상됩니다.

타이어 리트레드 산업 개요

Bridgestone Corporation, Southern Tire Mart, TreadWright, Goodyear 등 주요 기업이 타이어 리트레드 시장을 독점하고 있습니다. 이러한 업계 리더들은 지속 가능한 솔루션과 혁신적인 기술을 추진하여 상용 플릿과 광범위한 운송 부문을 지원합니다.

- 2023년 12월, 브리지스톤은 CES 2024에 출전하여 지속가능성과 효율성에 대한 노력을 발표했습니다. 브리지 스톤 반다그의 리트레드 서비스는 ENLITEN 기술과 첨단 함대 관리 솔루션과 같은 혁신적인 기술과 함께 타이어의 수명을 지속적으로 연장한다는 것을 입증합니다.

- 2023년 11월, 미슐랭은 프랑스 리옹에서 열린 Solutrans 2023의 주역이 되어 친환경 타이어 라인업을 전시했습니다. 미슐랭 X 멀티 HD Z와 Agilis CrossClimate 등의 주목 제품은 구름 저항과 재활용 소재에 대한 전문 지식을 활용하여 환경 풋 프린트의 절감을 강조하고 있습니다. 또한 미슐랭은 "미슐랭 커넥티드 모빌리티"서비스군을 전개.

- 2023년 9월, 미슐랭은 거의 모든 트럭 및 버스 타이어 리트레드 가능성을 발표하고 고비를 맞이했습니다. 리틀레드 한 세기를 기념하여 미슐랭은 영국과 독일 공장에서 약 3,000만 그루의 타이어가 재생되었음을 자랑스럽게 말했습니다. 이러한 성취는 미쉐린의 실력을 강조할 뿐만 아니라 150만 톤의 원재료 절감과 약 350만 톤의 CO2 배출량 감소로 이어집니다. 이 이니셔티브의 특징인 미슐랭 리믹스 프로세스는 리뉴얼된 트레드가 새로운 타이어의 소재와 기술에 적합함을 보장하고 안전성, 트랙션, 그립에 대한 브랜드의 헌신을 지지합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 성장의 원동력이 되는 환경면에서의 장점

- 시장 성장 억제요인

- 고무 생산량 감소와 불안정한 원재료 비용

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 자동차 유형

- 승용차

- 소형 상용차

- 중형 및 대형 트럭

- 버스

- 생산 방법

- 사전 경화

- 금형 경화

- 타이어 유형

- 래디얼

- 바이어스

- 솔리드

- 판매 채널

- OEM

- 독립 리트레더

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 브라질

- 멕시코

- 아랍에미리트(UAE)

- 기타 국가

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Bridgestone Corporation

- Goodyear Tire and Rubber Company

- Marangoni SpA

- Michelin SCA

- Oliver Rubber Company

- Southern Tire Mart

- Parrish Tire Company

- Redburn Tire Company

- Southern Tire Mart

- TreadWright Tires

- Sumitomo Rubber Industries, Ltd.

- Rethread(Pty) Ltd

- Pirelli & CSpA

- MRF Limited

- Vipal Rubber Corporation

제7장 시장 기회와 앞으로의 동향

KTH 25.04.09The Tire Retreading Market size is estimated at USD 5.61 billion in 2025, and is expected to reach USD 6.61 billion by 2030, at a CAGR of 3.31% during the forecast period (2025-2030).

In 2020, the global automotive industry faced significant challenges due to lockdowns imposed in response to the COVID-19 pandemic. These lockdowns halted manufacturing activities, including tire retreading, for several weeks in the year's first half, stunting market growth. Yet, by 2023, the automotive sector rebounded robustly, signaling a promising trajectory for the tire retreading market in the coming years.

Medium-term projections suggest that the tire retreading market will be bolstered by rising prices of new tires, particularly for sports utility vehicles. This surge in tire prices is largely due to escalating natural rubber costs and volatile crude oil prices. Additionally, the growing global fleet of commercial vehicles is set to further fuel the market's expansion.

Recognizing the burgeoning demand for tire retreading, tire manufacturers are diving deep into this technology. For instance,

Key Highlights

- In July 2023, Bridgestone unveiled its ambitious plans to bolster tire material recycling. Their focus is on crafting "rubber that can be readily reused," aiming to transform waste tires into new ones. Bridgestone is championing renewable resources and is advancing technologies like retreading-where a new tread is applied to worn tires-and chemical recycling, which repurposes waste tires into raw materials.

The eco-friendly advantages and cost savings of retreaded tires over new ones are set to propel the tire retreading market. Retreading not only conserves landfill space by reusing existing tires but also curbs carbon dioxide emissions and conserves millions of gallons of oil-an essential resource in new tire production.

Tire Retreading Market Trends

Commercial Vehicles is the Largest Segment in the Tire Retreading Market

Due to the high utilization and wear rates of tires, the commercial vehicle segment leads the tire retreading market. Trucks, buses, and heavy-duty transporters in this segment cover extensive daily distances, resulting in rapid tire degradation. For fleet operators, retreading presents a cost-effective alternative, significantly curtailing operating costs compared to buying new tires. Given that tire expenses constitute a major portion of a commercial fleet's maintenance costs, retreading stands out as a financially savvy choice, extending tire life and ensuring consistent performance.

Additionally, the environmental advantages of tire retreading play a pivotal role in its appeal within the commercial vehicle sector. Retreading consumes far fewer raw materials and energy than producing new tires, leading to a reduced carbon footprint. Fleet operators, increasingly cognizant of these environmental benefits, are keen to adopt sustainable practices, bolstering their corporate social responsibility image. Furthermore, with many regions' regulatory bodies promoting eco-friendly practices, the retreading market has gained traction as the go-to option for commercial vehicles.

Technological advancements and the reliability of retreading processes have further cemented the adoption of retreaded tires in the commercial vehicle sector. Modern techniques, like pre-cure and mold-cure processes, ensure retreaded tires match the performance and safety of new ones. This newfound reliability has fostered trust among fleet operators, who prioritize vehicle safety and performance. The widespread availability of quality retreading services and a robust network of retreading facilities further facilitate access to retreaded tires for commercial vehicle operators, reinforcing the segment's leadership in the tire retreading market.

Additionally, market players are rolling out discounts, cost-effective policies, and new product launches, likely fueling market growth in the coming years. For instance,

Continental Tires' Conti Bharosa program extends warranty coverage against manufacturing defects for five years, surpassing the traditional two to three-year coverage offered by Indian tire manufacturers. Furthermore, Conti Bharosa provides warranty coverage for the second life of tires, safeguarding against manufacturing defects post-first retread for those used in standard load applications.

Moreover, tire retreading is witnessing rapid growth among medium-duty vehicles, with last-mile delivery services and logistics companies increasingly deploying them. For instance, major parcel-delivery giants like UPS and FedEx are already utilizing retreads for their last-mile operations. Goodyear has acknowledged the growth of the medium-duty trucking segment and is ramping up investments in retreads as a strategic cost-saving measure.

Asia-Pacific Continues to be the Largest Market

China stands tall as a global automotive giant, boasting the world's largest fleet of passenger cars. This dominance not only underscores China's pivotal role in the production of both passenger and commercial vehicles but also signals a burgeoning demand for tire retreading. In 2023, China's production of passenger and commercial vehicles hit a notable 30.16 million units, marking a robust annual growth of 12%.

Japan, registering a total of 8.99 million vehicles, including 1.23 million commercial ones, is another key player in the tire retreading arena. The nation's significant commercial vehicle volume, paired with its technological prowess, bolsters the advancement and uptake of premium retreading processes. Japan's commitment to sustainability dovetails seamlessly with the eco-friendly advantages of tire retreading, which not only conserves raw materials but also curtails waste. Moreover, Japan's rigorous regulations guarantee that retreaded tires uphold superior safety and performance standards, rendering them a trustworthy and economical choice for commercial operators.

In India, the transportation and logistics sectors' heavy reliance on commercial vehicles fuels a robust demand for tire retreading services. Given India's cost-sensitive market, retreading emerges as a strategic advantage, allowing fleet operators to significantly curtail operational costs. Moreover, as infrastructure projects burgeon and road networks expand in India, the uptick in commercial vehicle usage further amplifies the tire retreading market's growth.

Additionally, the automobile tire market thrives, buoyed by a myriad of raw material suppliers and supportive government policies. Given the prominence of agricultural vehicles in nations like Japan, China, and South Korea, the demand for automotive tires in this sector is poised to remain strong.

Considering all these dynamics, coupled with the recent inauguration of new tire retreading manufacturing facilities, the tire retreading market is set for a promising trajectory in the coming years.

Tire Retreading Industry Overview

Bridgestone Corporation, Southern Tire Mart, TreadWright, Goodyear, and other key players dominate the tire retreading market. These industry leaders are pushing forward with sustainable solutions and innovative technologies, catering to commercial fleets and the broader transport sector. For instance,

- In December 2023, Bridgestone, set to participate in CES 2024, unveiled its commitment to sustainability and efficiency. Among the highlights will be Bridgestone Bandag's retreading service, a testament to extending tire life sustainably, alongside innovations like ENLITEN Technology and advanced fleet management solutions.

- In November 2023, Michelin took center stage at Solutrans 2023 in Lyon, France, showcasing its eco-conscious tire lineup. Featured products, including the Michelin X Multi HD Z and Agilis CrossClimate, emphasize reduced environmental footprints, leveraging expertise in rolling resistance and recycled materials. Additionally, Michelin rolled out its "Michelin Connected Mobility" suite of services.

- In September 2023, Michelin marked a milestone, announcing the retreadability of nearly all its truck and bus tires. Celebrating a century of retreading, Michelin proudly noted the renewal of around 30 million tires at its UK and German plants. This achievement not only underscores Michelin's prowess but also translates to a savings of 1.5 million tons in raw materials and a reduction of nearly 3.5 million tons in CO2 emissions. The MICHELIN Remix process, a hallmark of this initiative, ensures that the renewed tread matches the materials and technologies of new tires, upholding the brand's commitment to safety, traction, and grip.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Environmental Benefits Driving Growth

- 4.2 Market Restraints

- 4.2.1 Decreasing Rubber Production And Volatile Raw Material Cost

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value (USD)

- 5.1 Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Light commercial vehicle

- 5.1.3 Medium and Heavy duty Truck

- 5.1.4 Bus

- 5.2 Production Method

- 5.2.1 Pre-cure

- 5.2.2 Mold Cure

- 5.3 Tire Type

- 5.3.1 Radial

- 5.3.2 Bias

- 5.3.3 Solid

- 5.4 Sales Channel

- 5.4.1 OEM

- 5.4.2 Independent Retreaders

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United State

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Bridgestone Corporation

- 6.2.2 Goodyear Tire and Rubber Company

- 6.2.3 Marangoni SpA

- 6.2.4 Michelin SCA

- 6.2.5 Oliver Rubber Company

- 6.2.6 Southern Tire Mart

- 6.2.7 Parrish Tire Company

- 6.2.8 Redburn Tire Company

- 6.2.9 Southern Tire Mart

- 6.2.10 TreadWright Tires

- 6.2.11 Sumitomo Rubber Industries, Ltd.

- 6.2.12 Rethread (Pty) Ltd

- 6.2.13 Pirelli & C. S.p.A.

- 6.2.14 MRF Limited

- 6.2.15 Vipal Rubber Corporation