|

시장보고서

상품코드

1690197

엔지니어드 우드 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Engineered Wood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

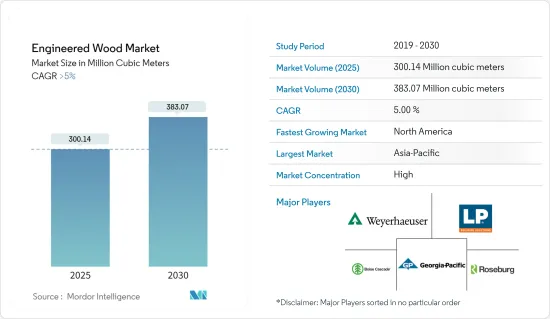

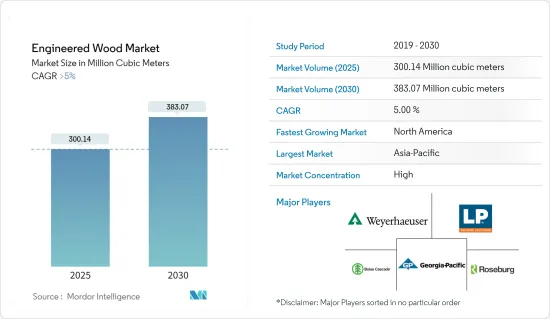

엔지니어드 우드 시장 규모는 2025년에는 3억 14만 입방미터, 2030년에는 3억 8,307만 입방미터에 이를 것으로 예측되며, 예측 기간 중(2025년-2030년) CAGR은 5%를 초과할 것으로 예측됩니다.

COVID-19의 대유행은 시장에 부정적인 영향을 주었습니다.

주요 하이라이트

- 중기적으로는 비주택 분야에서의 수요 증가와, 건축 재료로서의 CLT(CLT(Cross Laminated Timber))의 사용 증가가 예측 기간중 시장을 견인한다고 생각됩니다.

- 그 반면, 포름알데히드의 배출에 관한 엄격한 환경 문제가 시장 성장의 방해가 될 가능성이 높습니다.

- 인도와 중국에서의 주택 건설 증가는 예측 기간 중에 기회가 될 것으로 예상됩니다.

- 아시아태평양은 세계 시장을 독점할 가능성이 높고, 북미는 예측 기간 중에 엔지니어드 우드의 소비가 가장 빨라질 것으로 예상됩니다.

엔지니어드우드 시장 동향

시장을 독점하는 주택 부문

- 엔지니어드 우드는 가구, 벽, 바닥, 문, 지붕, 캐비닛, 기둥, 보, 계단 등 폭넓은 용도에 사용되고 있습니다.

- 집성재의 용도는 급속하게 확대하고 있습니다.저층 건축의 경우, CLT 벽 패널의 내하중성의 향상은 종래의 스터드 프레임의 벽보다 더욱 큰 메리트를 가져옵니다.

- 유럽이나 북미의 중층 주택 분야에서는 CLT는 벌써 확립된 시스템이 되고 있습니다. 또한, 높이 150미터를 넘는 초고층 빌딩의 건설에 CLT(Cross Laminated Timber)가 사용되는 예도 늘고 있습니다.

- 벽, 바닥, 지붕 등 다양한 주택용도로 OSB의 용도가 확대되고 있는 것이 시장을 견인할 것으로 추정됩니다.

- 모든 유형의 엔지니어드 우드가 주택 분야의 다양한 용도로 크게 사용되고 있습니다.

- 유럽의 가구 기업은 매우 성공적이며 혁신적입니다.

- 미국 인구조사국이 발표한 데이터에 의하면, 2023년의 미국에 있어서의 민간 건축의 연간 총액은 전년대비로 4.7% 증가했습니다.

- 2023년의 건설 총액은 1조 9,787억 달러로, 2022년의 건설 총액을 7% 웃돌았습니다.

- 2023년 12월에는 2022년의 1조 8,409억 달러에 대해 2조 960억 달러가 지출되어 건설 지출은 13.9% 증가했습니다.

- 이와 같이, 전술한 측면으로부터, 주택 부문이 예측 기간 중에 시장을 견인할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양에는 중국, 인도, ASEAN, 일본 등의 주요 국가가 있습니다.

- 중국은 주택 및 상업건설 부문의 충분한 개발이 주된 원동력이 되고 있으며, 경제 성장에 지지되고 있습니다.

- 또, 2025년까지 7,000개 이상의 쇼핑 센터가 건설될 전망입니다.

- 인도에서는 2024년까지 합리적인 가격의 주택이 70% 정도 증가할 것으로 예상되고 있습니다.

- 또 2030년까지 인구의 30% 이상이 인도의 도시에 살게 될 것으로 예상되며 2,500만 호의 중급 주택과 저렴한 추가 수요가 증가해 예측 기간 중에 엔지니어드우드 제품 수요가 높아질 것으로 예상됩니다.

- 아시아태평양에서는 일본과 중국이 OSB 시장에서 상당한 점유율을 차지하고 있습니다.

- 따라서 아시아태평양이 세계 시장을 독점할 것으로 예상됩니다.

엔지니어드 우드 산업 개요

엔지니어드 우드 시장은 부분적으로 통합되어 있으며 대부분의 기업이 약간의 시장 점유율을 차지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 비주택분야에서의 수요 증가

- 건설자재로서의 집성재(CLT)의 사용 증가

- 기타 기회

- 억제요인

- 포름알데히드 배출에 관한 엄격한 환경 문제

- 기타 억제요인

- 산업 밸류체인 분석

- 포터 Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 유형

- 합판

- 배향성 스트랜드 보드(OSB)

- 구루람

- CLT(Cross Laminated Timber)(CLT)

- 라미네이트·베니어·램버(LVL)

- 파티클 보드

- 기타(파이버 보드, 병렬 가닥, 기타)

- 용도

- 비주택용

- 주택용

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 튀르키예

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**, 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Binderholz GmbH

- Boise Cascade

- Georgia-Pacific(Georgia-Pacific Wood Products LLC)

- HASSLACHER Holding GmbH

- Havwoods India Pvt. Ltd

- Huber Engineered Woods LLC

- KLH Massivholz Wiesenau GmbH

- Kronoplus Limited

- Louisiana-Pacific Corporation

- Mayr-Melnhof Holz Holding AG

- Nordic Structures

- Pacific Woodtech Corporation

- Resolute Forest Products

- Roseburg

- Stora Enso

- West Fraser

- Weyerhaeuser Company

제7장 시장 기회와 앞으로의 동향

- 인도와 중국의 주택 건설 성장

- 기타 기회

The Engineered Wood Market size is estimated at 300.14 million cubic meters in 2025, and is expected to reach 383.07 million cubic meters by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic had a negative impact on the market. However, the market for engineered wood has now been close to reaching pre-pandemic levels because of increasing construction and restoration activities in the post-pandemic period.

Key Highlights

- Over the medium term, growing demand from the non-residential sector and increasing use of cross-laminated timber (CLT) as a construction material are likely to drive the market during the forecast period.

- On the flip side, stringent environmental concerns related to formaldehyde emissions are likely to hinder market growth.

- The growing residential construction in India and China is expected to act as an opportunity in the forecast period.

- Asia-Pacific is likely to dominate the global market, while North America is expected to witness the fastest consumption of engineered wood during the forecast period.

Engineered Wood Market Trends

The Residential Segment to Dominate the Market

- Engineered wood is used for a wide range of applications, including furniture, walls, flooring, doors, roofs, cabinets, columns, beams, and staircases.

- The application of cross-laminated wood has been increasing rapidly. For low-rise construction, the increased loadbearing capacity of CLT wall panels adds further benefits over conventional stud-framed walls.

- Cross-laminated timber is now an established system in the mid-rise residential sector in Europe and North America. In addition, there are increasing examples of cross-laminated timber being used to construct skyscrapers for buildings over 150 meters tall.

- The growing application of OSB in various residential applications, such as walls, flooring, and roofs, is estimated to drive the market.

- All types of engineered woods are significantly used in various applications in the residential sector. With 73% of its population living in urban areas, Europe is expected to be over 80% urban by 2050.

- European furniture companies are very successful and innovative. The German, Italian, and Nordic furniture companies act as benchmarks in the field of high-class design.

- According to the data released by the United States Census Bureau, the total annual value of private construction in the country increased by 4.7% in 2023 compared to the previous year.

- The total value of construction in 2023 was USD 1,978.7 billion, which was 7% above the total value of construction in 2022.

- In December 2023, a total of USD 2,096 billion was spent compared to USD 1,840.9 billion in 2022, registering a 13.9% rise in construction spending.

- Thus, based on the aforementioned aspects, the residential segment is expected to drive the market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific has several major countries, such as China, India, ASEAN, and Japan.

- China has been majorly driven by ample developments in the residential and commercial construction sectors and is supported by a growing economy. In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030.

- China is also likely to witness the construction of 7,000 more shopping centers, which are estimated to start functioning by 2025.

- In India, the availability of affordable housing is expected to rise by around 70% by 2024. By 2025, India's construction industry is expected to reach USD 1.4 trillion, as per Invest India.

- Also, by 2030, more than 30% of the population is expected to live in urban India, creating a demand for 25 million additional mid-end and affordable units, thus bolstering the demand for engineered wood products during the forecast period.

- In Asia-Pacific, Japan and China have a considerable share of the OSB market. Norbond has been marketing its OSB panels in Japan for over 20 years, and it has established a track record of high performance in a variety of end-user construction.

- Hence, Asia-Pacific is expected to dominate the global market.

Engineered Wood Industry Overview

The engineered wood market is partially consolidated, with most players accounting for a marginal market share. Major companies in the market (in no particular order) include Weyerhaeuser Company, Boise Cascade, Georgia-Pacific, Roseburg Forest Products, and Louisiana-Pacific Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Non-residential Sector

- 4.1.2 Increasing Use of Cross-laminated Timber (CLT) as Construction Materials

- 4.1.3 Other Opportunities

- 4.2 Restraints

- 4.2.1 Stringent Environmental Concerns Related to Formaldehyde Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Plywood

- 5.1.2 Oriented Strand Board (OSB)

- 5.1.3 Glulam

- 5.1.4 Cross-laminated Timber (CLT)

- 5.1.5 Laminated Veneer Lumber (LVL)

- 5.1.6 Particleboard

- 5.1.7 Other Types (Fiber Board, Parallel Strand, Others)

- 5.2 Application

- 5.2.1 Non-residential

- 5.2.2 Residential

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Binderholz GmbH

- 6.4.2 Boise Cascade

- 6.4.3 Georgia-Pacific (Georgia-Pacific Wood Products LLC)

- 6.4.4 HASSLACHER Holding GmbH

- 6.4.5 Havwoods India Pvt. Ltd

- 6.4.6 Huber Engineered Woods LLC

- 6.4.7 KLH Massivholz Wiesenau GmbH

- 6.4.8 Kronoplus Limited

- 6.4.9 Louisiana-Pacific Corporation

- 6.4.10 Mayr-Melnhof Holz Holding AG

- 6.4.11 Nordic Structures

- 6.4.12 Pacific Woodtech Corporation

- 6.4.13 Resolute Forest Products

- 6.4.14 Roseburg

- 6.4.15 Stora Enso

- 6.4.16 West Fraser

- 6.4.17 Weyerhaeuser Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Residential Construction in India and China

- 7.2 Other Opportunities