|

시장보고서

상품코드

1690744

미국의 관리 서비스 산업 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)United States (US) Managed Services Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

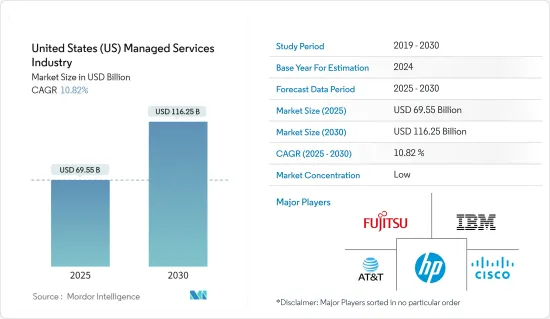

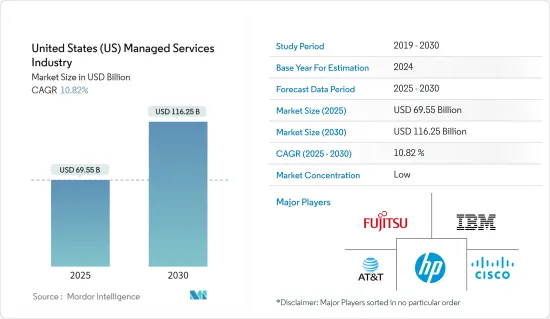

미국의 관리 서비스 산업은 2025년 695억 5,000만 달러에서 2030년에는 1,162억 5,000만 달러로 성장할 것으로 예측되고, 예측 기간(2025-2030년)의 CAGR은 10.82%를 나타낼 것으로 전망됩니다.

주요 하이라이트

- 관리 서비스는 특정 IT 기능이나 프로세스를 타사 제공업체에 아웃소싱하여 운영을 간소화하고 비용을 절감하는 것을 목표로 합니다. 이 접근 방식은 서비스 품질, 운영 효율성 및 고객 만족도를 향상시키는 동시에 비용을 절감합니다.

- 시장 조사에 따르면 사물 인터넷(IoT) 디바이스의 수가 급증함에 따라 관리 IoT 서비스에 대한 수요가 증가하면서 이러한 연결된 디바이스를 보호, 모니터링 및 최적화해야 할 필요성이 강조되고 있는 것으로 나타났습니다.

- 하이브리드 IT는 온프레미스 인프라와 클라우드 기반 솔루션을 결합한 것입니다. 사물 인터넷(IoT)의 부상으로 인해 기업들은 고객 참여 전략을 재고해야 했습니다.

- 미국의 관리 서비스 시장 전망에서 다양한 기술의 통합과 업계 규정 준수는 종종 과제로 제기됩니다.

- 코로나19 팬데믹 초기에는 기업들이 생존에 집중하고 비필수적인 투자를 연기하면서 일시적인 수요 감소가 발생했고, 이후 봉쇄 조치가 이어졌습니다. 이로 인해 관리 서비스 계약 이행이 지연되었습니다. 하지만 원격 근무가 급증하면서 보안, 클라우드 마이그레이션, 협업 도구, 네트워킹에 대한 필요성이 부각되어 관리 서비스 제공업체(MSP)의 업계 성장 기회가 생겼습니다.

미국의 관리 서비스 산업 동향

상당한 시장 성장을 목격하는 클라우드 부문

- 클라우드 기반 관리 서비스는 유연성과 확장성을 제공하여 서비스 제공업체가 클라우드 환경 내에서 원격으로 액세스하고 모니터링하며 문제를 해결할 수 있도록 지원합니다. 또한 시장 데이터에 따르면 AI/ML, 빅 데이터 분석, 위협 인텔리전스, 고급 자동화 플랫폼과 같은 기술의 도입이 클라우드 기반 서비스로의 전환을 촉진하고 있는 것으로 나타났습니다.

- 예를 들어, 2023년 11월 글로벌 사이버 보안 제공업체인 SonicWall은 수백 개의 관리 서비스 제공업체(MSP)를 지원하는 관리 보안 서비스 제공업체(MSSP)인 SGI(Solutions Granted Inc.)를 인수했습니다. 이번 인수를 통해 SonicWall은 파트너에 대한 약속을 더욱 강화할 수 있게 되었습니다.

- IT 및 통신 부문은 클라우드 관리 서비스 산업에서 상당한 시장 점유율을 차지하고 있습니다.

- 이러한 서비스는 클라우드 인프라의 원격 관리 및 유지보수를 용이하게 하여 기업이 외부 전문 지식을 활용하면서 핵심 목표에 집중할 수 있도록 지원함으로써 업계 성장을 촉진합니다.

IT 및 통신이 가장 큰 최종 사용자 산업

- 미국의 통신 업계는 관리 보안 서비스에 대한 수요가 매우 높으며, 주요한 업계 트렌드 중 하나로 꼽힙니다. 이는 주로 통신 회사가 고객 정보 및 네트워크 인프라 세부 정보를 포함한 방대한 양의 민감한 데이터를 처리하기 때문에 사이버 공격의 주요 표적이 되기 때문입니다. 또한 통신 네트워크의 복잡성과 진화하는 사이버 위협의 특성으로 인해 효과적인 보호를 위한 전문 지식이 필요합니다.

- 5G 네트워크의 등장으로 최종 사용자의 보안과 양질의 경험을 보장하는 데 초점이 맞춰지고 있으며, 이는 통신 관리 서비스의 업계 개요에서 강조된 변화입니다. 2023년 4월 현재 미국 503개 도시에서 5G 네트워크 접속이 가능해졌으며, 이는 전 세계 어느 국가보다 많은 수치로, 기존의 기술 중심 접근 방식에서 벗어나 네트워크 관리 및 최적화에 상당한 변화를 요구하고 있습니다. 이에 따라 이러한 전환을 지원하기 위한 통신사 관리 서비스에 대한 수요가 증가하여 시장 성장에 기여하고 있습니다.

- 2023년 7월, 관리 IT, 사이버 보안 및 클라우드 솔루션을 제공하는 선도적인 기업인 Dataprise는 텍사스에 기반을 둔 보안 관리 서비스 제공업체인 RevelSec을 인수했습니다.

- 시장 보고서에 따르면 관리 인프라는 고급 네트워크 인프라를 필요로 하는 IoT, AI, 엣지 컴퓨팅과 같은 혁신에 힘입어 상당한 시장 점유율을 차지하고 있습니다.

미국의 관리 서비스 산업 개요

미국의 관리 서비스 시장 개요는 부문화되어 있으며, Fujitsu, Cisco Systems Inc., IBM Corporation, AT&T Inc., HP Inc.와 같은 시장에서 강력한 고객 기반을 가진 최대 기업에 의해 지배되고 있습니다.

- 2024년 2월 : Ubiquity는 라스트 마일 디지털 인프라 복원력을 강화하기 위해 Fujitsu와 파트너십을 체결했습니다. Ubiquity는 Fujitsu 네트워크 운영 센터를 활용하여 미국 주요 4개 시장에서 라스트 마일 광대역 인프라를 지원할 예정입니다.

- 2024년 1월 : Cisco는 데이터 스토리지, 인프라, 하이브리드 클라우드 관리를 전문으로 하는 Hitachi Ltd의 자회사인 Hitachi Vantara와 협력하여 차세대 하이브리드 클라우드 관리 서비스를 발표했습니다. 이 서비스는 현대 기업이 직면하고 있는 지속적인 데이터 관리 문제를 해결하기 위해 특별히 맞춤화되었습니다. Hitachi EverFlex와 Cisco Powered Hybrid Cloud의 합작 솔루션은 자동화 솔루션과 예측 분석을 결합한 것입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 산업 밸류체인 분석

- COVID-19의 산업에 대한 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 하이브리드 IT로의 전환 증가

- 비용 및 운영 효율성 향상

- 시장의 과제

- 통합, 규제 문제 및 신뢰성 문제

제6장 시장 세분화

- 전개별

- 온프레미스

- 클라우드

- 유형별

- 관리 데이터센터

- 관리 보안

- 관리 커뮤니케이션

- 관리 네트워크

- 관리 인프라

- 관리 모빌리티

- 기업 규모별

- 중소기업

- 대기업

- 산업별

- BFSI

- IT 및 통신

- 의료

- 엔터테인먼트 미디어

- 소매

- 제조

- 정부

- 기타

제7장 경쟁 구도

- 기업 프로파일

- Fujitsu Limited

- Cisco Systems Inc.

- IBM Corporation

- AT& T Inc.

- HP Inc.

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Rackspace Technology Inc.

- Tata Consultancy Services Limited

- Citrix Systems Inc.

- Wipro Limited

제8장 투자 분석

제9장 시장의 미래

HBR 25.05.09The United States Managed Services Industry is expected to grow from USD 69.55 billion in 2025 to USD 116.25 billion by 2030, at a CAGR of 10.82% during the forecast period (2025-2030).

Key Highlights

- Managed services comprise outsourcing specific IT functions or processes to third-party providers, aiming to streamline operations and reduce costs. This approach enhances service quality, operational efficiency, and customer satisfaction while lowering expenses.

- Market research indicates that the soaring number of Internet of Things (IoT) devices has heightened the demand for managed IoT services, emphasizing the need to secure, monitor, and optimize these connected devices. In response, IT infrastructure providers are collaborating on IoT solutions.

- Hybrid IT combines on-premise infrastructure with cloud-based solutions. The rise of the Internet of Things (IoT) has prompted organizations to rethink their customer engagement strategies. Managed service providers (MSPs) play a crucial role in bolstering security within the IoT ecosystem, ensuring robust protection.

- Relatively speaking, managed services are known to be cost-effective and efficient, as compared to in-house services in the US, as they enable organizations to focus on their core competencies while outsourcing the non-core areas.In the US managed services market outlook, the integration of diverse technologies and adherence to industry regulations often pose challenges. Companies must navigate a web of standards and legal requirements, impacting the implementation and operation of managed services.

- The initial days of the COVID-19 pandemic and subsequent lockdowns caused a temporary dip in demand as businesses focused on survival and delayed non-essential investments. This led to a delay in implementing managed services contracts. However, the surge in remote work highlighted the need for security, cloud migration, collaboration tools, and networking, creating opportunities for industry growth among Managed Service Providers (MSPs).

United States (US) Managed Services Industry Trends

Cloud to Witness Significant Market Growth

- Cloud-based managed services offer flexibility and scalability, empowering service providers to remotely access, monitor, and resolve issues within the cloud environment. Furthermore, market data shows that the adoption of technologies like AI/ML, big data analytics, threat intelligence, and advanced automation platforms is propelling this transition to cloud-based services. Market players are launching innovative and collaborative services in response to industry trends.

- For example, in November 2023, SonicWall, a global cybersecurity provider, acquired Solutions Granted Inc. (SGI), a Managed Security Service Provider (MSSP) catering to hundreds of Managed Service Providers (MSPs). This acquisition bolsters SonicWall's commitment to its partners. It expands its portfolio to include US-based Security Operations Center services (SOCaaS), Managed Detection and Response (MDR), and other tailored managed services for MSPs and MSSPs.

- The IT and Telecom sector holds a significant market share in the cloud-managed services industry. For the 2023 fiscal year, the US federal government allocated around USD 24.4 billion for major federal IT investments, where cloud-managed services are gaining traction in the United States due to their ability to streamline IT operations, bolster security, and offer scalable solutions, thereby reflecting a steady market growth rate.

- These services facilitate remote management and maintenance of cloud infrastructure, which enables businesses to focus on their core objectives while leveraging external expertise, thereby fostering industry growth. The demand for managed services is set to rise as cloud adoption continues to surge, fostering innovation and efficiency in the digital realm.

IT and Telecom to be the Largest End-user Vertical

- The telecom industry in the United States has a strong demand for managed security services and is identified as one of the major significant industry trends. This is primarily due to the telecom companies' handling of vast volumes of sensitive data, including customer information and network infrastructure details, making them prime targets for cyberattacks. Additionally, the complexity of telecom networks and the evolving nature of cyber threats necessitate specialized expertise for effective protection.

- With the advent of 5G networks, the focus has shifted to ensuring end users' security and quality experiences, a shift highlighted in the industry overview of telecom-managed services. According to VIAVISION, as of April 2023, 5G network access was available in 503 United States cities, the most of any country globally, and this requires a significant shift in managing and optimizing networks, moving away from the traditional technology-centric approach. As a result, there is a rising demand for telecom-managed services to aid in this transition, contributing to market growth.

- In July 2023, Dataprise, a leading provider of managed IT, cybersecurity, and cloud solutions, acquired RevelSec, a Texas-based security managed service provider. This acquisition expands Dataprise's national presence and enhances its vertical expertise while providing RevelSec clients access to a broader range of services from Dataprise.

- According to the market report, managed infrastructure holds a significant market share, driven by innovations like IoT, AI, and edge computing, which necessitate advanced network infrastructure. Managed services play an important role in facilitating the adoption of these technologies.

United States (US) Managed Services Industry Overview

The United States managed services market overview is fragmented and is dominated by largest companies, such as Fujitsu Limited, Cisco Systems Inc., IBM Corporation, AT&T Inc., and HP Inc., among other companies that have a strong client base in the market. These players are constantly providing increased and enhanced offerings. Companies are employing powerful competitive strategies in order to survive in the market and retain their clients, thereby intensifying competitive rivalry in the market.

- February 2024 - Ubiquity partnered with Fujitsu to augment Last-Mile Digital Infrastructure Resilience. Ubiquity would utilize the Fujitsu Network Operations Center to support last-mile fiber broadband infrastructure in four major US markets. Fujitsu delivers Ubiquity with 24x7 managed network services from their carrier-class NOC in Texas.

- January 2024 - Cisco, in collaboration with Hitachi Vantara, the subsidiary of Hitachi Ltd specializing in data storage, infrastructure, and hybrid cloud management, unveiled Next-Gen hybrid cloud managed services. These services are specifically tailored to tackle the persistent data management hurdles faced by contemporary businesses. The joint solution, known as Hitachi EverFlex with Cisco Powered Hybrid Cloud, combines automation solutions and predictive analytics. It aims to equip organizations with a forward-looking toolkit for streamlined infrastructure management, cost optimization, and enhanced operational efficiency.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Challenges

- 5.2.1 Integration and Regulatory Issues and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small and Medium Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Limited

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Inc.

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Rackspace Technology Inc.

- 7.1.10 Tata Consultancy Services Limited

- 7.1.11 Citrix Systems Inc.

- 7.1.12 Wipro Limited