|

시장보고서

상품코드

1690868

북미의 농약 포장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Agricultural Chemical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

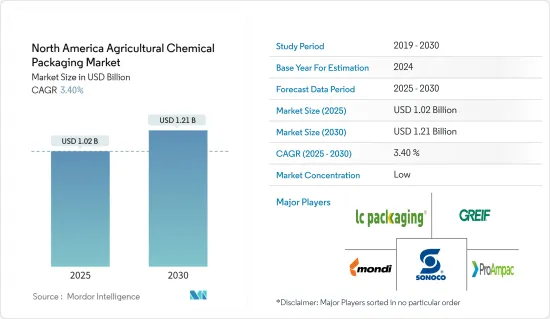

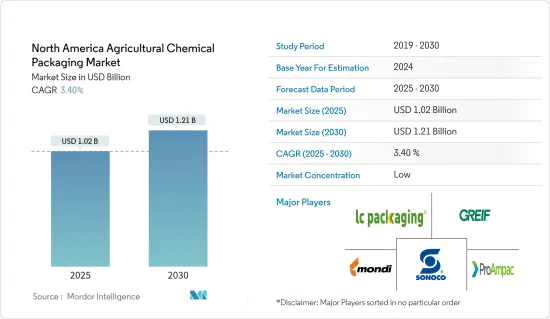

북미의 농약 포장 시장 규모는 2025년에 10억 2,000만 달러로 추정되고, 2030년에는 12억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 3.4%를 나타낼 전망입니다.

주요 하이라이트

- 비료와 살충제와 같은 농약은 독성이 있기 때문에 농약 포장은 농업 산업에서 매우 중요한 부분 중 하나입니다.

- 그 중에서도 플라스틱은 농약 제품에 가장 널리 사용되는 포장재입니다.

- 생분해성 포장 솔루션의 발전으로 이러한 포장 솔루션에 대한 수요가 증가함에 따라 시장의 다양한 공급업체가 재활용 수지를 중심으로 이러한 솔루션을 제품의 일부로 채택하는 데 주력하고 있습니다.

- 연방의 법과 규정에 따라 미국에서 제품을 판매하기 전에 제품의 라벨이나 표시가 준수해야 하는 많은 규정이 있습니다. 법적 도량형과 관련된 라벨링 요건은 공정 포장 및 라벨링법(FPLA) 및 통일 포장 및 라벨링 규정(UPLR)을 준수해야 합니다. 또한 미국으로 수입되는 모든 제품은 미국 연방규정 제19장 4절 1304조 및 19 CFR 134, 원산지 표시 규정을 준수해야 합니다.

- 포장 규정은 무게와 수량 규정을 준수해야 하므로 공급업체의 이윤을 제한하고 더 작은 포장으로 나누어야 합니다.

- 코로나19는 국제 무역과 필수 및 비필수 상품과 서비스의 글로벌 공급망에 영향을 미쳤습니다. 코로나19가 전 세계로 확산되면서 기업들은 큰 타격을 입었습니다. 팬데믹으로 인해 시장은 초기에 영향을 받았습니다. 이 지역의 많은 국가들이 일회용 플라스틱 사용 금지를 연기했습니다.

북미의 농약 포장 시장 동향

비료가 주요 시장 점유율을 차지

- 비료, 살충제, 제초제 및 기타 화학 물질과 같은 농약의 경우 북미 시장은 지난 몇 년 동안 수요가 꾸준히 유지되면서 상당한 성숙 단계에 도달했습니다.

- 북미는 비료 분야에서 가장 성숙한 시장 중 하나이며 지난 몇 년간 성장률이 둔화되었습니다.

- 작물 중에서는 옥수수와 밀 작물이 미국 질소 비료 수요의 거의 절반을 차지했습니다. 따라서 이 지역에서 질소 비료를 제공하는 공급업체는 비료 시장의 주요 점유율을 차지하고 있으며 포장 솔루션에 대한 수요를 주도하고 있습니다.

- 미국에서는 암모니아 생산의 대부분이 루이지애나, 오클라호마, 텍사스의 대규모 천연가스 매장지 근처에서 이루어지며, 이는 천연가스를 수소 공급 원료로 사용하고 암모니아 생산에 필요한 높은 온도와 압력에 연료를 공급하기 때문입니다. 암모니아의 대부분은 해외 기업에서 생산되어 국내 소비용으로 사용되며, 트리니다드토바고와 캐나다에서 일부 수입됩니다. 이 지역에서 생산되는 암모니아는 극소량만 수출됩니다.

- 이 지역에서 가장 큰 암모니아 생산업체는 Nutrien, CF Industries, Moasaic, Yara입니다.

- 전 세계 비료 부문에서 이 지역이 차지하는 비중이 높기 때문에 미국과 캐나다의 포장재에 대한 제조업체의 수요는 상당합니다. 또한 이 지역의 공급업체들은 간편하고 지속 가능한 비료 포장 솔루션에 주목하고 있습니다.

플라스틱이 가장 큰 시장 점유율을 차지

- 미국과 캐나다 등 북미 지역의 국가는 전 세계적으로 플라스틱 수지를 생산하는 대표적인 국가입니다. 미국화학회의 플라스틱 산업 생산자 통계(PIPS) 그룹에 따르면, 북미 지역의 수지 생산량은 2020년 1,231억 파운드에서 0.7% 증가한 1,242억 파운드로 증가했습니다. 미국화학위원회에 따르면 폴리에틸렌(PE)이 2020년 생산량에서 가장 큰 비중을 차지했으며, 폴리프로필렌(PP), 폴리염화비닐(PVC), 폴리스티렌(PS)이 그 뒤를 이었습니다.

- 폴리에틸렌(PE)은 보편적으로 사용되기 때문에 가장 선호되는 소재 중 하나입니다. 열가소성 플라스틱이므로 이상적인 밀봉 매체이며 우수한 수분 장벽을 형성합니다. 특히 습한 기후에서 농약 제제를 보존하는 것이 가장 중요한 요구 사항입니다.

- 고밀도 폴리에틸렌(HDPE) 블로우 성형 용기는 설계 및 제작 시 유연성이 뛰어나고 수분 차단성이 우수하며 탄화수소 용매에 대한 저항성이 낮습니다. 또한 이축 배향 폴리에스테르는 용매 및 수성 액체 제품 포장에 널리 사용됩니다.

- 60개 이상의 주요 브랜드, 비영리 단체, 정부 기관이 미국 내 플라스틱 순환 경제를 만들기 위해 협력하고 있습니다. 이러한 노력은 이 지역의 농약 제품에 대한 일회용 플라스틱 사용을 줄일 수 있을 것으로 기대됩니다.

북미의 농약 포장 산업 개요

북미 농약 포장 시장은 세분화되어 있으며, 지역 및 글로벌 업체가 상당수 존재합니다.

- 2022년 2월 : 연포장 및 재료 과학 분야의 선두주자 중 하나인 ProAmpac은 수상 경력에 빛나는 연포장 제품 제조업체인 Belle-Pak Packaging을 인수했다고 발표했습니다.

- 2021년 9월 : GreifInc.는 환경 내 플라스틱 쓰레기를 줄이고 지구를 보호하기 위해 50개 이상의 회사로 구성된 비영리 단체와 연합을 맺었습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

- 대체품의 위협

- 산업 밸류체인 분석

- COVID-19의 농약 포장 시장에 대한 영향

- 산업 규정 및 표준

- B2B와 직접 채널에 의한 판매 내역에 관한 정성적 고찰

제5장 시장 역학

- 시장 성장 촉진요인

- 제품의 유통 기한을 늘리기위한 재료 기반 혁신과 포장의 지속 가능성이라는 지속적인 주제

- 시장의 과제

- 규제 및 가격 관련 과제

제6장 시장 세분화

- 제품 유형별

- 가방 및 파우치

- 용기 및 캔

- 중간 벌크 용기(IBC)

- 기타

- 재료별

- 플라스틱

- 종이 및 판지

- 금속

- 기타

- 용도별

- 비료

- 살충제

- 제초제

- 기타

제7장 경쟁 구도

- 기업 프로파일

- LC Packaging International BV

- Greif Inc.

- Mondi Group

- Sonoco Products Company

- ProAmpac LLC

- Mauser Packaging Solutions

- Greif, Inc

- Tri Rinse

- Silgan Holdings

- Hoover CS

제8장 투자 분석

제9장 시장의 미래

HBR 25.05.09The North America Agricultural Chemical Packaging Market size is estimated at USD 1.02 billion in 2025, and is expected to reach USD 1.21 billion by 2030, at a CAGR of 3.4% during the forecast period (2025-2030).

Key Highlights

- Agrochemical packaging is one of the crucial parts of the agriculture industry as agrochemical products, such as fertilizers and pesticides, are toxic. They require advanced packaging solutions, helping reduce the risk of storing, handling, and transporting such chemical products. Packaging solutions used here are designed for better sealing.

- Among the materials, plastic is the most widely used packaging material for agrochemical products. The demand for bags, bottles, pouches, and containers is increasing, and vendors in the market are offering innovative and high-safety packaging solutions. For example, Scholle IPN offers a bag-in-a-box pouch packaging solution for packaging agricultural chemical products in the market.

- With the advancements in biodegradable packaging solutions fueling the demand for such packaging solutions, various vendors in the market are focusing on adopting such solutions as part of their offering, focusing on recycled resins. For example, in January 2021, Mauser Packaging Solutions introduced the KORTRAX Barrier Tight-Head container for transporting hazardous solvent-based products that are traditionally difficult to contain. KORTRAX containers are 100% recyclable post-use and are available in 20-liter, 5-gallon, and 10-liter sizes.

- According to Federal laws and regulations, there are many regulations with which a product's label or markings must comply before being sold in the United States. Labeling requirements related to legal metrology must abide by The Fair Packaging and Labeling Act (FPLA) and Uniform Packaging and Labeling Regulation (UPLR). In addition, all products imported into the US must conform to Title 19, United States Code, Chapter 4, Section 1304 and 19 CFR 134, Country of Origin Marking regulations.

- The packaging regulations limit vendor profits and divide them into smaller packages as weight and quantity regulations are to be followed. Packaging solution providers also invest in compliance consultants and even outsource these compliance handling processes to entities that take care of these processes, thus impacting their profits in the market.

- The COVID-19 outbreak has affected international trade and global supply chains of essential and non-essential goods and services. With the spread of COVID-19 across the world, businesses have suffered significantly. The market was initially impacted due to the pandemic. Many countries in the region postponed the ban on single-use plastic. The pandemic led to the increase in the usage of plastic packaging for chemicals due to significant growth in e-commerce.

North America Agricultural Chemical Packaging Market Trends

Fertilizers to Hold Major Market Share

- In terms of agrochemicals, such as fertilizers, pesticides, herbicides, and other chemicals, the North American market has reached significant maturity, with the demand maintaining a steady point over the last few years. It is expected to remain the same over the coming years as well.

- North America is one of the most mature markets for fertilizer; it witnessed a slower growth rate in the last few years. According to the IFA, a prominent share of Nitrogen fertilizer application in the United States was held by Ammonia, Urea, and UAN, with a combined percentage share of over 60%.

- Among the crops, Maize and Wheat crops held nearly half of the country's Nitrogen fertilizer demand. Hence, vendors offering Nitrogen fertilizers in the region command a major share of the fertilizer market and drive the demand for packaging solutions.

- In the United States, most ammonia production occurs near large natural gas reserves in Louisiana, Oklahoma, and Texas due to the use of natural gas as a hydrogen feedstock and to fuel the high temperature and pressure needed to produce ammonia. A major share of the ammonia is produced by international companies and used for domestic consumption, with some imports from Trinidad and Tobago and Canada. A very small amount of ammonia produced in the region is exported.

- The region's largest ammonia producers are Nutrien, CF Industries, Moasaic, and Yara. Nitrogen fertilizer production facilities operate daily but have limited storage capacity, so fertilizers must be transported to warehouses and terminals for storage. Modes of transportation used to transport ammonia include refrigerated barge, rail car, pipeline, and tank truck.

- With the region's major share of the global fertilizer sector, the manufacturers' demand for packaging in the United States and Canada is significant. In addition, the region's vendors are witnessing easy and sustainable packaging solutions for fertilizers. For instance, in April 2021, Johnny Appleseed Organic came out with ClimateGard, a no-kill fertilizer for gardens that comes in sustainable cotton bags.

Plastic to Hold the Largest Market Share

- The countries in the North American region, such as the United States and Canada, are prominent manufacturers of plastic resins worldwide. According to the American Chemistry Council's Plastics Industry Producers Statistics (PIPS) Group, North American resin output increased by 0.7% to 124 billion pounds, up from 123.1 billion pounds in 2020. Polyethylene (PE) accounted for the largest share of production in 2020, followed by polypropylene (PP), polyvinyl chloride (PVC), and polystyrene (PS), according to the American Chemistry Council.

- Polyethylene (PE) is one of the most preferred materials because it has universal application. It is thermoplastic, and therefore an ideal sealing medium, and forms an excellent moisture barrier. The predominant requirement is the preservation of agrochemical formulations, particularly in humid climates.

- Blow-molded containers of high-density polyethylene (HDPE) offer broad flexibility in design and construction, good moisture barrier properties, and poor resistance to hydrocarbon solvents. Also, Biaxially oriented polyester is widely used for packaging solvent and aqueous-based liquid products.

- More than 60 major brands, nonprofits, and government agencies are coming together to create a circular economy for plastics in the United States. Such acts are poised to reduce the usage of single-use plastics for agrochemical products in the region.

- Further, major cities are taking corrective measures to reduce the application of plastic packaging solutions for agricultural chemicals. For instance, in August 2021, Montreal made plans to ban many single-use plastics by March 2023.

North America Agricultural Chemical Packaging Industry Overview

The North American agricultural chemical packaging market is fragmented, with a considerable number of regional and global players. Owing to their market penetration and the ability to offer advanced products, intense competitive rivalry is expected. Moreover, the involvement of large-scale investment also increases the barriers to exit for existing players, thereby pushing the industry toward improved competition.

- February 2022 - ProAmpac, one of the leaders in flexible packaging and material science, announced that it has acquired Belle-Pak Packaging, an award-winning manufacturer of flexible packaging products. With the addition of Belle-Pak, ProAmpac expands its growing presence in Canada and extends its reach in high-growth e-commerce, healthcare and logistics end markets.

- September 2021 - Greif Inc. joined an alliance with a non-profit organization consisting of over 50 companies to end plastic waste in the environment and protect the planet. The alliance consists of member companies and supporters representing companies and organizations from across the plastic value chain and they partner with government, environmental and non-governmental organizations around the world to address the challenge of ending plastic waste in the environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Agricultural Chemical Packaging Market

- 4.5 Industry Regulations and Standards

- 4.6 Qualitative Coverage on the Beakdown of B2B and Direct Channel-based Sales

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging

- 5.2 Market Challenges

- 5.2.1 Regulatory and Price-related Challenges

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Bags and Pouches

- 6.1.2 Containers and Cans

- 6.1.3 Intermediate Bulk Containers (IBCs)

- 6.1.4 Other Product Types

- 6.2 By Material Type

- 6.2.1 Plastic

- 6.2.2 Paper and Paperboard

- 6.2.3 Metal

- 6.2.4 Other Materials

- 6.3 By Application Type

- 6.3.1 Fertilizers

- 6.3.2 Pesticides

- 6.3.3 Herbicides

- 6.3.4 Other Application Types

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 LC Packaging International BV

- 7.1.2 Greif Inc.

- 7.1.3 Mondi Group

- 7.1.4 Sonoco Products Company

- 7.1.5 ProAmpac LLC

- 7.1.6 Mauser Packaging Solutions

- 7.1.7 Greif, Inc

- 7.1.8 Tri Rinse

- 7.1.9 Silgan Holdings

- 7.1.10 Hoover CS