|

시장보고서

상품코드

1690889

창고 자동화 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Warehouse Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

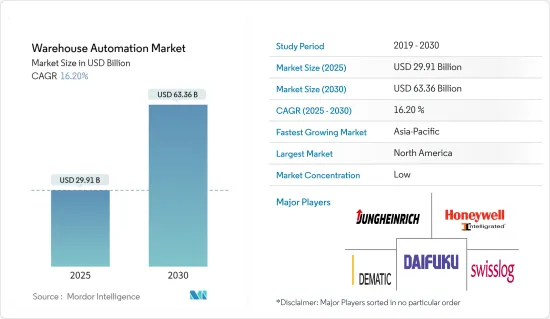

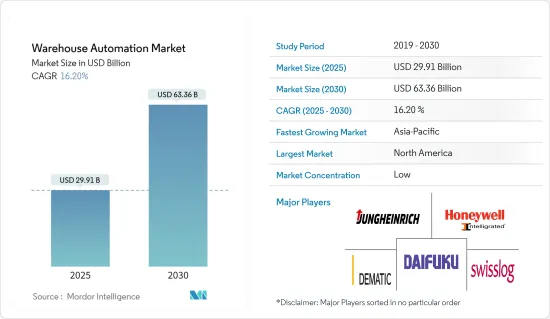

창고 자동화 시장 규모는 2025년에 299억 1,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 16.2%로 성장할 전망이며, 2030년에는 633억 6,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 물류 자동화는 제어 시스템, 기계 및 소프트웨어를 사용하여 업무 효율성을 높이는 것을 의미합니다. 이는 보통 창고나 배송 센터에서 실행되어야 하는 프로세스에 적용되며 최소한의 인적 개입만 필요로 합니다. 자동화 물류의 이점으로는 고객 서비스 향상, 확대성 및 속도, 조직 관리, 실수 절감 등을 들 수 있습니다.

- 창고의 자동화는 최소한의 인적 지원으로, 창고로의, 창고내의, 창고로부터 고객으로의 재고 이동을 자동화합니다. 자동화 프로젝트의 일환으로서, 기업은 반복적인 육체 노동이나 수작업에 의한 데이터 입력 및 분석을 수반하는 노동 집약적인 업무를 배제할 수 있습니다.

- 게다가 세계의 전자상거래 산업의 성장과 효율적인 창고 관리 및 재고 관리의 요구가 높아지면서 시장 조사의 원동력이 되고 있습니다. 창고 관리의 자동화는 전체적인 비즈니스 비용을 절감하고 제품 배송의 실수를 줄이는 면에서 매우 편리합니다. 저명한 3PL 기업이자 창고 자동화 솔루션의 중요한 최종 사용자인 DHL에 따르면 이점이 있음에도 불구하고 창고의 80%는 '자동화를 지원하지 않고 아직까지 수작업으로 운영되고 있습니다'. 게다가 창고, 즉 컨베이어, 소터, 픽앤플레이스 솔루션을 사용하는 창고는 전체 창고의 15%를 차지하고 있습니다. 반면 자동화된 창고는 현재 창고의 5%에 불과합니다.

- 예측 불가능한 수요 및 공급망과의 투명성과 협업의 부족은 많은 제조업체들이 비즈니스 목표를 달성하기 위한 큰 장벽이 되고 있습니다. 그러나 제조사가 복잡성 원인을 평가하고 창고 관리를 최적화함으로써 공급망에 대한 시각을 높이면서 변동하는 수요에 효율적으로 대응할 것으로 기대됩니다.

- 마찬가지로, 창고 관리 시스템(WMS)은 워크플로우 효율성을 개선하고, 오류를 줄이고, 오류와 관련된 비용을 절약하며, 주문 처리에 걸리는 턴어라운드 시간을 단축할 수 있지만, WMS 운영은 전자상거래 사업에 시간과 비용이 듭니다. WMS 운영에는 하드웨어를 위한 막대한 초기 비용, 대규모 훈련, 유지를 위한 추가적인 월 비용이 필요합니다.

창고 자동화 시장 동향

소매업이 크게 성장

- 창고 자동화는 전자상거래 및 식료품과 같은 다양한 소매업에서 이용되고 있습니다. 창고 자동화에는 생산성 향상에서 노동 관련 위험 감소까지 여러 이점이 있습니다. 전자상거래 창고 자동화는 물류 시설에 기술을 도입하고 업무 성능을 높이는 것으로 이루어져 있습니다. 상무부 인구조사국에 따르면 2022년 전자상거래 총 매출액은 1조 341억 달러로 2021년부터 7.7% 증가(+-0.4%)했습니다. 2022년 소매 총매출액은 2021년부터 8.1% 증가(+-0.9%)했습니다.

- 이 엄청난 수요에 대응하기 위해 수작업에 의한 창고를 자동화된 풀필먼트 업무로 전환하는 창고 자동화가 급속히 확대되고 있으며, 미래 운영 비용을 관리하면서 대규모 고객 수요에 대응하기 위해 필수적인 것이 되고 있습니다. 현재, 많은 소매 기업이 규모가 확대되고 복잡해지는 전자상거래 물류 업무에 대응해, 늘어나는 고객 수요를 보다 신속하고 비용 효율적으로 채우기 위해, 창고 자동화 솔루션의 도입을 진행하고 있습니다.

- 소매점의 창고에는 제품을 보관하기 위한 자동 취급 장비부터 제품 정리 정돈을 극대화하는 디지털 시스템에 이르기까지 모든 작업을 수행하기 위한 다양한 자동화 솔루션을 도입할 수 있습니다. 대형 소매 기업은, 전자상거래 및 옴니 채널 시설의 풀필먼트 업무를 간소화하기 위해서, 작업원과 함께 일하는 자동 반송차(AGV)나, 자동화의 다음 레벨인 자동 이동 로봇(AMR)을 활용하고 있습니다.

- 게다가 급속히 확대되는 전자상거래 부문에 대응하고 세계의 유행에서 배운 교훈을 고려하기 위해 대기업은 창고의 응답성, 회복력, 신뢰성을 높이기 위해 노력하고 있습니다. 예를 들어, 아마존은 2022년 4월 '공급망, 풀필먼트 및 물류 혁신에 박차를 가하기 위해' 자동화 및 직장 로보틱스에 중점을 둔 10억 달러의 신흥 기업 자금 조달 프로그램인 Amazon Industrial Innovation Fund(AIIF)를 설립했습니다.

아시아태평양이 큰 점유율을 차지할 전망

- 아시아태평양의 창고 자동화 시장은 이 지역의 산업 수가 증가하고 투자 수익률(ROI)을 높이기 위한 자동화와의 통합으로 크게 확대되고 있습니다. 아시아태평양 창고 자동화는 자동화 제품의 생산, 판매 및 무역이 증가하는 중국이 지배적일 것으로 예측됩니다.

- 게다가 중국 정부는 국가계획 '메이드 인차이나 2025' 하에 중국을 제조업의 거인에서 세계 제조 대국으로 변모시킬 계획이기 때문에 창고 자동화 산업은 제조업에서 중국의 우위성에서 혜택을 받을 것으로 예상됩니다. 이 계획에는 중국의 로봇 공급업체를 강화하고 중국 내외 시장 점유율을 더욱 급증시키는 것도 포함되어 있습니다.

- 창고 자동화에 대한 수요에는 자동화된 공급망이 포함되며, 더욱 유리한 투자에 의해 지원됩니다. 이 나라에서는 시장 성장을 더욱 촉진하기 위한 몇 가지 투자가 연구되고 있으며, 주요 주요 기업이 이 지역에 진출하거나 벤처 캐피탈이 미래의 신흥 기업에 자금을 도입하고 있습니다.

- 인도에서도 제조업이 고성장 부문 중 하나로 떠오르고 있습니다. 예를 들어 Make in India 프로그램은 인도를 중요한 제조 거점으로 세계 지도에 게재하여 인도 경제에 세계의 인지도를 주고 있습니다. Make in India 캠페인은 인도 산업용 로봇의 새로운 출시를 지원하고 창고 자동화 기회를 촉진하고 있습니다.

창고 자동화 산업 개요

창고 자동화 시장은 경쟁이 치열해지고 있습니다. 이 시장의 주요 세계 참가 기업에는 Dematic Group, Daifuku Co.Ltd., Swisslog Holding AG, Honeywell Intelligrated, Junheinrich AG 등이 있습니다. 제품의 출시, 인수 및 파트너십은 창고 자동화 산업에서 사업을 전개하는 시장 진입 기업이 채용하는 주요 전략입니다.

2023년 1월-JungheinrichAG는 미국 창고 자동화 시장에 대한 액세스를 강화하기 위해 미국 래킹 및 창고 자동화 솔루션의 주요 공급업체인 인디애나의 Storage Solutions group을 인수했습니다.

2022년 9월-Dematic은 Upshopto와 제휴하여 식료품 산업과 함께 성장하는 통합 풀필먼트 서비스를 기재하고 있습니다. 이 제휴를 통해 풀필먼트 비즈니스의 확대를 원하는 식료품점은 소비자 데이터를 보관하고 관리할 수 있는 툴을 이용할 수 있게 됩니다. Dematic은 현재 Upshop 프로세스에 연결하기 위한 간단한 소프트웨어와 함께 자동화 경험을 기재하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력-Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 산업 밸류체인 분석

- COVID-19의 산업에 대한 영향 평가

- 창고 투자 시나리오

- 창고 자동화 시장에 대한 거시 경제 요인의 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 전자상거래 산업의 급성장 및 고객 기대

- 제조 복잡화 및 기술 이용 가능성 증가

- 시장의 과제

- 고액의 설비 투자

제6장 시장 세분화

- 컴포넌트별

- 하드웨어

- 이동 로봇(AGV, AMR)

- 자동 보관 및 검색 시스템(AS/RS)

- 자동 컨베이어 및 분류 시스템

- 디파레타이징 및 팔레타이징 시스템

- 자동인식 데이터 수집(AIDC)

- 피스 피킹 로봇

- 소프트웨어(창고 관리 시스템(WMS) 및 창고 실행 시스템(WES))

- 서비스(부가가치 서비스, 유지보수 등)

- 하드웨어

- 최종 사용자별

- 식음료(제조 시설, 배송 센터 포함)

- 우편 및 소포

- 소매

- 의류

- 제조업(내구 및 비내구)

- 기타

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Dematic Group(Kion Group AG)

- Daifuku Co. Limited

- Swisslog Holding AG(KUKA AG)

- Honeywell Intelligrated(Honeywell International Inc.)

- Jungheinrich AG

- Murata Machinery Ltd

- Knapp AG

- TGW Logistics Group GmbH

- Kardex Group

- Mecalux SA

- BEUMER Group GmbH & Co. KG

- SSI Schaefer AG

- Vanderlande Industries BV

- WITRON Logistik Informatik GmbH

- Oracle Corporation

- One Network Enterprises Inc.

- SAP SE

제8장 투자 분석

제9장 시장의 미래

AJY 25.05.09The Warehouse Automation Market size is estimated at USD 29.91 billion in 2025, and is expected to reach USD 63.36 billion by 2030, at a CAGR of 16.2% during the forecast period (2025-2030).

Key Highlights

- Automation in logistics refers to using control systems, machinery, and software to enhance the efficiency of operations. It usually applies to the processes that must be performed in a warehouse or distribution center, which requires minimal human intervention. Some benefits of automation logistics are improved customer service, scalability and speed, organizational control, and reduction of mistakes, among others.

- Warehouse automation automates inventory movement into, within, and out of warehouses to customers with minimal human assistance. As part of an automation project, a business can eliminate labor-intensive duties that involve repetitive physical work and manual data entry and analysis.

- Moreover, the growth in the e-commerce industry worldwide and the growing need for efficient warehousing and inventory management are driving the market studied. Automation in warehousing offers extreme convenience when cutting down overall business costs and reducing errors in product deliveries. According to DHL, a prominent 3PL company and a significant end-user of warehouse automation solutions, despite the advantages, 80% of warehouses are 'still manually operated with no supporting automation.' Furthermore, warehouses, i.e., those that use conveyors, sorters, and pick and place solutions, account for 15% of the entire warehouses. In contrast, only 5% of current warehouses are automated.

- Unpredictable demand and a lack of transparency and collaboration with the supply chain present a significant barrier to reaching business goals for many manufacturers. However, when manufacturers evaluate the sources of complexity and optimize warehouse management, they are expected to efficiently meet variable demand while increasing their view of the supply chain.

- Similarly, while warehouse management systems (WMS) can improve workflow efficiency, reduce errors, save on costs associated with errors, and get faster turn-around time for order fulfillment, running a WMS can be time-consuming and expensive for an e-commerce business. It requires huge upfront costs for hardware, extensive training, and additional monthly costs for upkeep.

Warehouse Automation Market Trends

Retail to Have a Significant Growth

- Warehouse automation is used in various retail activities, including e-commerce and grocery. For warehouses, automation has multiple advantages, from boosting production to lowering labor-related risks. E-commerce warehouse automation consists of implementing technologies in logistics facilities to boost operational performance. According to the Census Bureau of the Department of Commerce, Total e-commerce sales for 2022 were USD 1,034.1 billion, an increase of 7.7 percent (+-0.4%) from 2021. Total retail sales in 2022 increased by 8.1 percent (+-0.9%) from 2021.

- To address this massive demand, warehouse automation is rapidly expanding to transform manual warehouses into automated fulfillment operations, which are proving vital to meeting customer demand at scale while managing operating costs in the future. Currently, many retailers are increasingly implementing warehouse automation solutions that seek to handle the growing scale and complexity of their e-commerce logistics operations and meet the ever-increasing demand of their customers more quickly and cost-effectively.

- A retail warehouse can be outfitted with various automated solutions to carry out all tasks, from automatic handling equipment for storing products to digital systems that maximize product organization. Big retailers are utilizing automated guided vehicles (AGVs) and the next level of automation-automated mobile robots (AMRs)-working alongside workers to simplify the fulfillment operations of their e-commerce and omnichannel facilities.

- Moreover, to meet the rapidly expanding e-commerce sector and consider the lessons learned from the worldwide pandemic, leading retailers strive to make warehouses responsive, resilient, and dependable. For instance, in April 2022, Amazon established the Amazon Industrial Innovation Fund (AIIF), a USD 1 billion startup funding program that will be used to "spur supply chain, fulfillment, and logistics innovation," focusing on automation and workplace robotics.

Asia-Pacific is Expected to Hold Significant Share

- The market for warehouse automation in the Asia-Pacific is expanding significantly due to the rising number of industries in the region and their integration with automation to increase the return on investment (ROI). The Asia-Pacific warehouse automation is predicted to be dominated by China with the growing production, sales, and trade of automation products.

- Moreover, The warehouse automation industry is expected to benefit from China's dominance in the manufacturing sector as the Chinese government plans to transform China from a manufacturing giant to a global manufacturing power under the national plan "Made in China 2025". This plan includes strengthening Chinese robot suppliers and further surging their market shares in China and abroad.

- The demand for warehouse automation includes an automated supply chain, further supported by favorable investments. The country has been marked with several investments to further the market's growth studied, with major key players expanding into the region and introducing funds by venture capitalists in emerging start-ups with potential.

- Manufacturing has emerged as one of the high-growth sectors in India as well. For instance, the Make in India program places India on the world map as a significant manufacturing hub and provides global recognition to the Indian economy. The Made in India campaign has bolstered multiple new launches in industrial robots in the country, thus driving opportunities for warehouse automation.

Warehouse Automation Industry Overview

The warehouse automation market is highly competitive. Some key global players in this market are Dematic Group, Daifuku Co. Limited, Swisslog Holding AG, Honeywell Intelligrated, and Jungheinrich AG. Product launch, acquisition, and partnership are key strategies market players operating in the warehouse automation industry adopt.

In January 2023, JungheinrichAG acquired Indiana-based Storage Solutions group, a leading provider of racking and warehouse automation solutions in the United States, to gain enhanced access to the US warehousing and automation market.

In September 2022, Dematic partnered with Upshopto to offer integrated fulfillment services that grow with the grocery industry. With the help of the alliance, grocery stores wishing to expand their fulfillment businesses will have access to tools that let them store and manage their consumer data. Dematic will offer its experience in automation along with simple software to connect with current Upshop processes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

- 4.5 Warehouse Investment Scenario

- 4.6 Impact of Macro-economic Factors on the Warehouse Automation Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Exponential Growth of the E-commerce Industry and Customer Expectation

- 5.1.2 Increasing Manufacturing Complexity and Technology Availability

- 5.2 Market Challenges

- 5.2.1 High Capital Investment

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.1.1 Mobile Robots (AGV, AMR)

- 6.1.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3 Automated Conveyor & Sorting Systems

- 6.1.1.4 De-palletizing/Palletizing Systems

- 6.1.1.5 Automatic Identification and Data Collection (AIDC)

- 6.1.1.6 Piece Picking Robots

- 6.1.2 Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES))

- 6.1.3 Services (Value Added Services, Maintenance, etc.)

- 6.1.1 Hardware

- 6.2 By End-User

- 6.2.1 Food and Beverage (Including Manufacturing Facilities and Distribution Centers)

- 6.2.2 Post and Parcel

- 6.2.3 Retail

- 6.2.4 Apparel

- 6.2.5 Manufacturing (Durable and Non-Durable)

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dematic Group (Kion Group AG)

- 7.1.2 Daifuku Co. Limited

- 7.1.3 Swisslog Holding AG (KUKA AG)

- 7.1.4 Honeywell Intelligrated (Honeywell International Inc.)

- 7.1.5 Jungheinrich AG

- 7.1.6 Murata Machinery Ltd

- 7.1.7 Knapp AG

- 7.1.8 TGW Logistics Group GmbH

- 7.1.9 Kardex Group

- 7.1.10 Mecalux SA

- 7.1.11 BEUMER Group GmbH & Co. KG

- 7.1.12 SSI Schaefer AG

- 7.1.13 Vanderlande Industries BV

- 7.1.14 WITRON Logistik + Informatik GmbH

- 7.1.15 Oracle Corporation

- 7.1.16 One Network Enterprises Inc.

- 7.1.17 SAP SE