|

시장보고서

상품코드

1692105

헬리콥터 서비스 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Helicopter Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

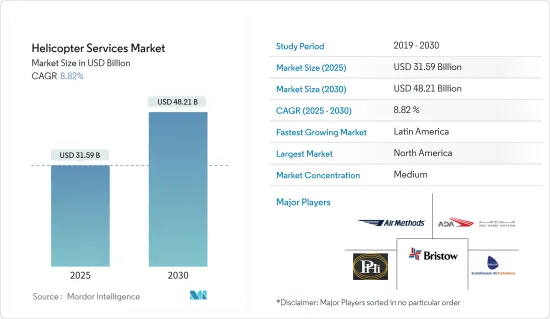

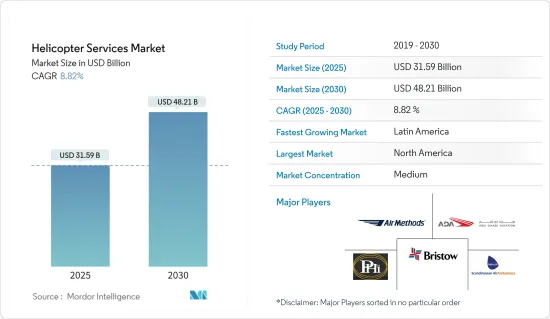

헬리콥터 서비스 시장 규모는 2025년에 315억 9,000만 달러, 2030년에는 482억 1,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 8.82%로 성장할 것으로 예상됩니다.

헬리콥터는 호버링, 착륙, 수직 이륙 및 제한된 공간으로 출입할 수 있기 때문에 다양한 분야에서 널리 사용됩니다. 사용 및 운영 비용에 따라 운영자는 특정 헬리콥터 모델을 선택합니다. 현재 에어버스, 벨, 로빈슨 헬리콥터가 신규 납품기수로 시장을 독점하고 있습니다. 또한 경량 헬리콥터에 대한 다양한 최종 사용자 수요는 예측 기간 동안 시장을 긍정적으로 이끌 것으로 예상됩니다.

첨단 비행 능력을 갖춘 대형 무인 항공기의 도입은 헬리콥터 회사가 현재 기술적 제약을 없앨 수 없다는 사실과 관련하여 일부 애플리케이션에서 드론 서비스가 헬리콥터 서비스를 대체 할 수있게 되었습니다. 이 요인은 예측 기간 동안 시장 성장에 도전을 줄 수 있습니다.

그러나 심각한 도로 정체와 특히 신흥 국가의 응급 의료 서비스에서 헬리콥터 서비스의 신속한 공중 운송의 필요성과 같은 요인이 헬리콥터 서비스 시장에 새로운 기회를 창출하고 있습니다.

헬리콥터 서비스 시장 동향

예측기간 중 가장 높은 성장이 예상되는 항공구급차 부문

항공 구급차는 원격지로의 접근 제한과 장시간 이동의 문제를 줄일 수 있기 때문에 기존 도로 구급차 서비스보다 많은 장점이 있습니다. 항공 구급차에는 다양한 의료기기가 장착되어 있으며, 의료 승무원이 탑승하여 환자에게 초기 응급 의료를 제공합니다. 구명률 향상, 빠르고 편안한 운송, 짧은 시간 내에 넓은 범위를 커버할 수 있는 등 여러 장점이 있기 때문에 항공 응급 서비스 시장은 증가의 길을 따라가고 있습니다. 이러한 이점으로부터, 헬리콥터는 응급 의료 반송의 유력한 선택이 되고 있습니다.

예를 들면, 2019년부터 2023년에 걸쳐, 세계 전체에서 268기의 헬리콥터가 운항되어, 다양한 구급 및 의료 서비스를 실시했습니다. 항공 응급 서비스를 위한 헬리콥터는 상대방 브랜드 제조업체(OEM)에 의해 경량화되었습니다. 이 수요에 대응하기 위해 여러 국가가 새로운 항공 응급 헬리콥터를 조달하고 있습니다. 예를 들어, 2023년 11월, 노르웨이 항공 구급대는 덴마크에서 헬리콥터에 의한 응급 의료 서비스를 실시하기 위해, H135를 3기와 5장 날개의 H145를 2기 납입하는 계약을 에어 버스에 발주했습니다. 마찬가지로 2023년 12월, 가마 항공은 웨일스 항공 응급 자선을 위해 헬리콥터 응급 의료 서비스(HEMS)를 시작했습니다. 7,000만 달러의 계약으로 에어버스 H145 헬리콥터 4대가 운용 및 보수되고, 그 거점은 자선 단체의 기존 시설이 됩니다. 이와 같이 상대방 상표 제품 제조업체(OEM)에 의한 이러한 기술적 진보로 로터 크래프트 분야는 예측 기간 동안 눈부신 성장을 보일 것으로 보입니다.

예측기간 중 북미가 최대 시장 점유율을 차지

헬리콥터 서비스 시장에서는 북미가 가장 높은 점유율을 차지합니다. 이 이점은 헬리콥터 보유 대수가 가장 많고 항공 응급 서비스에 헬리콥터 이용이 증가하고 있기 때문입니다. 미국의 헬리콥터 보유기 수는 약 7,014대이며, 그 중 항공 구급차는 1,000대 이상입니다. 보다 깨끗하고 지속 가능한 에너지 수요에 대한 경사가 강해지고 있는 가운데, 전미에서 증가하는 해상 풍력 발전소 프로젝트가 헬리콥터 서비스 수요를 밀어 올리고 있습니다. 그 결과 새로운 계약과 파트너십이 시장 가치를 높이고 있습니다.

예를 들어 Orsted와 Eversource는 2022년 4월 HeliService International Inc.가 양사의 합작 사업인 미국 북동부의 해상 풍력 발전 프로젝트의 헬리콥터 승무원 교체 업무를 수주했다고 발표했습니다. 이 회사는 Leonardo AW169 헬리콥터를 사용하여 일상 업무를 지원합니다. 이 나라에서는 석유 및 가스 부문으로부터의 수입이 증가하고 있어 헬리콥터 서비스 업계의 해외 분야에서의 헬리콥터 서비스의 필요성에 직접 영향을 주고 있습니다.

게다가 프라이빗 에퀴티 투자자들이 항공 구급시장의 유지 및 운영에 진입하고 있기 때문에 보다 나은 서비스를 제공할 가능성은 높아지고 있는 것, 운항 비용의 증대가 고객에게 부과되는 리스크도 있습니다. 마찬가지로 응급의료서비스, 수색구조, 레저용 전세편 등 다양한 용도의 헬리콥터에 대한 수요가 캐나다의 운항회사로부터 높아지고 있는 것도 이 지역 전체 시장 성장을 뒷받침하고 있습니다.

헬리콥터 서비스 산업 개요

헬리콥터 서비스 시장은 반통합적이며 여러 사업자가 다양한 헬리콥터 서비스를 제공하고 있는 것이 특징입니다. 수년 동안 항공 규제 기관은 헬리콥터 운항 회사에 엄격하고 강압적인 규칙과 규정을 도입해 왔습니다. 그러나 현재는 다양한 정부가 헬리콥터나 고정익기의 운항을 장려하는 지원법을 도입하여 일반 항공 부문의 발전에 노력하고 있습니다. 이 때문에 현지 기업의 유입이 늘어나 기존 기업의 신 시장 진출도 확대되고 있습니다. 또한 주요 기업은 전략적 파트너십, 합병 및 인수를 통해 사업 확대에 주력하고 있습니다. 이러한 전략은 예측 기간 동안 기업의 성장에 도움이 될 것으로 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자 및 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 용도

- 항공 구급차

- 비즈니스 및 기업 출장

- 수색과 구조

- 레저 전세

- 수송

- 미디어 및 엔터테인먼트

- 측량

- 해외

- 기타 용도

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 인도네시아

- 말레이시아

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 터키

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Acadian Air Med Services(Acadian Companies)

- Air Methods Corporation

- Heli-union

- Abu Dhabi Aviation

- Emsos Medical Pvt. Ltd.

- Bristow Group Inc

- LUXEMBOURG AIR RESCUE ASBL

- PHI Group, Inc.

- Babcock Scandinavian Air Ambulance(Babcock International Group)

- CHC Group LLC

제7장 시장 기회와 앞으로의 동향

SHW 25.04.09The Helicopter Services Market size is estimated at USD 31.59 billion in 2025, and is expected to reach USD 48.21 billion by 2030, at a CAGR of 8.82% during the forecast period (2025-2030).

Helicopters are widely used in several sectors because they can hover, land, take off vertically, and enter and exit confined spaces. Depending upon the application and cost of operation, operators select a particular helicopter model. Airbus, Bell, and Robinson helicopters are currently dominating the market in terms of new deliveries. In addition, the demand from various end users for lightweight helicopters is expected to drive the market positively during the forecast period.

The introduction of large drones with advanced flight capabilities, coupled with the inability of helicopter companies to eliminate current technology limitations, resulted in drone services continuing to be a substitute for helicopter services in several applications. This factor might challenge the market's growth during the forecast period.

However, factors such as severe road congestion and the need for quicker aerial transportation for helicopter services in emergency medical services, especially in developing countries, create new opportunities for the helicopter services market.

Helicopter Services Market Trends

Air Ambulance Segment is Projected to Show the Highest Growth During the Forecast Period

Air ambulance offers numerous advantages over conventional road ambulance services, as the former helps mitigate the issue of limited access to remote areas and prolonged travel durations. Air ambulances are equipped with different medical equipment and have an onboard medical crew that provides initial emergency medical care to patients. The market for air ambulance services is on the rise owing to several benefits, such as increased survival rates, swift and comfortable transportation, and a vast coverage range in a shorter time. These advantages make helicopters a compelling choice for emergency medical transportation.

For instance, globally, from 2019 to 2023, 268 helicopters were in operation, performing various emergency and medical services. Helicopters for air ambulance services have been made lightweight by original equipment manufacturers (OEMs). Multiple countries are procuring new air ambulance helicopters to cater to this demand. For instance, in November 2023, the Norwegian Air Ambulance awarded a contract to Airbus to deliver three H135s and two five-bladed H145s to carry out helicopter emergency medical service missions in Denmark. Similarly, in December 2023, Gama Aviation launched its Helicopter Emergency Medical Services (HEMS) for the Wales Air Ambulance Charity. Under a USD 70 million contract, a fleet of four Airbus H145 helicopters will likely be operated and maintained, with their base of operations being the charity's existing sites. Thus, such technological advancements made by the original equipment manufacturers (OEMs) will lead to the rotor-craft segment showing impressive growth during the forecast period.

North America to Exhibit the Largest Market Share During the Forecast Period

North America held the highest shares in the helicopter services market. This dominance is owing to the presence of the largest helicopter fleet and the rising use of helicopters for air ambulance services. The US has a total fleet of around 7,014 helicopters, with air ambulances recorded at more than 1000 units. With the increase in inclination toward cleaner, more sustainable energy demands, the increasing offshore wind farm projects across the country have driven the demand for helicopter services. As a result, new contracts and partnerships have increased market value.

For instance, Orsted and Eversource announced in April 2022 that HeliService International Inc. had been awarded the contract for helicopter crew change operations for the two companies' joint venture of offshore wind projects in the Northeast United States. The company will use Leonardo AW169 helicopters to support its everyday operations. The country's increasing revenue from the oil and gas sector has been witnessing an increasing demand, which has thus directly impacted the need for helicopter services in the offshore segment of the helicopter services industry.

Furthermore, the growing influx of private equity investors into maintaining and operating the air ambulance market, despite improving the chances for better services, poses a risk of the increased cost of operations that could be levied on the customers. Similarly, the growing demand for helicopters for various applications such as emergency medical services, search and rescue, leisure charters, and others from Canadian operators drives the market growth across the region.

Helicopter Services Industry Overview

The helicopter services market is semi-consolidated and is characterized by several operators providing various helicopter services. Some of the major players in the market are Babcock Scandinavian Air Ambulance (Babcock International Group), Abu Dhabi Aviation, Air Methods Corporation, Bristow Group Inc., and PHI Group, Inc. Over the years, the aviation regulatory bodies introduced tough and rigid rules and regulations for helicopter operators. However, various governments are now introducing supportive laws encouraging helicopter and fixed-wing aircraft operations to develop the general aviation sector. This leads to increased influx of local players and expanding existing players into new markets. Furthermore, the key players focus on business expansion through strategic partnerships, mergers, and acquisitions. Such strategies are expected to help the players' growth during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Air Ambulance

- 5.1.2 Business and Corporate Travel

- 5.1.3 Search and Rescue

- 5.1.4 Leisure Charter

- 5.1.5 Transport

- 5.1.6 Media and Entertainment

- 5.1.7 Surveying

- 5.1.8 Offshore

- 5.1.9 Other Applications

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Indonesia

- 5.2.3.6 Malaysia

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Turkey

- 5.2.5.5 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Acadian Air Med Services (Acadian Companies)

- 6.2.2 Air Methods Corporation

- 6.2.3 Heli-union

- 6.2.4 Abu Dhabi Aviation

- 6.2.5 Emsos Medical Pvt. Ltd.

- 6.2.6 Bristow Group Inc

- 6.2.7 LUXEMBOURG AIR RESCUE ASBL

- 6.2.8 PHI Group, Inc.

- 6.2.9 Babcock Scandinavian Air Ambulance (Babcock International Group)

- 6.2.10 CHC Group LLC