|

시장보고서

상품코드

1692510

북미의 공조설비 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Air Conditioning Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

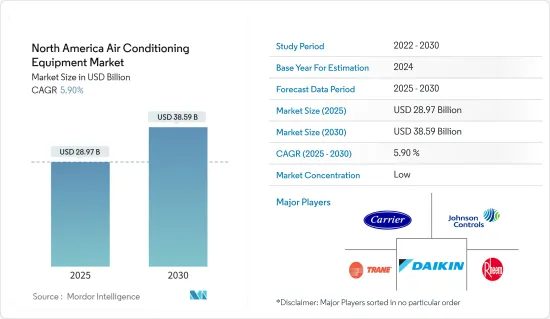

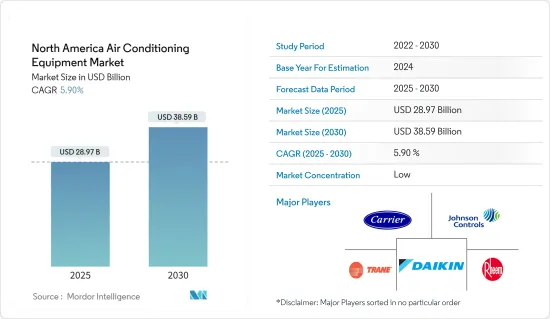

북미의 공조설비 시장 규모는 2025년 289억 7,000만 달러로 추정되고, 2030년에는 385억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 5.9%로 확대될 것으로 보입니다.

에어컨은 열을 꺼내 외부로 전달하여 공간을 냉각하는 시스템입니다. 이 냉각된 공기는 환기에 의해 건물 전체에 분배됩니다.

주요 하이라이트

- 미국의 부동산 시장은 주택, 상업, 공업의 각 분야에서 건설 지출이 증가하고 건축 허가 건수가 급증함에 따라 강력한 상승을 목격하고 있습니다. 정부에 의한 다액의 인프라 투자에 밀려, 더욱 확대하는 태세를 정돈하고 있는 것입니다. 이 기세는 공적인 대처에 그치지 않고, 민간의 상업 건설 사업도 견인력을 늘리고 있습니다.

- 이러한 상호 연결된 스마트 AC 장비에는 여러 가지 장점이 있습니다. 스마트 AC 시스템은 사용자 선호도를 배우고 그에 따라 냉방 일정을 조정하여 에너지 사용을 최적화하는 데 도움이 됩니다. 앱과 음성 명령으로 AC 시스템을 원격으로 조작할 수 있는 기능은 소비자의 표준 기대가 되고 있습니다.

- 1970년대의 오일 쇼크 이후, 가정에서의 에너지 효율 향상의 대처는 큰 변동을 경험해, 에너지 소비 삭감에 대한 경제적 인센티브가 높아졌습니다.

- 북미의 HVAC 업계는 엄격한 안전 규제와 기준을 준수하도록 요구되고 있습니다.

- IoT 대응의 스마트 공조설비는 스마트폰이나 데스크톱으로 공조를 조작 및 관리할 수 있기 때문에 소비자의 사이에서 인기를 모았습니다.

북미 공조설비 시장 동향

주택부문이 시장을 독점

- 이 지역의 주택용 공조설비 수요는 여름철의 더위를 완화해, 쾌적함을 제공하기 위해서 매우 중요하다는 점에서 증가하고 있습니다.

- 에너지 정보국(EIA)에 따르면, 센트럴 에어콘은 북미 사람들이 집을 식히는 주된 방법으로 널리 채택하고 있습니다. 또 다른 인기 옵션은 덕트리스 미니 스플릿 시스템입니다.

- 기후 변화로 인한 지역의 기온 상승으로 많은 주에서 에어컨 시스템의 필요성이 사치품에서 필수품으로 높아지고 있습니다. 지구의 기온이 상승하고 있기 때문에 이 채용 동향은 한층 더 에스컬레이트 하는 것으로 예측됩니다.

- 또한 미국 인구조사국에 따르면 2024년 4월 주택 빌딩과 주택 건설은 2023년 4월에 비해 8% 증가했습니다. 이런 요인이 시장의 성장을 가속할 것으로 예측됩니다.

현저한 성장을 이루는 캐나다.

- 이 나라에서는 고급 주택 인프라 프로젝트가 증가함에 따라 공조 수요가 급증하고 있습니다.

- CREA에 따르면 2023년 주택 판매 건수는 443,511건으로, 2025년에는 약 525,500건에 달할 것으로 예상되고 있습니다. 많은 지역에서는 기온의 상승과 습도의 높이를 특징으로 하는 비정상적인 더위와 열파가 발생하고 있습니다.

- 이러한 사태를 피하기 위해 정부는 공조 설비의 무료 제공에 힘을 쏟고 있습니다.

- BC Hydro가 관리하는 이 프로그램에서는 이 시점까지 6,000대의 에어컨이 무료로 배포되고 있어 추가 자금에 의해 합계 약 2만 8,000대의 에어컨이 배포될 전망입니다.

북미 공조설비 산업 개요

북미 공조설비 시장은 많은 밸브 시장 기업에 의해 단편화되고 있습니다. 공조설비 업계는 최대 시장 중 하나이기 때문에 시장 점유율을 저해하지 않고 이와 같은 다수의 대형 벤더가 존재하는 것은 지속 가능하며, 기업으로서는 Daikin Industries Ltd, Carrier Corporation, Rheem Manufacturing Company, Tran Inc.(Trane Technologies PLC), Johnson Controls International PLC 등이 있습니다.

- 2024년 3월 Carrier Corporation은 데이터센터용 고성능 냉각기의 첨단 혁신적인 제품 라인을 발표했습니다. 이 냉각기는 에너지 소비와 이산화탄소 배출량을 줄이고 데이터센터 운영자의 운영 비용을 줄이기 위해 고안되었습니다. 486.4 kW에서 1,464 kW까지의 이 장치는 신뢰할 수 있는 캐리어 스크류 컴프레서를 활용하여 효율성과 긴 수명을 보장합니다.

- 2024년 2월 Daikin Industries Ltd은 중요한 요소에 중점을 두고 에어컨을 강화했습니다. 지구 온난화 계수가 낮은 R32 냉매인 HFC-32를 채용해, 환경성과 에너지 절약성을 중시. 또한 에어컨의 기본 성능도 강화했습니다. 중요한 움직임으로 Daikin은 빌딩용 멀티 에어컨 VRV 7 시리즈를 2024년 11월에 발매했니다. 이 시리즈는 업계 최고의 에너지 효율을 자랑하며 환경 발자국 및 운영 부하를 줄이는 데 매우 중요합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 상정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- COVID-19의 후유증과 기타 거시경제 요인이 시장에 미치는 영향

- 산업 밸류체인 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 기존 기기의 성능 향상과 공조설비 감세의 부활

- 홈 오토메이션과 빌딩 오토메이션 시스템의 채용 확대

- 시장 성장 억제요인

- 엄격한 규제 준수 및 안전 기준

제6장 시장 세분화

- 유형별

- 유닛 에어컨

- 덕트 부착 스플릿

- 덕트리스 미니스플릿

- 실내 패키지형 및 루프탑형

- 룸 에어컨

- 패키지, 터미널, 에어컨

- 칠러

- 가변 냉매 흐름(VRF)

- 유닛 에어컨

- 최종 사용자별

- 주택용

- 상업용 및 산업용

- 국가별

- 미국

- 캐나다

- 효율별

- 저효율(13 SEER)

- 고효율(13 SEER 이상)

제7장 경쟁 구도

- 기업 프로파일

- Daikin Industries Ltd

- Carrier Corporation

- Rheem Manufacturing Company

- Trane Inc.(Trane Technologies PLC)

- Johnson Controls International PLC

- Mitsubishi Electric Corporation

- Lennox International Inc.

- Systemair AB

- Robert Bosch GmbH

- Electrolux AB

- LG Electronics Inc.

- Midea Group

- Schneider Electric SE

- GE Appliances

- Whirlpool Corporation

제8장 냉방기기 유통채널 분석 중앙공조, 룸공조

- 직접 판매

- 소매업체

- 도매업체, 판매자, 계약자

제9장 투자 분석

제10장 시장의 미래

JHS 25.05.15The North America Air Conditioning Equipment Market size is estimated at USD 28.97 billion in 2025, and is expected to reach USD 38.59 billion by 2030, at a CAGR of 5.9% during the forecast period (2025-2030).

An air conditioner is a system that cools a space by extracting heat and transferring it outside. This cooled air is then distributed throughout a building via ventilation. As an essential part of the HVAC system, air conditioners regulate home temperatures to enhance comfort and livability.

Key Highlights

- The US real estate market is witnessing a robust upswing, buoyed by escalating construction outlays and a surge in building permits across residential, commercial, and industrial segments. Notably, the US construction sector is poised for further expansion, fueled by substantial federal investments in infrastructure. This momentum extends beyond public initiatives, with private commercial construction endeavors also gaining traction.

- These interconnected and smart AC equipment offer numerous benefits. Smart AC systems help optimize energy usage by learning user preferences and adjusting cooling schedules accordingly. This not only provides comfort but also reduces energy consumption and costs. The ability to control AC systems remotely via smartphone apps or voice commands is becoming a standard consumer expectation. Advanced smart AC systems can monitor their own performance and alert users to potential issues before they become major problems. This can extend the life of the unit and ensure it operates efficiently.

- Efforts to promote energy efficiency in homes have experienced significant fluctuations since the oil shocks of the 1970s, which increased the financial incentives for reducing energy consumption. Currently, energy efficiency is a primary driver for home renovations, supported by various policies across North America. These policies include energy audits, energy performance certificates, and financial incentives like grants, subsidies, tax credits, low-interest loans, and third-party financing.

- The North American HVAC industry is required to follow strict safety regulations and standards. Utilizing gas detection and monitoring systems shows dedication to compliance and following safety guidelines. By incorporating these systems, HVAC companies can meet regulatory standards, create a safe workplace, and reduce the likelihood of facing penalties or legal consequences.

- IoT-enabled smart air conditioning equipment gained traction among consumers as these systems enable users to operate and manage ACs using smartphones and desktops. In April 2024, Soracom Inc., a prominent global IoT connectivity provider, announced its collaboration with Mitsubishi Electric Europe BV. The partnership aims to integrate Soracom's cellular connectivity into MELCloud, Mitsubishi Electric's cloud-based remote management system. MELCloud specifically caters to Mitsubishi Electric's air conditioning, heating, and heat recovery/ventilation products, ushering in a new era of remote control and management capabilities.

North America Air Conditioning Equipment Market Trends

Residential Sector to Dominate the Market

- The demand for residential air conditioning units in the region is increasing as they are crucial for providing comfort and relief from hot temperatures during the summer months. The types of air conditioning systems commonly used in residential settings vary depending on factors such as climate, building design, energy availability, and cultural preferences.

- According to the Energy Information Administration (EIA), central air conditioning is widely adopted by North Americans as the primary method of cooling their homes. The EIA reports a growing trend of households in the region opting for central air conditioning systems, which are significantly more favored than window or wall units. Another popular option is ductless mini-split systems. They provide zoned cooling, allowing homeowners to control the temperatures of different areas of the house independently.

- The rising temperatures in the region, attributed to climate change, have elevated the need for air conditioning systems from a luxury to a necessity in many states. Consequently, a growing number of individuals in the region are choosing to equip their homes with air conditioning. This adoption trend is poised to escalate further as the planet's temperature continues its upward trajectory. Given the shifting climate dynamics, the residential air conditioning market is set for significant growth over the forecast period.

- In addition, according to the US Census Bureau, construction of residential buildings and homes increased by 8% in April 2024 compared to April 2023. In April 2024, construction spending in residential reached an estimated annual rate of USD 902.29 billion. Such factors are anticipated to drive the market's growth. Furthermore, the growing residential construction across the region is expected to create new market opportunities in the coming years.

Canada to Witness Significant Growth

- The country is experiencing a surge in air conditioning demand due to the rise in luxury residential infrastructure projects. Market players can expect numerous opportunities over the forecast period, thanks to factors such as increased urbanization and higher per capita income. Central air conditioning systems are highly favored in Canada and are ideal for mid-to-large family homes, as well as for homes with multiple stories.

- According to CREA, the number of home sales in 2023 was recorded at 443,511, and it is expected to reach almost 525,500 by 2025. Due to the variable climate and severe winters, air conditioner equipment has become essential in the majority of Canadian households. Numerous regions in Canada experience extreme heat events or heat waves characterized by soaring temperatures and high levels of humidity. According to the initial data disclosed by the BC Coroners Service, a total of 619 individuals lost their lives due to the intense heat during the prolonged summer heat wave in British Columbia.

- To avoid such circumstances, the government is focusing on providing free air conditioning equipment. For instance, in May 2024, the BC government announced an additional CAD 20 million (USD 14.53 million) to provide thousands of free air conditioning units to those who need financial assistance and people vulnerable to heat.

- The program managed by BC Hydro has distributed 6,000 complimentary AC units up to this point, with additional funding anticipated to result in a total of approximately 28,000 AC units being distributed.

North America Air Conditioning Equipment Industry Overview

The North American air conditioning equipment market is fragmented due to many valve market players. Since the AC equipment industry is one of the largest markets, the existence of such a sheer number of major vendors without compromising their market shares is sustainable, and some of the players include Daikin Industries Ltd, Carrier Corporation, Rheem Manufacturing Company, Trane Inc. (Trane Technologies PLC), and Johnson Controls International PLC.

- March 2024: Carrier Corporation introduced an advanced, innovative line of high-performance chillers for data centers. These chillers are engineered to slash energy consumption and carbon footprints and lower operational expenses for data center operators. Ranging from 486.4 kW to 1,464 kW, these units leverage Carrier's trusted screw compressors, guaranteeing efficiency and longevity in operation.

- February 2024: Daikin Industries Ltd enhanced its air conditioners by focusing on critical elements. This includes shifting to HFC-32, an R32 refrigerant with low global warming potential, emphasizing its eco-friendliness and energy efficiency. Additionally, Daikin has bolstered the fundamental performance of its air conditioning units. In a significant move, Daikin is set to launch the VRV 7 multi-air conditioner series for buildings in November 2024. This series boasts the industry's top energy efficiency and is pivotal in lessening environmental footprints and operational burdens.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Replace Existing Equipment With Better Performance Equipment and Reinstate Tax Credits for Air Conditioning Equipment

- 5.1.2 Growing Adoption of Home and Building Automation Systems

- 5.2 Market Restraint

- 5.2.1 Stringent Regulatory Compliance and Safety Standards

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Unitary Air Conditioners

- 6.1.1.1 Ducted Splits

- 6.1.1.2 Ductless Mini-splits

- 6.1.1.3 Indoor Packaged and Roof Tops

- 6.1.2 Room Air Conditioners

- 6.1.3 Packaged Terminal Air Conditioners

- 6.1.4 Chillers

- 6.1.5 Variable Refrigerant Flow (VRF)

- 6.1.1 Unitary Air Conditioners

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Commercial and Industrial

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

- 6.4 By Efficiency

- 6.4.1 Low Efficiency (13 SEER)

- 6.4.2 High Efficiency (>13 SEER)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daikin Industries Ltd

- 7.1.2 Carrier Corporation

- 7.1.3 Rheem Manufacturing Company

- 7.1.4 Trane Inc. (Trane Technologies PLC)

- 7.1.5 Johnson Controls International PLC

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Lennox International Inc.

- 7.1.8 Systemair AB

- 7.1.9 Robert Bosch GmbH

- 7.1.10 Electrolux AB

- 7.1.11 LG Electronics Inc.

- 7.1.12 Midea Group

- 7.1.13 Schneider Electric SE

- 7.1.14 GE Appliances

- 7.1.15 Whirlpool Corporation

8 ANALYSIS OF COOLING EQUIPMENT DISTRIBUTION CHANNEL CENTRAL AIR CONDITIONING, ROOM AIR CONDITIONING

- 8.1 Direct

- 8.2 Retailers

- 8.3 Wholesalers/Dealers/Contractors