|

시장보고서

상품코드

1693392

프랑스의 실란트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)France Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

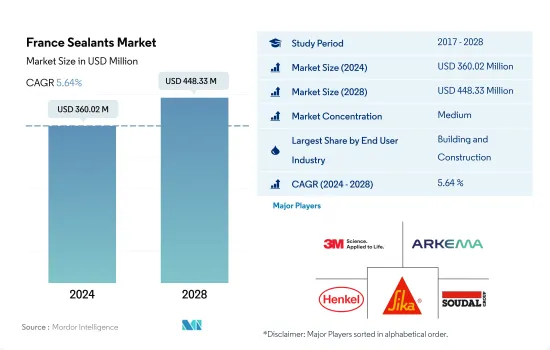

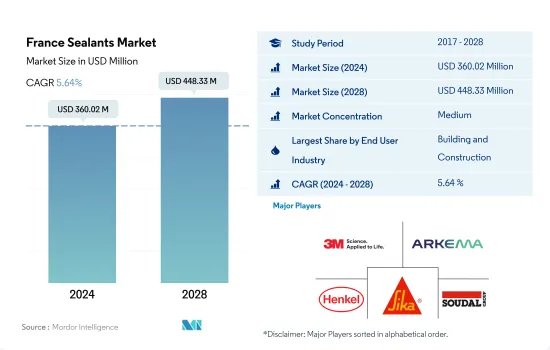

프랑스 실란트 시장 규모는 2024년 3억 6,002만 달러, 2028년에는 4억 4,833만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR 5.64%를 나타낼 것으로 예측됩니다.

주택건설 증가로 실란트 성장 촉진

- 프랑스 실란트 시장은 실란트의 방수, 내후성 실링, 균열 실링, 접합부 실링의 용도에 의해 주로 건설 업계가 견인하고 있습니다.

- 기타 최종 사용자 산업 부문은 전자 및 전기 기기 제조업에서의 포팅이나 보호재 등 다양한 용도에 의해 프랑스의 실란트 시장에서 2번째로 큰 점유율을 차지한다고 생각됩니다. 특히, 센서나 케이블의 씰에 사용되고 있습니다. 예측기간 중에도 실란트 수요를 창출할 것으로 예상됩니다.

- 실란트는 헬스케어와 자동차 산업에서 상당한 용도가 있으며, 프랑스는 수십 년에 걸쳐 이러한 분야에서 크게 발전해 왔습니다. 금속, 플라스틱, 도장면 등 다양한 기재에 실란트가 사용되고 있어 주로 엔진이나 자동차의 개스킷에 사용되고 있습니다. 이러한 요인에 의해 예측 기간중, 프랑스에 있어서의 실란트 수요는 증가할 것으로 예상됩니다.

프랑스 실란트 시장 동향

2024년 올림픽 개최가 프랑스 건설 부문을 뒷받침

- 프랑스는 유럽에서 2번째로 큰 건설산업국입니다.

- 2020년 건설 부문은 대폭적인 침체를 보였으며 총 건설생산량과 신규수주고는 크게 감소했습니다.

- 프랑스의 총 건설생산액은 2021년 4분기에 2020년 4분기 대비 0.2% 감소했으며, 전년 동기 대비 1.2% 감소했습니다.

- 그러나 프랑스 국내 총 건설업 생산량은 2022년 1분기에 2021년 1분기 대비 0.9% 증가했으며 전년 동기 대비 2.6% 증가했습니다. 같은 달 대비 1.5% 증가, 2022년 3월 대비 1.2% 증가했습니다.

- 따라서 위의 모든 요인은 조사된 시장에 영향을 미칠 것으로 예상됩니다.

2035년까지 자동차 배출량 넷 제로에 더해 전기차 등록 대수 증가가 자동차 생산을 촉진할 가능성이 높습니다.

- 프랑스 자동차 산업은 유럽의 다른 주요 국가에 비해 훨씬 호조입니다. 자동차 생산 대수는 2018년까지 지속적인 성장을 이뤘지만, 자동차 시장이 COVID-19 팬데믹의 악영향을 받았기 때문에 2019년에는 8.3% 감소를 보였습니다.

- 2020년 자동차 및 소형 상용차 생산량은 2019년 217만 5,350대에 비해 131만 6,371대로 39.5% 감소했습니다. 팬데믹에 따라 국내 각지의 제조 부문은 일시적인 운영 중단을 강요했습니다. 원재료 공급이 제한되어 있던 것도 자동차 부문이 직면한 과제에 박차를 가했습니다.

- 2021년에는 이 나라의 플러그인 전기자동차의 신규 등록 대수는 31만 5,000대를 넘어, 2020년 대비 62%의 성장률을 기록해, 프랑스에서의 전기자동차 부문 수요를 높였습니다. 이에 따라 2022년 3월 전기차 시장 점유율은 전년 동월 대비 16.1%에서 21.4%로 상승했습니다.

- 프랑스 자동차 산업은 2035년부터 내연 기관차의 생산을 금지하는 유럽 의회의 채결을 만장일치로 비난했습니다. 이 나라는 2035년까지 자동차 배출량 넷 제로를 달성할 계획이며, 예측 기간 동안 이 나라의 자동차 시장을 견인할 가능성이 높습니다.

프랑스의 실란트 산업 개요

프랑스의 실란트 시장은 중간 정도로 통합되어 상위 5개사에서 43.64%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. 3M, Arkema Group, Henkel AG & Co. KGaA, Sika AG, Soudal Holding NV(알파벳순)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 규제 프레임워크

- 프랑스

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 헬스케어

- 기타 최종 사용자 산업

- 수지

- 아크릴

- 에폭시

- 폴리우레탄

- 실리콘

- 기타 수지

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- 3M

- Arkema Group

- CERMIX

- Dow

- Henkel AG & Co. KGaA

- ISPO Group

- MAPEI SpA

- RPM International Inc.

- Sika AG

- Soudal Holding NV

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 접착제 및 실란트 산업의 개요

- 개요

- Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 성장 촉진요인, 저해요인, 기회

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The France Sealants Market size is estimated at 360.02 million USD in 2024, and is expected to reach 448.33 million USD by 2028, growing at a CAGR of 5.64% during the forecast period (2024-2028).

Growing construction in residential sector to foster the growth of sealants

- The French sealants market is driven mainly by the construction industry due to applications of sealants waterproofing, weather-sealing, crack-sealing, and joint-sealing. The construction industry of France surged by 10.5% in 2021 in volume, which increased the demand for sealants. The rapid growth of residential dwellings and maintenance of aged housing are expected to constantly foster the demand for sealants in France over the forecast period.

- The other end-user industries segment will likely account for the second-largest share in the French sealants market owing to the diverse applications in the electronics and electrical equipment manufacturing industry for potting and protecting materials. They are used for sealing sensors and cables, among others. The French electronics market has registered steady growth over the few years, and it is expected to continue, creating demand for sealants over the forecast period. The consumer electronics segment will likely register a CAGR of 1.39% up to 2027. In addition, the rising demand for sealants in the locomotive, marine, and DIY industries for sustainable and energy-efficient applications is expected to boost the market share over the forecast period.

- Sealants have considerable applications in the healthcare and automotive industries, and France has developed significantly in these sectors over the decades. They are used in healthcare primarily for assembling and sealing medical devices. The automotive sector also exhibits significant application of sealants to various substrates, such as glass, metal, plastic, and painted surfaces, and is mainly used in engines and car gaskets. These factors are expected to augment the demand for sealants in France over the forecast period.

France Sealants Market Trends

Hosting the 2024 Olympics is likely to boost the construction sector in the country

- France has the second-largest construction industry in the European region. The construction index in the country witnessed slow growth, with a gradual increase in the industry turnover index over the past few years. The construction industry in the country recently gained momentum after eight long years of decline.

- In 2020, the construction sector witnessed a huge decline, with the total construction output and new orders declining considerably. The growth of the French construction industry fell by over -12% due to the severe impact of the COVID-19 pandemic.

- The total construction production in France declined by 0.2% in Q4 2021 compared to Q4 2020 and by 1.2% compared to the previous quarter in the same year. In December 2021, the country's production from the construction industry declined by 2.6% compared to the same month in the previous year and declined by 7% compared to November 2021, decreasing the demand for the market.

- However, the total construction production in France increased by 0.9% in Q1 2022 compared to Q1 2021 and by 2.6% compared to the previous quarter of the same year. In April 2022, the country's production from the construction industry increased by 1.5% compared to the same month in the previous year and increased by 1.2% compared to March 2022. The recovery of the residential construction sector from the pandemic and the upcoming 2024 Olympics are estimated to drive the market during the forecast period.

- Therefore, all the abovementioned factors are expected to impact the market studied.

In addition to net-zero vehicle emissions by 2035, electric vehicle registrations growth is likely to propel the automotive production

- The automotive industry in France has fared much better compared to other major European economies. Automotive vehicle production experienced continuous growth till 2018 and further exhibited a decline of 8.3% in 2019, as the automotive market was negatively affected by the COVID-19 pandemic.

- In 2020, the country produced 1,316,371 cars and light commercial vehicles compared to 2,175,350 vehicles produced during 2019, recording a decline of 39.5%, as production came to a halt in 2020 due to the COVID-19 pandemic. The pandemic forced the temporary shutdown of manufacturing units across different parts of the country. Limited raw material supply added to the challenges faced by the automobile sector.

- In 2021, the country's new plug-ins electric vehicle registration stood at over 315,000, registering a growth rate of 62% compared to 2020, enhancing the demand of the electric vehicle segment in France. Along with it, electric vehicles registered a 21.4% market share in March 2022, up from 16.1% Y-o-Y.

- The French car industry has unanimously condemned the European Parliament's vote to ban the production of combustion engine cars from 2035. The country plans to achieve net-zero vehicle emissions by 2035, which is likely to drive the automotive vehicle market in the country over the forecast period.

France Sealants Industry Overview

The France Sealants Market is moderately consolidated, with the top five companies occupying 43.64%. The major players in this market are 3M, Arkema Group, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 France

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 CERMIX

- 6.4.4 Dow

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 ISPO Group

- 6.4.7 MAPEI S.p.A.

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms