|

시장보고서

상품코드

1693394

영국의 실란트 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United Kingdom Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

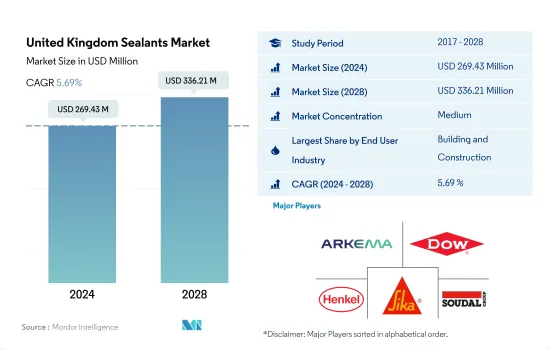

영국의 실란트 시장 규모는 2024년에 2억 6,943만 달러로 평가되었고, 2028년에는 3억 3,621만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR은 5.69%를 나타낼 전망입니다.

영국 일렉트로닉스 시장이 예측기간 실란트 수요 증가

- 영국의 실란트 시장은 방수, 내후성 실링, 균열 실링, 눈지 실링 등, 건축 및 건설 활동에 있어서의 실런트의 다양한 용도에 의해 건설 산업이 크게 견인해, 기타 최종사용자 산업이 그에 이어집니다. 2019년에 영국경제에 대한 부가가치 총액의 약 6%를 기록했습니다.

- 다른 최종 사용자 산업은 전자 및 전기 장비 제조 산업에서 포팅 및 보호 재료의 다양한 용도로 인해 영국 실란트 시장에서 두 번째로 큰 시장 점유율을 얻을 가능성이 높습니다. 수요를 증가시키는 것으로 예측됩니다. 또한, 전자상거래 활동의 급성장과 소비자 일렉트로닉스 부문의 강력한 시장 포지셔닝은 영국의 실란트 시장을 추진하고자 합니다.

- 실란트는 영국이 수십년에 걸쳐 큰 발전을 이루어 온 의료산업에 있어서 상당한 용도가 있습니다.

영국 실란트 시장 동향

정부의 주택과 인프라 투자 증가로 건설산업 활성화

- 영국은 유럽 최대의 건설 시장 중 하나입니다. 2020년 영국의 건설 시장은 COVID-19의 유행에 의해 19.5% 축소되었습니다. 이뤄진 신축 주택은 115,455호로 국내에서 COVID-19가 유행했기 때문에 전년 대비 23% 감소했습니다. House Building Council)은 2021년 신축 주택 등록 건수를 153,339건으로 발표하여 2020년 대비 25% 증가했습니다.

- 영국에서는 민간 부문의 등록 건수가 주요 견인역으로 되어 있으며, 등록 건수는 2020년의 80,475건에서 2021년에는 114,477건으로 40% 이상 증가했습니다. 임대 부문의 신축 주택 등록 건수는 주택 협회의 자본 예산이 기존 주택 재고의 건물 안전 보수 작업으로 전용되면서 2020년 42,460건에서 2021년 38,862건으로 8% 감소했습니다.

- 2021년의 연간 건설생산량은 팬데믹(세계적 대유행)에 의해 2020년이 매우 저조한 것을 요인으로 하여 2020년 대비 과거 최고의 12.7% 증가가 되었습니다. 금액은 2021년 3분기 대비 9.2% 증가(11억 2,100만 유로)했습니다.

- 전국에 더 나은 인프라를 국민에게 제공하기 위해 정부는 국가생산성 투자기금(NPIF)의 일환으로 2020-2050년에 걸쳐 GDP의 1-2%를 건설 인프라에 투자할 계획입니다.

2030년까지 친환경 운송 외에도 전기차 등록 대수 증가로 자동차 생산을 촉진할 높은 가능성

- 영국의 자동차 산업은 영국 경제에 필수적인 산업이며, 매출은 602억 유로를 넘어 영국 경제에 119억 유로의 부가가치를 가져오고 있습니다. 그러나 2020년 영국 자동차 산업이 COVID-19 팬데믹에의 대응이나 Brexit의 영향에 대비한 태세의 재건 등, 역사상 최대의 과제에 직면했기 때문에 영국의 자동차 생산 대수는 2019년 동기 대비 29.5% 감소했습니다.

- 2020년 29.5% 감소한 영국 자동차 생산은 반도체 부족이 생산에 심각한 영향을 미쳤기 때문에 2021년에는 4.7% 더 감소했습니다.

- 영국은 2030년까지 휘발유차와 디젤차를 단계적으로 폐지해 보다 친환경 수송으로의 이행을 촉진할 계획입니다.

- 영국에 있어서의 BEV, PHEV, HEV의 총 등록 대수는 2020년의 28만 5,199대에 대해, 2021년에는 45만 2,527대가 되어, 전년대비 58.7%의 성장률을 기록했습니다. BEV가 19만 727대(76.3%), PHEV가 11만 4,554대(70.6%), HEV가 14만 7,246대(34.0%)였습니다.

영국 실란트 산업 개요

영국 실란트 시장은 중간 정도로 통합되어 있으며 상위 5개 기업에서 41.26%를 차지하고 있습니다. Arkema Group, Dow, Henkel AG & Co.KGaA, Sika AG, Soudal Holding NV 등입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 규제 프레임워크

- 영국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 의료

- 기타

- 수지

- 아크릴

- 에폭시

- 폴리우레탄

- 실리콘

- 기타

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- 3M

- Adshead Ratcliffe & Co Ltd.

- Arkema Group

- Dow

- Henkel AG & Co. KGaA

- Hodgson Sealants

- MAPEI SpA

- RPM International Inc.

- Sika AG

- Soudal Holding NV

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 접착제 및 실란트 산업 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 성장 촉진요인, 억제요인, 기회

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The United Kingdom Sealants Market size is estimated at 269.43 million USD in 2024, and is expected to reach 336.21 million USD by 2028, growing at a CAGR of 5.69% during the forecast period (2024-2028).

United Kingdom's electronics market to augment the demand for sealants in the forecast period

- The UK sealants market is largely driven by the construction industry, followed by other end-user industries due to diverse applications of sealants in building and construction activities, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. The construction industry registered about 6% of gross value added to the economy of the United Kingdom in 2019. However, construction of new work for housing decreased by 20.7% in 2020 due to COVID-19 restrictions and scarcity of raw materials, which was restored in 2021, thus, increasing the sealants demand across the country.

- Other end-user industries will likely obtain the second largest market share in the UK sealants market owing to the diverse applications in the electronics and electrical equipment manufacturing industry for potting and protecting materials. The UK electronics market is expected to showcase an annual growth rate of 7.26% in the coming years, which will increase demand for sealants. Moreover, the rapid growth of e-commerce activities and the strong market positioning of the consumer electronics segment would like to propel the UK sealants market. In addition, sustainable growth of the locomotive, marine, and DIY industries would like to foster the demand for sealants in the United Kingdom during the forecast period.

- Sealants have considerable applications in the healthcare industry, in which the United Kingdom has achieved significant development over the decades. Sealants are used in healthcare mostly for assembling and sealing medical device parts. Increasing demand for electric vehicles due to favorable government policies and consumer preferences for lightweight vehicles will gradually influence the demand for sealants.

United Kingdom Sealants Market Trends

Rising investments in housing and infrastructure by the government to boost the construction industry

- The United Kingdom is one of the largest construction markets in Europe. In 2020, the UK construction market contracted by 19.5% due to the COVID pandemic. The number of new homes registered to be built in the United Kingdom declined by 23.2% in 2020, falling to 123,151 homes. There were 115,455 new homes completed, 23% down from the previous year because of COVID-19 in the country. However, in 2021, the construction market recovered and registered a growth rate of 4.7% compared to the same period in 2020. The National House Building Council (NHBC) announced 153,339 new home registrations in 2021, a 25% increase compared to 2020.

- Private sector registrations are the key driver in the United Kingdom, and registrations rose from 80,475 in 2020 to 114,477 in 2021, an increase of more than 40%. In contrast, new home registrations in the rental sector decreased by 8% from 42,460 in 2020 to 38,862 in 2021 due to the deflection of Housing Association capital budgets toward building safety remediation on existing housing stock.

- The annual construction output increased by a record 12.7% in 2021 compared to 2020, mainly due to the pandemic contributing to a very weak 2020. The total new orders for construction increased by 9.2% (EUR1,121 million) in Q4 2021 compared to Q3 2021. The total construction output (seasonally adjusted) grew by 2.0% (EUR 281 million) in December 2021 compared to November 2021.

- To provide better infrastructure to the population across the country, the government has planned to invest 1-2% of its GDP in construction and infrastructure between 2020 and 2050 as part of the National Productivity Investment Fund (NPIF). Therefore, all the abovementioned factors are likely to impact the market studied.

In addition to eco-friendly transportation by 2030, electric vehicle registrations growth is likely to propel the automotive production

- The UK automotive industry is a vital part of the UK economy, worth more than EUR 60.2 billion in turnover and adding EUR 11.9 billion value to the UK economy. However, in 2020, the automotive vehicle production in the country reduced by 29.5% compared to the same period in 2019, as the UK automotive sector faced some of the biggest challenges in its history while responding to the COVID-19 pandemic and repositioning for Brexit implications.

- After contracting by 29.5% in 2020, British automotive vehicle production further declined by 4.7% in 2021, as the semiconductor shortage severely affected production. New car registrations decreased 34% Y-o-Y in September 2021, which is excepted to affect the UK sealants market in the future.

- The United Kingdom is planning to phase out gasoline and diesel vehicles to promote the transition to more eco-friendly transportation by 2030. The country also planned an investment of over GBP 1.8 billion in infrastructure and grants to expand access to zero-emission vehicles and support a green economic recovery, thereby increasing the demand for the electric vehicles market in the country.

- The total number of BEV, PHEV, and HEV registrations in the United Kingdom accounted for 452,527 in 2021, registering a growth rate of 58.7% Y-o-Y, compared to 285,199 registrations in 2020. Out of total registrations in 2021 (with percentage Y-o-Y change), 190,727 (76.3%) were BEVs, 114,554 (70.6%) were PHEVs, and 147,246 (34.0%) were HEVs. In 2021, BEV, PHEV, and HEV captured around 27.5% share of total car registrations in the country.

United Kingdom Sealants Industry Overview

The United Kingdom Sealants Market is moderately consolidated, with the top five companies occupying 41.26%. The major players in this market are Arkema Group, Dow, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 United Kingdom

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Adshead Ratcliffe & Co Ltd.

- 6.4.3 Arkema Group

- 6.4.4 Dow

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Hodgson Sealants

- 6.4.7 MAPEI S.p.A.

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms