|

시장보고서

상품코드

1693562

영국의 항공 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)UK Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

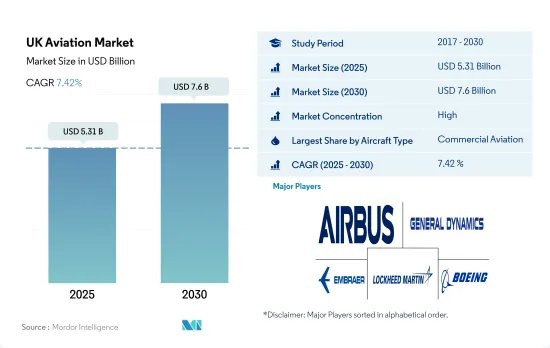

영국 항공 시장 규모는 2025년에 53억 1,000만 달러, 2030년에는 76억 달러에 이르고, 예측 기간(2025-2030년)의 CAGR은 7.42%를 나타낼 것으로 예측됩니다.

민간항공산업은 향후 대폭 성장할 전망

- 영국에서는 항공사와 그 공급망을 포함한 항공 산업의 GDP가 860억 달러에 달할 것으로 예측됩니다. 또한 해외 관광객의 소비로 인해 340억 달러가 추가되어 총 1,200억 달러가 영국의 GDP에 기여합니다. 항공 운송 산업에 대한 투자와 항공편으로 도착하는 외국인 관광객은 영국 GDP의 4.5%를 차지합니다.

- 일반항공산업은 영국에서 약 1만 2,000명을 고용하고 있습니다. 인가 파일럿은 1만명, 프라이빗 파일럿 라이선스(PPL)를 가지는 사람은 2만 8,000명 있습니다.

- 2022년 영국 군사예산은 685억 달러로, 3.7% 증가했습니다. 나토 회원국으로서 영국은 연간 GDP의 2%를 국방에 투자하기로 되어있습니다. 현재, 영국은 GDP의 2% 이상을 군사비에 충당하고 있습니다.

- 영국 항공사는 항공 여객율 상승에 따른 수요에 부응하고 노후화된 항공기를 연비가 좋은 모델로 대체하기 위해 새로운 항공기를 조달하고 있습니다.Virgin Atlantic 항공은 AirbusA330-900neo를 15기, A350-1,000을 5기 발주했습니다.

영국 항공 시장 동향

국내 여행을 하는 사람이 늘고 국내 여행자 수요가 증가

- 영국을 거점으로 하는 항공사는 2021년의 1억 8,964만명에 대해, 2022년에는 총 2억 635만명의 영국을 경유하는 항공 여객을 증가시켰습니다.

- 2022년 브리티시 에어웨이즈의 여객수는 1,166만명으로 영국을 거점으로 하는 항공사 중에서 가장 많았습니다. 전체적으로 2022년 미국 항공교통서비스(NATS)는 2020년 102만 8,254편과 같은 106만 2,945편을 관리했지만, 모두 250만편을 넘은 2019년의 편수를 대폭 밑돌았습니다.

- 우크라이나와 러시아의 전쟁으로 영국은 러시아 항공기에 대해 독자적인 상공비행 및 착륙금지조치를 강구했습니다. 이 제재는 영국 항공사들이 러시아 영공을 피하기 위해 비행 경로를 우회해야 한다는 것을 의미하며, 그 결과 비행 시간이 길어졌습니다.

- 비행 시간이 길어지면 연료 소비량이 늘어나고, 특정 노선에서는 운항 비용이 급증할 가능성이 있습니다. 노선 변경과 항공편 연장은 항공 승객들에게 불편을 가져오고, 비행이 완전히 취소되는 위험이 높아져, 여객의 신뢰를 저하시킬 가능성이 있습니다.

지정학적 위협 증가가 국방비 증가의 원동력

- NATO 회원국인 영국은 매년 GDP의 2%를 국방비로 지출하는 것을 약속하고 있습니다.

- 최근 발표된 2021-2031년 국방 장비 계획에 따르면 영국은 미래의 위협과 싸우기 위해 군사의 근대화를 계획하고 있습니다. 영국은 2021년부터 2022년까지 향후 10년간 장비 조달 및 지원에 3,210억 달러(2,380억 파운드)를 지출할 계획입니다.

- 해군 함대 확대를 목적으로 영국 해군은 432억 달러(381억 유로)의 지출을 계획하고 있습니다. 244억 달러(215억 유로)의 자금이 제공되었습니다.

영국 항공 산업 개요

영국 항공 시장은 상당히 통합되어 있으며 상위 5개 기업에서 88.21%를 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 항공 여객 수송량

- 항공화물 수송량

- 국내총생산

- 수입 여객 킬로(rpk)

- 인플레이션율

- 액티브 플릿 데이터

- 국방 지출

- 개인 부유층(hnwi)

- 규제 프레임워크

- 밸류체인 분석

제5장 시장 세분화

- 항공기 유형

- 민간 항공기

- 서브 항공기 유형별

- 화물기

- 여객기

- 바디 유형별

- 협폭동체 항공기

- 와이드 바디 기계

- 일반 여객기

- 서브 항공기 유형별

- 비즈니스 제트

- 바디 유형별

- 대형 제트기

- 소형 제트기

- 중형 제트기

- 피스톤 고정익기

- 기타

- 군용기

- 서브 항공기 유형별

- 고정익기

- 바디 유형별

- 다용도 항공기

- 훈련용 항공기

- 수송기

- 기타

- 회전익기

- 바디 유형별

- 멀티미션 헬리콥터

- 수송용 헬리콥터

- 기타

- 민간 항공기

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Airbus SE

- Bombardier Inc.

- Cirrus Design Corporation

- Embraer

- Leonardo SpA

- Lockheed Martin Corporation

- MD Helicopters LLC

- Robinson Helicopter Company Inc.

- Textron Inc.

- The Boeing Company

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The UK Aviation Market size is estimated at 5.31 billion USD in 2025, and is expected to reach 7.6 billion USD by 2030, growing at a CAGR of 7.42% during the forecast period (2025-2030).

The commercial aviation industry is expected to experience substantial growth in the future

- In the United Kingdom, the GDP of the aviation industry, including airlines and their supply chains, is projected to be USD 86 billion. An additional USD 34 billion, totaling USD 120 billion of the country's GDP, is supported by international visitor spending. The inputs to the air transport industry and foreign visitors who arrive by air contribute 4.5% to the country's GDP.

- General aviation employs around 12,000 people in the United Kingdom. About 96% of the 21,000 civilian aircraft registered in the United Kingdom are used for general aviation, and the GA fleet logs between 1.25 million and 1.35 million hours of flight time yearly. There are 10,000 certified glider pilots and 28,000 people with Private Pilot Licenses (PPL). The use of more accessible aircraft, such as microlights, locally built airplanes, and smaller helicopters, saw a rise in the past 20 years.

- The country's military budget for 2022 was USD 68.5 billion, a rise of 3.7%. Out of the total government spending, the country has allocated 2.2% of its share to the military. Its NATO membership commits the United Kingdom to devote 2% of its annual GDP to defense. Currently, the United Kingdom dedicates more than 2% of its GDP to the military. The country is buying new-generation aircraft to improve its aviation capabilities, thus resulting in increased military spending.

- UK airlines are procuring new aircraft to cater to the demand generated by the rising rates of air travel and to replace aging aircraft with fuel-efficient models. Easyjet has ordered 128 A320neo and 33 A321neo models. Virgin Atlantic has ordered 15 Airbus A330-900neo and five A350-1000 aircraft. British Airways ordered 40 aircraft, comprising five A320neo and nine Boeing 787-10 aircraft.

UK Aviation Market Trends

More people are traveling domestically now, leading to an increase in demand from domestic travelers

- The UK-based airlines were responsible for uplifting a total of 206.35 million air passengers who traveled through the UK in 2022, compared to 189.64 million in 2021. The growth between 2022 and 2021 was 8.8%, and the growth between 2022 and 2020 was 566%.

- In 2022, British Airways handled 11.66 million passengers, the most among all UK-based airlines. It was followed by EasyJet, which handled about 11.4 million passengers. Overall, in 2022, National Air Traffic Services (NATS) managed 1,062,945 flights, similar to the 1,028,254 flights in 2020, both significantly less than 2019 flight numbers, which were more than 2.5 million. The UK's recovery has lagged in Europe, primarily due to government restrictions and European restrictions on UK travel.

- The war between Ukraine and Russia resulted in the UK imposing its own overflight and landing ban on Russian aircraft. The sanctions mean that UK airlines will have to divert flight routes to avoid Russian airspace, resulting in longer flight times. For instance, Virgin Atlantic announced that avoiding Russian airspace will add up to an hour to its flights between the UK, Pakistan, and India.

- Longer flights will cause an increase in fuel consumption and can result in a sharp increase in operating costs for certain routes. The increasing fuel costs will particularly impact airlines, thus resulting in increased costs to passengers through higher ticket prices. Re-routing and longer flights may also cause inconvenience for air passengers, with an increased risk of flights being canceled completely and may decrease passenger confidence. The unpredictability of the situation in Ukraine is likely to be a major challenge for UK airlines and further delay the recovery in air passenger numbers.

Rising geopolitical threats are the driving factor for rising defense expenditure

- As a member of NATO, the United Kingdom is committed to spending 2% of its GDP on defense each year. The country's military budget for 2022 was USD 68.5 billion, a rise of 3.7%. Out of the total government spending, the country has allocated 2.2% of its share to the military. At present, the United Kingdom spends more than 2% of its gross domestic product (GDP) on military expenses.

- According to the recently published Defense Equipment Plan for 2021-2031, the United Kingdom plans to modernize its armed forces to combat future threats. The nation plans to spend USD 321 billion (GBP 238 billion) on equipment procurement and support over the next 10 years, starting from 2021 to 2022. The Army Command allocated USD 55.7 billion (GBP 41.3 billion) to aircraft procurement, including an allocation for AH-64 Apache attack helicopters.

- For the purpose of expanding the naval fleet, the British Navy plans to spend USD 43.2 billion (EUR 38.1 billion). Fundings of USD 39.7 billion (EUR 35 billion), USD 58.8 billion (EUR 58.1 billion), and USD 24.4 billion (EUR 21.5 billion) were provided to the UK Strategic Command, the Defence Nuclear Organization, and the Strategic and Combat Air Program, respectively. The UK Ministry of Defence also announced its plans to procure additional F-35s and A400M aircraft in the coming years. The Air Command plans to retire equipment that is becoming increasingly obsolete in the digital and future operational environments.

UK Aviation Industry Overview

The UK Aviation Market is fairly consolidated, with the top five companies occupying 88.21%. The major players in this market are Airbus SE, Bombardier Inc., Embraer, Lockheed Martin Corporation and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-net-worth Individual (hnwi)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 By Sub Aircraft Type

- 5.1.1.1.1 Freighter Aircraft

- 5.1.1.1.2 Passenger Aircraft

- 5.1.1.1.2.1 By Body Type

- 5.1.1.1.2.1.1 Narrowbody Aircraft

- 5.1.1.1.2.1.2 Widebody Aircraft

- 5.1.2 General Aviation

- 5.1.2.1 By Sub Aircraft Type

- 5.1.2.1.1 Business Jets

- 5.1.2.1.1.1 By Body Type

- 5.1.2.1.1.1.1 Large Jet

- 5.1.2.1.1.1.2 Light Jet

- 5.1.2.1.1.1.3 Mid-Size Jet

- 5.1.2.1.2 Piston Fixed-Wing Aircraft

- 5.1.2.1.3 Others

- 5.1.3 Military Aviation

- 5.1.3.1 By Sub Aircraft Type

- 5.1.3.1.1 Fixed-Wing Aircraft

- 5.1.3.1.1.1 By Body Type

- 5.1.3.1.1.1.1 Multi-Role Aircraft

- 5.1.3.1.1.1.2 Training Aircraft

- 5.1.3.1.1.1.3 Transport Aircraft

- 5.1.3.1.1.1.4 Others

- 5.1.3.1.2 Rotorcraft

- 5.1.3.1.2.1 By Body Type

- 5.1.3.1.2.1.1 Multi-Mission Helicopter

- 5.1.3.1.2.1.2 Transport Helicopter

- 5.1.3.1.2.1.3 Others

- 5.1.1 Commercial Aviation

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Bombardier Inc.

- 6.4.3 Cirrus Design Corporation

- 6.4.4 Embraer

- 6.4.5 Leonardo S.p.A

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 MD Helicopters LLC

- 6.4.8 Robinson Helicopter Company Inc.

- 6.4.9 Textron Inc.

- 6.4.10 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms