|

시장보고서

상품코드

1693632

유럽의 중형 및 대형 상용차 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Medium and Heavy-duty Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

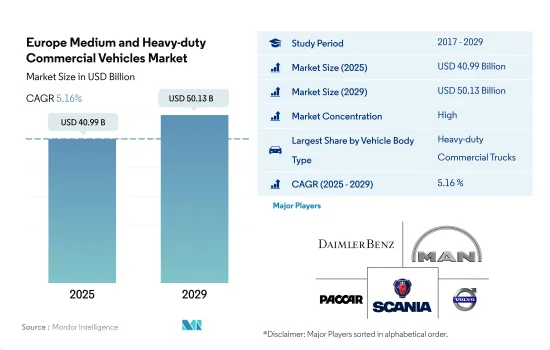

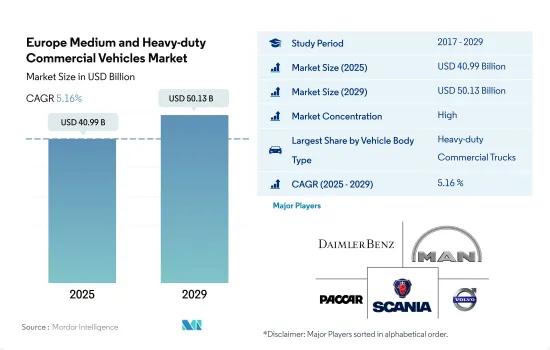

유럽의 중형 및 대형 상용차 시장 규모는 2025년에 409억 9,000만 달러로 추계되고, 2029년에는 501억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2029년)의 CAGR은 5.16%를 나타낼 것으로 예측됩니다.

유럽의 상업용 운송 환경에서 중형 및 대형 차량의 전략적 중요성으로 인해 기업들은 효율성과 규정 준수에 집중하고 있습니다.

- 운송은 유럽 경제를 강화하고 성장을 촉진하며 경쟁력을 강화하는 데 중추적인 역할을 합니다. 상용차 부문은 파리 협정에 명시된 기후 목표에 적극적으로 부응하고 있습니다. 대체 연료와 파워트레인의 도입이 주목을 받고 있지만, 상용차를 위한 충전 및 주유 인프라의 가용성은 여전히 제한적입니다. 630만 대 이상의 차량이 EU의 도로를 누비고 있으며, 연간 150억 톤의 엄청난 화물을 운송하면서 전체 육상 화물의 76.7%를 차지하고 있습니다.

- 유럽은 3월과 4월에 약 5만 대의 생산 손실이 발생하면서 코로나19의 영향을 가장 크게 받았습니다. 이는 주로 엄격한 공장 폐쇄, 직장 규제, 공급망 중단, 자택 대기 명령으로 인한 것이었습니다. 2020년 말까지 유럽의 상용차 생산량은 전년 대비 20% 가까이 급감했습니다.

- 물류 및 건설 활동의 성장은 자재 운송에 대한 수요를 촉진하여 유럽 전역의 상용차 판매량 급증으로 이어졌습니다. 이러한 추세는 가까운 미래에 비즈니스 차량 시장을 더욱 강화할 것으로 예상됩니다. 이 시장은 건설 및 전자상거래의 증가에 힘입어 성장세를 이어갈 것으로 보입니다.

유럽의 중형 및 대형 상용차 시장 동향

환경 문제, 정부 지원, 탈탄소화 목표가 유럽 전기자동차 수요와 판매를 촉진합니다.

- 유럽 국가의 전기차 수요와 판매량은 지난 몇 년 동안 크게 증가했습니다. 독일은 2021년 대비 2022년 전기차 판매량이 22% 증가했으며, 영국은 2021년 대비 2022년 18.40%의 증가율을 보였습니다. 환경에 대한 관심 증가, 엄격한 정부 규범, 연비, 낮은 유지비, 탄소 배출 없음, 정부의 보조금 등 전기자동차의 장점은 유럽 국가에서 전기자동차가 성장하는 데 기여하는 요인 중 일부입니다.

- 유럽 국가에서는 전기 상용차, 특히 경트럭에 대한 수요가 점차 증가하고 있습니다. 또한 여러 국가의 정부도 전기자동차 도입을 지원하고 있습니다. 2021년 11월, 영국 정부는 2040년까지 모든 대형 차량을 무공해 차량으로 만들겠다는 공약을 발표했습니다. 이러한 요인으로 인해 영국 내 전기 상용차 판매량은 2021년 대비 2022년에 23.17% 증가했으며, 여러 국가에서 유사한 정책이 시행되면서 유럽 전역에서 전기 상용차에 대한 수요가 증가하고 있습니다.

- 유럽 국가들의 차량 전기화는 향후 몇 년 동안 엄청난 성장을 이룰 것으로 예상됩니다. 탈탄소화를 위한 각국 정부의 노력이 유럽 내 전기 상용차 시장을 견인할 것으로 예상됩니다. 예를 들어, 2022년 1월 독일 교통부 장관은 2030년까지 1,500만 대의 전기차를 도로에 배치하겠다는 목표를 발표했습니다.

유럽의 중형 및 대형 상용차 산업의 개요

유럽의 중형 및 대형 상용차 시장은 상위 5개 기업이 87%를 점유하는 등 상당히 통합되어 있습니다. 이 시장의 주요 업체는 Daimler AG (Mercedes-Benz AG), Man Truck & Bus, PACCAR Inc., Scania AB, Volvo Group(알파벳 순 정렬)입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 인구

- 1인당 GDP

- 차량 구매를 위한 소비자 지출(CVP)

- 인플레이션율

- 자동차 대출 금리

- 전기화의 영향

- EV 충전소

- 배터리 팩 가격

- Xev 신모델 발표

- 물류성능지수

- 연료 가격

- OEM 생산 통계

- 규제 프레임워크

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 차량 부문

- 상용차

- 추진 부문

- 하이브리드 자동차와 전기자동차

- 연료 카테고리별

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 연료 카테고리별

- 천연가스

- 디젤

- 가솔린

- LPG

- 하이브리드 자동차와 전기자동차

- 국가명

- 오스트리아

- 벨기에

- 체코 공화국

- 덴마크

- 에스토니아

- 프랑스

- 독일

- 아일랜드

- 이탈리아

- 노르웨이

- 폴란드

- 러시아

- 스페인

- 스웨덴

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Daimler AG(Mercedes-Benz AG)

- Man Truck & Bus

- PACCAR Inc.

- Scania AB

- Volvo Group

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Medium and Heavy-duty Commercial Vehicles Market size is estimated at 40.99 billion USD in 2025, and is expected to reach 50.13 billion USD by 2029, growing at a CAGR of 5.16% during the forecast period (2025-2029).

Due to the strategic importance of medium and heavy-duty vehicles in Europe's commercial transport landscape, businesses are focusing on efficiency and regulatory compliance

- Transport plays a pivotal role in bolstering Europe's economy, fostering growth, and enhancing its competitiveness. The commercial vehicle sector is actively aligning with the climate goals outlined in the Paris Agreement. While the adoption of alternative fuels and powertrains is gaining traction, the availability of charging and refueling infrastructure for commercial vehicles remains limited. With over 6.3 million vehicles plying the roads of the EU, they account for a staggering 76.7% of all land-based freight, moving a colossal 15 billion tonnes annually.

- Europe bore the brunt of the COVID-19 impact, witnessing a production loss of approximately 50,000 units in March and April. This was primarily due to stringent factory closures, workplace regulations, supply chain disruptions, and stay-at-home orders. By the close of 2020, commercial vehicle manufacturing in Europe had plummeted by nearly 20% compared to the preceding year. Notably, countries like Poland in Central Europe and Italy in the West, pivotal hubs for the continent's trucking industry, are projected to witness the sharpest demand decline.

- The growth in logistics and construction activities has spurred the demand for material transportation, leading to a surge in commercial vehicle sales across Europe. This trend is expected to further bolster the business vehicle market in the near future. The market is poised for growth, driven by the uptick in construction and e-commerce operations. Additionally, the shift toward electric vehicles holds promising prospects for market expansion in the coming years.

Europe Medium and Heavy-duty Commercial Vehicles Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Medium and Heavy-duty Commercial Vehicles Industry Overview

The Europe Medium and Heavy-duty Commercial Vehicles Market is fairly consolidated, with the top five companies occupying 87%. The major players in this market are Daimler AG (Mercedes-Benz AG), Man Truck & Bus, PACCAR Inc., Scania AB and Volvo Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Norway

- 5.3.11 Poland

- 5.3.12 Russia

- 5.3.13 Spain

- 5.3.14 Sweden

- 5.3.15 UK

- 5.3.16 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Daimler AG (Mercedes-Benz AG)

- 6.4.2 Man Truck & Bus

- 6.4.3 PACCAR Inc.

- 6.4.4 Scania AB

- 6.4.5 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms