|

시장보고서

상품코드

1693673

중국의 원료의약품(API) 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)China Active Pharmaceutical Ingredients (API) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

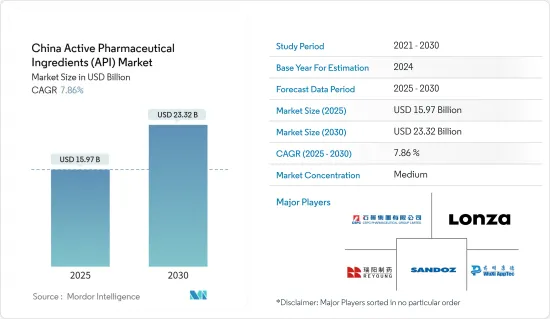

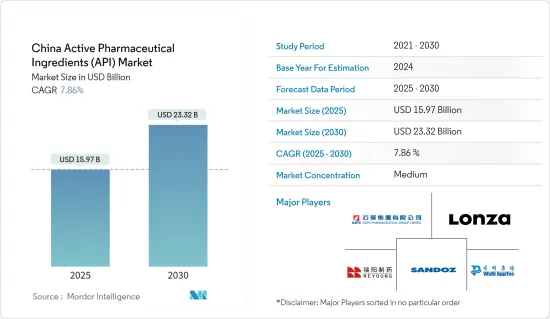

중국의 원료의약품 시장 규모는 2025년 159억 7,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 7.86%로 확대되어, 2030년에는 233억 2,000만 달러에 달할 것으로 예측됩니다.

이 시장은 만성 질환의 유병률 증가, 예측 기간 중의 생물 제제와 바이오시밀러의 채용 및 승인 증가에 의해 성장이 전망되고 있습니다.

중국에서는 만성질환, 감염증, 유전성질환의 유병률과 발병률이 증가하고 있어 효과적이고 안전한 의약품에 대한 수요가 높아지고 있습니다. 2022년 3월 Chinese Medical Journal에 게재된 기사에 따르면, 2022년에 중국에서 새롭게 암으로 진단된 환자수는 약 482만명으로, 전년은 450만명이었습니다. 이와 같이, 대장암을 포함한 암 환자수 증가가 예상되는 것으로부터, 치료용의 신규 약제 수요가 높아지면 이 것이, 예측 기간중의 API

또한 허혈성 심장 질환, 뇌졸중, 알츠하이머병 등의 치매, 만성 폐색성 폐질환은 국민의 장애조정 생존년수의 4대 원인이 되고 있습니다. 2023년 6월 BMC Public Health에 게재된 종이제에 따르면, 2050년까지 중국에 사는 약 4,000만명이 알츠하이머병과 관련된 치매에 시달릴 것으로 예상되고 있습니다.

게다가 생물제제와 바이오시밀러의 채용과 승인이 증가하고 있는 것도 예측기간 중 시장을 견인할 것으로 예측됩니다. 전문약품은 비용 절감이 큰 차이를 가져오는 현저한 부문 중 하나입니다. 왜냐하면 생물 제제의 비용이 높고 국가의 의약품 지출 전체에 불균형한 공헌을 하고 있기 때문입니다.

예를 들어 2023년 10월에 Health Policy 잡지에 게재된 기사에 따르면, 2022년 중국에서는 암 치료의 바이오시밀러의 비용은 기준약의 비용의 69%에서 90%이며, 그 보급률은 54%에서 83%에 이르렀습니다. 마찬가지로, 2022년 6월 Bioengineered 잡지에 게재된 기사에서, 중국의 연구자는 바이오시밀러 단클론항체는 중국에 있어서의 연구개발의 핫스팟의 하나이며, 지속적인 시책의 개선과 바이오시밀러의 연구개발에 대한 관심 증가가 있다고 관찰하고 있습니다.

이와 같이 바이오의약품 시장 개척으로 중국의 바이오시밀러 수요는 점차 확대될 것으로 예상되고 국가 가이드라인의 개선으로 다양한 만성질환과 감염증 치료에 대한 채용이 더욱 증가하고 시장 성장에 기여하고 있습니다.

따라서 만성질환의 유병률 증가, 생물제제와 바이오시밀러의 채용 및 승인 증가 등 앞서 언급한 요인에 따라 예측기간 중에 시장이 성장할 것으로 예측됩니다. 그러나 이 나라의 의약품 승인에 대한 엄격한 규제와 약가 시책이 예측 기간 동안 시장 성장을 방해할 것으로 예측됩니다.

중국의 원료의약품(API) 시장 동향

암 영역은 높은 연간 성장률이 예상된다.

암 환자의 부담 증가는 중국의 주요 의료 문제 중 하나입니다. 암의 이환율은 연령과 함께 극적으로 상승하지만, 이는 연령과 함께 증가하는 특정 암의 위험이 축적되기 때문이라고 생각됩니다. 따라서 암의 적절한 관리가 필요하며 첨단 의약품으로 가능합니다. 이와 같이 다양한 유형의 암을 관리하기 위한 첨단 의약품에 대한 요구 증가는 암 치료의 최종 제제를 제조하기 위한 원료의약품 수요에 박차를 가할 것으로 예측됩니다.

중국에서는 암 환자의 부담이 크기 때문에 암 치료용 혁신적인 의약품에 대한 수요가 높아지고 예측 기간 중에 산업 확대가 가속될 것으로 예측되고 있습니다. 예를 들어, 2023년 1월에 BMC Cancer에 게재된 종이제에 따르면, 중국에서는 지난 3년간 4,16,371건의 유방암 신규 환자가 발생하고 있습니다. 이와 같이 암의 유병률의 높이는 암 치료용 신약 수요를 촉진할 것으로 예상되며, 이 나라 시장 성장을 지원할 가능성이 높습니다.

게다가 이 나라에서는 노인이 증가하고 있으며, 노인층에서의 암의 부담이 높기 때문에 예측기간 중에 이 나라 시장 성장이 촉진될 것으로 예측되고 있습니다. 2022년 12월 Science China Life Sciences Journal이 발표한 기사에 따르면 중국에서는 고령자의 암 부담이 높아지고 있습니다. 이처럼 중국 인구에서 암 부담 증가는 암 관리를 위한 신규 약제 치료에 대한 왕성한 수요를 만들어 내고 산업의 확대에 박차를 가할 것으로 예측됩니다.

또한 다양한 암 치료 개발에 주력하는 기업이 증가하고 있는 것도 원료의약품 수요를 높여 시장의 성장을 뒷받침하고 있습니다. Glenmark Pharmaceuticals는 2024년 1월, 3D Medicines와 Jiangsu Alphamab Biopharmaceuticals와 제휴해, 각종 암의 치료 envafolimab를 발매했습니다.

따라서 이러한 계약은 예측 기간 동안 산업 확대에 박차를 가할 것으로 예측됩니다. 따라서 주요 기업에 의한 인수 및 제휴 등 전략적 활동 증가도 예측 기간 중 부문 수익을 끌어올릴 것으로 예측됩니다.

따라서 위의 요인으로부터 중국에서 암환자의 유병률 상승과 주요 기업에 의한 전략적 활동 증가가 예측기간 중 시장을 견인할 것으로 예측됩니다.

브랜드 의약품 부문이 큰 시장 점유율을 차지할 전망

브랜드 의약품은 일반적으로 특정 기간 동안 법적 특허 보호를 받은 혁신적인 의약품입니다. 의약품의 제제화에 필요한 원료의약품을 제조하기 위한 견고한 원료의약품 제조 시설에 의해 초래되고 있습니다.또한, 이 나라에서의 의약품 시장의 성장과 시장 진출기업에 의한 다양한 전략적 이니셔티브가, 예측 기간중의 부문 확대를 촉진할 것으로 예측되고 있습니다.

중국은 세계의 주요 의약품 시장 중 하나입니다. 따라서 대부분 시장 진출 기업은 비즈니스 기회를 강화하기 위해 중국과 국제 시장에서 제품을 출시하고 수출하고 있습니다. 이 나라에서 브랜드 의약품 제조를 위한 원료의약품 수요를 촉진할 것으로 예측되며, 이는 예측 기간 동안 부문 확대를 지원할 것으로 예측됩니다. Leqembi는 알츠하이머병의 치료에 사용되는 항체 기반의 치료입니다. 내부 시장 성장을 가속할 것으로 예측됩니다. 마찬가지로 세계 제약 회사의 중국 제약 시장에 대한 투자 의욕 증가는 새로운 치료법의 개발에 박차를 가할 것으로 예상되며, 그 결과 조사 기간 동안 같은 부문의 흡수를 촉진할 것으로 예측됩니다. AG와 RTW Investments, LP는 중국 Ji Xing Pharmaceuticals Limited에 3,500만 달러와 1억 2,700만 달러를 투자했습니다. 이와 같이, 이러한 투자는 브랜드 의약품의 개발에 큰 기대를 안겨, 나아가 원료의약품 수요를 촉진할 것으로 기대되고 있습니다.

이 부문은 또한 시장 각 회사가 의약품 의약품 생산 능력을 육성하기 위해 수행하는 여러 노력에서 혜택을 누릴 것으로 예측됩니다. 예를 들어, 2022년 9월, Asymchem은 중국 장쑤성 태흥시에 토지를 양도하고 화학 원료, 저분자 원료의약품, 의약품의 연구개발 및 생산시설을 건설하기로 합의했습니다. 이와 같은 사례는 이 나라에서의 의약품제약 생산능력이 강화될 것으로 예상되며, 예측기간 동안 동 부문 시장 성장에 박차가 걸릴 것으로 기대됩니다.

이와 같이 위의 요인, 브랜드 제품에 대한 수요 증가, 성장하는 의약 시장, 기업에 의한 몇 가지 전략적 이니셔티브는 예측 기간 동안 부문의 확대를 가속할 것으로 예측됩니다.

중국의 원료의약품(API) 산업 개요

중국의 의약품 원료 시장은 상대적으로 부문화되어 있습니다. API 시장에서는 여러 업체들이 제휴, 시설 확대, 의약품 승인 등 다양한 사업 전략을 채택하여 발자국 확대에 주력하고 있습니다. 주요 시장 진출기업으로는 CSPC Pharmaceutical Group Limited, WuXi AppTec(WuXi STA), Lonza 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 만성질환의 유병률 증가

- 생물제제와 바이오시밀러의 채용과 승인 증가

- 시장 성장 억제요인

- 약가 통제 시책

- 원료의약품 제조업체간의 높은 경쟁과 엄격한 규제

- 산업의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 비즈니스 모드별

- 캡티브 API

- 머챈트 API

- 합성 유형별

- 합성

- 바이오

- 의약품 유형별

- 제네릭

- 브랜드

- 용도별

- 순환기

- 종양학

- 호흡기 내과

- 신경학

- 정형외과

- 안과

- 기타

제6장 경쟁 구도

- 기업 프로파일

- Teva Pharmaceutical Industries Ltd

- Shenzhen Shengda Pharma Limited

- Jinzhou Pharmaceuticals

- WuXi AppTec

- Sandoz Group AG

- Pfizer Inc.

- Jinan Shengqi Pharmaceutical Co. Ltd

- Reyoung Pharmaceuticals

- Lonza

- CSPC Pharmaceutical Group Limited(Shijiazhuang Pharmaceutical Group Co. Ltd)

제7장 시장 기회와 앞으로의 동향

JHS 25.05.13The China Active Pharmaceutical Ingredients Market size is estimated at USD 15.97 billion in 2025, and is expected to reach USD 23.32 billion by 2030, at a CAGR of 7.86% during the forecast period (2025-2030).

The market is expected to grow due to the increasing prevalence of chronic disorders and the rising adoption and approval of biologics and biosimilars during the forecast period.

The increasing prevalence and incidence of chronic diseases, infectious diseases, and genetic disorders in China are driving the demand for effective and safe drugs. Thus, the need for active pharmaceutical ingredients across the country is increasing for the development of novel drugs for various diseases. This, in turn, is further expected to fuel the growth of the active pharmaceutical ingredients market during the forecast period. For instance, according to an article published in the Chinese Medical Journal in March 2022, it has been observed that about 4.82 million new cancer cases were diagnosed in China in 2022, compared to 4.5 million cases in the last year. Thus, the expected increase in the number of people who have cancer, including colorectal cancer, raises the demand for novel drugs for the treatment. This, in turn, is anticipated to propel the growth of the APIs market during the forecast period.

Also, ischemic heart disease, stroke, Alzheimer's and other dementias, and chronic obstructive pulmonary disease are the four most frequent causes of disability-adjusted life years among the population. For instance, according to an article published in BMC Public Health in June 2023, it was observed that about 40 million people living in China are expected to suffer from Alzheimer's disease and related dementias by 2050. Thus, the expected increase in the patient population raises the need to develop novel biological drugs, which is expected to increase the demand for APIs in China.

Moreover, the increasing adoption and approval of biologics and biosimilars are expected to drive the market during the forecast period. Healthcare systems worldwide actively seek ways to lower costs and raise revenues. Innovative formulary management provides a way to save prescription prices without sacrificing patient care. Specialty pharmaceuticals are one prominent area in which cost reductions would make a significant difference because of the high cost of biologics, which results in a disproportionate contribution to the total national drug spending. Thus, using less expensive biosimilars offers a chance to reduce drug costs and spending on biologics without compromising patient outcomes.

For instance, according to an article published in Health Policy in October 2023, it was observed that the cost of cancer biosimilars was 69% to 90% of the costs for the reference drugs, and their uptake reached 54% to 83% in China in 2022. Hence, biosimilars' lower cost and clinical benefits are expected to increase their adoption, ultimately driving the market during the forecast period. Similarly, in an article published in Bioengineered in June 2022, the Chinese researchers observed that biosimilar monoclonal antibodies are one of the hotspots of research and development in China, with continuous improvement of policies and increasing interest in research and development of biosimilars.

Thus, owing to the development of biopharmaceuticals markets, the demand for biosimilars in China is expected to grow gradually, with the improvement of the national guidelines, further increasing its adoption for the treatment of various chronic and infectious disorders, contributing to the market growth.

Therefore, the market is expected to grow during the forecast period due to the aforementioned factors, such as the increasing prevalence of chronic diseases and the increasing adoption and approval of biologics and biosimilars. However, the country's stringent regulations for drug approvals and drug price policies are expected to hinder market growth during the forecast period.

China Active Pharmaceutical Ingredients (API) Market Trends

The Oncology Segment is Expected to Register a High Annual Growth Rate

The growing burden of cancer cases is one of the primary healthcare concerns in China. The incidence of cancer rises dramatically with age, most likely due to a build-up of risks for specific cancers that increase with age. Hence, there should be proper management of cancer, which is possible with advanced medicines. Thus, the growing need for advanced medicines for the management of various types of cancers is projected to spur the demand for APIs to manufacture finished dosage forms of cancer medicine.

The significant burden of cancer cases in China is projected to foster demand for innovative medicines for cancer treatment, which is, in turn, projected to accelerate industry expansion during the forecast period. For instance, according to an article published in BMC Cancer in January 2023, there were 4,16,371 new cases of breast cancer in China over the last three years. Thus, the high prevalence of cancers is expected to drive the demand for new medicines for cancer treatment, which will likely support the country's market growth.

In addition, the increasing geriatric population in the country and a higher burden of cancer in the elderly population are projected to foster the country's market growth during the forecast period. For instance, according to an article published by the Science China Life Sciences Journal in December 2022, the burden of cancer among the geriatric population was higher in China. It is estimated that there were 2.79 million cases in older people, representing 55.8% of the overall population in 2022. Thus, the escalating burden of cancer among the Chinese population is anticipated to create a robust demand for novel drug therapies for cancer management, which, in turn, is projected to spur industry expansion.

Also, the rising company focus on developing various cancer-treating drugs raises the demand for APIs, propelling the market growth. For instance, in December 2023, AstraZeneca acquired Gracell, a Chinese cancer therapy firm, for USD 1.2 billion. The deal marks a further investment in cancer research and treatment in China, accounting for about one-third of AstraZeneca's business and its continued push to expand in China. Similarly, in January 2024, Glenmark Pharmaceuticals partnered with 3D Medicines and Jiangsu Alphamab Biopharmaceuticals to launch envafolimab to treat various types of cancers. Under this agreement, Jiangsu Alphamab is the manufacturer of envafolimab.

Thus, such agreements are projected to spur industry expansion during the forecast period. Hence, increasing strategic activities, such as acquisitions and collaborations by key players, are also expected to drive the segment revenue during the forecast period.

Therefore, owing to the above-mentioned factors, the rising prevalence of cancer cases in China and increasing strategic activities by key players are expected to drive the market during the forecast period.

The Branded Drugs Segment is Expected to Hold Significant Market Share

Branded drugs are usually innovative pharmaceuticals with legal patent protection for a specific period. When any investigational candidate fulfills all the research requirements, it is represented as a brand for a specific disease area. The segment growth is mainly driven by the increasing demand for branded medicines and robust API manufacturing facilities to manufacture the API required for the formulation of branded pharmaceuticals. In addition, the growing pharmaceutical market in the country and various strategic initiatives undertaken by market players are further projected to foster segment expansion during the forecast period.

China is one of the major pharmaceutical markets in the world. Hence, most market players launch and export their products in Chinese and international markets to strengthen their business avenues. Thus, various strategic initiatives undertaken by pharmaceutical companies, such as approvals, new launches, investments, and business expansions, are projected to foster demand for APIs to manufacture branded medicines in the country. This is projected to support segment expansion during the forecast period. For instance, in January 2024, Biogen and Eisai's Leqembi received approval from China's National Medical Products Administration. Leqembi is the antibody-based therapeutics used in the treatment of Alzheimer's disease. China has become the third country to approve Leqembi, following the United States and Japan. Thus, the approval of the new product is expected to propel the demand for Leqembi's API production in the country, which is expected to foster market growth during the forecast period. Similarly, the increased efforts of global pharmaceutical players to invest in the Chinese pharmaceutical market are expected to spur the development of novel therapies, which, in turn, are projected to fuel segment uptake over the study period. For instance, in January 2024, Bayer AG and RTW Investments, LP invested USD 35 million and 127 million in Ji Xing Pharmaceuticals Limited of China. This investment was made to accelerate the development of cardiovascular and ophthalmology medicines in China. In addition, this investment allowed Bayer AG to strengthen its presence in the Chinese market. Thus, such investments are expected to hold a strong promise for the development of branded medicines, which, in turn, is expected to foster the demand for APIs.

The segment is further expected to benefit from several efforts undertaken by market players to foster API production capabilities. For instance, in September 2022, Asymchem agreed to transfer land in Taixing, Jiangsu Province, China, to construct a proposed R&D and production facility for chemical raw materials, small-molecule APIs, and drug products. Thus, such instances are expected to strengthen API manufacturing capabilities in the country, which is expected to spur segment market growth during the forecast period.

Thus, the above-mentioned factors, increasing demand for branded products, growing pharmaceutical markets, and several strategic initiatives undertaken by companies are expected to accelerate segment expansion during the forecast period.

China Active Pharmaceutical Ingredients (API) Industry Overview

The Chinese active pharmaceutical ingredients market is relatively fragmented. The API market has several manufacturers focusing on expanding their footprints by adopting various business strategies, such as collaborations, facility expansion, and drug approvals. Some key market players include CSPC Pharmaceutical Group Limited (Shijiazhuang Pharmaceutical Group Co. Ltd), WuXi AppTec (WuXi STA), and Lonza.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Disorders

- 4.2.2 Increasing Adoption and Approval of Biologicals and Biosimilars

- 4.3 Market Restraints

- 4.3.1 Drug Price Control Policies

- 4.3.2 High Competition Between API Manufacturers and Stringent Regulations

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Business Mode

- 5.1.1 Captive API

- 5.1.2 Merchant API

- 5.2 By Synthesis Type

- 5.2.1 Synthetic

- 5.2.2 Biotech

- 5.3 By Drug Type

- 5.3.1 Generic

- 5.3.2 Branded

- 5.4 By Application

- 5.4.1 Cardiology

- 5.4.2 Oncology

- 5.4.3 Pulmonology

- 5.4.4 Neurology

- 5.4.5 Orthopedic

- 5.4.6 Ophthalmology

- 5.4.7 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Teva Pharmaceutical Industries Ltd

- 6.1.2 Shenzhen Shengda Pharma Limited

- 6.1.3 Jinzhou Pharmaceuticals

- 6.1.4 WuXi AppTec

- 6.1.5 Sandoz Group AG

- 6.1.6 Pfizer Inc.

- 6.1.7 Jinan Shengqi Pharmaceutical Co. Ltd

- 6.1.8 Reyoung Pharmaceuticals

- 6.1.9 Lonza

- 6.1.10 CSPC Pharmaceutical Group Limited (Shijiazhuang Pharmaceutical Group Co. Ltd)