|

시장보고서

상품코드

1693700

인도의 소프트웨어 서비스 수출 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)India Software Services Export - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

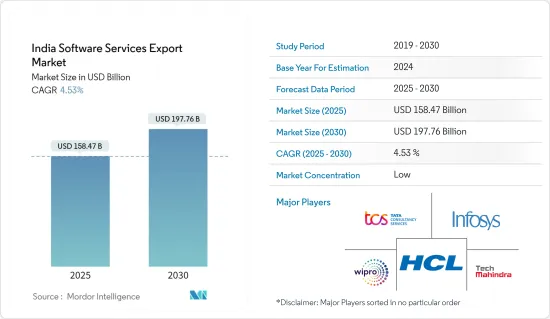

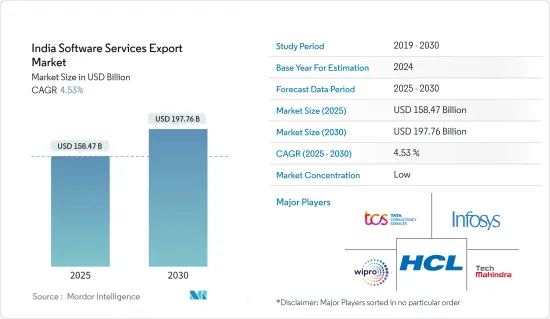

인도의 소프트웨어 서비스 수출 시장 규모는 2025년에 1,584억 7,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 4.53%로 확대되어, 2030년에는 1,977억 6,000만 달러에 달할 것으로 예측됩니다.

북미와 유럽 국가에서의 클라우드 변혁은 비용이 많이 들고 적절한 자원이 부족하기 때문에 오프쇼어링과 아웃소싱의 최전선에 있어 새로운 동향, 기술, 기술을 갱신하고 있는 인도가 선정되고 있습니다.

주요 하이라이트

- 산업 전체에서 디지털 전환이 급속히 진행되고, IoT, AI, 블록체인 등의 신기술이 채용되어, 비중핵 업무를 아웃소싱함으로써 코어 컴피턴스를 활용하는 것이 중시되게 되어 있는 것이, 시장의 주요 촉진요인이 되고 있습니다.

- 인도 기업이 디지털 변혁을 위해 클라우드, 인공지능(AI), 자동화, 네트워크 인프라, 사물인터넷(IoT), 기타 선진 기술에 기울이는 가운데, 디지털 전환(DX)과 IT의 근대화에 대한 지출은 인도 기업의 최우선 과제가 되고 있습니다.

- 클라우드 서비스로의 전환이 진행되고 있는 것은 조사 대상 시장의 중요한 촉진요인이며, 그 결과 거기에서 수익을 창출하는 중요한 협력 관계가 탄생하고 있습니다. 클라우드로의 마이그레이션을 통해 대기업과 중소기업 모두 소프트웨어 용도, 데이터베이스 및 기타 IT 리소스를 클라우드 서버로 마이그레이션하여 완벽하고 안전하며 투명한 시스템을 구현할 수 있습니다. 이를 통해 기업의 소프트웨어 개발 수명 주기 프로세스 관리가 더욱 효율적입니다. 기업은 일반적으로 더 나은 확장성, 가용성 및 소프트웨어 서비스의 신속한 배포를 위해 클라우드 마이그레이션 전략에 투자합니다.

- 소프트웨어 제품에 대한 인도 국가 시책은 소프트웨어 제품 생태계를 지원하기 위해 승인된 차세대 인큐베이션 체계(NGIS)에 의해 부분적으로 다루어지고 있습니다. 강력한 IT 섹터의 지속적인 확장, 새로운 고용 창출 및 경쟁 향상을 지원하기 위해 활발한 소프트웨어 제품 생태계를 구축할 계획입니다. NASSCOM의 견적에 따르면 인도의 소프트웨어 제품 산업은 2023년 매출에서 역사적인 성과를 올리고 142억 달러에 달했습니다.

- 그러나 규제 및 컴플라이언스 요구 관리와 같은 요인은 예측 기간 동안 시장 성장을 억제할 수 있습니다. 이는 운영 비용 증가, 엄격한 데이터 보호법에 의한 서비스 제공의 제한, 변화하고 진화하는 규제에 대한 끊임없는 적응의 필요성에 의한 혁신과 확대 노력으로부터의 자원의 유용을 수반하기 때문입니다.

- 게다가 COVID-19의 유행 이후 일부 기업은 직원들이 재택근무를 하게 되어 효율적인 IT 시스템을 도입할 필요성이 크게 높아지고 있습니다. 애플리케이션 및 소프트웨어를 클라우드 및 클라우드 기반 플랫폼으로 마이그레이션하는 조직도 증가하고 있습니다. 이러한 상황은 조사 대상 시장의 성장 기회를 크게 증가시키고 있습니다.

인도의 소프트웨어 서비스 수출 시장 동향

인프라 현대화, 디지털 지원, 클라우드 서비스에 대한 수요 증가

- 인프라의 현대화에는 성능, 확장성 및 보안 향상을 목표로 하는 조직의 IT 설정 강화가 포함됩니다. 주요 목적은 민첩성을 높이고 운영 비용을 줄이고 디지털 변환을 촉진하고 기업이 기술 동향과 고객 요구를 선점할 수 있도록하는 것입니다.

- 사이버 보안, 운영 효율성 및 비용 효율성에 중점을 둔 경향은 인프라의 현대화를 뒷받침하고 있습니다.

- 인도는 선진시장 경제국가로의 전환을 추진하고 있으며, 선진기술의 도입은 이 과정에서 중요한 역할을 할 것으로 기대되고 있습니다. Vi Business(Vodafone Idea의 산하)의 최근 조사에 따르면, 약 1,000사의 MSME는 다양한 업종에 걸쳐 디지털화를 받아들이고 있는 기업은 60% 이하라고 응답하고 있습니다.

- 전자정보기술부(Ministry of Electronics and Information Technology)에 따르면 인도의 IT/ITeS 산업은 세계적으로 중요한 지위를 차지하고 있으며 수출과 고용 창출을 크게 촉진하고 있습니다. IT-ITeS 산업은 고용을 대폭 강화해, 약 543만명의 전문가를 고용할 것으로 예상되고 있습니다.

- 시장 관계자는 기업의 디지털 전환 IT 전략을 구축하는 데 도움을 줍니다.

IT 서비스가 큰 시장 점유율을 획득할 전망

- 많은 국가들은 인건비를 절약하기 위해 IT 업무를 인도와 같은 신흥 경제 국가에 수출해 왔습니다. 인도는 IT 컨설팅과 구현 서비스에 대한 수요가 발생하고 있습니다.

- 인도의 IT 서비스 상황은 급속히 변화하고 있습니다. 다양한 최종 사용자 산업에서의 빅 데이터나 머신러닝과 같은 첨단 기술의 보급은 IT 인프라의 갱신의 필요성을 부추기고 있습니다. 클라우드 기반 플랫폼에서의 IT 운영의 진보로 IT 서비스는 보다 데이터 주도로 실시간으로 되어, 특히 업무 효율화, 비즈니스 기회의 발견, 원격 액세스의 최적화 등, 비즈니스에 큰 가치를 창출하고 있습니다.

- 게다가 클라우드 컴퓨팅은 기업, 정부, 소비자를 변화시키는 기술로 가정됩니다. 국제무역국에 따르면 ICT 섹터와 디지털 경제는 함께 인도의 GDP의 13% 이상을 차지하며 매우 중요한 경제의 기둥이 되고 있습니다.

- 또한 IT 서비스 제공업체는 다양한 최종 사용자 기업과 파트너십을 맺고 첨단 기술의 도입을 지원하고 있습니다. 진적 기술과 전문 지식을 이용할 수 있게 되어, 손해 보험 산업에 있어서의 지위가 강화되었습니다.

- 게다가 가입자 수가 증가함에 따라 CRM, 과금, 네트워크 관리 시스템 등 전기 통신에 특화된 소프트웨어 솔루션 수요가 높아지고, 시장의 성장을 크게 뒷받침하고 있습니다. 이와 같은 전기통신의 확대와 소프트웨어 수요의 시너지 효과가 시장의 성장을 크게 촉진하고 있습니다. 2023년 12월 현재, 인도 델리에서의 도시의 전기통신 가입자는 5,800만명을 넘고 있어, 측정 기간중의 인도 전토의 도시 전기통신 가입자 총수는 6억 6,200만명을 넘고 있습니다.

인도의 소프트웨어 서비스 수출 산업 개요

인도의 소프트웨어 서비스 수출 산업 시장은 세분화되어 있으며 Tata Consultancy Services Limited, Infosys Limited, Wipro Limited, HCL Technologies, Tech Mahindra Ltd 등이 주요 기업입니다.

- 2024년 4월: HCL Tech는 Google Cloud와의 제휴를 발표하고, 산업 솔루션을 확립하고, 멀티모달 대규모 언어 AI 모델인 Gemini를 배포합니다.

- 2024년 2월: 기술 서비스와 컨설팅 회사인 Wipro Limited는 Wipro Enterprise Artificial Intelligence (AI)-Ready Platform을 시작하여 고객이 엔터프라이즈 수준의 완벽하게 통합되어 맞춤형 AI 환경을 구축할 수 있도록 했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 거시 경제 동향이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 유행 문제에 따른 인프라 현대화, 디지털 지원, 클라우드 서비스에 대한 수요 증가

- 컴플라이언스 삭감, 생산성 향상, 국제 경쟁 강화를 실현한 IT 산업을 지원하는 정부 개혁

- 시장 성장 억제요인

- 세계 각지의 규제와 컴플라이언스·니즈의 관리

- 소프트웨어 서비스의 동향과 기술 개발

- 지역 분석

- 카르나타카주

- 타밀나두주

- 테랑가나주

- 마하라슈트라주

- 우타르 프라데시주

- 할리야나주

제6장 시장 세분화

- 활동별

- IT서비스

- 소프트웨어 제품 개발

- BPO 서비스

- 엔지니어링 서비스

- 서비스 유형별

- 현장

- 오프사이트

- 수출처별

- 북미

- 유럽

- 아시아태평양

- 기타

제7장 경쟁 구도

- 기업 프로파일

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- HCL Technologies

- Tech Mahindra Ltd

- Mphasis Limited

- Oracle Corporation

- LTIMindtree Limited

- Microsoft Corporation

- Capgemini Technology Services India Ltd

- IBM Corporation

- Accenture PLC

- Deloitte Touche Tohmatsu Limited

- PWC LLP

제8장 캡처 기업 목록

제9장 자문 회사 목록

제10장 투자 분석

제11장 시장의 미래

JHS 25.05.13The India Software Services Export Market size is estimated at USD 158.47 billion in 2025, and is expected to reach USD 197.76 billion by 2030, at a CAGR of 4.53% during the forecast period (2025-2030).

As the cloud transformation in the North American and European nations involves high costs and lacks proper resources, India is preferred as it is at the forefront of offshoring and outsourcing and is updated with emerging trends, techniques, and technology. This factor is expected to contribute to the market's expansion during the forecast period.

Key Highlights

- Rapidly increasing digital transformation across industries, adoption of new technologies such as IoT, AI, and blockchain, and a growing emphasis on leveraging the core competencies by outsourcing non-core operations are the major driving factors of the market.

- As Indian organizations gravitate toward the cloud, artificial intelligence (AI), automation, network infrastructure, Internet of Things (IoT), and other developed technologies to transform them digitally, spending on digital transformation (DX) and IT modernization are the top priorities of Indian companies.

- The growing migration to cloud services is a crucial driving factor in the market studied, resulting in significant collaborations generating revenue from it. Cloud migration facilitates both large and small businesses to move their software applications, databases, and other IT resources to cloud servers for seamless, secure, and transparent systems. This allows the company's software development lifecycle process management to be more efficient. Businesses generally invest in cloud migration strategies for better scalability, availability, and quicker deployment of software services.

- The Indian National Policy on Software Products has been addressed partly by the Next Generation Incubation Scheme (NGIS), which has been approved to support the software product ecosystem. It is planned to build a thriving software product ecosystem to support the strong IT sector's sustained expansion, new job creation, and competitiveness improvement. As per NASSCOM estimate, the Indian Software Product industry has made historic achievements in revenue in FY 2023, reaching USD 14.2 billion.

- However, factors like managing regulatory and compliance needs can restrain the market's growth during the forecast period. It is because this involves increasing operational costs, limiting service offerings due to stringent data protection laws, and diverting resources from innovation and expansion efforts due to the constant need to adapt to varying and evolving regulations.

- Furthermore, after the COVID-19 pandemic, several businesses have employees working from home, and the need to adopt efficient IT systems has increased substantially. Organizations have increasingly migrated to the cloud or cloud-based platforms for their applications and software. This situation has significantly augmented the growth opportunities for the market studied.

India Software Services Export Market Trends

Increasing Demand for Infrastructure Modernization, Digital Support, and Cloud Services

- Infrastructure modernization involves enhancing an organization's IT setup for better performance, scalability, and security. This encompasses transitioning from older systems to cloud-based platforms, embracing containerization, and integrating automation and DevOps methodologies. The primary goal is to boost agility, cut operational expenses, and facilitate digital transformation, empowering businesses to stay ahead of tech trends and customer needs.

- The increasing emphasis on cybersecurity, operational efficiency, and cost-effectiveness is driving the push for infrastructure modernization. These enhancements empower Indian software service providers to not only meet the evolving demands of global clients but also to stay competitive in the international market by delivering high-quality, innovative, and secure solutions.

- India is on a journey to transition into a developed market economy and advanced technology deployment, which is expected to play a significant part in this process. Moreover, India's Finance Minister has emphasized India's digital infrastructure in driving economic formalization in the modern era in the country's interim budget. According to a recent survey by Vi Business (the Arm of Vodafone Idea), nearly one lakh MSMEs said that less than 60% of businesses had embraced digitalization across various verticals.

- As per the Ministry of Electronics and Information Technology, India's IT/ITeS industry holds a significant global position, significantly bolstering exports and job creation. The nation's IT-BPM sector (excluding e-commerce) is poised to hit a valuation of USD 254 billion, with exports making up approximately USD 200 billion in the fiscal year 2023-24 (estimated). The IT-ITeS industry has also significantly bolstered employment and is anticipated to employ a total workforce of around 5.43 million professionals. This marks an increase of 60,000 individuals from the previous fiscal year (FY 2022-2023). Notably, women constitute 36% of the industry's workforce.

- The market players are helping companies build their digital transformation IT strategies. For instance, in March 2024, Tata Consultancy Services declared the multimillion-dollar strategic partnership to support the end-to-end IT transformation of Ramboll, an architecture, engineering, and consultancy company headquartered in Denmark. The company would modernize and streamline Ramboll's IT operating model to strive for business growth in IT over the next seven years.

IT Services Expected to Capture Significant Market Share

- Many countries have long exported IT work to developing economies like India to save on labor costs. With the country housing many major IT service export players, the demand for IT services export is expected to gain significant momentum in India in the coming years. In the wake of digital transformation worldwide, companies are rapidly upgrading their legacy IT infrastructure, thus creating demand for IT consulting and implementation services in India. Digital transformation provides companies with a strategic and competitive advantage in terms of determining IT services and their importance, further organizes the IT services as an activity of a plan-build-run framework, and defines the IT service strategy for the organization.

- The landscape of IT services in India is changing rapidly. The proliferation of advanced technologies, like big data and machine learning in various end-user industries, fuels the need for updated IT infrastructure. In addition, this adoption of emerging technologies enables businesses to replace outdated infrastructure and hardware, driving the IT services segment's growth in India. Moreover, due to advancements in IT operation across the cloud-based platform, IT services have become more data-driven and real-time, creating greater value for the business, especially in operational efficiency, business opportunity discovery, and remote access optimization. As per data by NASSCOM, the technology sector grew by USD 245 billion in India due to investments in advanced and modern digital infrastructure.

- Furthermore, cloud computing is envisioned as a transformative technology for enterprises, governments, and consumers. It not only supports digital transformation but also enables innovation and collaboration among the IT ecosystem players. According to the International Trade Administration, the ICT sector and the digital economy collectively account for over 13% of India's GDP, making them pivotal economic pillars. India has set an ambitious target, aiming to elevate the ICT sector to a USD 1 trillion valuation by 2025, representing a significant 20% of the projected GDP.

- In addition, IT service providers are indulging in partnerships with various end-user companies to assist them with advanced technology implementation. In February 2024, Wipro announced becoming a majority shareholder in Aggne. This move strengthens Wipro's position in the property and casualty (P&C) insurance industry by giving them access to Aggne's advanced technology and expertise. The integrated capabilities of Wipro and Aggne will help leverage technologies to deliver faster speed-to-market and more competitive services to clients in the P&C sector.

- Furthermore, the rising number of telecom subscribers is driving the market's growth significantly, as it increases the demand for telecom-specific software solutions, such as CRM, billing, and network management systems. Enhanced connectivity and communication capabilities boost remote collaboration and outsourcing opportunities, enabling software service providers to deliver their services globally. In addition, telecom advancements promote the development of innovative applications and digital services, expanding market opportunities for software exporters. This synergy between telecom expansion and software demand fuels the growth of the market significantly. According to TRAI, as of December 2023, there were over 58 million urban telecom subscribers in Delhi, India, and the total number of urban telecom subscribers across India during the measured time period was more than 662 million.

India Software Services Export Industry Overview

The Indian software services export industry market is fragmented. Tata Consultancy Services Limited, Infosys Limited, Wipro Limited, HCL Technologies, and Tech Mahindra Ltd are among the major companies. The corporations continue to innovate and form strategic partnerships to maintain their market share.

- April 2024: HCL Tech announced an alliance with Google Cloud to establish industry solutions and deploy Gemini for its multimodal large-language AI model. HCL planned to boost the HCL Tech AI Force platform with Gemini's advanced code completion and summarization capabilities, which allow engineers to code efficiently, solve issues, reduce delivery time, and enhance the quality of software projects for clients.

- February 2024: Wipro Limited, a technology services and consulting company, launched the Wipro Enterprise Artificial Intelligence (AI)-Ready Platform to help clients create enterprise-level, fully integrated, and customized AI environments. This platform provides the necessary infrastructure and core software for the consumption of AI and generative AI workloads for automation, dynamic resource management to adjust to varying workloads using predictive analytics dynamically, and investment in improvements in incident reduction and operational efficiency in the enterprise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Infrastructure Modernization, Digital Support, and Cloud Services Owing to Pandemic Challenges

- 5.1.2 Government Reforms Aiding IT Industry that has Reduced Compliance, Increased Productivity, and Increased Global Competitiveness

- 5.2 Market Restraints

- 5.2.1 Managing Regulatory and Compliance Needs Across the World

- 5.3 Trends and Technology Developments in Software Services

- 5.4 Regional Analysis

- 5.4.1 Karnataka

- 5.4.2 Tamil Nadu

- 5.4.3 Telangana

- 5.4.4 Maharashtra

- 5.4.5 Uttar Pradesh

- 5.4.6 Haryana

6 MARKET SEGMENTATION

- 6.1 By Activity

- 6.1.1 IT Services

- 6.1.2 Software Product Development

- 6.1.3 BPO Services

- 6.1.4 Engineering Services

- 6.2 By Services Type

- 6.2.1 On-site

- 6.2.2 Off-site

- 6.3 By Export Destination

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tata Consultancy Services Limited

- 7.1.2 Infosys Limited

- 7.1.3 Wipro Limited

- 7.1.4 HCL Technologies

- 7.1.5 Tech Mahindra Ltd

- 7.1.6 Mphasis Limited

- 7.1.7 Oracle Corporation

- 7.1.8 LTIMindtree Limited

- 7.1.9 Microsoft Corporation

- 7.1.10 Capgemini Technology Services India Ltd

- 7.1.11 IBM Corporation

- 7.1.12 Accenture PLC

- 7.1.13 Deloitte Touche Tohmatsu Limited

- 7.1.14 PWC LLP