|

시장보고서

상품코드

1693820

인도의 엔지니어링 플라스틱 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)India Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

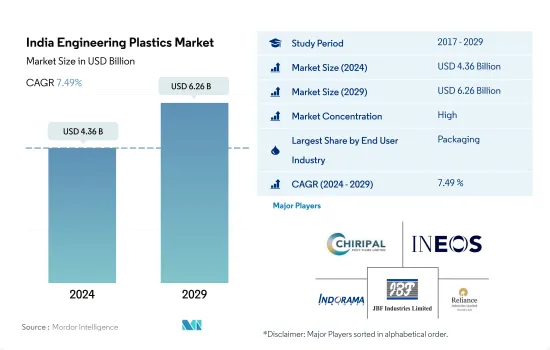

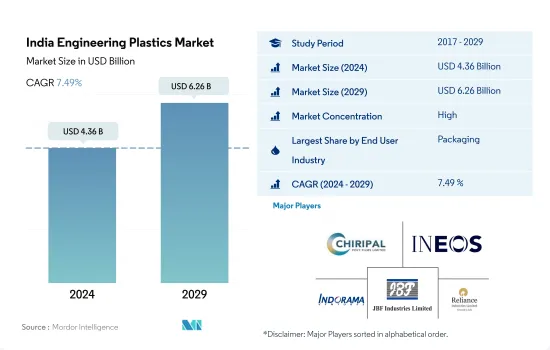

인도의 엔지니어링 플라스틱 시장 규모는 2024년에 43억 6,000만 달러에 달했고, 2029년에는 62억 6,000만 달러에 이르고, 예측 기간 중(2024-2029년)의 CAGR은 7.49%를 나타낼 것으로 예상됩니다.

예측기간 동안에도 포장산업이 우위를 유지

- 엔지니어링 플라스틱의 용도는 항공우주의 내장벽 패널이나 도어에서 경질포장과 연질포장에 이르기까지 폭넓습니다.

- 인도의 엔지니어링 플라스틱 시장에서는 포장이 최대의 점유율을 차지하고 있습니다. 인도의 포장 산업은 신제품을 발매할 때의 플라스틱 포장 수요에 의해 2급 도시에서 활발해지고 있습니다. 또한 주로 수지의 저비용과 유연성에 의해 성장이 촉진되어 환경에 대한 이산화탄소 배출량도 낮게 억제되고 있습니다.

- 전기 및 전자산업은 인도에서 가장 급속히 확대되고 있는 부문이며, 2021년 동국의 GDP에 약 3.4% 기여했습니다. 2022년 9월에 20억 907만 달러로 전년 동월 대비 71.99% 증가했습니다.

인도의 엔지니어링 플라스틱 시장 동향

정부의 규제 지원이 산업 성장에 중요한 역할

- 인도에서는 2020-2021년에 걸쳐 전기 및 전자기기 매출이 19.6% 증가했습니다. 2020-2021년에는 673억 달러로 증가했습니다.

- 인도의 전자제품 수출은 2022년 9월에 20억 907만 달러가 되어 전년대비 71.99% 증가했습니다. 전자 및 IT 부는 인도의 전자 산업 수출액이 2026년까지 1,200억 달러에 달할 것으로 예상하고 있습니다.

- 전자제품에 대한 요구가 높아짐에 따라 정부는 동국의 전자제품산업을 촉진하기 위해 생산연동형 장려금(PLI), 전자부품·반도체제조(SPECS), 개량형 전자제조 클러스터(EMC) 2.0) 등을 내세웠습니다. 렉트로닉스 부문은 인도의 비즈니스 프로세스 아웃소싱(BPO) 산업 시장 개척과 점유율 확대로 향후 3-5년 만에 인도 최고의 수출 부문 중 하나가 될 가능성을 갖고 있습니다.

인도의 엔지니어링 플라스틱 산업 개요

인도의 엔지니어링 플라스틱 시장은 상당히 통합되어 있으며 상위 5개 기업에서 85.39%를 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 포장

- 수출입 동향

- 가격 동향

- 재활용 개요

- 폴리아미드(PA) 재활용 동향

- 폴리카보네이트(PC) 재활용 동향

- 폴리에틸렌 테레프탈레이트(PET) 재활용 동향

- 스티렌 공중합체(ABS 및 SAN) 재활용 동향

- 규제 프레임워크

- 인도

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 산업 및 기계

- 포장

- 기타

- 수지 유형

- 불소수지

- 하위 수지 유형별

- 에틸렌테트라플루오로에틸렌(ETFE)

- 플루오르화 에틸렌-프로필렌(FEP)

- 폴리테트라플루오로에틸렌(PTFE)

- 폴리비닐플루오라이드(PVF)

- 폴리비닐리덴 플루오라이드(PVDF)

- 기타 하위 수지

- 액정 폴리머(LCP)

- 폴리아미드(PA)

- 하위 수지 유형별

- 아라미드

- 폴리아미드(PA) 6

- 폴리아미드(PA) 66

- 폴리프탈아미드

- 폴리부틸렌테레프탈레이트(PBT)

- 폴리카보네이트(PC)

- 폴리에테르에테르케톤(PEEK)

- 폴리에틸렌 테레프탈레이트(PET)

- 폴리이미드(PI)

- 폴리메틸메타크릴레이트(PMMA)

- 폴리옥시메틸렌(POM)

- 스티렌 공중합체(ABS 및 SAN)

- 불소수지

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Bhansali Engineering Polymers Limited

- Chiripal Poly Film

- DuPont

- Ester Industries Limited

- Gujarat Fluorochemicals Limited(GFL)

- Gujarat State Fertilizers & Chemicals Limited(GSFC)

- Hindustan Fluorocarbons Limited.

- INEOS

- IVL Dhunseri Petrochem Industries Private Limited(IDPIPL)

- JBF Industries Ltd

- LANXESS

- Mitsubishi Chemical Corporation

- Polyplex

- Reliance Industries Limited

- Solvay

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The India Engineering Plastics Market size is estimated at 4.36 billion USD in 2024, and is expected to reach 6.26 billion USD by 2029, growing at a CAGR of 7.49% during the forecast period (2024-2029).

Packaging industry to remain dominant during the forecast period

- Engineering plastics have applications ranging from interior wall panels and doors in aerospace to rigid and flexible packaging. The engineering plastics market in India is led by industries such as packaging, electrical and electronics, and automotive. Packaging and electrical and electronics accounted for the highest market revenue shares of 27.58% and 21.10%, respectively, in 2022.

- Packaging holds the largest share of India's engineering plastics market. The packaging industry in India is flourishing in second-tier cities due to the demand for plastic packaging in launching new products. Domestic and foreign firms are adopting strategies such as joint ventures and partnerships that positively impact market growth. The growth is also primarily driven by the low cost and flexibility of the resins, which also maintain a low-carbon footprint on the environment. India's plastic packaging production had a volume of 4.16 million tons in 2022 from 4 million tons in 2021, at a Y-o-Y growth of 3.97% by volume.

- The electrical and electronics industry is India's most rapidly expanding sector, with the electronics segment contributing approximately 3.4% to the country's GDP in 2021. The government has outlined a strategy to promote the electronics industry and increase its value to USD 17 billion through four PLI (production-linked incentive) schemes for smartphones, semiconductors, design, and IT software and hardware components over the next few years. India's export of electronic goods stood at USD 2,009.07 million in September 2022, with an increase of 71.99% Y-o-Y. These factors are expected to impetus the growth of engineering plastics in the electronics industry, registering a CAGR of 9.42%, by value, over the forecast period in India.

India Engineering Plastics Market Trends

Regulatory support by the government to play key role in industry growth

- India witnessed an increase in electrical and electronics revenue by 19.6% from 2020 to 2021. The electronics manufacturing industry's production grew from a value of USD 37.1 billion in 2015-16 to USD 67.3 billion in 2020-21. However, COVID-19-related disruptions impacted the growth trajectory in 2020-21 and led to a decline in output.

- India's export of electronic goods stood at USD 2,009.07 million in September 2022, an increase of 71.99% Y-o-Y. Mobile phones, IT hardware (laptops, tablets), consumer electronics (TV and audio), industrial electronics, and auto electronics are key export products in this sector. The Ministry of Electronics & IT estimates that India's electronics industry exports are expected to reach a value of USD 120 billion by 2026. The United States is the largest importer of India's electronic exports, followed by the United Arab Emirates, accounting for 18% and 17% of the overall exports, respectively. Mobile phone exports from India find significant markets in South Asia, Africa, and the Middle East, making them key importing regions for these products.

- With the growing need for electronic goods, the government launched production-linked incentives (PLI), Manufacturing of Electronic Components and Semiconductors (SPECS), Modified Electronic Manufacturing Clusters (EMC 2.0), etc., to promote the country's electronic goods industry. The country's electronics industry is expected to reach a value of USD 300 billion by 2025-26 from USD 75 billion in 2020-21. India's electronics sector has the potential to become one of the top exporting sectors of India in the next 3-5 years due to the development and increase in the market share of the Indian business process outsourcing (BPO) industry.

India Engineering Plastics Industry Overview

The India Engineering Plastics Market is fairly consolidated, with the top five companies occupying 85.39%. The major players in this market are Chiripal Poly Film, INEOS, IVL Dhunseri Petrochem Industries Private Limited (IDPIPL), JBF Industries Ltd and Reliance Industries Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 India

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Bhansali Engineering Polymers Limited

- 6.4.2 Chiripal Poly Film

- 6.4.3 DuPont

- 6.4.4 Ester Industries Limited

- 6.4.5 Gujarat Fluorochemicals Limited (GFL)

- 6.4.6 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 6.4.7 Hindustan Fluorocarbons Limited.

- 6.4.8 INEOS

- 6.4.9 IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- 6.4.10 JBF Industries Ltd

- 6.4.11 LANXESS

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Polyplex

- 6.4.14 Reliance Industries Limited

- 6.4.15 Solvay

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록