|

시장보고서

상품코드

1693936

유럽의 위성 자세 궤도 제어 시스템(AOCS) 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 성장 예측Europe Satellite Attitude and Orbit Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

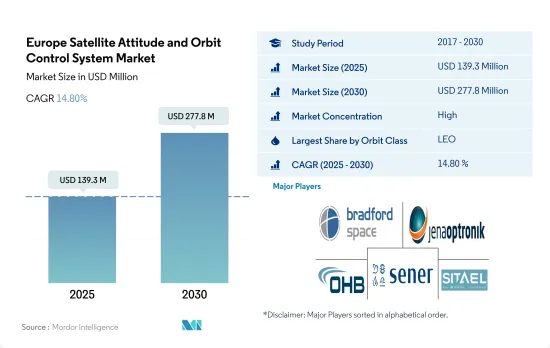

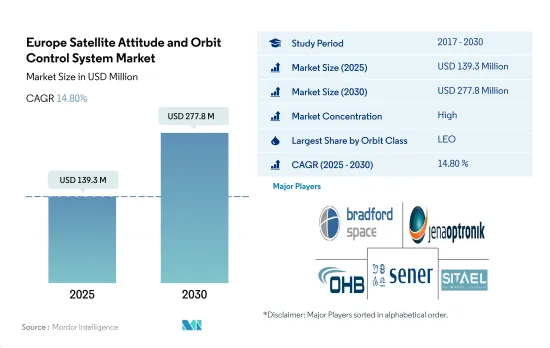

유럽의 위성 자세 궤도 제어 시스템 시장 규모는 2025년에 1억 3,930만 달러로 추정되며, 2030년에는 2억 7,780만 달러에 이를 것으로 예측되고, 예측 기간(2025-2030년) 동안 CAGR 14.80%로 성장할 전망입니다.

2029년에는 LEO 위성이 73.6%로 큰 점유율을 차지해 시장 수요를 견인할 전망입니다.

- 유럽에서는 LEO, MEO, GEO 위성의 AOCS 시장은 통신, 지구 관측, 네비게이션 등 위성의 고정밀 측위와 방위를 필요로 하는 위성 기반의 서비스에 대한 투자 증가에 의해 견인되고 있습니다.

- LEO 위성은 지구 관측, 원격 탐사, 과학 연구 등의 용도로 사용됩니다. 발사되는 소형 위성의 수가 증가하고 있어 효율적이고 비용 효과가 높은 AOCS가 필요하다는 점도 시장을 견인하고 있습니다.

- GEO 위성은 통신, 방송, 일기 예보 등의 용도로 사용됩니다. 고속 인터넷 접속과 디지털 방송 수요는 GEO 위성용 AOCS 시장의 성장을 가속할 것으로 예상되고 있습니다.

- MEO 위성은 GPS, Galileo, BeiDou와 같은 전 지구 항법 위성 시스템(GNSS)에 사용됩니다. Thales Alenia Space, OHB System AG, RUAG Space는 MEO 위성용 AOCS를 제공하는 주요 기업입니다.

유럽의 위성 자세 궤도 제어 시스템 시장 동향

소형 위성이 시장 수요를 낳을 전망

- 우주선의 질량별 분류는 로켓의 크기와 위성을 발사하는 비용을 결정하는 주요 지표 중 하나입니다. 올해에는 유럽 기관에 속하는 35대 이상의 대형 위성이 발사되었으며, 2017년부터 2022년까지 15기 이상의 중형 위성을 유럽의 조직이 운용하고 있었습니다. 질량 500kg 이하의 위성은 소형 위성으로 간주되며 이 지역에서는 약 460기 이상의 소형 위성이 발사되고 있습니다.

- 이 지역에서는 개발 기간이 짧아 전체 임무 비용을 절감할 수 있기 때문에 소형 위성에 대한 경향이 커지고 있습니다.유럽의 소형 위성 산업은 특정 용도에 맞추어 소형 위성을 설계 및 제조하기 위한 견고한 프레임워크에 의해 지지되고 있습니다.

지구 관측, 위성 항법, 연결성 부문에 대한 투자 기회가 시장 성장을 견인

- 유럽 국가들은 우주 산업에서의 다양한 투자의 중요성을 인식하고 있으며 세계 우주 산업에서 경쟁을 유지하기 위해 지구 관측, 위성 항법, 연결성, 우주 연구, 기술 혁신 등의 부문에 대한 지출을 늘리고 있습니다. 유럽우주국(ESA)은 측량에서 유럽의 리드를 유지하고 항법 서비스를 확대하여 미국과의 탐사 파트너십을 결성하기 위해 향후 3년간 우주 자금을 25% 증액할 것을 발표했습니다. ESA는 2023-2025년 예산 185억 유로에 대한 자금 지원을 22개국에 요청했습니다. 2022년 11월, 독일은 통신에 약 3억 6,500만 유로, 기술 프로그램에 5,000만 유로, 우주 상황 인식과 우주 보안에 1억 5,500만 유로, 우주 수송과 운용에 3억 6,800만 유로 등, 약 23억 7,000만 유로를 할당한다고 발표했습니다.

- 영국 우주청은 영국의 우주산업을 뒷받침하기 위한 18개의 프로젝트를 지원하기 위해 650만 유로의 자금을 제공한다고 발표했습니다. 18개 프로젝트는 공공 서비스를 강화하기 위한 지구 관측 데이터 활용 등 지역 문제를 해결하기 위한 다양한 혁신적 우주 기술을 개척합니다.

유럽의 위성 자세 궤도 제어 시스템 산업 개요

유럽의 위성 자세 및 궤도 제어 시스템 시장은 상당히 통합되어 있으며 상위 5개 기업에서 98.52%를 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 위성의 소형화

- 위성 질량

- 우주 개발에의 지출

- 규제 프레임워크

- 프랑스

- 독일

- 러시아

- 영국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 용도

- 통신

- 지구 관측

- 네비게이션

- 우주 관측

- 기타

- 위성 질량

- 10-100kg

- 100-500kg

- 500-1,000kg

- 10kg 이하

- 1,000kg 이상

- 궤도 클래스

- GEO

- LEO

- MEO

- 최종 사용자

- 상업

- 군사 및 정부

- 기타

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- AAC Clyde Space

- Bradford Engineering BV

- Innovative Solutions in Space BV

- Jena-Optronik

- NewSpace Systems

- OHB SE

- SENER Group

- Sitael SpA

- Thales

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Satellite Attitude and Orbit Control System Market size is estimated at 139.3 million USD in 2025, and is expected to reach 277.8 million USD by 2030, growing at a CAGR of 14.80% during the forecast period (2025-2030).

LEO satellites are driving the market demand by occupying a significant share of 73.6% in 2029

- In Europe, the AOCS market for LEO, MEO, and GEO satellites is driven by increasing investments in satellite-based services, such as communication, Earth observation, and navigation, which require high-precision positioning and orientation of satellites.

- LEO satellites are used for applications such as Earth observation, remote sensing, and scientific research. The growing demand for high-resolution satellite imagery and remote sensing data is expected to drive the LEO segment. The market is also driven by the rising number of small satellites being launched into orbit, which require efficient and cost-effective AOCS. Between 2017 and 2022, approximately 531 satellites were launched into LEO.

- GEO satellites are used for applications like communication, broadcasting, and weather forecasting. The demand for high-speed internet connectivity and digital broadcasting is expected to drive the growth of the AOCS market for GEO satellites. Key players in the market include Airbus Defence and Space, Lockheed Martin, and Northrop Grumman. Between 2017 and 2022, approximately 16 satellites were launched into GEO.

- MEO satellites are used for global navigation satellite systems (GNSS) like GPS, Galileo, and BeiDou. The increasing demand for GNSS applications in various industries, such as automotive, aviation, and maritime, is expected to drive the growth of the AOCS market for MEO satellites. Thales Alenia Space, OHB System AG, and RUAG Space are some of the leading companies providing AOCS for MEO satellites. Between 2017 and 2022, approximately 16 satellites were launched into MEO. The segment is expected to record a 15% CAGR during the forecast period.

Europe Satellite Attitude and Orbit Control System Market Trends

Small satellites are poised to generate demand in the market

- The classification of spacecraft by mass is one of the primary metrics for determining the launch vehicle size and the cost of launching satellites into orbit. The success of a satellite mission depends heavily on the accuracy of its pre-flight mass measurement and the proper balance of the satellite in order to generate mass within limits. Satellites are classified according to their mass. The main mass classifications include large satellites that weigh over 1,000 kg. Between 2017 and 2022, more than 35 large satellites belonging to European organizations were launched. A medium-sized satellite has a mass between 500 and 1,000 kg, and European organizations operated more than 15 such satellites launched during 2017-2022. Similarly, satellites with a mass of less than 500 kg are considered small satellites, and about 460+ small satellites have been launched from this region.

- There is a growing trend toward smaller satellites in the region due to their shorter development times, which can reduce overall mission costs. They have made it possible to significantly reduce the time required to obtain scientific and technological results. Small spacecraft missions tend to be more flexible and thus can better respond to new technological opportunities or needs. The small satellite industry in Europe is supported by a robust framework for the design and manufacturing of small satellites tailored to serve specific applications. The number of operations in the European region is expected to increase between 2023 and 2029, driven by growing demand in the commercial and military space industries.

Investment opportunities in Earth observation, satellite navigation, and connectivity areas are driving market growth

- European countries are recognizing the importance of various investments in the space industry and increasing their spending in areas such as Earth observation, satellite navigation, connectivity, space research, and innovation to stay competitive in the global space industry. In November 2022, the ESA announced that it had proposed a 25% boost in space funding over the next three years designed to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in exploration with the United States. The ESA has asked its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. In September 2022, the French government announced that it was planning to allocate more than USD 9 billion to space activities, an increase of about 25% over the past three years. In November 2022, Germany announced that about EUR 2.37 billion was allocated, including about EUR 669 million for Earth observation, about EUR 365 million for telecommunications, EUR 50 million for technology programs, EUR 155 million for space situational awareness and space security, and EUR 368 million for space transport and operations.

- The UK Space Agency announced that it would be funding EUR 6.5 million to support 18 projects aimed at boosting the UK space industry. The funding will stimulate growth in the UK space industry by supporting high-impact, locally-led schemes, and space cluster development managers. The 18 projects will pioneer a range of innovative space technologies to combat local issues, such as utilizing Earth observation data to enhance public services. In April 2023, the UK government announced that it is expecting to allocate USD 3.1 billion for space-related activities.

Europe Satellite Attitude and Orbit Control System Industry Overview

The Europe Satellite Attitude and Orbit Control System Market is fairly consolidated, with the top five companies occupying 98.52%. The major players in this market are Bradford Engineering BV, Jena-Optronik, OHB SE, SENER Group and Sitael S.p.A. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Russia

- 4.4.4 United Kingdom

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 Below 10 Kg

- 5.2.5 above 1000kg

- 5.3 Orbit Class

- 5.3.1 GEO

- 5.3.2 LEO

- 5.3.3 MEO

- 5.4 End User

- 5.4.1 Commercial

- 5.4.2 Military & Government

- 5.4.3 Other

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 AAC Clyde Space

- 6.4.2 Bradford Engineering BV

- 6.4.3 Innovative Solutions in Space BV

- 6.4.4 Jena-Optronik

- 6.4.5 NewSpace Systems

- 6.4.6 OHB SE

- 6.4.7 SENER Group

- 6.4.8 Sitael S.p.A.

- 6.4.9 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록