|

시장보고서

상품코드

1693970

지속가능성 컨설팅 서비스 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Sustainability Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

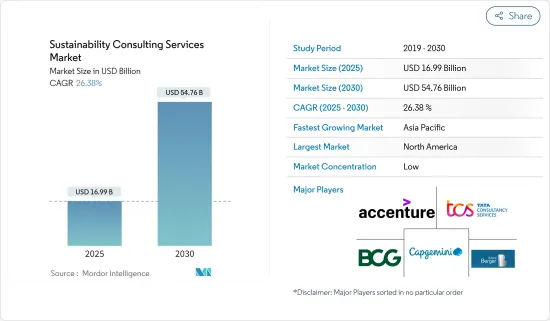

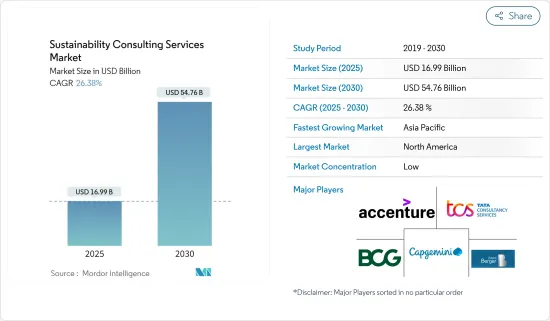

지속가능성 컨설팅 서비스 시장 규모는 2025년에 169억 9,000만 달러, 2030년에는 547억 6,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 26.38%를 나타낼 전망입니다.

지속가능경영 컨설팅 서비스 시장의 확대는 여러 요인에 의해 초래되고 있습니다.

주요 하이라이트

- 이 성장은 지속가능경영이 기업전략과 의사결정의 중심을 차지하는 비즈니스 환경의 매우 중요한 변화를 의미하고 있습니다.글로벌 지속가능경영 컨설팅 서비스 시장은 지속적으로 확장하는 태세를 갖추었습니다.

- 이산화탄소 배출량 감소에 대한 관심 증가와 기업의 넷 제로 목표를 달성할 필요성 증가가 지속가능성 컨설팅 서비스에 대한 수요를 뒷받침하고 있습니다.

- 세계 각국은 기후 변화와 싸우기 위한 국가 목표를 설정하고 지속가능성 컨설팅 서비스에 대한 수요를 크게 끌어 올리고 있습니다.

- 현실과의 격차가 크고 도입 수준이 낮은 것이 세계의 지속가능경영 컨설팅 서비스 시장의 성장을 방해하는 큰 요인이 되고 있습니다. 조직은 재정적, 기술적, 인적 자원에 한계가 있기 때문에 기후 변화에 대한 적응과 같은 복잡하고 논쟁적인 문제에 대처하기 어렵고, 고전을 강요받는 경우가 많습니다.

- 현재 진행중인 러시아 우크라이나 전쟁은 세계의 지속가능성 컨설팅 서비스 시장에 큰 영향을 미치고 있습니다. 전쟁은 특히 지속가능성 프로젝트에 불가결한 재료나 상품공급 체인을 혼란시키고 있습니다. 특히, 전기자동차 배터리에 필수적인 니켈과 팔라듐은 공급망에서 큰 문제에 직면하고 있습니다.

지속가능성 컨설팅 서비스 시장 동향

기후 변화 컨설팅 서비스가 주요 시장 점유율을 차지

- 기후 변화 컨설팅 서비스에는 탄소 발자국과 완화 분석, 대체 에너지 개발 및 에너지 효율화, 기후 적응과 전략, 긴급 상황 관리, 탄소 오프셋 및 넷 제로 서비스, 환경 규제 준수 서비스, 폐기물 관리 및 순환형 사회 및 기타 서비스가 포함됩니다.

- 기후 변화 컨설턴트 서비스에 대한 수요 증가는 환경 부하 저감, 탄소 실적 삭감, 기후 변동 적응, 리스크 관리, 법규 준수의 철저, 지속 가능한 실천에 관한 전문가의 조언을 요구하는 기업이나 조직에 의한 것입니다.

- 전 세계적으로 기업은 기후 변화의 영향을 받고 있습니다. 결과적으로 물리적 위험, 과도적 위험, 배상 책임으로 인한 위험 등 기후 변화와 관련된 위험을 관리하는 것은 경쟁을 유지하고 새로운 넷 제로 패러다임에서 중요합니다. 이런 상황의 변화에 의해 기후 변동을 중심으로 한 다양한 컨설팅 서비스에 수요가 높아지고 있어, 복잡한 상황을 극복하기 위한 지원을 실시했습니다.

- The Emissions Database for Global Atmospheric Research/Joint Research Centre(EDGAR/JRC)'가 발표한 세계 각국의 온실가스(GHG) 배출량에 관한 2024년판 보고서에 의하면, 세계의 온실효과가스(GHG) 배출량은 2023년에 과거 최고를 기록해, 이산화탄소 환산으로 529억 6,000만 톤(Gt CO2e)에 도달하여 전년 대비 2% 증가했습니다.

- 게다가 기후 변화 문제에 솔선하고 맞서는 기업은 평판을 높여 지속가능경영의 리더로서의 지위를 확립하게 하고 있습니다.

- 지속가능경영 컨설팅 시장공급업체는 기후 변화 컨설팅 회사를 인수하고 있습니다.

- 예를 들어, 2024년 6월, 지속가능경영자인 ERM은 호주를 기반으로 하는 기후 변화 위험과 에너지 전환 컨설턴트 회사인 Energetics를 인수하는 것으로 합의했다고 발표했습니다. Energyics는 기후 복원력 전략 수립, 기후 위험 및 재생 에너지 전환에 대한 인사이트 제공, 기업의 넷 제로 목표 달성 안내, 재생 에너지 거래를 위한 전력 구매 계약(PPA) 모니터링 등 맞춤형 서비스를 전문으로 합니다.

- 전반적으로 기후 변화 컨설팅 서비스는 세계 지속가능경영 컨설팅 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 기업과 조직이 기후 영향에 대해 더 많이 인식하고, 탄소 발자국을 줄여야 한다는 규제 압력에 직면해, 기후 변화 대책에 대한 대처가 세계적으로 급증하는 가운데, 기후 변동 컨설팅 서비스에 수요가 높아지고 있습니다.

큰 성장을 이루는 아시아태평양

- 다양한 규제 프레임워크과 급속한 산업화가 아시아태평양의 지속가능경영 컨설팅 시장을 형성하고 있습니다. 지역 확대에 크게 기여하고 있습니다. 이를 받아 아시아태평양의 지속가능성 컨설팅 회사는 기업이 컴플라이언스 목표를 달성하고 녹색 전략을 채택하고 지속 가능한 사례를 업무에 도입하는 것을 지원합니다.

- 중국과 인도와 같은 국가들은 급속한 도시화와 산업화가 진행되고 있으며, 환경 악화에 직면하고 있습니다. 지속 가능성 컨설팅 회사는 매우 중요한 역할을 담당하고 있으며, 국내와 국제적인 지속가능성 벤치마크를 확실히 준수하면서 성장과 환경 스튜어드십을 조화시키는 비즈니스 모델을 구축하도록 기업을 지도하고 있습니다.

- 예를 들어, 도시화의 진전과 2030년까지 탄소 배출량의 피크를, 2060년까지 완전한 탄소 중립을 목표로 하는 「듀얼 카본」국가 목표에 추진되어, 중국은 건축 및 건설 섹터의 그린화 대처를 강화하고 있습니다. 정부의 데이터에 따르면, 2020년에는 중국의 새로운 도시 건설 프로젝트의 77%가 친환경 건물로 분류되었습니다.

- 2023년 10월, 상하이시는 시내에 진출하는 외자계 기업의 ESG 능력을 강화하는 것을 목적으로 한 3개년 계획을 발표했습니다.

- 아시아태평양에서는 세계 투자자를 불러들여 브랜드 평가를 높이기 위해 ESG 원칙을 채용하는 기업이 늘어나고 있습니다.

지속가능성 컨설팅 서비스 시장 개요

지속가능성 컨설팅 서비스 시장은 기존 참가 기업과 신흥 참가 기업 모두가 다양하게 혼합되어 있는 것을 특징으로 합니다. Accenture PLC, The Boston Consulting Group, Inc., Tata Consultancy Services Limited, Capgemini SE, and Roland Berger GmbH 등이 주요 진출기업입니다.

이 시장에서 적당한 출구 장벽은 신규 진출기업에 인센티브를 부여하는 한편, 기존 기업은 저수익기에 철수할 수 있도록 하고 있습니다. 솔루션에 점점 더 힘을 쏟고 있습니다. 이와는 대조적으로, 소규모로 신규 진입하는 기업은 대기업에 대항하기 위해 비용 효율적인 전략을 채택하여 경쟁을 격화시킬 것으로 예측됩니다.

게다가 최근 합작 투자와 인수가 눈에 띄게 늘어나고 있는 것은 세계의 비즈니스계가 지속가능성을 중시하고 있음을 뒷받침하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 시장의 거시경제 요인 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 카본 풋 프린트의 삭감과 넷 제로 목표의 달성에 대한 주목의 고조

- 기후 변화와 싸우기 위한 세계 각국의 국가 목표

- 시장의 과제

- 현실적인 시나리오에 큰 격차가 있는 저수준의 보급률

제6장 시장 세분화

- 서비스 유형별

- 기후 변화 컨설팅 서비스

- 그린빌딩 컨설팅 서비스

- ESG 컨설팅 서비스

- 기타 지속가능성 컨설팅 서비스

- 최종 사용자별

- 건설 및 부동산

- 에너지 전력

- 공공 부문

- 기타

- 지역별

- 북미

- 유럽

- 영국

- 독일

- 베네룩스

- 스페인

- 프랑스

- 북유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Accenture PLC

- The Boston Consulting Group, Inc.

- Tata Consultancy Services Limited

- Capgemini SE

- Roland Berger GmbH

- Bain & Company, Inc.

- KPMG International Limited

- Ernst & Young Global Limited

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers LLP

- McKinsey & Company

- Kearney

- Godrej & Boyce Mfg. Co. Ltd(Godrej Industries Limited)

- RPS Group(Tetra Tech Inc.)

- SEA Energy

제8장 투자 분석

제9장 시장 전망

SHW 25.05.15The Sustainability Consulting Services Market size is estimated at USD 16.99 billion in 2025, and is expected to reach USD 54.76 billion by 2030, at a CAGR of 26.38% during the forecast period (2025-2030).

The expansion of the sustainability consulting services market is driven by several factors. These include increased awareness of environmental, social, and governance (ESG) issues, a stronger focus on reducing carbon footprints, heightened stakeholder pressures, more stringent regulatory compliance requirements, and the necessity for businesses to adopt sustainable practices to meet customer expectations and enhance their reputation.

Key Highlights

- Moreover, this growth signifies a pivotal transformation in the business landscape, with sustainability taking center stage in corporate strategies and decision-making. As companies increasingly adapt to evolving climate conditions, aim to reduce greenhouse gas emissions, and strive to meet global sustainability benchmarks, the global sustainability consulting services market is poised for continued expansion. Consequently, consulting firms play a vital role in assisting governments, businesses, and nonprofit entities in creating strategies, adopting sustainable practices, and navigating the increasing complexities of the changing climate.

- The rising focus on carbon footprint reduction and the growing need to fulfill businesses' net zero targets drive the demand for sustainability consulting services. Companies worldwide increasingly commit to achieving "net zero" greenhouse gas emissions, aligning with initiatives to combat climate change. This positively drives businesses' demand for sustainability consulting services to achieve their net-zero targets efficiently.

- Countries worldwide are setting national goals to combat climate change, significantly boosting the demand for sustainability consulting services. Governments are implementing measures to achieve net-zero emissions, fueling the demand for sustainability consulting services, which are pivotal in guiding governments and formulating strategies toward their net-zero targets.

- Lower levels of adoption, with large gaps in reality, are a major factor hindering the growth of the global sustainability consulting services market. Environmental consulting firms face challenges in promoting sustainability due to the sluggish adoption of sustainability initiatives across various nations. Organizations frequently struggle with limited financial, technical, and human resources, making addressing intricate and contentious issues such as climate change adaptation difficult. Consequently, this dynamic results in diminished uptake of sustainability consulting services, both in the private sector and among public sector enterprises.

- The ongoing Russia-Ukraine War significantly impacts the global sustainability consulting services market. It has profoundly affected global economic growth and labor markets, intensifying inflationary pressures and causing significant supply chain disruptions. The war has disrupted supply chains, especially for materials and goods vital to sustainability projects. Notably, nickel and palladium, essential for electric vehicle batteries, have faced significant supply chain challenges.

Sustainability Consulting Services Market Trends

Climate Change Consultancy Services Type Holds Major Market Share

- Climate change consultancy services considered under the scope include Carbon Footprint and Mitigation Analysis, Alternative Energy Development and Energy Efficiency, Climate Adaptation and Strategy, Emergency Management, Carbon Offset/Net Zero Services, Environmental Regulatory Compliance Services, Waste Management and Circularity, and Other Services.

- The increasing demand for climate change consultancy services is driven by businesses and organizations seeking expert advice on reducing environmental impact, lowering carbon footprints, adapting to climate change, managing risks, ensuring regulatory compliance, and implementing sustainable practices.

- Across the globe, businesses are grappling with the repercussions of climate change. As a result, managing climate-related risks, such as physical, transitional, or liability-based, has become paramount for firms eager to maintain their competitive edge and thrive in the emerging Net Zero paradigm. This evolving landscape has spurred a heightened demand for various consultancy services centered on climate change, aiding businesses in navigating these complexities.

- According to the 2024 report on GHG emissions from all world countries, published by 'The Emissions Database for Global Atmospheric Research/Joint Research Centre (EDGAR/JRC)'' global greenhouse gas (GHG) emissions hit a record high in 2023, reaching 52.96 billion metric tons of carbon dioxide equivalent (Gt CO2e), marking a two percent year-over-year increase.

- Moreover, companies that take the initiative in confronting climate change issues bolster their reputation and position themselves as leaders in sustainability. Such a proactive stance can translate into a significant competitive advantage, drawing in customers, top talent, and valuable partnerships.

- Vendors in the sustainability consulting market are acquiring climate change consulting firms. This strategy aims to broaden their service offerings, bolster their market presence, and cater to the rising demand for climate change consultancy services.

- For instance, in June 2024, ERM, a sustainability advisory firm, announced its agreement to acquire Energetics, a climate risk and energy transition consultancy based in Australia. This move aims to bolster ERM's growth in the Asia Pacific region. Energetics specializes in tailored services, such as crafting climate resiliency strategies, offering insights on climate risks and renewable energy transitions, guiding companies towards net-zero goals, and monitoring power purchase agreements (PPAs) for renewable energy transactions. ERM asserts that this acquisition will bolster its capacity to provide clients with both strategic advice and hands-on implementation across Australia and the broader Asia Pacific region.

- Overall, climate change consultancy services are expected to hold the largest share of the global sustainability consulting market. As businesses and organizations become more aware of climate impacts, face regulatory pressures to reduce their carbon footprints, and witness a global surge in climate action initiatives, there's a rising demand for climate change consultancy services. This demand is further fueled by businesses seeking a competitive edge through proactive climate change risk management.

Asia Pacific to Register Major Growth

- Diverse regulatory frameworks and swift industrialization shape the sustainability consulting market in the Asia-Pacific region. The region's expansion is largely fueled by heightened government regulations on environmental standards, especially in energy-intensive sectors such as manufacturing, oil and gas, and construction. In response, sustainability consulting firms in the Asia-Pacific help businesses meet compliance targets, adopt green strategies, and weave sustainable practices into their operations.

- Countries like China and India, witnessing rapid urbanization and industrialization, face environmental degradation. This has led their governments to enforce stricter environmental standards. In this context, sustainability consulting firms play a pivotal role, guiding companies to craft business models that harmonize growth with environmental stewardship, all while ensuring adherence to both national and international sustainability benchmarks.

- For instance, driven by rising urbanization and its national "Dual Carbon" targets-aiming for peak carbon emissions by 2030 and full carbon neutrality by 2060-China is intensifying its efforts to green its building and construction sector. Government data reveals that in 2020, a significant 77% of China's new urban construction projects were classified as green buildings.

- In October 2023, Shanghai unveiled a three-year initiative aimed at bolstering the ESG capabilities of foreign businesses in the city. Thereby, the plan encourages companies to ramp up Research and Development investments and embrace digital, green, and low-carbon technologies, enhancing their innovation and competitiveness, and heightening the demand for sustainability consulting solutions.

- In the Asia-Pacific region, companies are increasingly adopting ESG principles to draw in global investors and bolster their brand reputation. Sustainability consulting firms assist these businesses by pinpointing areas for enhancement, executing ESG strategies, and gearing up for international sustainability reporting standards.

Sustainability Consulting Services Market Overview

The sustainability consulting services market is characterized by a diverse mix of both established and emerging players. Some of the major players in the market are Accenture PLC, The Boston Consulting Group, Inc., Tata Consultancy Services Limited, Capgemini SE, and Roland Berger GmbH, among others.

Moderate exit barriers in the market incentivize new entrants while allowing established firms to exit during low-profit periods. Leading industry players are increasingly focusing on integrated solutions to attract customers. In contrast, smaller and newer market entrants are expected to adopt cost-benefit strategies to vie with their larger counterparts, intensifying competition.

Furthermore, a notable surge in joint ventures and acquisitions recently underscores the global business community's heightened emphasis on sustainability. As a result, competitive rivalry in the global sustainability market remains pronounced.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Focus on the Reduction of Carbon Footprint and Fulfilment of Net Zero Targets

- 5.1.2 National Goals Across the Globe to Combat Climate Change

- 5.2 Market Challenges

- 5.2.1 Lower Levels of Adoption with Large Gaps in the Realistic Scenario

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Climate Change Consultancy Services

- 6.1.2 Green Building Consultancy Services

- 6.1.3 ESG Consultancy Services

- 6.1.4 Other Sustainability Consultancy Services

- 6.2 By End User

- 6.2.1 Construction and Real Estate

- 6.2.2 Energy and Power

- 6.2.3 Public Sector

- 6.2.4 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 Benelux

- 6.3.2.4 Spain

- 6.3.2.5 France

- 6.3.2.6 Nordics

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Accenture PLC

- 7.1.2 The Boston Consulting Group, Inc.

- 7.1.3 Tata Consultancy Services Limited

- 7.1.4 Capgemini SE

- 7.1.5 Roland Berger GmbH

- 7.1.6 Bain & Company, Inc.

- 7.1.7 KPMG International Limited

- 7.1.8 Ernst & Young Global Limited

- 7.1.9 Deloitte Touche Tohmatsu Limited

- 7.1.10 PricewaterhouseCoopers LLP

- 7.1.11 McKinsey & Company

- 7.1.12 Kearney

- 7.1.13 Godrej & Boyce Mfg. Co. Ltd (Godrej Industries Limited)

- 7.1.14 RPS Group (Tetra Tech Inc.)

- 7.1.15 SEA Energy