|

시장보고서

상품코드

1836464

인도의 약물전달 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)India Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

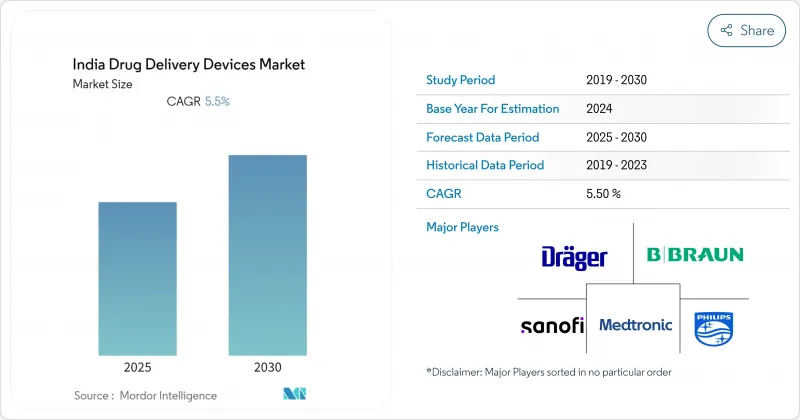

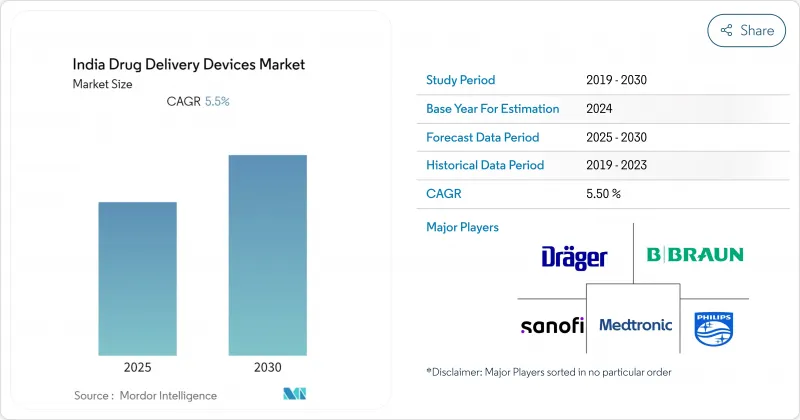

인도의 약물전달 기기 시장은 2025년에 68억 8,000만 달러로 평가되고, 예측 기간 동안 10.93%의 연평균 복합 성장률(CAGR)을 나타내 2030년에는 115억 6,000만 달러에 이를 것으로 예상됩니다.

헬스케어 인프라 확대, 만성질환 유병률 급증, 국내 생산 정책 지원은 첨단 치료 플랫폼에 대한 지속적인 수요를 촉진하고 있습니다. Production Linked Incentive(생산 연동 장려금) 제도에 따른 지속적인 정부 자금 지원과 신속한 규제 패스웨이는 특히 주사제 및 연결 시스템과 같은 신규 장치에 대한 장벽을 낮추고 있습니다. 또한 의료기기 국가정책 2023은 기준을 세계표준에 맞추어 구자라트주, 마할라슈트라주, 타밀나두주, 히마찰프라데시주의 혁신 클러스터를 육성하는 것입니다. 의료비 자체 부담이 대부분을 차지하는 인도 의료 시장에서는 지속적인 비용 압력이 있으며 공급업체는 병원에서 가정 환경으로 안전하게 전환할 수 있는 가치 지향적이고 사용자 친화적인 기술을 개발해야 합니다.

인도의 약물전달 기기 시장 동향과 인사이트

헬스케어 액세스를 지원하는 정부의 이니셔티브

2024-2025년도 연방예산에서는 의료에 대한 공공 지출이 89,287 칼로르 루피로 증가하여 1차 케어와 Tier 2 및 Tier 3 도시에서 장비 조달에 자금이 투입되었습니다. 국가 의료기기 정책 2023에 기반한 합리화된 승인 경로는 주사 및 임베디드 시스템 승인을 가속화하고 기존 일정을 거의 3분의 1로 줄였습니다. 2025년에 설립된 의료기기 수출 촉진 협의회와 함께 현지 기업은 보다 신속한 수출 인증과 시장 진입 지원을 얻을 수 있습니다. 이러한 정책적인 움직임으로 반도시 지역의 병원에서 합리적인 가격의 자동 주사기 채용이 확대되고 인도의 약물전달 기기 시장 전체 수요 증가에 박차를 가하고 있습니다. 자금 조달 증가는 임상 검증 연구를 추가로 지원하고 국산 신제품이 국제 기준을 충족하는지 확인합니다.

바이오시밀러 등 비용 효율적인 의약품에 대한 높은 수요

Biocon과 Dr.Reddy's로 대표되는 인도의 바이오시밀러 제조업체는 전용 전달 형식을 필요로 하는 생물제제의 염가판을 출시하고 있습니다. Biocon사의 릴라글루티드 제네릭은 2024년에 승인되었으며, 다제 투여 요법을 위해 설계된 재사용 가능한 펜의 대량 생산이 시작되었습니다. 게다가 15유형의 펩티드 제제가 승인 가까이 되어, 재택에서의 피하 투여에 적합한 콤팩트한 자동 주사기 수요가 급증하고 있습니다. 도시에서의 채용이 특히 진행되고 있어, 거기에서는 임상의가 총치료비를 억제하기 위해 바이오시밀러를 처방하게 되어, 투여 데이터를 전자 의료 기록에 업로드하는 커넥티드 펜의 보급이 확대되고 있습니다. 바이오시밀러 성장과 기기 기술 혁신의 선순환은 인도의 약물전달 기기 시장에서 국내 기업의 경쟁력을 강화하고 있습니다.

고급 이식 시스템의 보급을 막는 고액의 사비 부담

인도 총 의료비의 55%는 여전히 자기 부담액이며, 1대 2,000-5,000달러의 임베디드 펌프에 대한 액세스가 제한되어 있습니다. 대규모 민간 보험 회사 이외의 경우에는 상환이 여전히 불안정하기 때문에 많은 환자들은 저렴한 가격의 외부 펌프와 기존 주사기를 사용합니다. 그러므로 보급은 도시의 병원에 집중되어 인도의 약물전달 기기 시장 전체에 편재를 일으키고 있습니다. 정부가 Pradhan Mantri Jan Arogya Yojana의 적용 범위를 임베디드 약물 플랫폼으로 확대할 계획으로 이 제약이 완화될 수 있지만, 단기 도입은 농촌 지역의 가격 격차에 의해 제한된 채로 남아 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 고령화와 함께 만성 질환이나 감염증의 부담이 증가

- 의료기기의 국내 제조를 촉진하는 정부 및 시장 기업의 대처

- 승인 지연을 일으키는 제제의 분류에 관한 규제 불확실성

부문 분석

당뇨병, 종양학, 면역학 치료에 있어서의 펜, 자동 주사기, 안전 주사기 수요의 높이를 반영해 2024년 인도 약물전달 기기 시장의 45.0%를 주사기가 차지했습니다. 프리필드 주사기는 취급 실수를 최소화하고, 스프링식 자동 주사기는 특히 손목의 용이함에 어려움을 겪는 노인 환자의 자가 투여를 개선합니다. 바이오시밀러의 수용 확대는 데드 스페이스가 적은 주사기 형식과 재사용 가능한 펜형 플랫폼에 대한 수량 요건을 확대하고 있습니다. 병원이 가장 큰 고객임에 변화는 없지만, 약국이 자기 사용 기구를 조제하는 케이스가 늘어나고 있어 소매 유통 모델에 박차가 걸려 있습니다.

이식형 기구는 2030년까지의 CAGR이 12.04%를 나타낼 전망입니다. 티타늄 합금과 생체 흡수성 고분자와 같은 재료는 진통제, 진경제, 신경 활성 화합물의 방출 제어를 가능하게합니다. 심뇌 펌프는 파킨슨병과 간질에 유망하며 초기 임상 데이터는 지속적인 증상 조절과 전신 노출 감소를 보여줍니다. 국내 신흥기업이 IIT와 협력해 소형화 에너지원을 개량해 메이크 인 인디아의 목표에 따릅니다. 조달 비용이 낮아짐에 따라 임플란트 유형은 인도의 약물전달 기기 시장 규모 예측에서 더 높은 판매 점유율을 얻는 것으로 보입니다.

2024년 인도의 약물전달 기기 시장 규모에서는 경구 투여가 불가능한 생물학적 제형에 지원되는 주사 경로가 50.0%의 점유율을 차지했습니다. 스마트 펜은 복용 기록을 저장하고 암호화된 기록을 임상의에게 전송하여 복약 준수 불량의 조기 발견을 가능하게 합니다. 상 변화 패키징과 같은 콜드체인 기술 혁신은 마지막 원 마일 배송 중 제품의 무결성을 보호하고 지리적 범위를 확대합니다.

경비 전달은 2030년까지 연평균 복합 성장률(CAGR) 11.45%를 나타낼 전망입니다. 접착성 젤과 계면활성제 강화 스프레이는 약물 흡수를 개선하고 후각 상피를 통과하여 뇌에 도달할 가능성이 있습니다. 중점 분야에는 편두통, 알츠하이머, 심지어 바늘을 사용하지 않는 백신 부스터 등이 있습니다. 인도 기업은 멤브레인 투과 증진제의 라이선스를 취득하고 개발주기를 단축하고 있습니다. 3차 병원의 조종사 프로그램은 비강 치료에 대한 환자의 강한 선호를 보여주며 중추 신경계를 적응증으로 하는 미래의 인도의 약물전달 기기 시장 점유율을 높일 가능성이 높습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 헬스케어 액세스를 지원하는 정부의 대처

- 바이오시밀러 등 비용 효율적인 의약품에 대한 높은 수요

- 고령화에 수반하는 질병·감염증 부담의 증대

- 의료기기의 국내 제조를 뒷받침하는 정부 및 시장 기업의 대처

- 스마트/커넥티드·약물전달 기기에 대한 기술의 진보와 의식의 고조

- 재택치료나 원격 의료 모델의 급속한 확대가 자기 투여 기기를 뒷받침

- 시장 성장 억제요인

- 고액의 의료비 부담이 고도의 이식형 시스템의 보급 제한

- 조합 제품의 분류에 관한 규제상의 불확실성이 승인 지연의 원인

- Tier2/3 도시에서의 숙련 헬스케어 전문가의 부족이 주입 펌프의 안전한 사용을 방해

- 콜드체인 물류가 분단되어 온도에 민감한 주사 기기의 보급 범위가 제한

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 기기 유형별

- 주사 투여 기기

- 흡입 투여 기기

- 주입 펌프

- 경피 패치

- 이식형 약물전달 시스템

- 안구 삽입물 및 투여 임플란트

- 비강 및 구강 점막 투여 기기

- 투여 경로별

- 주사제

- 흡입제

- 경피제

- 구강 점막제(구강 및 설하)

- 안구제

- 비강제

- 용도별

- 암

- 심혈관 질환

- 당뇨병

- 호흡기 및 감염성 질환

- 신경계 질환

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 재택 헬스케어

- 클리닉 및 기타

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Sanofi

- Becton, Dickinson and Company(BD) India

- Cipla Ltd

- Novo Nordisk India Pvt Ltd

- Sun Pharmaceutical Industries Ltd

- Biocon Ltd

- Dr. Reddy's Laboratories Ltd

- Lupin Ltd

- Meril Life Sciences

- Zydus Lifesciences Ltd

- Medtronic Plc

- Terumo India Pvt Ltd

- Baxter India Pvt Ltd

- B. Braun Medical(India) Pvt Ltd

- Ysomed

- Bayer Pharmaceuticals India Ltd

- Pfizer Ltd(India)

- Johnson & Johnson Pvt Ltd(Janssen)

- Roche Products(India) Pvt Ltd

- Abbott India Ltd

제7장 시장 기회와 전망

KTH 25.10.27The India drug delivery devices market is valued at USD 6.88 billion in 2025 and is expected to reach USD 11.56 billion by 2030, reflecting a 10.93% CAGR through the forecast period.

Expanding healthcare infrastructure, a sharp rise in chronic disease prevalence, and policy support for domestic production are driving sustained demand for advanced therapeutic platforms. Continued government funding under the Production Linked Incentive scheme and fast-track regulatory pathways have lowered barriers for novel devices, particularly in injectables and connected systems. Manufacturers are also benefiting from the National Medical Devices Policy 2023, which aligns standards with global norms and fosters local innovation clusters in Gujarat, Maharashtra, Tamil Nadu, and Himachal Pradesh. Persistent cost pressures in India's predominantly out-of-pocket healthcare market have pushed suppliers to develop value-oriented, user-friendly technologies that can safely transition from hospital to home settings.

India Drug Delivery Devices Market Trends and Insights

Government Initiatives To Support Healthcare Access

Public spending on health rose to INR 89,287 crore in the 2024-25 Union Budget, channeling capital into primary care and device procurement within Tier 2 and Tier 3 cities. A streamlined approval pathway under the National Medical Devices Policy 2023 now accelerates clearances for injectable and implantable systems, cutting previous timelines by nearly one-third. Coupled with the Export Promotion Council for Medical Devices established in 2025, local firms gain faster export certifications and market entry support. These policy moves have widened adoption of affordable autoinjectors in semi-urban hospitals, fueling incremental demand across the India drug delivery devices market. Increased funding further supports clinical validation studies, ensuring new domestic products meet international standards.

High Demand for Cost-Effective Drugs Such as Biosimilars

Indian biosimilar producers, led by Biocon and Dr. Reddy's, have launched low-cost versions of biologics that require dedicated delivery formats. Biocon's generic liraglutide received clearance in 2024, triggering higher volumes of reusable pens designed for multi-dose regimens. As 15 additional peptide formulations near approval, demand has surged for compact autoinjectors configured for subcutaneous delivery in home settings. Urban adoption is especially strong, where clinicians now prescribe biosimilars to lower total treatment expenses, thereby expanding penetration of connected pens that upload dosing data to electronic medical records. The virtuous cycle between biosimilar growth and device innovation strengthens competitiveness of domestic firms in the India drug delivery devices market.

High Out-of-Pocket Spending Restricting Adoption of Advanced Implantable Systems

Out-of-pocket payments still make up 55% of India's total health expenditure, limiting access to implantable pumps that cost USD 2,000-5,000 each. Reimbursement remains patchy outside large private insurers, pushing many patients toward lower-cost external pumps or conventional syringes. Uptake therefore concentrates in metro hospitals, creating uneven distribution across the India drug delivery devices market. Government plans to expand Pradhan Mantri Jan Arogya Yojana coverage to implantable drug platforms could ease this constraint, yet short-term adoption remains capped by affordability gaps in rural districts.

Other drivers and restraints analyzed in the detailed report include:

- High Burden of Chronic and Infectious Diseases Coupled with Aging Population

- Government and Market Players Initiatives for Boosting Domestic Manufacturing of Medical Devices

- Regulatory Uncertainty Around Classification of Combination Products Causing Approval Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Injectable delivery devices represented 45.0% of the India drug delivery devices market in 2024, reflecting high demand for pens, autoinjectors, and safety syringes across diabetes, oncology, and immunology care. Prefilled syringes minimize handling errors, while spring-loaded autoinjectors improve self-administration, particularly for aging patients who face dexterity challenges. Growing acceptance of biosimilars has expanded volume requirements for low-dead-space syringe formats and reusable pen platforms. Hospitals remain the largest customers, yet pharmacies increasingly dispense self-use devices, spurring retail distribution models.

Implantable devices are on track for a 12.04% CAGR to 2030. Materials such as titanium alloys and bioresorbable polymers provide controlled release for analgesics, antispasmodics, and neuroactive compounds. Deep-brain pumps demonstrate promise for Parkinson's and epilepsy, with early clinical data showing sustained symptom control and lower systemic exposure. Domestic startups collaborate with IITs to refine miniaturized energy sources, aligning with Make-in-India objectives. As procurement costs fall, implantables will capture higher revenue share within the broader India drug delivery devices market size projections.

The injectable route held a 50.0% share of the India drug delivery devices market size in 2024, supported by biologicals that cannot be delivered orally. Smart pens store dosing logs, forwarding encrypted records to clinicians, and enable early detection of non-adherence. Cold-chain innovations, such as phase-change packaging, safeguard product integrity during last-mile delivery, widening geographic reach.

Nasal delivery is moving at an 11.45% CAGR through 2030. Mucoadhesive gels and surfactant-enhanced sprays improve drug absorption and can traverse the olfactory epithelium to reach the brain. Focus areas include migraine, Alzheimer's, and even needle-free vaccine boosters. Indian firms license membrane-permeation enhancers, shortening development cycles. Pilot programs in tertiary hospitals show strong patient preference for nasal therapies, likely to boost future India drug delivery devices market share in central nervous system indications.

The India Drug Delivery Devices Market is Segmented by Device Type (Injectable Delivery Devices, Inhalation Delivery Devices, Infusion Pumps, and More), Route of Administration (Injectable, Inhalational, Trandermal and More), and Application (Cancer, Cardiovascular Diseases, Diabetes and More), End User (Hospitals, Ambulatory Surgical Centers and More). The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Sanofi

- Becton, Dickinson and Company (BD) India

- Cipla

- Novo Nordisk India Pvt Ltd

- Sun Pharmaceuticals Industries

- Biocon Ltd

- Dr. Reddy's Laboratories Ltd

- Lupin

- Meril Life Sciences

- Zydus Lifesciences Ltd

- Medtronic

- Terumo India Pvt Ltd

- Baxter India Pvt Ltd

- B. Braun Medical (India) Pvt Ltd

- Ysomed

- Bayer

- Pfizer Ltd (India)

- Johnson & Johnson Pvt Ltd (Janssen)

- Roche Products (India) Pvt Ltd

- Abbott India Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Initiatives To Support Healthcare Access

- 4.2.2 High Demand for Cost Effective Drugs Such as Biosimiliar

- 4.2.3 High Burden of Chrnoic and Infectious Diseases Coupled with Aging Population

- 4.2.4 Government and Market Players Initiatitives for Boosting Domestic Manufacruring of Medical Devices

- 4.2.5 Technological Advancement and Increased Awareness for Smart/ Connected Drug Delivery Devices

- 4.2.6 Rapid Expansion of Home-care and Tele-medicine Models Encouraging Self-administration Devices

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Spending Restricting Adoption of Advanced Implantable Systems

- 4.3.2 Regulatory Uncertainty Around Classification of Combination Products Causing Approval Delays

- 4.3.3 Skilled Healthcare Professional Shortage in Tier-2/3 Cities Impeding Safe Use of Infusion Pumps

- 4.3.4 Fragmented Cold-chain Logistics Limiting Reach of Temperature-Sensitive Injectable Devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Injectable Delivery Devices

- 5.1.2 Inhalation Delivery Devices

- 5.1.3 Infusion Pumps

- 5.1.4 Transdermal Patches

- 5.1.5 Implantable Drug Delivery Systems

- 5.1.6 Ocular Inserts and Delivery Implants

- 5.1.7 Nasal & Buccal Delivery Devices

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Inhalation

- 5.2.3 Transdermal

- 5.2.4 Oral Mucosal (Buccal and Sublingual)

- 5.2.5 Ocular

- 5.2.6 Nasal

- 5.3 By Application

- 5.3.1 Cancer

- 5.3.2 Cardiovascular Diseases

- 5.3.3 Diabetes

- 5.3.4 Respiratory and Infectious Diseases

- 5.3.5 Neurological Disorders

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Home Healthcare Settings

- 5.4.4 Clinics and Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sanofi

- 6.4.2 Becton, Dickinson and Company (BD) India

- 6.4.3 Cipla Ltd

- 6.4.4 Novo Nordisk India Pvt Ltd

- 6.4.5 Sun Pharmaceutical Industries Ltd

- 6.4.6 Biocon Ltd

- 6.4.7 Dr. Reddy's Laboratories Ltd

- 6.4.8 Lupin Ltd

- 6.4.9 Meril Life Sciences

- 6.4.10 Zydus Lifesciences Ltd

- 6.4.11 Medtronic Plc

- 6.4.12 Terumo India Pvt Ltd

- 6.4.13 Baxter India Pvt Ltd

- 6.4.14 B. Braun Medical (India) Pvt Ltd

- 6.4.15 Ysomed

- 6.4.16 Bayer Pharmaceuticals India Ltd

- 6.4.17 Pfizer Ltd (India)

- 6.4.18 Johnson & Johnson Pvt Ltd (Janssen)

- 6.4.19 Roche Products (India) Pvt Ltd

- 6.4.20 Abbott India Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment