|

시장보고서

상품코드

1836474

운송 컨테이너 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Shipping Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

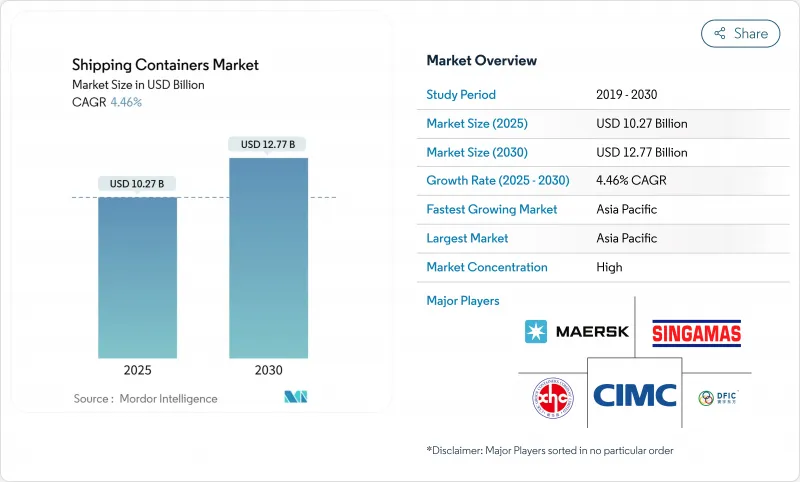

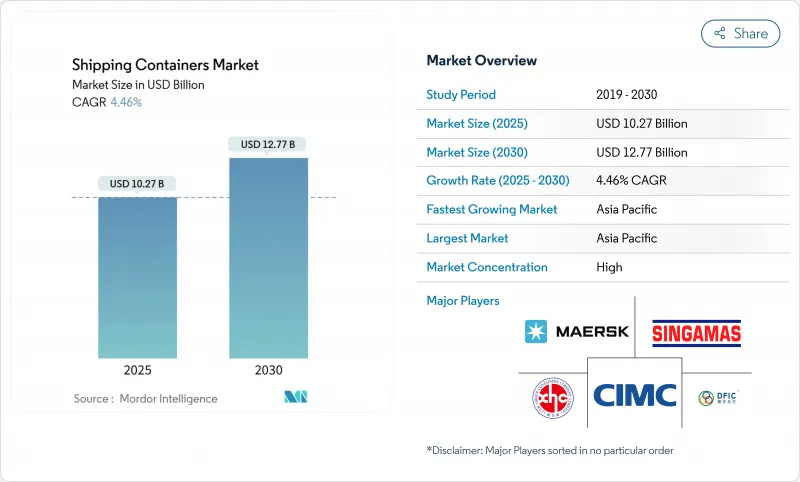

운송 컨테이너 시장 규모는 2025년에 102억 7,000만 달러에 달하고, 예측 기간(2025-2030년)의 CAGR은 4.46%를 나타내, 2030년에는 127억 7,000만 달러에 달할 것으로 전망됩니다.

전자상거래 융합, 의약품의 콜드체인 확대, 복합 일관 운송의 효율화가 안정적인 구조적 수요를 가져오고 있습니다. 세계 무역의 90%를 처리하는 컨테이너화의 역할이 이러한 성장을 지원하는 반면, 디지털 추적 도구와 보다 스마트한 설계는 사업자의 항만 체류 시간 단축과 자산 회전율 향상에 도움이 됩니다. 지속가능성의 목표는 보다 가벼운 복합재에 대한 재료 혁신을 뒷받침하고, 운송사 간의 얼라이언스 재편이 보다 대형이고 기술에 대응한 선대에 유리한 용량 배치 전략을 재구축하고 있습니다. 지정학적 혼란은 단기적인 변동성을 향상시킬 뿐만 아니라 다양한 무역 레인과 역동적인 라우팅의 중요성을 강화하고 있습니다.

세계의 운송 컨테이너 시장 동향과 인사이트

국경을 넘어서는 전자상거래의 폭발적 성장으로 24시간 턴어라운드에 대한 기대가 높아집니다.

전자상거래가 확대됨에 따라 더 작은 화물이 더 빨리 운송되고, 그 초점은 선박 용량에서 항구 속도로 이동하고 있습니다. 운송 회사는 고주파 루프에 장비를 추가하고 항만은 한 변화 내에서 선박을 통관시키는 자동 크레인에 투자합니다. 스마트 트래킹을 통해 화물주는 입항 전에 통관 절차를 수행하여 철도 발착 범위를 예약할 수 있습니다. 이러한 운영상의 이점은 재고 사이클을 단축하고 표준 드라이 박스에 대한 선호도를 높이고 무역량이 변동하더라도 높은 가동률을 유지합니다. 온라인 마켓플레이스가 신흥국에 침투함에 따라 운송 컨테이너 시장은 다양한 무역 레인에서 기준선 수요를 지속하고 있습니다.

콜드체인의 세계적인 보급이 선진적인 리퍼 화물의 수주를 가속

제약 제조업체는 온도 관리에 타협하지 않고 비용과 배출량을 줄이기 위해 장거리 운송을 항공 운송에서 해상 운송으로 전환합니다. 최신 리퍼는 -0.5 ° C의 정확도를 유지하고 실시간으로 편차에 플래그를 지정하는 원격 측정을 통합하므로 항해 도중에 시정 조치를 취할 수 있습니다. 신선한 식료품 수출업체도 유사한 기술을 채택하여 부패를 최소화하여 먼 소비자에게 전달합니다. 듀얼 연료 냉동 장치를 제공하는 제조업체는 에너지 소비를 줄이고 낮은 GWP 규제를 충족함으로써 상자 당 가격 실현을 높입니다. 식료품의 전자상거래가 새로운 시장으로 확대됨에 따라 첨단 리퍼 수요는 일반화물의 성장을 능가하고 있습니다.

유행 후 박스 공급 과잉은 이용률을 감소시킵니다.

2021년부터 2023년까지 진행된 기록적인 신조선은 임시 잉여를 낳고 임대료를 밀어내고 운영자에게 새로운 주문을 지연하도록 촉구했습니다. 무역이 연화되면 게이트웨이 항구에 유휴 재고가 축적되고, 저장소는 재배치 사업을 유치하기 위해 보관 수수료를 인하해야합니다. 제조업체는 생산 이동을 줄이고 보다 안정적이고 수요가 있는 특수 설계에 생산 능력을 돌려서 적응합니다. 스크랩이 선대의 노후화를 따라잡고 무역이 정상화되면 조정은 해소될 것으로 예측됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- D2C 브랜드가 주문제작 로고가 들어간 용기를 요구

- 재사용 가능한 용기의 채용을 추진하는 기업의 ESG 의무

- 예산에 불투명감을 초래하는 열연 코일 강판 가격의 변동성

부문 분석

하이큐브 제품은 13%의 헤드룸이 있기 때문에 전자상거래 소포와 경량 가전제품 등의 용적을 극대화할 수 있기 때문에 수요 증가를 포착하고 있습니다. 40피트형은 2024년에 52.64%의 매출을 계상해, 해상화물에 뿌리 깊은 인기가 있는 것을 나타낸 한편, 40피트 하이큐브 유닛은 2030년까지 연평균 복합 성장률(CAGR) 5.61%를 나타낼 것으로 예측됩니다. 하이큐브 유닛의 운송 컨테이너 시장 규모는 무게 제한을 저촉하지 않고 대용량을 요구하는 화물의 선호도를 반영합니다.

항구 인프라 업그레이드는 높이가 있는 스택을 지원하며 터미널 운영자는 이러한 장치를 효율적으로 처리하기 위해 리프팅 높이를 확장한 도달범위 스태커를 추가합니다. 물류 인티그레이터는 철도 수레 할당과 저장소 교환을 간소화하기 위해 40피트 프로파일의 표준화를 추진하고 있습니다. Triton Containers는 재배치를 줄이기위한 유연한 픽업 옵션을 갖춘 하이 큐브리스를 판매하고 채택을 강화합니다. 전반적으로, 발송인은 입방체의 효율성과 포장의 통합에 중점을 두고 있으며, 주요 무역 코리도에서 하이큐브 견인이 계속되고 있습니다.

드라이 스토리지 박스는 2024년 출하량의 72.75%를 차지했으며, 세계 상품 흐름의 백본으로서의 지위를 명확히 했습니다. 이와는 대조적으로, 신선한 식품 수출업체와 의약품 제조업체가 해상 항로를 확장함에 따라 리퍼 유닛의 2030년까지 연평균 복합 성장률(CAGR)은 6.42%를 나타낼 전망입니다. 냉장 컨테이너는 현재 운송 컨테이너 시장의 고급품이며, 드라이 유닛보다 2-3배 높은 렌탈료가 설정되어 있습니다.

기술 업그레이드에는 가변 속도 컴프레서와 유휴 에너지 소비를 줄이는 태양 보조 전력 모듈이 포함됩니다. 의약품 운송업자는 중복 온도 프로브와 편차로부터 몇 초 이내에 경고를 발하는 도어 센서가 필요하며 제조업체 간의 차별화를 촉진합니다. 온도 변화에 민감한 화물을 공수에서 해상 운송으로 이행함으로써 관련 배출의 최대 80%를 회피할 수 있기 때문에 리퍼도 탈탄소화의 혜택을 받습니다.

운송 컨테이너 시장은 사이즈별(20피트(TEU), 40피트(FEU), 기타), 컨테이너 유형별(드라이 스토리지(표준), 냉장, 기타), 재료별(콜텐강, 스테인리스 스틸, 기타), 최종용도 산업별(소비재 및 소매, 기타), 운송 수단별(해상·심해, 기타), 지역별(북미, 남미) 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

2024년 매출은 아시아태평양이 60.50%를 차지했고 2030년까지의 CAGR은 5.67%를 나타낼 전망입니다. 중국이 제조의 주도권을 유지하고 있지만, 기업이 조달처를 다양화하고 있기 때문에 동남아시아가 증가량을 획득하고 있습니다. 말레이시아와 인도의 메가 항만 프로젝트는 연간 2,500만 TEU 이상의 용량을 추가하고, 지역의 처리량을 안정화하고, 피더 네트워크 전체의 컨테이너 수요를 자극합니다. 통화 안정성과 지지적인 무역 협정은 또한 지역의 리스풀에 함대의 확대를 촉구하고 있습니다.

북미는 전자기기나 자동차 조립을 소비 시장 근처로 이동시키는 니어쇼어링의 혜택을 받습니다. 미국 항만 당국은 수십억 달러 규모의 준설 및 버스 전기 프로그램을 승인하고 멕시코와 캐나다의 게이트웨이에 대한 경쟁력을 강화합니다. 미국 중서부의 철도 인터모달 정비는 대서양과 태평양을 8일 이내에 연결하는 비용 효과적인 육교를 개통하여 스택 트레인에 대응하는 컨테이너 설계의 채용을 촉진합니다.

유럽은 지정학적 긴장으로 인해 아시아-유럽 항로가 아프리카 주변으로 우회되고 교통 시간이 늘어나면서 지중해의 허브 항로로의 기항이 증가했기 때문에 마을의 성장을 기록했습니다. 런던 게이트웨이와 로테르담 마스브랙테의 자동화 투자는 크레인 시간당 처리 능력을 높이고 박스당 비용 지표를 완화합니다. 엄격한 환경 규제는 재활용 컨테이너 유닛을 채택하기 위해 더 오래되고 무거운 박스의 퇴역을 가속화하고 무역량의 성장 문제에도 불구하고 교체 수요를 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 국경을 넘어서는 전자상거래의 폭발적인 성장으로 표준 건식 컨테이너에 24시간 납기에 대한 기대 증가

- 신선 식료품과 밀 키트의 택배 세계의 콜드체인의 보급에 의해 선진적인 리퍼 박스의 주문이 가속

- 소비자 직접 판매(D2C) 브랜드는 이동 가능한 팝업 스토어 및 완성 허브로 맞춤형 로고가 포함된 컨테이너를 요구

- 기업의 ESG 의무화로 인해 발송인은 일회용 팔레트 랩보다 재사용 가능한 멀티 모달 컨테이너를 요구하게 되어 교환 수요 증가

- 실시간의 위치 정보와 상태 데이터를 제공하는 IoT 대응 스마트 박스의 채용에 의해 프리미엄 유닛에 대한 발송인의 지불 의향 증가

- 구독 기반과 모듈형 하우징의 개념은 은퇴한 운송 컨테이너의 두 번째 라이프 전환에 박차

- 시장 성장 억제요인

- 유행 후 컨테이너 공급 과잉이 가동률을 저하시켜 신축 투자를 억제

- 열간 압연 코일 강재 가격의 난고 하에서 컨테이너 구매자에게 예산의 불확실성을 초래

- 요람으로부터 묘지까지의 규제 강화와 확대 생산자 책임(EPR) 규칙에 의한 평생 소유 비용의 팽창

- 접이식 및 접이식 대체 컨테이너의 급속한 출현이 기존의 단단한 상자에 대한 수요를 다짐

- 가치/공급망 분석

- 규제와 기술의 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 가격 분석 - 표준 컨테이너와 특수 컨테이너의 비교

- 스포트라이트 : 복합 일관 운송과 철도의 이용

- 세계의 컨테이너 상황

- 지정학적 이벤트가 시장에 미치는 영향

제5장 시장 규모와 성장 예측(금액, 수량)

- 사이즈별

- 20피트(TEU)

- 40피트(FEU)

- 40피트 하이큐브

- 기타(>45ft 등)

- 컨테이너 유형별

- 건식 저장(표준)

- 냉장(리퍼)

- 탱크(ISO 탱크, 극저온)

- 플랫랙 및 오픈탑

- 특수 용도(사이드 도어, 터널, 단열, 접이식)

- 재료별

- 코르텐 강판

- 스테인리스 강판

- 알루미늄 합금

- FRP 및 복합재

- 기타

- 산업별

- 소비재 및 소매

- 식음료

- 산업기계 및 자동차

- 화학 및 석유

- 제약 및 헬스케어

- 기타

- 운송 수단별

- 해상 운송

- 근해 및 연안 운송

- 철도 복합 운송

- 도로 내륙 운송 및 외부 저장

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 페루

- 칠레

- 아르헨티나

- 기타 남미

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아(싱가포르, 말레이시아, 태국, 인도네시아, 베트남, 필리핀)

- 기타 아시아태평양

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 노르딕스(덴마크, 핀란드, 아이슬란드, 노르웨이, 스웨덴)

- 기타 유럽

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향(M&A, 생산능력 확대, 임대 계약)

- 시장 점유율 분석

- 기업 프로파일

- China International Marine Containers(CIMC)

- Dong Fang International Containers

- CXIC Group(CSSC)

- Maersk Container Industry A/S

- Singamas Container Holdings

- W&K Container

- Sea Box Inc.

- TLS Offshore Containers

- Storstac Inc.

- CARU Containers BV

- China Eastern Containers

- Valisons & Co.

- YMC Container Solutions

- American Intermodal Container Manufacturing

- Triton International

- Textainer Group Holdings

- Florens Container Services

- CAI International

- Touax Group

- UES International

제7장 시장 기회와 전망

KTH 25.10.27The Shipping Containers Market size is estimated at USD 10.27 billion in 2025, and is expected to reach USD 12.77 billion by 2030, at a CAGR of 4.46% during the forecast period (2025-2030).

E-commerce fulfillment, pharmaceutical cold-chain expansion, and rising intermodal efficiency provide stable, structural demand. Containerization's role in handling 90% of global trade underpins this growth, while digital tracking tools and smarter designs help operators shorten port stays and boost asset turnover. Sustainability targets are pushing material innovation toward lighter composites, and alliance restructuring among carriers is reshaping capacity deployment strategies in favor of larger, technology-enabled fleets. Geopolitical disruptions add short-term volatility but also reinforce the importance of diversified trade lanes and dynamic routing.

Global Shipping Containers Market Trends and Insights

Explosive Growth of Cross-Border E-Commerce Creating 24-Hour Turnaround Expectations

E-commerce expansion drives more frequent, smaller shipments, shifting focus from vessel capacity toward port velocity. Carriers commit additional equipment to high-frequency loops, while ports invest in automated cranes that clear vessels inside one shift. Smart tracking allows shippers to pre-clear customs and book rail slots before docking. These operational gains shorten inventory cycles and reinforce preference for standard dry boxes, keeping utilization high even when trade volumes fluctuate. As online marketplaces penetrate emerging economies, the shipping container market sees sustained baseline demand across diverse trade lanes.

Worldwide Cold-Chain Penetration Accelerates Advanced Reefer Orders

Pharmaceutical producers are migrating long-haul shipments from air to ocean to cut costs and emissions without compromising temperature control. Modern reefers maintain +-0.5 °C accuracy and integrate telemetry that flags deviations in real time, allowing corrective actions mid-voyage. Fresh grocery exporters adopt similar technology to reach distant consumers with minimal spoilage. Manufacturers offering dual-fuel refrigeration units reduce energy consumption and meet low-GWP regulations, enabling higher price realisation per box. As grocery e-commerce extends to new markets, advanced reefer demand continues to outpace general cargo growth.

Post-Pandemic Oversupply of Boxes Eroding Utilization Rates

Record new builds made during 2021-2023 create a temporary surplus, pushing lease rates down and prompting operators to delay fresh orders. Idle inventories accumulate in gateway ports when trade softens, forcing depots to lower storage fees to attract repositioning business. Manufacturers adapt by trimming production shifts and redirecting capacity toward specialized designs with steadier demand. The correction is expected to resolve once scrappage catches up with ageing fleets and trade normalizes.

Other drivers and restraints analyzed in the detailed report include:

- Direct-to-Consumer Brands Demanding Bespoke, Logo-Printed Containers

- Corporate ESG Mandates Pushing Reusable Container Adoption

- Volatility in Hot-Rolled Coil Steel Prices Creating Budget Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-cube offerings are capturing incremental demand because their 13% extra headroom maximizes volumetric loads such as e-commerce parcels and lightweight consumer electronics. 40-ft formats generated 52.64% revenue in 2024, demonstrating entrenched popularity for ocean freight, whereas 40-ft high-cube units are forecast to grow at 5.61% CAGR to 2030. The shipping container market size for high-cube units reflects shipper preference for greater capacity without breaching weight restrictions.

Port infrastructure upgrades accommodate taller stacks, and terminal operators add reach-stackers with extended lifting heights to handle these units efficiently. Logistics integrators promote standardization on the 40-ft profile to streamline rail wagon allocation and depot interchange. Triton Containers markets high-cube leases with flexible pick-up options to reduce repositioning, reinforcing adoption. Overall, shipper focus on cubic efficiency and consolidation of packaging drives continued high-cube traction across primary trade corridors.

Dry storage boxes accounted for 72.75% of 2024 shipments, underscoring their status as the backbone of global commodity flows. In contrast, reefer units record a 6.42% CAGR to 2030 as fresh produce exporters and drug makers scale ocean routes. Refrigerated boxes currently represent the premium slice of the shipping container market, commanding rental rates two to three times higher than dry units.

Technology upgrades include variable-speed compressors and solar-assisted power modules that cut energy draw during idle periods. Pharmaceutical shippers require redundant temperature probes and door sensors that trigger alerts within seconds of deviation, driving differentiation among manufacturers. Reefers also benefit from decarbonization, as shifting temperature-sensitive goods from air to sea avoids up to 80% of related emissions.

The Shipping Container Market is Segmented by Size (20-Ft (TEU), 40-Ft (FEU) and More), by Container Type (Dry Storage (Standard), Refrigerated, and More), by Material (Corten Steel, Stainless Steel and More), End-Use Industry (Consumer Goods & Retail and More), by Mode of Transport (Maritime Deep-Sea and More), by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 60.50% revenue in 2024 and is set to grow at a 5.67% CAGR to 2030. China retains manufacturing leadership, yet Southeast Asia captures incremental volumes as firms diversify sourcing. Malaysian and Indian mega-port projects add more than 25 million TEU of annual capacity, anchoring regional throughput and stimulating container demand across feeder networks. Currency stability and supportive trade agreements also encourage regional leasing pools to expand their fleets.

North America benefits from nearshoring that shifts electronics and automotive assembly closer to consumption markets. United States port authorities approve multi-billion-dollar dredging and berth electrification programs, enhancing competitiveness against Mexican and Canadian gateways. The rail intermodal build-out across the Midwest unlocks cost-effective land bridges that connect Atlantic and Pacific basins in under eight days, driving uptake of stack-train compatible container designs.

Europe records mixed growth as geopolitical tensions divert Asia-Europe sailings around Africa, extending transit times but also directing additional calls to Mediterranean hubs. Investments in automation at London Gateway and Rotterdam Maasvlakte raise throughput per crane hour, cushioning cost-per-box metrics. Stringent environmental regulations accelerate the retirement of older, heavier boxes in favor of recycled-content steel units, supporting replacement demand despite subdued trade volume growth.

- China International Marine Containers (CIMC)

- Dong Fang International Containers

- CXIC Group (CSSC)

- Maersk Container Industry A/S

- Singamas Container Holdings

- W&K Container

- Sea Box Inc.

- TLS Offshore Containers

- Storstac Inc.

- CARU Containers B.V.

- China Eastern Containers

- Valisons & Co.

- YMC Container Solutions

- American Intermodal Container Manufacturing

- Triton International

- Textainer Group Holdings

- Florens Container Services

- CAI International

- Touax Group

- UES International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of cross-border e-commerce creating 24-hour turnaround expectations for standard dry containers.

- 4.2.2 Worldwide cold-chain penetration of fresh grocery and meal-kit delivery accelerating orders for advanced reefer boxes.

- 4.2.3 Direct-to-consumer (D2C) brands demanding bespoke, logo-printed containers to double as mobile pop-up stores and fulfilment hubs.

- 4.2.4 Corporate ESG mandates pushing shippers toward reusable, multimodal containers over single-use pallet wrap, lifting replacement demand.

- 4.2.5 Adoption of IoT-enabled -smart- boxes providing real-time location & condition data, raising shipper's willingness to pay for premium units.

- 4.2.6 Subscription-based and modular housing concepts spurring second-life conversions of retired shipping containers.

- 4.3 Market Restraints

- 4.3.1 Post-pandemic oversupply of boxes eroding utilisation rates and discouraging new-build investment.

- 4.3.2 Volatility in hot-rolled coil steel prices creating budget uncertainty for container purchasers.

- 4.3.3 Stricter cradle-to-grave regulations and extended-producer-responsibility (EPR) rules inflating lifetime ownership costs.

- 4.3.4 Rapid emergence of foldable and collapsible container alternatives cannibalising demand for conventional rigid boxes.

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Pricing Analysis - Standard vs. Special Containers

- 4.8 Spotlight: Intermodal & Rail Uptake

- 4.9 Global Container Leasing Landscape

- 4.10 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts (Value, Volume)

- 5.1 By Size

- 5.1.1 20-ft (TEU)

- 5.1.2 40-ft (FEU)

- 5.1.3 40-ft High-Cube,

- 5.1.4 Others ( >45-ft, etc)

- 5.2 By Container Type

- 5.2.1 Dry Storage (Standard)

- 5.2.2 Refrigerated (Reefer)

- 5.2.3 Tank (ISO Tank, Cryogenic)

- 5.2.4 Flat-Rack & Open-Top

- 5.2.5 Special Purpose (Side-Door, Tunnel, Insulated, Collapsible)

- 5.3 By Material

- 5.3.1 Corten Steel

- 5.3.2 Stainless Steel

- 5.3.3 Aluminium Alloy

- 5.3.4 FRP & Composite

- 5.3.5 Others

- 5.4 By End-Use Industry

- 5.4.1 Consumer Goods & Retail

- 5.4.2 Food & Beverage

- 5.4.3 Industrial Machinery & Automotive

- 5.4.4 Chemicals & Petroleum

- 5.4.5 Pharmaceuticals & Healthcare

- 5.4.6 Others

- 5.5 By Mode of Transport

- 5.5.1 Maritime Deep-Sea

- 5.5.2 Short-Sea & Coastal

- 5.5.3 Rail Intermodal

- 5.5.4 Road Inland Haulage & Off-Site Storage

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab of Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Capacity Expansion, Leasing Deals)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 China International Marine Containers (CIMC)

- 6.4.2 Dong Fang International Containers

- 6.4.3 CXIC Group (CSSC)

- 6.4.4 Maersk Container Industry A/S

- 6.4.5 Singamas Container Holdings

- 6.4.6 W&K Container

- 6.4.7 Sea Box Inc.

- 6.4.8 TLS Offshore Containers

- 6.4.9 Storstac Inc.

- 6.4.10 CARU Containers B.V.

- 6.4.11 China Eastern Containers

- 6.4.12 Valisons & Co.

- 6.4.13 YMC Container Solutions

- 6.4.14 American Intermodal Container Manufacturing

- 6.4.15 Triton International

- 6.4.16 Textainer Group Holdings

- 6.4.17 Florens Container Services

- 6.4.18 CAI International

- 6.4.19 Touax Group

- 6.4.20 UES International

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment