|

시장보고서

상품코드

1836488

이탈리아의 영상 진단 장비 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Italy Diagnostic Imaging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

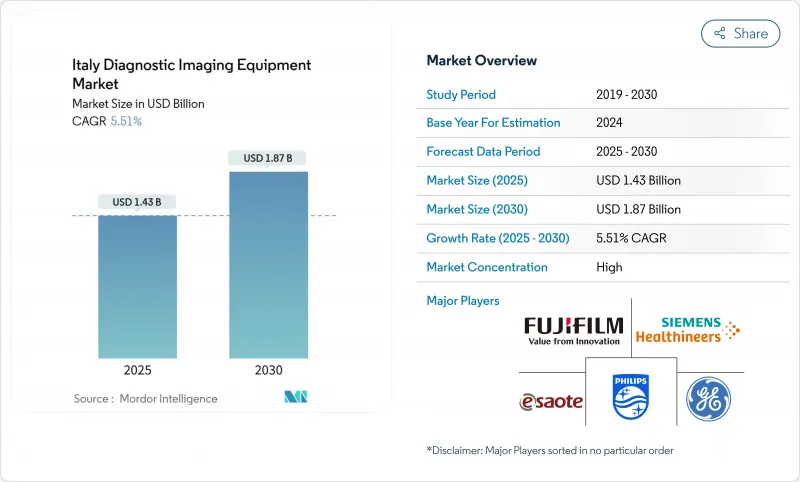

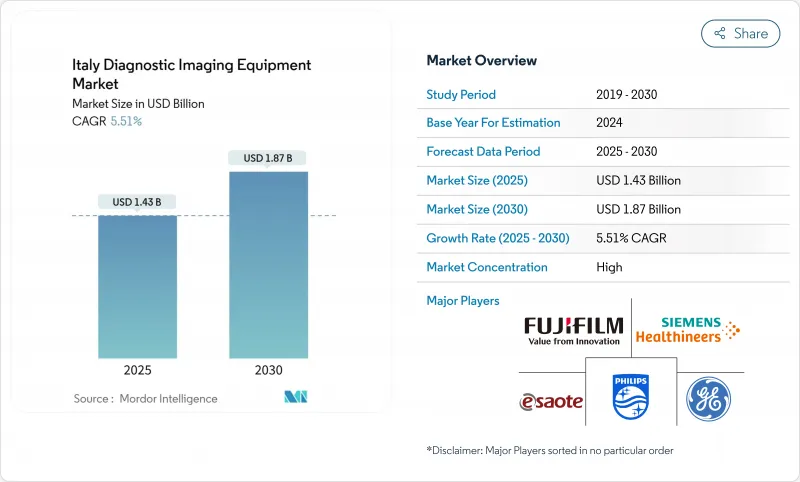

이탈리아의 영상 진단 장비 시장 규모는 2025년에 14억 3,000만 달러에 달하고, 2030년에는 18억 7,000만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 5.51%를 나타낼 전망입니다

국가부흥강인화계획(PNRR)과 민간투자에 의해 충당되는 용량의 업그레이드는 기기의 교환 사이클과 디지털 접속을 가속화하고 있습니다. 인구의 고령화, 암이나 심혈관질환의 고부담, 화상판독을 위한 인공지능(AI)의 채용이 진행됨에 따라 수요가 강화됩니다. 벤더는 검사 시간을 단축하고 새로운 POC(Point-of-Care) 워크플로우에 적합한 포톤 카운팅 CT, 오픈 아키텍처 MRI, 모바일 X선 시스템으로 대응하고 있습니다. 2025년에 도입되는 지역 수렴 정책과 전국 일률 요금에 의해 지금까지 충분한 서비스를 받지 못했던 남부의 주에서의 검사 건수가 증가할 것으로 예상되는 한편, 이탈리아의 광대한 민간 진단 네트워크에 의한 호스피탈리티가, 자비 진료나 국경을 넘은 환자를 계속 끌어들이고 있습니다.

이탈리아의 영상 진단 장비 시장 동향과 인사이트

인구 역학의 고령화와 만성 질환 이환율 상승

65세 이상의 고령자는 2050년까지 24%에서 34%로 증가할 것으로 예상되며 암, 심장병, 근골격계 질환에 대한 멀티모달리티에 따른 후속 조치가 추진됩니다. 병원의 방사선 부서는 높은 처리량 CT 스캐너, 와이드 보어 MRI 및 반복 재구성 소프트웨어가 선호되는 검사의 복잡성을 보고합니다. 워크플로우의 자동화와 환자의 편안함 기능은 허약한 환자가 더 긴 포지셔닝 시간을 필요로 하기 때문에 우선합니다. 저선량 프로토콜과 신속한 이미지 재구성을 결합한 공급업체는 영상 진단 장비 시장에서 경쟁력을 얻고 있습니다.

헬스케어 근대화를 위한 대규모 정부·EU 부흥 기금

PNRR은 3,100개의 레거시 시스템을 교체하고, 280개의 응급 부서를 디지털화하기 위한 자금을 확보하며, 사이버 보안 상호 운용성을 보장할 수 있는 프리미엄 벤더에게 이익을 주는 집중적인 장비 구매 사이클을 유도합니다. 남부 병원은 평균을 초과하는 예산 배분을 받고 역사적인 남북 기술 격차가 축소됩니다. 공공 입찰은 AI 지원 아키텍처, 원격 서비스 진단, 에너지 절약 대기 모드를 제공하는 시스템을 선호하며 이탈리아의 영상 진단 장비 시장 전반에 걸쳐 고품질의 교체를 강화했습니다.

영상 진단 장비와 절차의 높은 비용

의료비의 자기 부담액은 2023년에 10.3% 증가하여 450만명의 국민이 비용을 이유로 의료를 받지 않게 되었습니다. 소규모 병원의 설비 예산은 추천되는 5-7년의 임베디드 사이클에 뒤쳐져 있어, 하이엔드 MRI나 하이브리드 스캐너 수요를 억제하고 있습니다. 서비스 계약, 소프트웨어 업그레이드 및 에너지 비용은 재정적 부담을 증가시키고 이탈리아 영상 진단 장비 시장의 일부에서 구매력을 제한하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 멀티 모달 이미징의 급속한 기술적 획기적인

- POC(Point-of-Care), 휴대용, 모바일 이미징 플랫폼의 보급 확대

- 규제, 상환, 공공 입찰 절차에 시간이 걸립니다.

부문 분석

X선은 보편적인 임상사용과 경제적인 운영비용에 힘입어 2024년 30.84%의 점유율을 유지했습니다. 디지털 X선 촬영장치의 업그레이드가 필름 시스템으로 대체되고 있으며, 이탈리아의 영상 진단 장비 시장에서 안정적인 교체 수요를 확보하고 있습니다. 첨단 검출기와 선량 감소 알고리즘은 화질을 향상시켜 규제 준수를 용이하게 합니다.

한편 MRI는 오픈 보어 시스템이 폐소 공포증을 경감하고 3T 플랫폼이 스캔 시간을 단축하기 때문에 CAGR 7.28%를 나타낼 전망입니다. Esaote의 Magnifico Open은 2023년 매출을 3.3% 증가시켰습니다. 신경 종양학, 근골격계 스포츠 부상, 심장의 바이어빌리티 검사가 임상 적응을 확대해, 이탈리아 영상 진단 장비 시장의 MRI 슬라이스를 병원·민간 불문하고 확대시켰습니다.

고정 장치는 2024년 매출의 81.79%를 차지하며, PACS 및 병원 정보 시스템과 통합된 고처리량 CT, MRI, 앤지오 스위트가 중심이 되었습니다. PNRR 예산은 동급 장비 교체를 선호하며 이탈리아 영상 진단 장비 시장의 이 부문에서 단기 안정성을 보장합니다.

모바일 및 핸드헬드 기기는 CAGR 6.92%를 나타낼 전망입니다. 무선 초음파 프로브와 바퀴가 달린 DR 카트는 ICU 및 응급실에서 서지 용량을 지원합니다. 그 유연성은 호스피탈 앳 홈 등 진화하는 케어 모델에 맞추어 중량, 배터리 수명, 화질을 최적화하는 벤더의 이탈리아의 영상 진단 장비 시장 점유율을 확대합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 인구동태의 고령화와 만성질환 이환율의 상승

- 헬스케어 근대화를 위한 대규모 정부·EU 부흥 지원금

- 멀티 모달 이미징의 급속한 기술 혁신

- POC(Point-of-Care), 휴대용, 모바일 이미징 플랫폼 증가

- 정밀의료, 예방 의료, 가치에 근거한 의료 모델의 중시의 고조

- 민간 진단 및 외래 영상 진단 네트워크의 확대

- 시장 성장 억제요인

- 영상 진단 장비와 수술의 고비용

- 규제, 상환, 공적 입찰 수속의 장기화

- 유자격의 방사선기사와 검사기사의 지속적인 부족

- 화상 진단 인프라의 이용과 액세스에 있어서의 지역 격차

- 가격 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(금액)

- 모달리티별

- MRI

- 컴퓨터 단층 촬영

- 초음파

- X선

- 핵의학 영상(PET/SPECT)

- 형광 투시

- 유방촬영술

- 이동성별

- 고정식 시스템

- 이동형 및 휴대형 시스템

- 용도별

- 심장학

- 종양학

- 신경학

- 정형외과

- 위장관학

- 산부인과

- 기타 용도

- 최종 사용자별

- 병원

- 진단 영상 센터

- 외래 수술 센터(ASC)

- 기타 최종 사용자

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Siemens Healthineers AG

- Koninklijke Philips NV

- GE HealthCare

- Canon Medical Systems Corporation

- Fujifilm Holdings Corporation

- Esaote SpA

- Italray SRL

- Gilardoni SpA

- Hologic Inc.

- Carestream Health

- Agfa-Gevaert Group

- SAMSUNG(SamsungHealthcare.com)

- Shimadzu Corporation

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd

- Bracco Imaging SpA

- GMM Group

- Villa Sistemi Medicali Spa

- Guerbet SA

제7장 시장 기회와 전망

KTH 25.10.27The Italy diagnostic imaging equipment market size is estimated at USD 1.43 billion in 2025, and is expected to reach USD 1.87 billion by 2030, at a CAGR of 5.51% during the forecast period (2025-2030).

Capacity upgrades financed by the National Recovery and Resilience Plan (PNRR) and private-sector investments are accelerating equipment replacement cycles and digital connectivity. Demand is reinforced by population aging, the high burden of oncological and cardiovascular diseases, and progressive adoption of artificial intelligence (AI) for image interpretation. Vendors respond with photon-counting CT, open-architecture MRI, and mobile X-ray systems that shorten exam times and fit emerging point-of-care workflows. Regional convergence policies and uniform national tariffs introduced in 2025 are expected to lift procedure volumes in historically underserved Southern provinces, while the hospitality of Italy's sprawling private diagnostics network continues to attract self-pay and cross-border patients.

Italy Diagnostic Imaging Equipment Market Trends and Insights

Demographic Aging and Escalating Chronic-Disease Incidence

Citizens aged >=65 are expected to climb from 24% to 34% by 2050, driving multi-modality follow-up for cancers, heart disease, and musculoskeletal conditions. Hospital radiology departments report increasing examination complexity that favors higher-throughput CT scanners, wide-bore MRI, and iterative reconstruction software. Workflow automation and patient-comfort features gain priority as frail patients require longer positioning times. Vendors that combine low-dose protocols with rapid image reconstruction gain a competitive edge in the Italy diagnostic imaging equipment market.

Large-Scale Government & EU Recovery Funding for Healthcare Modernization

The PNRR sets aside funds to replace 3,100 legacy systems and digitalize 280 emergency departments, triggering a concentrated equipment buying cycle that benefits premium vendors able to guarantee cyber-secure interoperability. Southern hospitals receive above-average budget shares, narrowing the historic North-South technology gap. Public tenders favor systems offering AI-ready architectures, remote service diagnostics, and energy-saving standby modes, reinforcing high-spec replacements across the Italy diagnostic imaging equipment market.

High Cost of Imaging Equipment & Procedures

Out-of-pocket healthcare spending rose 10.3% in 2023, and 4.5 million citizens skipped care due to cost. Capital budgets in smaller hospitals lag behind recommended five-to-seven-year replacement cycles, suppressing demand for high-end MRI and hybrid scanners. Service contracts, software upgrades, and energy costs compound financial strain, limiting purchasing power in parts of the Italy diagnostic imaging equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Technological Breakthroughs in Multimodal Imaging

- Rising Uptake of Point-of-Care, Portable and Mobile Imaging Platforms

- Lengthy Regulatory, Reimbursement and Public-Tender Procedures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

X-ray retained 30.84% share in 2024, underpinned by universal clinical use and economical operating costs. Digital radiography upgrades continue to replace film systems, securing steady replacement demand within the Italy diagnostic imaging equipment market. Advanced detectors and dose-reduction algorithms enhance image quality while easing regulatory compliance.

MRI, however, is set to grow at a 7.28% CAGR as open-bore systems reduce claustrophobia and 3 T platforms shorten scan times. Esaote's Magnifico Open drove a 3.3% sales increase in 2023. Neuro-oncology, musculoskeletal sports injuries, and cardiac viability studies widen clinical indications, elevating the MRI slice of the Italy diagnostic imaging equipment market size for hospital and private settings alike.

Fixed units held 81.79% of 2024 revenues, anchored by high-throughput CT, MRI, and angio suites that integrate with PACS and hospital information systems. PNRR budgets prioritize like-for-like replacements, ensuring short-term stability in this segment of the Italy diagnostic imaging equipment market.

Mobile and handheld devices are scaling at 6.92% CAGR. Wireless ultrasound probes and wheeled DR carts support surge capacity in ICUs and emergency departments. Their flexibility aligns with evolving care models such as hospital-at-home, expanding the Italy diagnostic imaging equipment market share for vendors that optimize weight, battery life, and image quality.

The Italy Diagnostic Imaging Equipment Market Report is Segmented by Modality (MRI, Computed Tomography, Ultrasound, X-Ray, Nuclear Imaging (PET / SPECT), Fluoroscopy and Mammography), Portability (Fixed Systems and Mobile and Hand-Held Systems), Application (Cardiology, Oncology, Neurology, and More), and End-User (Hospitals, Diagnostic Imaging Centres, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Siemens Healthineers

- Koninklijke Philips

- GE Healthcare

- Canon

- FUJIFILM

- Esaote

- Italray

- Gilardoni SpA

- Hologic

- Carestream Health

- Agfa-Gevaert

- SAMSUNG (SamsungHealthcare.com)

- Shimadzu

- Mindray

- Bracco

- GMM Group

- Villa Sistemi Medicali Spa

- Guerbet SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demographic ageing and escalating chronic-disease incidence

- 4.2.2 Large-scale government & EU recovery funding for healthcare modernization

- 4.2.3 Rapid technological breakthroughs in multimodal imaging

- 4.2.4 Rising uptake of point-of-care, portable and mobile imaging platforms

- 4.2.5 Growing emphasis on precision, preventive and value-based care models

- 4.2.6 Expansion of private diagnostics and outpatient imaging networks

- 4.3 Market Restraints

- 4.3.1 High cost of imaging equipment & procedures

- 4.3.2 Lengthy regulatory, reimbursement and public-tender procedures

- 4.3.3 Persistent shortage of qualified radiologists and technologists

- 4.3.4 Regional disparities in imaging infrastructure utilization and access

- 4.4 Pricing Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Modality

- 5.1.1 MRI

- 5.1.2 Computed Tomography

- 5.1.3 Ultrasound

- 5.1.4 X-Ray

- 5.1.5 Nuclear Imaging (PET/SPECT)

- 5.1.6 Fluoroscopy

- 5.1.7 Mammography

- 5.2 By Portability

- 5.2.1 Fixed Systems

- 5.2.2 Mobile and Hand-held Systems

- 5.3 By Application

- 5.3.1 Cardiology

- 5.3.2 Oncology

- 5.3.3 Neurology

- 5.3.4 Orthopedics

- 5.3.5 Gastroenterology

- 5.3.6 Gynecology & Obstetrics

- 5.3.7 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Siemens Healthineers AG

- 6.3.2 Koninklijke Philips N.V.

- 6.3.3 GE HealthCare

- 6.3.4 Canon Medical Systems Corporation

- 6.3.5 Fujifilm Holdings Corporation

- 6.3.6 Esaote SpA

- 6.3.7 Italray SRL

- 6.3.8 Gilardoni SpA

- 6.3.9 Hologic Inc.

- 6.3.10 Carestream Health

- 6.3.11 Agfa-Gevaert Group

- 6.3.12 SAMSUNG (SamsungHealthcare.com)

- 6.3.13 Shimadzu Corporation

- 6.3.14 Shenzhen Mindray Bio-Medical Electronics Co., Ltd

- 6.3.15 Bracco Imaging SpA

- 6.3.16 GMM Group

- 6.3.17 Villa Sistemi Medicali Spa

- 6.3.18 Guerbet SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment