|

시장보고서

상품코드

1836495

프랑스의 약물전달 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)France Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

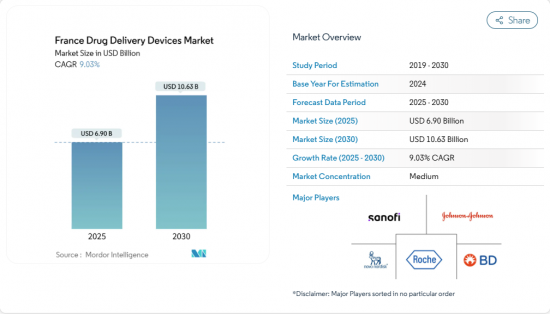

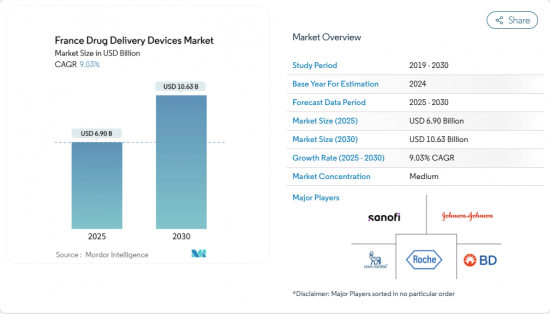

프랑스의 약물전달 기기 시장 규모는 2025년에 69억 달러에 이르고, CAGR 9.03%를 나타내 2030년에는 106억 3,000만 달러로 확대될 것으로 예측됩니다.

급속한 확장은 연결 장치의 혁신, 생물학적 제제 및 바이오시밀러 치료의 성장, 자기 투여를 장려하는 국가의 전자 건강 프로그램에 의해 촉진됩니다. 제조업체는 프랑스의 견고한 개발 제조 위탁 기관(CDMO) 생태계에서 기세를 얻고 있으며 만성 질환의 높은 유병률이 안정적인 수요를 지원합니다. 복잡한 가격 설정과 EU 의료기기 규제(MDR)의 준수가 여전히 현저한 장애가 되고 있는 것, 디지털 기기에 대한 조기 상환 패스웨이 등의 규제면의 이니셔티브는 시장 투입까지의 시간을 단축합니다. 이러한 요인들이 결합되어 프랑스의 약물전달 기기 시장은 유럽의 주요 성장 엔진으로 자리매김하고 있습니다.

프랑스의 약물전달 기기 시장 동향과 인사이트

홈케어와 자기투여로 이동

프랑스는 재택 관리를 선호하고 있으며, 최종 사용자 부문은 이미 13.03%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 2만 1,000개의 약국에서 판매되는 Sanofi의 Solosmart 센서는 인슐린 주사 기록을 캡처하여 환자용 앱과 원활하게 통합합니다. Sanofi의 Solosmart 센서는 2만 1,000개의 약국에서 판매되며 인슐린 주사 기록을 얻고 환자 앱과 원활하게 통합합니다. 이러한 장치는 사용성과 데이터 연결성을 약리적 성능과 동일한 수준으로 높여 경쟁을 재정의하여 프랑스 약물전달 기기 시장의 채택을 촉진합니다.

생물학적 제형 및 바이오시밀러 주사제 확대

고점도의 생물 제제에는 특수한 전달 형식이 필요합니다. 노보놀 디스크는 샤르트르 공장에 21억 유로를 투자하여 인슐린 생산 능력을 두 배로 늘렸습니다. BD의 Neopak XtraFlow 주사기는 이러한 제형을 목표로 하고 있으며, 제약 제조업체와 기기 제조업체의 공동 혁신을 두드러지게 하고 있습니다. 성장하는 생물학적 제형의 파이프라인은 프랑스의 약물전달 기기 시장, 특히 자체 주사기와 웨어러블 펌프의 지속적인 수요를 보장합니다.

복잡한 상환 가격 상한

프랑스에서는 의료기기와 서비스의 지불에 차이를 두고 판매자의 마진에 상한을 마련하고 있기 때문에 승인으로부터 상환까지의 평균 기간이 12.9개월로, 스위스의 6개월, 독일의 7.4개월에 비해 길어지고 있습니다. SMR/ASMR 스코어링 방식은 낮은 베네핏 제품을 보험 적용에서 제외할 수 있어 콤비네이션 기기의 매출을 감속시키고 프랑스의 약물전달 시장의 성장을 억제하고 있습니다.

부문 분석

주사제는 2024년에 45.34%의 점유율을 유지하여 안정적인 생물학적 제제의 사용과 프리필드 주사기와 자동 주사기의 지속적인 업그레이드에 지지되었습니다. Pharmapack2025에 전시된 BD의 RFID 지원 iDFill 주사기는 추적성과 환자의 안전성에 중점을 두고 있음을 강조합니다. 이러한 리드에도 불구하고, 이식형 주사기는 2030년까지 연평균 복합 성장률(CAGR) 11.89%를 나타낼 것으로 예상되고 있습니다. 이것은 투여 간격을 길게 하고 싶은 환자의 선호와 세마글루티드의 투여를월1회의 스케줄로 확대하는 하이드로겔 저장소의 출현을 반영합니다. 이 기세로 이식형은 프랑스의 약물전달 시장에서 파괴적인 힘을 가지고 있습니다.

경피 패치, 안구 삽입제, 비강 시스템은 치료 옵션을 확장합니다. 화이자가 편두통 치료제로 승인한 Zabspre 스프레이로 대표되는 비강내 투여는 호흡기 치료 이외에도 유용성이 확대되고 있습니다. 이러한 추가적인 모달리티는 장치의 다양성을 강화하고 프랑스의 약물전달 시장 전체의 회복력을 강화하고 있습니다.

주사제는 2024년 프랑스 약물전달 기기 시장 규모의 58.12%를 차지하며 만성 질환의 정밀 투여에 지지되었습니다. 주사 바늘의 지속적인 개선은 사용감을 향상시키고 병원과 가정 환경 모두에서 정착을 강화합니다.

흡입은 2025-2030년의 CAGR이 9.56%를 나타낼 예정입니다. 흡입 생물 제제에 관한 Chiesi-Affibody와 같은 파트너십을 통해 호흡기 영역의 포트폴리오가 확대되었습니다. 프랑스의 신흥 기업인 Lovaltech는 France 2030의 자금 지원에 따라 비강 백신 플랫폼을 개발하고 있습니다. 이러한 진보는 치료의 시야를 넓히고 프랑스 약물전달 기기 시장의 지속적인 성장으로 이어집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 재택 의료 환경와 자기 투여로의 변화

- 생물학적 제제·바이오시밀러 주사제의 확대

- 커넥티드 기기를 가속시키는 기술의 진보와 e헬스 전략

- 견고한 CDMO와 기기 제조 에코시스템

- 만성질환이 높은 부담

- 약물전달 기기 수요를 촉진하는 개혁과 규제의 지원

- 시장 성장 억제요인

- 복잡한 상환 가격의 상한

- 엄격한 규제 프레임워크

- 다양한 기기와 관련된 제한 및 위험

- 약물전달 기기의 조합의 가격에 영향을 미치는 병원의 입찰의 세분화와 제네릭 의약품에 관한 문제

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 기기 유형별

- 주사 투여 기기

- 흡입 투여 기기

- 주입 펌프

- 경피 패치

- 이식형 약물전달 시스템

- 안구 삽입물 및 투여 임플란트

- 비강 및 구강 점막 투여 기기

- 투여 경로별

- 주사제

- 흡입제

- 경피제

- 구강 점막제(구강 및 설하)

- 안구제

- 비강제

- 용도별

- 당뇨병

- 종양학

- 심혈관 질환

- 호흡기 질환

- 감염성 질환

- 자가면역 및 염증성 질환

- 중추 신경계 장애

- 최종 사용자별

- 병원

- 외래 수술 및 전문 클리닉

- 재택 의료 환경/자가 사용

- 소매 및 온라인 약국

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Sanofi

- Becton, Dickinson and Company

- F. Hoffmann-La Roche AG

- Novo Nordisk A/S

- Johnson & Johnson

- Solventum

- Baxter International Inc.

- Bayer AG

- Pfizer Inc.

- Terumo Corporation

- Gerresheimer AG

- Nemera

- AptarGroup, Inc.

- West Pharmaceutical Services

- Ypsomed AG

- Vetter Pharma-Fertigung

- B. Braun Melsungen AG

- Owen Mumford Ltd.

- Insulet Corporation

- Tandem Diabetes Care

- Eli Lilly and Company

- Recipharm AB

- Unither Pharmaceuticals

제7장 시장 기회와 전망

KTH 25.11.04The France drug delivery devices market size stands at USD 6.90 billion in 2025 and is projected to rise to USD 10.63 billion by 2030, reflecting a 9.03% CAGR.

Rapid expansion is fueled by connected-device innovation, growth in biologic and biosimilar therapies, and national e-health programs that encourage self-administration. Manufacturers gain momentum from France's robust contract development and manufacturing organization (CDMO) ecosystem, while high chronic-disease prevalence sustains steady demand. Regulatory initiatives such as early reimbursement pathways for digital devices shorten time to market, although complex pricing caps and EU Medical Device Regulation (MDR) compliance remain notable obstacles. Together, these factors position the France drug delivery devices market as a key growth engine within Europe.

France Drug Delivery Devices Market Trends and Insights

Shift to Home-Based Care & Self-Administration

France is prioritizing homecare, and the end-user segment already shows a 13.03% CAGR, the highest across settings. The National eHealth Roadmap (2023-2027) backs connected devices that transmit real-time dosing data and support remote consultations.Sanofi's Solosmart sensor, available in 21,000 pharmacies, captures insulin injection records and integrates seamlessly with patient apps. Such devices redefine competition by elevating usability and data connectivity to the same level as pharmacological performance, driving France drug delivery devices market adoption.

Expansion of Biologic & Biosimilar Injectables

High-viscosity biologics need specialized delivery formats. Novo Nordisk invested €2.1 billion in its Chartres site to double insulin capacity. BD's Neopak XtraFlow syringe targets these formulations, highlighting collaborative innovation between pharma and device makers. Growing biologic pipelines ensure sustained demand in the France drug delivery devices market, particularly for self-injectors and wearable pumps.

Complex Reimbursement Price Caps

France differentiates device and service payments and caps distributor margins, extending the average approval-to-reimbursement period to 12.9 months, compared with 6 months in Switzerland and 7.4 months in Germany. The SMR/ASMR scoring method can exclude low-benefit products from coverage, slowing revenue for combination devices and tempering growth within the France drug delivery devices market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements and e-Health Strategy

- Robust CDMO & Device Manufacturing Ecosystem

- Stringent Regulatory Framework

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Injectables retained 45.34% share in 2024, supported by steady biologic usage and continuous upgrades in prefilled syringes and autoinjectors. BD's RFID-enabled iDFill syringe shown at Pharmapack 2025 underscores a focus on traceability and patient safety. Despite this lead, implantables are forecast to rise at 11.89% CAGR to 2030, reflecting patient preference for longer dosing intervals and emerging hydrogel reservoirs that stretch semaglutide dosing to monthly schedules. This momentum positions implantables as a disruptive force inside the France drug delivery devices market.

Transdermal patches, ocular inserts, and intranasal systems broaden therapeutic choices. The nasal route, highlighted by Pfizer's approved Zavzpret spray for migraine, demonstrates expanding utility beyond respiratory therapy. These additive modalities bolster device diversity and reinforce overall resilience of the France drug delivery devices market.

Injectables accounted for 58.12% of France drug delivery devices market size in 2024, favored for precision dosing across chronic illnesses. Continuous needle-design refinements improve user comfort, strengthening retention in both hospital and home settings.

Inhalation is slated for 9.56% CAGR between 2025-2030. Partnerships such as Chiesi-Affibody on inhaled biologics widen respiratory portfolios. Nasal delivery gains traction for central nervous system targets; French start-up Lovaltech advances an intranasal vaccine platform under France 2030 funding. These advances expand treatment horizons and feed sustained growth within the France drug delivery devices market.

France Drug Delivery Devices Market Report is Segmented by Device Type (Injectable Delivery Devices, Inhalation Delivery Devices, Infusion Pumps and More), Route of Administration (Injectable, Inhalational, Transdermal and More), Application (Diabetes, Oncology, Cardiovascular Diseases and More), End User (Hospitals, Ambulatory Surgical & Specialty Clinics and More). The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Sanofi

- Beckton Dickinson

- Roche

- Novo Nordisk

- Johnson & Johnson

- Solventum

- Baxter

- Bayer

- Pfizer

- Terumo

- Gerresheimer

- Nemera

- AptarGroup, Inc.

- West Pharmaceutical Services

- Ypsomed

- Vetter Pharma-Fertigung

- B. Braun

- Owen Mumford

- Insulet

- Tandem Diabetes Care

- Eli Lilly and Company

- Recipharm

- Unither Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Home-Based Care & Self-Administration

- 4.2.2 Expansion of Biologic & Biosimilar Injectables

- 4.2.3 Technological Advancements and e-Health Strategy Accelerating Connected Devices

- 4.2.4 Robust CDMO & Device Manufacturing Ecosystem

- 4.2.5 High Burden of Chronic Diseases

- 4.2.6 Supporting Reforms and Regulations Fueling Demand for Drug Delivery Device

- 4.3 Market Restraints

- 4.3.1 Complex Reimbursement Price Caps

- 4.3.2 Stringent Regulatory Framework

- 4.3.3 Limitations Associated with Different Devices and Risks

- 4.3.4 Issues Related to Fragmented Hospital Tendering and Generics Affecting Price of Drug Device Combination

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Injectable Delivery Devices

- 5.1.2 Inhalation Delivery Devices

- 5.1.3 Infusion Pumps

- 5.1.4 Transdermal Patches

- 5.1.5 Implantable Drug Delivery Systems

- 5.1.6 Ocular Inserts & Delivery Implants

- 5.1.7 Nasal & Buccal Delivery Devices

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Inhalation

- 5.2.3 Transdermal

- 5.2.4 Oral Mucosal (Buccal & Sublingual)

- 5.2.5 Ocular

- 5.2.6 Nasal

- 5.3 By Application

- 5.3.1 Diabetes

- 5.3.2 Oncology

- 5.3.3 Cardiovascular Diseases

- 5.3.4 Respiratory Diseases

- 5.3.5 Infectious Diseases

- 5.3.6 Auto-Immune & Inflammatory Disorders

- 5.3.7 CNS Disorders

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical & Specialty Clinics

- 5.4.3 Homecare Settings / Self-Use

- 5.4.4 Retail & Online Pharmacies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sanofi

- 6.4.2 Becton, Dickinson and Company

- 6.4.3 F. Hoffmann-La Roche AG

- 6.4.4 Novo Nordisk A/S

- 6.4.5 Johnson & Johnson

- 6.4.6 Solventum

- 6.4.7 Baxter International Inc.

- 6.4.8 Bayer AG

- 6.4.9 Pfizer Inc.

- 6.4.10 Terumo Corporation

- 6.4.11 Gerresheimer AG

- 6.4.12 Nemera

- 6.4.13 AptarGroup, Inc.

- 6.4.14 West Pharmaceutical Services

- 6.4.15 Ypsomed AG

- 6.4.16 Vetter Pharma-Fertigung

- 6.4.17 B. Braun Melsungen AG

- 6.4.18 Owen Mumford Ltd.

- 6.4.19 Insulet Corporation

- 6.4.20 Tandem Diabetes Care

- 6.4.21 Eli Lilly and Company

- 6.4.22 Recipharm AB

- 6.4.23 Unither Pharmaceuticals

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment