|

시장보고서

상품코드

1836513

가성소다 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Caustic Soda - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

멤브레인 셀 부문은 2024년 생산량의 대부분을 차지하고, 가성소다 시장 점유율의 85%를 차지하고, 다이어프램 셀은 2030년까지 연평균 복합 성장률(CAGR) 5.12%로 확대됩니다.

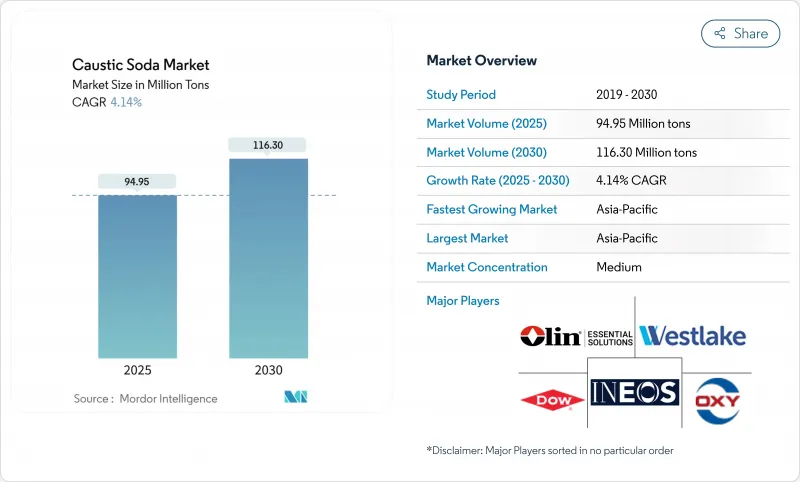

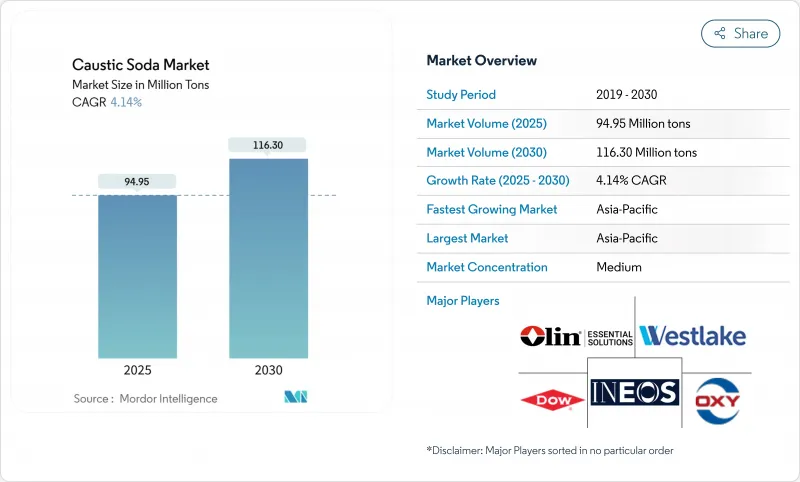

세계 가성소다 수요는 2025년에 9,495만 톤이 되고, 2030년에는 1억 1,630만 톤에 이를 것으로 예측되며, 2025-2030년의 CAGR은 4.14%로 예상됩니다. 견조한 성장은 알루미나 정제, 유기 화학 합성, 펄프 및 제지, 섬유, 수처리 등 이 화학약품이 폭넓은 산업 분야에서 이용되고 있기 때문입니다. 이미 생산량의 85%를 차지하고 있는 멤브레인 전지 기술은 기존의 수은 전지에 비해 전력 사용량을 약 30% 삭감하고 수은의 배출을 없앨 수 있기 때문에 확대되고 있습니다. 톤수의 64%를 차지하는 아시아의 우위는 경쟁력 있는 전력요금, 급속한 정유공사 건설, 적극적인 비스코스 섬유투자에 있습니다. 액체 등급은 출하량의 65%를 차지하며 파이프라인 운송 및 대량 보관에 유리합니다. 가격 스프레드는 지역 에너지 비용을 점점 더 추구하고 있으며, 생산자는 저탄소 전력 계약을 체결하고 가스가 풍부한 해안선 근처에 새로운 플랜트를 설치하도록 촉구하고 있습니다. 중국, 인도, 미국에서 발표된 생산 능력 증강은 에너지 안보, 탄소 정책, 국소 수요 클러스터 간의 신중한 균형을 강조하고 적당히 단편화된 가성소다 시장을 유지하고 있습니다.

세계 가성소다 시장 동향과 통찰

아시아의 알루미나 정련소 확장 가속

바이에르 제법으로 추출되는 알루미나 1톤당 2-3톤이 용해되기 때문에 정제능력 증가가 가성소다 인취량을 끌어올리고 있으며, 2024년에는 중국의 알루미늄 제조업체만으로 수천만 톤이 소비됩니다. 인도네시아와 인도의 새로운 제련 콤플렉스는 가격 상승을 헤지하기 위해 장기 공급을 계약하고 있으며 알루미늄 생산 비용은 전 분기 대비 6% 가까이 변동될 수 있습니다. 공장 경영자는 또한 레드 머드의 폐기량을 줄이기 위해 고순도 등급을 조달하고 있으며, 이는 저염 가성소다의 가격 프리미어로 이어집니다. 현재 일부 정유소 소유자는 후방 통합을 고려하고 있으며 업스트림 라이선스와 전력 액세스 간의 경쟁이 심화되고 있습니다. 100만 톤의 알루미나를 추가할 때마다 약 250만 톤의 가성소다가 필요하기 때문에 2025년부터 2027년으로 예정된 그린필드 프로젝트가 가성소다 시장의 구조적인 수요 증가를 지원하고 있습니다.

비누 및 세제 수요 증가

신흥국의 위생 주도의 도시화는 가성소다가 비누화 반응의 알칼리 골격을 형성하는 비누 및 세제의 통로를 넓히고 있습니다. 인도네시아, 나이지리아, 베트남의 계면활성제 제조업체로의 출하량은 2024년 2자리 증가했으며 프리미엄 식품용 가성소다는 현재 표준 50wt% 용액보다 12%의 가격 상승을 확보하고 있습니다. 스페셜리티 포뮬레이터는 투명 비누의 변색을 억제하는 초저철분과 니켈 사양을 요구하고 있어, 제조업체에게 식염수 정제 스키드에 대한 투자를 촉구하고 있습니다. 항균액에서 직물 전용 분말까지 폭넓은 제품 믹스가 가성소다 시장의 다양성을 유지하여 중공업의 주기적 불황을 완화하고 있습니다.

유럽의 불안정한 전력 가격

전기요금은 멤브레인 전해의 현금비용 중 50%를 차지하지만, 유럽의 전일비 가격은 2025년 초에 90유로/MWh를 넘어 Euro Chlor의 마진을 침식했습니다. 생산자는 EU 배출권 거래 체계 하에서 간접적인 CO2 수수료에 직면하고 있으며 러시아와 사우디 수출업체와의 비용 격차가 톤당 최대 120달러까지 확대되고 있습니다. 현재 논의되고 있는 보상안은 이러한 비용의 일부를 환불할 수 있지만 정책의 불확실성은 유럽의 신규 생산 능력에 대한 투자를 억제하고 있습니다. 그 결과, 북서유럽으로의 스폿 수입은 2024년에 전년 대비 19% 증가해, 이 지역의 가성소다 시장을 압박했습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 인도의 비스코스 단섬유 생산량의 급증

- 중동 및 아프리카의 탈염 능력 증강

- 에너지 집약적인 생산 공정

부문 분석

염화나트륨의 이점은 수은 기술의 규제 금지(특히 EU의 2017년 최종 단계적 폐지 기한)와 레거시 셀에 비해 30% 절전할 수 있다는 이점에 기인합니다. 또한 염화나트륨의 오염을 100ppm 이하로 억제할 수 있기 때문에 반도체 제조용 고순도 등급이 가능합니다. 중국, 미국, 독일 제조업체는 전류 밀도를 7kA m-2로 올려 기존 멤브레인 라인을 디보틀 넥킹하여 새로운 염수 회로 없이 톤수를 늘리고 있습니다. 병행하여 일본에도 투자의 물결이 밀려오고 있으며, Asahi Kasei는 2024년 국내 염소 알칼리 개수를 위해 멤브레인 스택 생산량을 확대하기 위한 정부의 백업을 확보했습니다. 가성소다 시장의 나머지는 격막과 잔류 수은의 생산 능력입니다.

액체 가성소다는 보통 50wt%로 발송되며 2024년 출하량의 65%를 차지하고, 고형 가성소다는 CAGR 4.87%로 증가할 것으로 예측됩니다. 염소알칼리 공장에서 300-500km 이내에 위치한 고객에게는 파이프라인의 연결성과 벌크 트럭에 의한 핸들링에 의해 액체가 디폴트가 되어 운임은 톤당 30달러 미만으로 억제되고 있습니다. 액체 수요는 펄프 및 제지 공장, 석유 정련소 및 수도 사업체 사이에서 특히 견조하며, 연속 주입 시스템은 표준 50wt% 원료에 의존하고 있습니다. 플레이크, 비드, 연탄 모양의 고체는 장거리 운송, 순도가 중요한 운송 또는 작은 배치 요구에 해당합니다. 고형 원료는 소량이지만, 제수, 프리링, 더스트 억제의 공정이 있기 때문에 1톤당 120미국의 프리미엄이 붙습니다. Hydrite의 2025년 출시된 밀폐 드럼 비드 포장은 흡습성 수분 픽업을 차단하고 최종 사용자의 안전 요구에 직접 대응합니다. 고체는 주로 전자 제품, 의약품 및 섬유 염색으로 자라며 생산자에게 상품성 가성소다 시장에서 마진을 올리는 방법을 제공합니다.

지역별 분석

아시아태평양이 2024년 출하량의 64%를 차지해 선두를 굳혔습니다. 중국의 염소 알칼리 공장은 유럽의 인수가 연화되어 수출이 감소했다고는 해도, 4,100만 톤 가까운 생산량을 기록했습니다. 국내 소비는 알루미늄과 PVC의 확대로 호조를 유지했습니다. 인도의 가성소다 시장은 Atul Products사가 2024년 동안 Valsad에 300TPD 시설을 가동시킴에 따라 기세를 늘렸습니다. 동남아시아의 생산자들은 비누, 바이오디젤, 전지 전구체의 지역 수요로부터 혜택을 받아 해상 운임의 익스포저를 줄이는 국경을 넘는 파이프라인 프로젝트의 발판을 구축했습니다.

북미는 점유율이 작고 셰일가스 유래 천연가스를 활용하여 세계 최저 수준의 전해전력비용을 누리고 가성소다와 염소유도체의 경쟁력 있는 수출을 촉진합니다. OxyChem은 2024년 텍사스 주에서 678kt의 냉동 등급 라인을 재가동시켜 국내 공급의 탄력성을 강화합니다. 이 지역의 포워드 파이프라인에는 PCC 그룹이 Chemours의 데리슬 공장에서 계획하고 있는 340kt의 염소 알칼리 장치가 포함되어 2028년에 시운전이 예정되어 있습니다. 이러한 브라운필드 통합은 성숙하지만 기술적으로 첨단 가성소다 시장에 상용 가성소다를 추가하는 한편 염소 아울렛을 고정화합니다.

유럽은 높은 불안정한 에너지 가격 하에서 고투하고 있습니다. 76개의 제조 거점이 있음에도 불구하고, 스팟 전력의 상승이 지역의 현금 비용을 러시아와 사우디아라비아를 훨씬 웃도는 수준으로 밀어 올렸고, 가동률은 떨어졌습니다. 정책 입안자는 현재 탄소 누출을 피하고 염소 알칼리 체인에서 35,000명의 직접 고용을 보호하기 위한 간접 비용 보상을 논의했습니다. 그럼에도 불구하고 유럽 생산자들은 전자, 의약품, 식품 가공 등의 분야에서 동대륙의 엄격한 품질 프로토콜을 고집하는 고객과의 거래를 계속하고 있으며, 폭넓은 비용 압력에도 불구하고 틈새 가치를 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아에서 알루미나 정련소 확장의 가속에 의한 가성소다 수요 증가

- 비누 및 세제 수요 증가

- 인도의 비스코스 단섬유 생산량 급증

- 중동 및 아프리카에서 해수 담수화 능력의 증강

- EU가 의무화하는 멤브레인 셀로의 전환이 업그레이드 프로젝트를 촉진

- 시장 성장 억제요인

- 유럽의 불안정한 전력 가격

- 에너지 집약적인 생산 공정

- 다양한 최종 사용자 산업에서의 대체품의 이용 가능성

- 밸류체인 분석

- 기술적 전망

- 가격 개관

- 무역 개요

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측(수량)

- 제조 공정별

- 멤브레인 셀

- 격막 셀

- 기타 프로세스

- 형상별

- 액체

- 고체

- 농도 등급별

- 32wt%

- 50wt%

- 73wt% 이상

- 용도별

- 펄프 및 종이

- 유기화학제품

- 무기화학제품

- 비누 및 세제

- 알루미나

- 수처리

- 섬유(비스코스 섬유, 염색)

- 기타(식품 및 의약품 가공, 광업 및 야금)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 북유럽

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일 {}(영어)

- AGC Inc.

- Atul Ltd

- BorsodChem(Wanhua Chemical Group)

- Covestro AG

- DCW Ltd.

- Dow

- Formosa Plastics Corporation

- GHCL Limited

- Grasim Industries Limited

- Gujarat Alkalies and Chemicals Limited

- Hanwha Solutions Corp.

- INEOS

- Nouryon

- Occidental Petroleum Corporation

- Olin Corporation

- SABIC

- Shin-Etsu Chemical Co. Ltd

- Tata Chemicals Ltd.

- Tosoh Corporation

- Westlake Corporation

- Xinjiang Zhongtai Chemical Co. Ltd.

제7장 시장 기회와 전망

- 나트륨 이온 전지 분야 수요 증가

- 에너지 효율이 높은 생산 공정에 대한 수요 증가

- 화이트 스페이스와 미충족 요구 평가

The membrane cell segment generated the bulk of 2024 output, commanding 85% of the caustic soda market share, and the diaphragm cell is expanding at a 5.12% CAGR to 2030.

Global demand for caustic soda totals 94.95 million tons in 2025 and is forecast to climb to 116.30 million tons by 2030, reflecting a 4.14% CAGR over 2025-2030. Robust growth springs from the chemical's wide industrial reach, with alumina refining, organic chemical synthesis, pulp and paper, textiles, and water treatment each deepening their consumption. Membrane cell technology, already responsible for 85% of output, is expanding because it cuts electricity use by roughly 30% relative to legacy mercury cells and eliminates mercury emissions. Asia's dominance, at 64% of tonnage, rests on competitive power tariffs, rapid refinery build-outs, and aggressive viscose fiber investments. Liquid grades command 65% of deliveries, favored for pipeline transfer and bulk storage. Pricing spreads increasingly track regional energy costs, prompting producers to lock in low-carbon electricity contracts and locate new plants near gas-rich coastlines. Capacity additions announced in China, India, and the United States underscore a careful balance between energy security, carbon policy, and localized demand clusters, sustaining a moderately fragmented caustic soda market.

Global Caustic Soda Market Trends and Insights

Accelerated Alumina Refinery Expansions in Asia

Rising refinery capacity is lifting caustic soda offtake because 2-3 tons are dissolved for every ton of alumina extracted in the Bayer process, and Chinese aluminum producers alone consumed tens of millions of tons in 2024. New smelter complexes in Indonesia and India are contracting long-term supply to hedge price spikes, which can swing aluminum production costs by nearly 6% quarter-on-quarter. Plant operators also source higher-purity grades to reduce red-mud disposal volumes, translating into price premia for low-salt caustic soda. Several refinery owners now consider backward integration, sharpening competition for upstream licenses and power access. With each 1 million-ton alumina addition requiring roughly 2.5 million tons of caustic soda, green-field projects scheduled for 2025-2027 underpin structural demand growth for the caustic soda market.

Increasing Demand for Soap and Detergent

Hygiene-led urbanization across emerging economies is widening the soap and detergent aisle, where caustic soda forms the alkali backbone of saponification reactions. Volumes shipped to surfactant makers in Indonesia, Nigeria, and Vietnam rose in double digits in 2024, and premium food-grade caustic soda now secures a 12% pricing uplift over standard 50 wt% solutions. Specialty formulators request ultra-low iron and nickel specifications that cut discoloration in transparent soaps, nudging producers to invest in brine purification skids. The widening product mix-from anti-bacterial liquids to fabric-specific powders-keeps the caustic soda market diversified, cushioning cyclical downturns in heavy industry.

Volatile Electricity Prices in Europe

Electricity can represent 50% of cash costs for membrane electrolysis, and European day-ahead prices surged above EUR 90/MWh in early 2025, eroding margins Euro Chlor. Producers face indirect CO2 charges under the EU Emissions Trading Scheme, widening cost gaps versus Russian or Saudi exporters by up to USD 120 per ton. Compensation proposals under discussion could reimburse a share of these expenses, yet policy uncertainty curtails investment in new European capacity. Consequently, spot imports into north-west Europe rose 19% year-on-year in 2024, pressuring the regional caustic soda market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Viscose Staple Fiber Output in India

- Desalination Capacity Additions in the Middle East and Africa

- Energy-Intensive Production Process

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Its dominance stems from regulatory bans on mercury technology, notably the EU's final 2017 phase-out deadline, and from a 30% electricity-savings advantage relative to legacy cells. In addition, sodium chloride contamination can be held below 100 ppm, enabling high-purity grades for semiconductor production. Producers in China, the United States, and Germany are debottlenecking existing membrane lines by raising current density to 7 kA m-2, adding incremental tonnage without new brine circuits. A parallel investment wave is visible in Japan, where Asahi Kasei secured government backing in 2024 to expand membrane stack output for domestic chlor-alkali retrofits. Diaphragm and residual mercury capacity accounts for the balance of the caustic soda market.

Liquid caustic soda, typically shipped at 50 wt%, covered 65% of deliveries in 2024 while solid form is projected to rise at a 4.87% CAGR. Pipeline connectivity and bulk-truck handling make liquids the default for customers located within 300-500 km of a chlor-alkali plant, limiting freight costs to under USD 30 per ton. Liquid demand is particularly resilient among pulp and paper mills, oil refineries, and water utilities, where continuous dosing systems rely on standard 50 wt% feedstock. Solid forms-flakes, beads, and briquettes-meet long-haul, purity-critical, or small-batch needs. Although representing a smaller volume, solids fetch up to USD 120 per ton premiums owing to de-watering, prilling, and dust-suppression steps. Hydrite's 2025 launch of sealed-drum bead packaging cuts hygroscopic moisture pick-up and directly addresses end-user safety demands. Solid volumes grow mainly in electronics, pharmaceuticals, and textile dyeing, giving producers an avenue to lift margin in an otherwise commodity-like caustic soda market.

The Caustic Soda Market Report Segments the Industry by Production Process (Membrane Cell, Diaphragm Cell, and Other Processes), Form (Liquid and Solid), Concentration Grade (32 Wt%, 50 Wt%, and 73 Wt% and Higher), Applications (Pulp and Paper, Organic Chemicals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific cemented its leadership with 64% of 2024 shipments. Chinese chlor-alkali plants recorded output near 41 million tons, even as exports dipped on softer European draws. Domestic consumption stayed buoyant thanks to aluminum and PVC expansions. India's caustic soda market gained momentum when Atul Products commissioned a 300 TPD facility in Valsad during 2024, complemented by captive 50 MW power that buffers electricity risk. Southeast Asian producers benefit from regional demand for soap, biodiesel, and battery precursors, building a springboard for cross-border pipeline projects that cut maritime freight exposure.

North America, holding a significant albeit smaller share, leverages shale-derived natural gas to enjoy one of the world's lowest electrolysis power costs, fostering competitive exports of both caustic soda and chlorine derivatives. OxyChem's 2024 restart of its 678 kt refrigeration-grade line in Texas bolsters domestic supply resilience. The region's forward pipeline includes PCC Group's planned 340 kt chlor-alkali unit at Chemours' DeLisle site, scheduled for commissioning in 2028. Such brownfield integrations anchor captive chlorine outlets while adding merchant caustic to a mature but technologically advanced caustic soda market.

Europe struggles under high and volatile energy prices. Despite hosting 76 manufacturing sites, capacity utilization dipped as spot electricity spikes pushed regional cash costs well above those in Russia or Saudi Arabia. Policymakers now debate indirect-cost compensation to avert carbon leakage and protect 35,000 direct jobs in the chlor-alkali chain. Nonetheless, European producers continue to court customers in electronics, pharmaceuticals, and food processing who insist on the continent's stringent quality protocols, preserving niche value despite broad cost pressures.

- AGC Inc.

- Atul Ltd

- BorsodChem (Wanhua Chemical Group)

- Covestro AG

- DCW Ltd.

- Dow

- Formosa Plastics Corporation

- GHCL Limited

- Grasim Industries Limited

- Gujarat Alkalies and Chemicals Limited

- Hanwha Solutions Corp.

- INEOS

- Nouryon

- Occidental Petroleum Corporation

- Olin Corporation

- SABIC

- Shin-Etsu Chemical Co. Ltd.

- Tata Chemicals Ltd.

- Tosoh Corporation

- Westlake Corporation

- Xinjiang Zhongtai Chemical Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated alumina refinery expansions in Asia boosting caustic demand

- 4.2.2 Increasing Demand for Soap and Detergent

- 4.2.3 Surge in viscose staple fiber output in India

- 4.2.4 Desalination capacity additions in the Middle East and Africa

- 4.2.5 EU-mandated switch to membrane cells driving upgrade projects

- 4.3 Market Restraints

- 4.3.1 Volatile electricity prices in Europe

- 4.3.2 Energy-intensive Production Process

- 4.3.3 Availability of substitutes in Various End User Industries

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Price Overview

- 4.7 Trade Overview

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 Market Size and Growth Forecasts ( Volume)

- 5.1 By Production Process

- 5.1.1 Membrane Cell

- 5.1.2 Diaphragm Cell

- 5.1.3 Other Processes

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.3 By Concentration Grade

- 5.3.1 32 wt%

- 5.3.2 50 wt%

- 5.3.3 73 wt% and Higher

- 5.4 By Application

- 5.4.1 Pulp and Paper

- 5.4.2 Organic Chemicals

- 5.4.3 Inorganic Chemicals

- 5.4.4 Soap and Detergent

- 5.4.5 Alumina

- 5.4.6 Water Treatment

- 5.4.7 Textile (Viscose Fibre, Dyeing)

- 5.4.8 Others (Food and Pharmaceutical Processing, Mining and metallurgy)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Nordics

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 AGC Inc.

- 6.4.2 Atul Ltd

- 6.4.3 BorsodChem (Wanhua Chemical Group)

- 6.4.4 Covestro AG

- 6.4.5 DCW Ltd.

- 6.4.6 Dow

- 6.4.7 Formosa Plastics Corporation

- 6.4.8 GHCL Limited

- 6.4.9 Grasim Industries Limited

- 6.4.10 Gujarat Alkalies and Chemicals Limited

- 6.4.11 Hanwha Solutions Corp.

- 6.4.12 INEOS

- 6.4.13 Nouryon

- 6.4.14 Occidental Petroleum Corporation

- 6.4.15 Olin Corporation

- 6.4.16 SABIC

- 6.4.17 Shin-Etsu Chemical Co. Ltd.

- 6.4.18 Tata Chemicals Ltd.

- 6.4.19 Tosoh Corporation

- 6.4.20 Westlake Corporation

- 6.4.21 Xinjiang Zhongtai Chemical Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 Rising Demand for Sodium-Ion Batteries Sector

- 7.2 Increasing Demand for Energy-efficient Production Processes

- 7.3 White-space and Unmet-need Assessment