|

시장보고서

상품코드

1906128

유럽의 가성소다 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Europe Caustic Soda - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

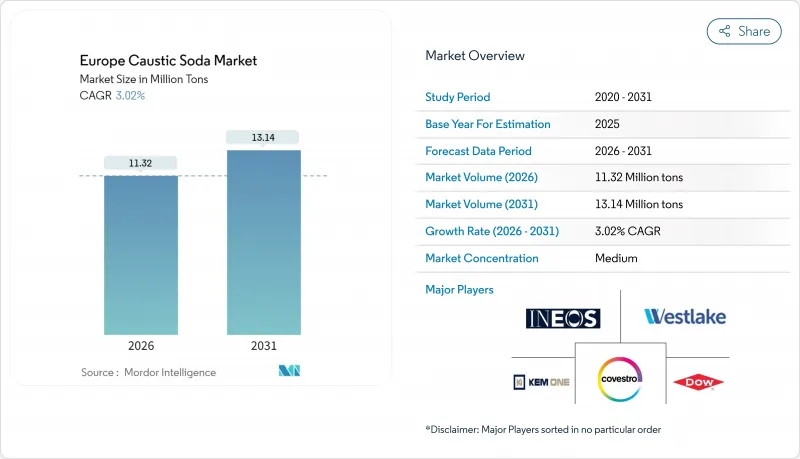

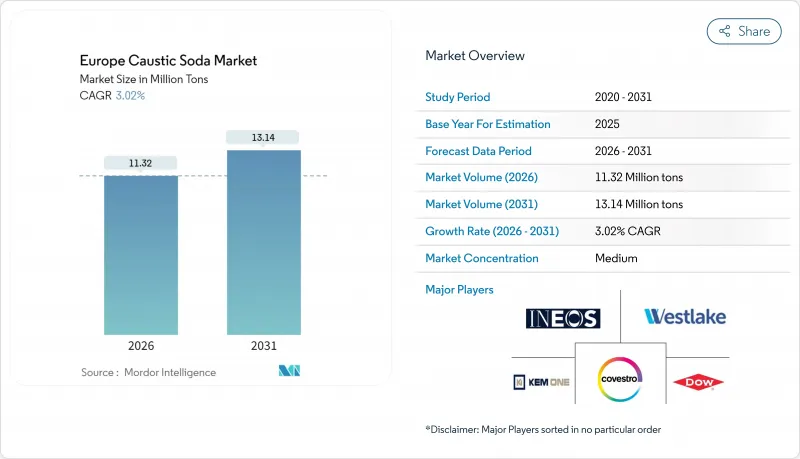

유럽의 가성소다 시장은 2025년 1,099만 톤으로 평가되었으며, 2026년 1,132만 톤에서 2031년까지 1,314만 톤에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 3.02%로 예상됩니다.

이 꾸준한 확대는 에너지 효율적인 기술과 규제면에서의 뒷받침이 전력 가격의 상승 등 성장 제약 요인을 웃도는 성숙 단계를 보여줍니다. 가성소다가 EU 중요화학물질법안에서 중요화학물질로 분류된 것은 지역의 산업자율성을 지키는 데 있어서의 전략적 역할을 강조하고 있습니다. 막전극 기술은 스팟 가격이 275유로/MWh라는 스트레스 테스트 수준까지 급등한 상황에서 전력 소비를 줄이기 위해 경쟁 환경에서 우위를 유지하고 있습니다. 다운스트림 통합은 액체 형태를 지속적으로 지지하는 한편, 폐수 처리, 전지용 알루미나 정제, 섬유계 포장재에 대한 지속적인 투자가 경기 순환의 침체기에 있어서도 수요의 회복력을 유지하고 있습니다. 동시에 저비용 아시아 수출국으로부터의 수입재정거래와 변동하는 에너지 비용이 이익률을 압박하여 기존 생산자 간 포트폴리오 합리화를 가속화하고 있습니다.

유럽의 가성소다 시장의 동향 및 분석

수처리 용도 수요 증가

새로운 도시 폐수 규제에 의해 EU 지역 내 전역에서 3차 및 4차 처리가 의무화되어, pH 제어나 인 제거를 위한 가성소다 투여량이 급증하고 있습니다. 스페인과 독일에서는 플랜트 업그레이드가 확대되고 있으며, 지자체는 2045년까지 에너지 중립 목표를 달성할 필요가 있기 때문에 시설이 재생에너지로 이행하는 가운데 기준 소비량이 보장됩니다. 미량 오염물질 제거 기준의 강화에 의해 고도의 산화 처리나 침전 처리에서의 가성소다의 사용 범위가 한층 더 확대되고 있습니다. 지자체의 설비 업그레이드는 수십억 유로 규모의 프로젝트이기 때문에 유럽의 가성소다 시장은 광범위한 산업 둔화의 영향을 받지 않는 안정적인 장기 수요를 누리고 있습니다. 업계 데이터에 따르면 염소 알칼리 공정은 염소 1톤당 약 2,600kWh를 소비하므로 가성소다 공급은 에너지 효율 투자와 직접적으로 연결됩니다.

EV 배터리 공급망에서 알루미나 수요 증가

유럽의 기가팩토리 주변에 집적하는 전지용 알루미나 정제소에서는 종래품에 비해 고순도 및 고소비량의 가성소다가 요구됩니다. 독일의 자동차산업 거점이 이 수요를 견인하는 한편, 프랑스와 벨기에의 거점은 지역 원료 확보를 서두르고 있습니다. 노스볼트사의 2024년 도산이 시장 심리를 위축시켰지만 차량의 전동화는 여전히 구조적인 성장 엔진입니다. 이 부문은 전 세계의 가성소다 소비량의 21%를 차지하고 있으며, 현재는 에너지 비용을 상쇄하는 프리미엄 가격의 혜택을 받아 장기적인 수요 기반을 강화하고 있습니다.

유럽의 높은 에너지 비용

염소 알칼리 제조에 드는 현금 비용의 절반 이상을 전력이 차지하기 때문에, 러시아 및 우크라이나 분쟁에 따른 가격 변동에 의해 전력 가격이 275유로/MWh에 육박했을 때 지역의 가동률이 급락했습니다. BASF는 국내 화학제품 생산량의 25%를 손실하면서 연간 8,000톤의 수소를 생산하고 7만 2,000톤의 배출 감축이 전망되는 54MW의 그린 수소 전해 장치를 도입하기로 결정했습니다. 재생가능에너지의 추가 도입으로 전력망이 안정될 때까지 생산자는 급등한 전력요금을 흡수할 수밖에 없으며, 이는 이익률의 압축이나 선택적인 가동 정지로 이어지고 있습니다.

부문 분석

2025년 시점에서 막 전해 셀 방식은 유럽의 가성소다 시장 점유율의 77.48%를 차지하고 있습니다. 이는 우수한 에너지 효율과 규제 적합성의 이점을 반영한 결과입니다. 전력 비용 급등을 받아 제조업체 각사는 격막식에서 막식으로의 전환을 가속하고 있습니다. 이 전환으로 막 전해 방식의 설비 증강은 2031년까지 연평균 복합 성장률(CAGR) 3.14%로 확대될 것으로 전망됩니다. 신흥 전기 투석 기술은 단위 전력 소비의 추가적인 감소를 보장하고 막 기술의 장기적인 우위를 강화하고 있습니다. 환경법령에 근거한 수은셀의 단계적 폐지가 의무화되고 있는 가운데, 유럽의 가성소다 시장에서의 막 부문의 규모는 꾸준히 확대될 것으로 예측됩니다. 게다가 유럽의 엔지니어링 기업이 공급하는 사우디아라비아 프로젝트는 이 지역 기술 공급자에게 세계 시장으로의 수출 기회를 보여주고 있으며, 혁신과 도입의 선순환을 지속하고 있습니다.

올린사 등의 사업자가 에너지강도 기준을 충족할 수 없는 구식 라인을 폐쇄하는 가운데, 종래의 격막식 설비는 축소 추세에 있습니다. 보수 활동은 자본 집약적이지만 대출 기관이 신용 비용을 배출 실적과 연동시키는 경우가 증가하고 있기 때문에 자금 조달은 여전히 가능성이 있습니다. 이로 인해 막 업그레이드의 투자 회수가 정량화되기 쉬워집니다. 한때 일반적이었던 수은 셀은 일부 고립된 통합 시설에만 남아 있으며 EU 지침에 따라 2027년까지 완전히 폐지될 전망입니다. 전반적으로 생산 과정의 상황은 유럽의 가성소다 시장에 점진적인 효율성 향상 기회를 제공하고 전력 가격 상승의 역풍을 부분적으로 상쇄할 전망입니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 수처리 용도에서의 수요 증가

- EV 배터리 공급망에서의 알루미나 수요 증가

- 섬유 소재 포장의 성장

- 비누 및 세제 제조 거점의 확대

- 화학 합성 수요 증가

- 억제요인

- 유럽의 높은 에너지 비용

- 노동안전보건 및 REACH 규제 대응 비용

- 수입재정거래에 의한 유럽연합의 이익률 축소

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 무역 분석

- 가격 동향

- 생산 분석

제5장 시장 규모 및 성장 예측(금액 및 수량)

- 제조 공정별

- 멤브레인 셀

- 다이어프램 셀

- 기타 제조 공정(구식 수은 전지, 신흥 전기 투석 및 직접 전기 합성)

- 형태별

- 고체

- 액체

- 용도별

- 펄프 및 제지

- 유기화학제품

- 무기화학제품

- 비누 및 세제

- 알루미나

- 수처리

- 기타 용도(식품 및 사료 가공 등)

- 지역별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- BASF

- Covestro

- Dow

- Ercros

- INEOS

- Kem One

- Nouryon

- Olin Corporation

- PCC SE

- Spolchemie

- Vynova Group

- Westlake Corporation

- WeylChem International GmbH

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Europe Caustic Soda Market was valued at 10.99 Million tons in 2025 and estimated to grow from 11.32 Million tons in 2026 to reach 13.14 Million tons by 2031, at a CAGR of 3.02% during the forecast period (2026-2031).

This steady expansion signals a mature phase in which energy-efficient technologies and regulatory tailwinds outweigh growth constraints such as elevated power prices. Caustic soda's classification as a critical chemical under the proposed EU Critical Chemicals Act underscores its strategic role in safeguarding regional industrial autonomy. Membrane cell technology dominates the competitive arena because it cuts electricity consumption at a time when spot prices have spiked to stress-test levels of EUR 275/MWh. Downstream integration continues to favor the liquid form, while sustained investments in wastewater treatment, battery-grade alumina refining and fiber-based packaging keep demand resilient across cyclical downturns. At the same time, import arbitrage from low-cost Asian exporters and volatile energy costs create margin pressure that accelerates portfolio rationalization among incumbent producers.

Europe Caustic Soda Market Trends and Insights

Increasing Demand from Water Treatment Application

New urban-wastewater rules require tertiary and quaternary treatment across the bloc, triggering a surge in caustic-soda dosing for pH control and phosphorus removal. Spain and Germany are scaling plant upgrades, and municipalities must comply with an energy-neutral target by 2045, guaranteeing baseline consumption even as facilities pivot to renewable power. Micropollutant removal standards further broaden caustic-soda usage in advanced oxidation and precipitation. Because municipal upgrades are multi-billion-euro projects, the European caustic soda market enjoys stable long-cycle demand insulated from broader industrial slowdowns. Industry data show chlor-alkali processes consume roughly 2,600 kWh per ton of chlorine, linking caustic-soda supply directly to energy-efficiency investments.

Rising Alumina Demand from EV-Battery Supply Chain

Battery-grade alumina refineries that cluster near European gigafactories require higher caustic-soda purity and volumes per output ton than legacy grades. German automotive hubs anchor this pull, while French and Belgian sites race to secure regional feedstock. Although Northvolt's 2024 bankruptcy dented sentiment, vehicle electrification remains a structural growth engine. The sector historically consumes 21% of global caustic soda and now benefits from premium pricing that offsets energy costs, strengthening the long-run demand case.

High Energy Costs in Europe

Electricity accounts for over half of chlor-alkali cash costs, so volatility tied to the Russia-Ukraine conflict slashed regional operating rates when prices neared EUR 275/MWh. BASF lost 25% domestic chemical output, prompting a 54 MW green-hydrogen electrolyzer that should yield 8,000 t of H2 annually and curb 72,000 t of emissions. Producers must absorb higher power tariffs until renewable additions stabilize the grid, translating into margin compression and selective shutdowns.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Fiber-Based Packaging

- Expansion of Soap and Detergent Manufacturing Hubs

- Import Arbitrage Squeezing EU Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The membrane cell route commands 77.48% of the European caustic soda market share in 2025, reflecting its superior energy profile and regulatory compliance advantages. Producers accelerated diaphragm-to-membrane conversions as electricity costs soared, a shift that lifted membrane capacity additions to 3.14% CAGR through 2031. Emerging electro-electrodialysis technologies promise further cuts in specific power consumption, reinforcing the long-term dominance of membranes. The European caustic soda market size for membrane-based output is forecast to widen steadily because legacy mercury cells face mandatory phase-outs under environmental statutes. In parallel, Saudi projects supplied by European engineering firms signal global export opportunities for the region's technology providers, sustaining a virtuous cycle of innovation and deployment.

Traditional diaphragm assets are shrinking as operators such as Olin shutter older lines that cannot meet energy-intensity benchmarks. Retrofit activity is capital-heavy, yet financing remains accessible because lenders increasingly link credit costs to emissions performance, giving membrane upgrades a quantifiable payback. Mercury cells, once common, linger only in isolated integrated complexes and will exit entirely before 2027 under EU directives. Overall, the production-process landscape positions the European caustic soda market for incremental efficiency gains that partly offset power-price headwinds.

The Caustic Soda Europe Market Report Segments the Industry by Production Process (Membrane Cell, Diaphragm Cell, Other Production Processes), Form (Solid, Liquid), Application (Pulp and Paper, Organic Chemical, Inorganic Chemical, Soap and Detergent, Alumina, Water Treatment, Other Applications), and Geography (Germany, United Kingdom, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (tons).

List of Companies Covered in this Report:

- BASF

- Covestro

- Dow

- Ercros

- INEOS

- Kem One

- Nouryon

- Olin Corporation

- PCC SE

- Spolchemie

- Vynova Group

- Westlake Corporation

- WeylChem International GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand from Water Treatment Application

- 4.2.2 Rising Alumina Demand from EV-Battery Supply Chain

- 4.2.3 Growth of Fiber-Based Packaging

- 4.2.4 Expansion of Soap and Detergent Manufacturing Hubs

- 4.2.5 Growing Requirement for Chemical Synthesis

- 4.3 Market Restraints

- 4.3.1 High Energy Costs in Europe

- 4.3.2 Occupational-Safety and REACH Compliance Costs

- 4.3.3 Import Arbitrage squeezing European Union's margins

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Trade Analysis

- 4.9 Price Trends

- 4.10 Production Analysis

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Production Process

- 5.1.1 Membrane Cell

- 5.1.2 Diaphragm Cell

- 5.1.3 Other Production Processes (Mercury Cell (legacy), Emerging Electro-electrodialysis and Direct Electro-synthesis)

- 5.2 By Form

- 5.2.1 Solid

- 5.2.2 Liquid

- 5.3 By Application

- 5.3.1 Pulp and Paper

- 5.3.2 Organic Chemicals

- 5.3.3 Inorganic Chemicals

- 5.3.4 Soap and Detergents

- 5.3.5 Alumina

- 5.3.6 Water Treatment

- 5.3.7 Other Applications (Food and Feed Processing, etc.)

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Russia

- 5.4.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Covestro

- 6.4.3 Dow

- 6.4.4 Ercros

- 6.4.5 INEOS

- 6.4.6 Kem One

- 6.4.7 Nouryon

- 6.4.8 Olin Corporation

- 6.4.9 PCC SE

- 6.4.10 Spolchemie

- 6.4.11 Vynova Group

- 6.4.12 Westlake Corporation

- 6.4.13 WeylChem International GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment