|

시장보고서

상품코드

1836521

유럽의 자동차 에어필터 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Automotive Airfilters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

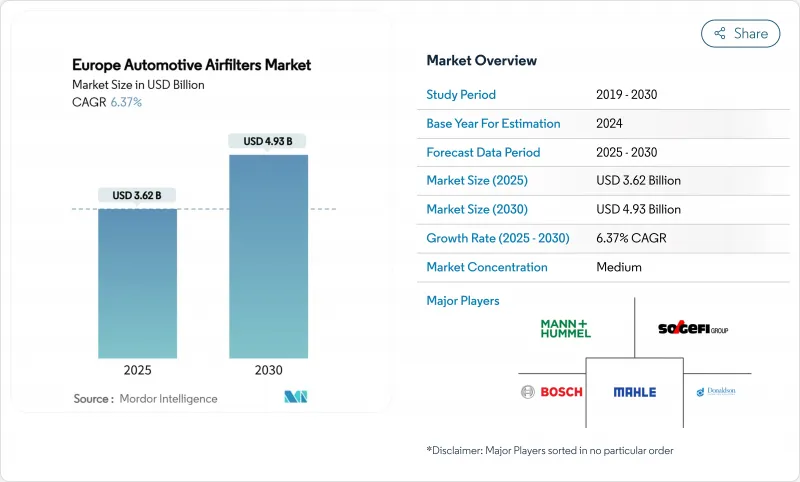

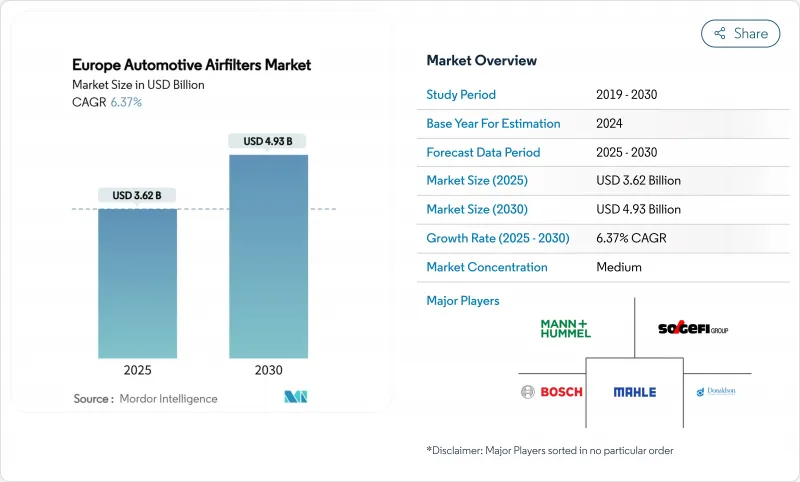

유럽의 자동차 에어필터 시장 규모는 2025년 36억 2,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR은 6.37%로 확대되어, 2030년에는 49억 3,000만 달러에 달할 것으로 예측됩니다.

Euro 7을 둘러싼 강력한 규제 기세, 도시 수준의 저배출 가스 지역의 급속한 확대, 소비자의 뿌리 깊은 건강 의식이 이 확대를 지원하고 있습니다. 상대방 상표 제품 제조업체(OEM)는 나노미터 단위의 미립자 규제를 충족하기 위해 흡기구와 차실 내의 필터 설계를 재검토하고 있으며, 독립형 애프터마켓 기업은 유럽 대륙의 노후화된 약 2억 8,000만대의 자동차 대수를 활용하고 있습니다. 따라서 유럽의 자동차 에어필터 시장은 상품 수량에서 부가가치 성능으로 전환하고 있으며, 여과를 컴플라이언스상 중요하고, 소비자의 눈에 닿기 쉽고, 텔레메트리가 가능한 차세대 이동성의 컴포넌트로 자리매김하고 있습니다.

유럽 자동차 에어필터 시장 동향과 통찰

고령화하는 자동차 시장, 독립형 애프터마켓 수요 증가

서유럽의 평균 차령은 2025년 12년에 이르고, 동유럽은 15-20년에 이릅니다. 낡은 내연 엔진(ICE) 모델은 흡기 필터와 캐빈 필터의 빈번한 교환을 필요로 하고, 독립 정비 공장은 경쟁력 있는 가격과 폭넓은 SKU 커버리지를 제공함으로써, 지역의 애프터마켓에서 상당한 점유율을 획득하고 있습니다. BEV의 보급으로 미래의 흡기 필터 수요가 없어져도 ICE의 잔존 차종이 장기간의 사용량을 보증하고 있기 때문에 유럽의 자동차 에어필터 시장은 적어도 1회는 전체 교환 사이클을 통해 견조를 유지합니다. 전자상거래 전문가는 레거시 플랫폼을 위한 SKU 구색을 늘리고, 프라이빗 브랜드의 활성탄 캐빈 엘리먼트를 도입하고, 전자상거래 마켓플레이스를 채용해 분산된 지방의 오너에 접근함으로써 대응하고 있습니다.

필터 교환 사이클을 가속화하는 Euro 7 및 Euro VI-D 배출 가스 규정

유럽 위원회는 2024년 5월에 Euro 7 규칙을 발표했으며, 가솔린 차량에 10나노미터의 미립자 기준치를 도입했으며, 테일파이프와 비배기 미립자 모두에 대해 평생 컴플라이언스를 도입했습니다. 차량 탑재 진단이 필터의 열화를 모니터하게 되었기 때문에 흡기 엘리먼트와 캐빈 엘리먼트는 기존보다 훨씬 길고 효율을 유지할 필요가 있어, 주행 거리가 많은 차량에서는 실제의 교환 사이클을 가능한 한 짧게 할 필요가 있습니다. 따라서 OEM 등급 공급업체는 규제 증명서와 RFID 태그를 통합한 이익률이 높은 다층 요소를 번들하여 단위당 매출을 늘리고 유럽 자동차 에어필터 시장을 재량적인 유지보수 부품이 아닌 중요한 컴플라이언스 레버로 강화하고 있습니다.

BEV의 보급으로 흡기 엔진용 에어필터 수요가 축소

배터리 전기자동차는 연소용 에어필터가 필요하지 않으므로 흡기 필터의 전체 재료비가 신차 수요에서 사라집니다. 독일에서는 2024년에 135만대의 EV가 조립되었으며, 플릿 평균 CO2 규제 하에서 2025년에는 167만대를 목표로 하고 있습니다. 따라서 유럽의 자동차 에어필터 시장은 주로 전기화가 가장 빠르게 진행되는 프리미엄 부문에서 구조적 대수의 역풍에 직면하고 있습니다. 캐빈 필터, 배터리 팩 냉각용 마이크로 필터, 에어 드라이어용 카트리지가 대항적인 성장을 보이고 있지만, 1대당 대수는 평균적으로 감소하고 있습니다. 중기 수익에 미치는 영향은 지금까지 R&D 예산에서 받은 고가치 흡기 부품에 집중되어 공급업체가 복합 오두막과 열 관리 틈새로 축발을 옮겨야 합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 차내의 공기 품질과 알레르기에 대한 소비자의 관심 증가

- EV의 항속 거리를 극대화하기 위한 초저압 드롭 미디어에 대한 OEM의 움직임

- 필터 엘리먼트의 수 및 사이즈를 줄이는 자동차의 소형화

부문 분석

종이 기반 필터는 2024년 유럽 자동차 에어필터 시장 점유율의 56.17%를 차지했으며 대량 생산되는 승용차 라인 전체에서 신뢰할 수 있는 환기 저항과 비용 효율성을 창출했습니다. 이 전통적인 기재는 성숙한 공급망과 지역의 펄프 가공 능력의 혜택을 받아 수십년 동안 유럽 자동차 에어필터 시장 규모를 지원했습니다. 그러나 휘발성 유기화합물(VOC)의 흡착과 알레르겐의 중화를 제약이 많은 차내에서 소비자가 요구하게 되었기 때문에 활성탄과 신흥 복합재가 2030년까지 연평균 복합 성장률(CAGR)로 6.51%의 성장할 것으로 예상되고 있습니다.

OEM은 셀룰로오스 골격 위에 나노섬유를 적층하고 압력저하를 15Pa 이하로 억제하면서 10나노미터의 입자를 포착하는 하이브리드 시트를 제조하고 있습니다. 거즈와 발포체는 각각 성능 튜닝과 오프 하이웨이 장비에서 틈새 옵션이며, 함유 층과 특대의 구멍이 먼지가 많은 환경에 적합합니다. Euro 7이 성숙함에 따라 종이 점유율은 점차 감소하고 있지만, 재활용 가능한 조성과 저체적 에너지에 의해 관련성이 유지되고 있으며, 유럽의 자동차 에어필터 시장에서 완전한 대체보다는 공존을 확보하고 있습니다.

캐빈 필터는 2024년 유럽 자동차 에어필터 시장 규모의 61.22%를 차지했으며, 그 지위는 유행 후 건강에 대한 우려, 도시 지역에서 스모그의 발생, 알레르기 인증 마케팅상의 어필에 의해 강화되었습니다. 이 분야는 2030년까지 연평균 복합 성장률(CAGR) 6.47%으로 성장해 흡기 여과기를 초과할 것으로 보입니다. 오염된 대도시권에서는 교환 빈도가 연 2회에 달하기도 하기 때문입니다. OEM은 여과 카트리지에 대한 액세스를 글러브 박스의 뒷면에 통합하여 스스로 교체하는 것을 단순화하고 독립 부품 소매 업체의 전자상거래 판매를 자극합니다.

흡기 필터는 잔여 점유율을 다루고 BEV의 대안에 맞서기 위해 노력하고 있지만 여전히 유럽의 대규모 레거시 ICE 차량에 서비스를 제공합니다. 유닛 수요의 난고하에 따라 공급업체는 캐빈용과 HVAC용의 2개의 기능을 가진 미립자 엘리먼트로 다각화를 진행하고 있습니다. EV에서는 캐빈 필터의 선택이 HVAC의 에너지 소비에 영향을 미치기 때문에 첨단 저압 강하 설계가 이익률이 높은 공장 설치를 이겨냅니다. 커넥티드카의 대시보드는 미립자의 축적량이 급증하면 운전자에게 경고를 내리고 적시에 교환을 촉구하며 유럽 자동차 에어필터 시장 전체의 프리미엄 단가를 유지합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차 산업의 고령화에 의한 독립계 애프터마켓(IAM) 수요 증가

- 필터 교환 사이클을 가속시키는 Euro 7과 Euro VI-D의 배기가스 규제

- 차내의 공기 환경과 알레르기에 대한 소비자의 관심 고조

- EV의 항속 거리를 극대화하기 위한 초저압손 미디어의 OEM 추진

- 유럽 전역에 있어서 도시 수준의 저배출 가스 존(LEZ)의 확대

- 구독 기반 OTA 기내 공기 품질 서비스에 의한 정기적인 필터 수익 창출

- 시장 성장 억제요인

- BEV의 보급에 의한 흡기 엔진용 에어필터 수요 축소

- 자동차의 소형화에 의해 필터 엘리먼트의 수나 사이즈가 감소

- 특수 부직포와 활성탄 미디어 공급 병목

- 프리미엄 부문에서 세정 가능한 성능 필터의 채용 증가

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액(USD)

- 소재 유형별

- 종이

- 거즈

- 폼

- 활성탄 및 복합

- 필터 유형별

- 흡기 필터

- 캐빈 필터

- 차종별

- 승용차

- 소형 상용차

- 대형 상용차 및 버스

- 판매 채널별

- OEM

- 애프터마켓

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- MANN HUMMEL

- MAHLE

- Sogefi

- Robert Bosch GmbH

- Donaldson

- Hengst SE

- Freudenberg Filtration Tech.

- Ahlstrom

- Cummins Inc.

- DENSO

- K&N Engineering

- Purolator Filters LLC

- Advanced Flow Engineering

- AIRAID

- S&B Filters

- AL Filters

- JS Automobiles

- Allena Group

- Wsmridhi Manufacturing

- UFI Filters

제7장 시장 기회와 전망

JHS 25.10.28The Europe Automotive Airfilters Market size is estimated at USD 3.62 billion in 2025, and is expected to reach USD 4.93 billion by 2030, at a CAGR of 6.37% during the forecast period (2025-2030).

Strong regulatory momentum around Euro 7, rapid expansion of city-level Low-Emission Zones, and persistent consumer health awareness anchor this expansion. Original-equipment manufacturers (OEMs) are redesigning intake and cabin filtration to meet nanometer-scale particulate limits, and independent aftermarket players are capitalizing on the continent's aging approximately 280 million-unit vehicle-parc. The Europe automotive air filters market is therefore transitioning from commodity volumes toward value-added performance, positioning filtration as a compliance-critical, consumer-visible, and telemetry-enabled component of next-generation mobility.

Europe Automotive Airfilters Market Trends and Insights

Ageing Car-Parc Expanding Independent Aftermarket Demand

Western Europe's average vehicle age reached 12 years in 2025, while Eastern European fleets stretch to 15-20 years. Older internal-combustion-engine (ICE) models require frequent intake and cabin filter swaps, and independent garages capture a considerable share of the regional aftermarket by offering competitive pricing and broad SKU coverage. Even as BEV penetration removes future intake filter demand, the residual ICE fleet guarantees long-dated volume, keeping the Europe automotive air filters market robust through at least one more full replacement cycle. Aftermarket specialists respond by widening SKU assortments for legacy platforms, introducing private-label activated-carbon cabin elements, and adopting e-commerce marketplaces to reach dispersed rural owners.

Euro 7 and Euro VI-D Emission Norms Accelerating Filter Replacement Cycles

The European Commission published Euro 7 rules in May 2024, introducing 10-nanometer particulate thresholds for gasoline vehicles and lifetime compliance for both tailpipe and non-exhaust particles. Because on-board diagnostics now monitor filter degradation, intake and cabin elements must sustain efficiency far longer than legacy, compressing real-world replacement to as low as possible in high-mileage fleets. OEM-grade suppliers therefore bundle higher-margin, multilayer elements that carry regulatory certificates and embedded RFID tags, lifting revenue per unit and reinforcing the Europe automotive air filters market as a critical compliance lever rather than a discretionary maintenance part.

BEV Adoption Shrinking Demand for Intake Engine Air-Filters

Battery-electric vehicles do not require combustion air filtration, removing entire intake filter bill-of-materials from new-vehicle demand. Germany assembled 1.35 million EVs in 2024 and is targeting 1.67 million units in 2025 under fleet-average CO2 rules, while Norway's new-car market reached majority of BEV share. The Europe automotive air filters market therefore confronts a structural volume headwind, chiefly in premium segments where electrification advances fastest. Counterbalancing growth arises in cabin filters, battery-pack cooling micro-filters, and air-drier cartridges-yet unit counts per vehicle fall on average. Medium-term revenue impact centers on high-value intake elements whose margins historically funded R&D budgets, compelling suppliers to pivot toward composite cabin and thermal-management niches.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Consumer Focus on In-Cabin Air Quality and Allergies

- OEM Drive for Ultra-Low Pressure-Drop Media to Maximize EV Range

- Vehicle Downsizing Reducing Number/Size of Filter Elements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper-based filters captured 56.17% of Europe automotive air filters market share in 2024, producing dependable airflow resistance and cost efficiency across high-volume passenger car lines. This traditional substrate underpinned Europe automotive air filters market size for decades, benefitting from mature supply chains and regional pulp processing capacity. Activated-carbon and emerging composite variants, however, are outpacing at 6.51% CAGR to 2030 as consumers demand volatile-organic-compound (VOC) adsorption and allergen neutralization within constrained cabin spaces.

OEMs are layering nanofibers atop cellulose backbones, creating hybrid sheets that trap 10-nanometer particles while holding pressure drops below 15 Pa. Gauze and foam remain niche options in performance tuning and off-highway equipment, respectively, where oil-impregnated layers or oversized pores suit dusty environments. As Euro 7 matures, paper's share erodes gradually but retains relevance due to recyclable composition and low embodied energy, ensuring coexistence rather than outright displacement inside the Europe automotive air filters market.

Cabin filters held 61.22% of the Europe automotive air filters market size in 2024, a position fortified by post-pandemic health concerns, urban smog episodes, and the marketing appeal of allergy certification. The segment grows at a 6.47% CAGR through 2030, outpacing intake filters, because replacement frequency can reach twice per year in polluted metropolitan zones. OEMs integrate filtration cartridge access behind glove boxes, simplifying do-it-yourself swaps and stimulating e-commerce sales by independent parts retailers.

Intake filters, covering the residual share, confront BEV substitution but still service Europe's large legacy ICE fleet. Turbulence in unit demand pushes suppliers to diversify toward dual-function cabin and HVAC micro-particle elements. Within EVs, cabin filter selection affects HVAC energy draw; thus, advanced low-pressure-drop designs win high-margin factory installs. Connected vehicle dashboards now alert drivers when particulate accumulation spikes, triggering timely replacements and preserving premium unit values across the Europe automotive air filters market.

The Europe Automotive Airfilters Market Report is Segmented by Material Type (Paper, Gauze, and More), Filter (Intake Filters and Cabin Filters), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEM and Aftermarket), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- MANN+HUMMEL

- MAHLE

- Sogefi

- Robert Bosch GmbH

- Donaldson

- Hengst SE

- Freudenberg Filtration Tech.

- Ahlstrom

- Cummins Inc.

- DENSO

- K&N Engineering

- Purolator Filters LLC

- Advanced Flow Engineering

- AIRAID

- S&B Filters

- AL Filters

- JS Automobiles

- Allena Group

- Wsmridhi Manufacturing

- UFI Filters

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing car-parc expanding independent aftermarket (IAM) demand

- 4.2.2 Euro 7 & Euro VI-D emission norms accelerating filter replacement cycles

- 4.2.3 Heightened consumer focus on in-cabin air quality & allergies

- 4.2.4 OEM drive for ultra-low pressure-drop media to maximise EV range

- 4.2.5 Expansion of city-level Low-Emission Zones (LEZs) across Europe

- 4.2.6 Subscription-based OTA cabin-air-quality services creating recurring filter revenue

- 4.3 Market Restraints

- 4.3.1 BEV adoption shrinking demand for intake engine air-filters

- 4.3.2 Vehicle downsizing reducing number/size of filter elements

- 4.3.3 Supply bottlenecks for specialty non-woven & activated-carbon media

- 4.3.4 Rising adoption of washable performance filters in premium segment

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Material Type

- 5.1.1 Paper

- 5.1.2 Gauze

- 5.1.3 Foam

- 5.1.4 Activated-carbon / Composite

- 5.2 By Filter Type

- 5.2.1 Intake Filters

- 5.2.2 Cabin Filters

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles & Buses

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 MANN+HUMMEL

- 6.4.2 MAHLE

- 6.4.3 Sogefi

- 6.4.4 Robert Bosch GmbH

- 6.4.5 Donaldson

- 6.4.6 Hengst SE

- 6.4.7 Freudenberg Filtration Tech.

- 6.4.8 Ahlstrom

- 6.4.9 Cummins Inc.

- 6.4.10 DENSO

- 6.4.11 K&N Engineering

- 6.4.12 Purolator Filters LLC

- 6.4.13 Advanced Flow Engineering

- 6.4.14 AIRAID

- 6.4.15 S&B Filters

- 6.4.16 AL Filters

- 6.4.17 JS Automobiles

- 6.4.18 Allena Group

- 6.4.19 Wsmridhi Manufacturing

- 6.4.20 UFI Filters

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment