|

시장보고서

상품코드

1836559

국소 약물전달 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Topical Drug Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

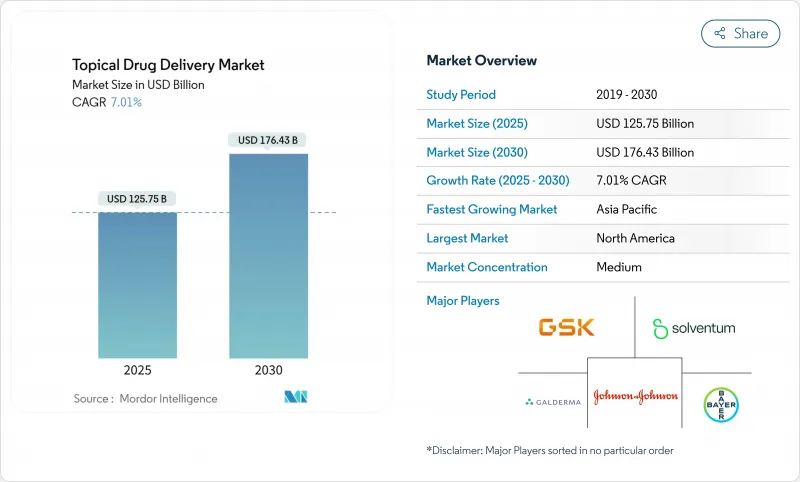

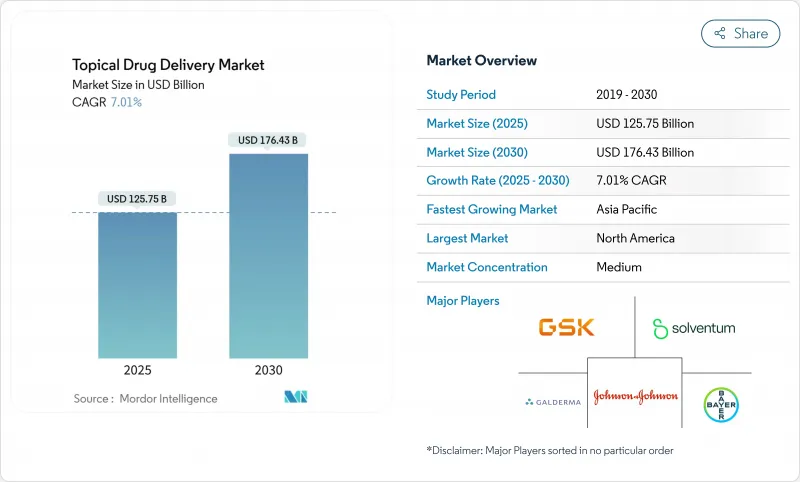

세계의 국소 약물전달 시장은 2025년 1,257억 5,000만 달러에 이르고, 2030년까지 1,764억 3,000만 달러에 이를 것으로 예측되며, CAGR은 7.01%가 될 것으로 보입니다.

이 확장은 기존의 크림과 연고에서 정밀 가공 패치, 마이크로니들 어레이, 스마트 센서 지원 장비로의 이동 정밀도와 치료 어드히어런스를 향상시키는 변화를 반영합니다. 비침습적인 만성 질환 치료제에 대한 강한 수요, 비오피오이드성 통증 치료제에 대한 규제 당국의 지원, 생물학적 제제의 급속한 진보가 종합적으로 기세를 지원하고 있습니다. 또한 대상을 좁힌 피부과 치료제의 꾸준한 출시 페이스와 임상의가 환자의 컴플라이언스를 원격 감시할 수 있는 커넥티드 헬스 에코시스템의 역할 확대도 기업의 이익이 되고 있습니다. 이러한 배경에서 국소 약물전달 시장은 선도적인 제약 제조업체와 전달 플랫폼에 특화된 민첩한 생명 공학 기업을 계속 끌어들이고 있습니다.

세계 국소 약물전달 시장 동향과 통찰

만성 및 감염성 피부질환이 높은 만연

건선과 아토피 피부염과 같은 만성 피부 질환은 여전히 세계에서 가장 흔한 10대 질환 중 하나입니다. 건선만으로도 2024년 4,000만명 이상이 앓고 있었으며, 국부 생물제제의 꾸준한 처방 증가에 박차를 가하고 있습니다. 2024년 12월에 승인된 Galderma의 Nemluvio는 1,900명의 환자를 대상으로 한 시험에서 뛰어난 가려움증 감소 효과를 보였으며, IL-31 길항제가 중등도에서 중증의 아토피 피부염 관리를 어떻게 재구성하는지를 명확히 하였습니다. 인공지능을 이용한 피부 매핑 도구는 현재 개별화된 요법을 이끌고 있으며, 200만 장의 이미지로 훈련된 멀티모달 시각 모델은 임상에서의 진단 정확도를 높입니다. 역학적 압력과 기술의 융합이 결합되어 만성 질환 관리는 국소 약물전달 시장의 장기적인 성장 엔진으로 자리매김하고 있습니다.

통증과 호르몬 치료에서 경피 패치의 급속한 보급

미국 식품의약국은 2025년 1월 Journavx(수제트리긴)를 중등도에서 심한 급성 통증에 적응하는 최초의 비오피오이드 패치로 승인했습니다. 이 결정은 새로운 비중독성 진통제에 대한 규제 당국의 긍정적인 지원을 보여줍니다. 호르몬 요법에서 Bayer의 엘린자네탄트 신약 승인 신청은 2030년까지 예상되는 세계 갱년기 인구 12억 명의 혈관운동 증상을 대상으로 합니다. Medherant의 TEPI 플랫폼과 같은 새로운 접착성 화학물질은 장기간 착용시 균일한 복용량을 제공하고 경구 요법보다 패치를 선호하는 환자를 증가시킵니다. 그 결과, 경피 흡수형 제제는 국소 약물 전달 시장 전체에서 점유율을 계속 확대하고 있습니다.

코르티코스테로이드 국부제의 세계 가격 규제의 엄격함

많은 정부들이 기준가격 제도를 엄격히 하고 있으며, 주류 코르티코스테로이드 제품의 금리를 줄이고 신규 전달 연구에 사용할 수 있는 현금 흐름을 제한하고 있습니다. 2025년에는 여러 브랜드 제제의 특허가 끊어지기 때문에 특히 판매량이 많은 신흥 시장에서는 저가 경쟁이 더욱 격화됩니다. 복잡한 생물학적 제형 파이프라인이 더 높은 R&D 투자를 요구하고 외용약 전달 시장의 특정 분야의 성장을 억제할 수 있는 압박 요인이 되었음에도 불구하고 공급업체는 비용 구조를 재구성해야 합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 고령 인구 증가

- 자기 투여 및 재택 케어에 적합한 포맷에 대한 수요

- 자주 발생하는 오염으로 인한 제품 리콜 및 경고장

부문 분석

경피 약물전달은 2024년에 국소 약물전달 시장 점유율의 45.33%를 차지했습니다. 생물학적 제제와 스마트 패치가 피부과와 전신에 침투함에 따라, 피부로부터의 국소 약물 전달 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 한편, 비강 투여는 편두통, 호흡기 감염, 신경학적 구조요법을 위한 비강내 스프레이의 보급에 따라 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 9.46%로 성장을 지속하고, 있습니다. 비강용으로 처방 된 안티센스 올리고 뉴클레오타이드의 파이프라인이 증가하고 상업적 열정을 나타냅니다. 디지털 헬스의 통합은 현재 투여 기록을 전자 의료 기록 장치에 중계하는 센서가 있는 패치를 통해 경피 경로로 확장되고 있으며, 연결된 흡입기도 폐에 적용하기 위해 유사한 피드백 루프를 제공합니다. 안과 치료는 눈 표면에 대한 손상을 줄이는 방부제가 없는 다회 투여 병을 제공하며 폐 장치는 진동 메쉬 기술을 활용하여 폐 깊은 곳에 침착을 향상시킵니다.

미세 바늘과 비강 및 피부 플랫폼의 융합은 고분자에 대한 접근을 넓히고 있습니다. 스마트 인터페이스는 앱 기반 튜토리얼을 통해 사용자를 안내하고 투약 실수를 줄입니다. 한편, 직장이나 경구 점막에의 투여는 각각 완화 케어나 뺨으로부터의 백신 투여라는 틈새 관계를 유지하고 있습니다. 모든 경로에서 제형 과학자들은 침투 촉진제, 나노에멀전 및 in situ 겔의 채택을 증가시켜 안전성을 손상시키지 않고 투여 목표를 달성합니다. 이러한 광범위한 툴박스는 새로운 임상 요구에 대응하는 각 경로의 능력을 강화하고 국소 약물전달 시장의 장기적인 다양화를 촉진합니다.

기존의 크림, 젤, 로션 및 스프레이는 2024년 국소 약물 전달 시장 규모의 71.21%를 차지했습니다. 이 제품은 의사에게 널리 받아들여지고 제조 규모가 크기 때문에 높은 시장 규모를 유지합니다. 발포체와 같은 반고형제는 신속한 흡수를 선호하는 환자에게 인기가 있으며, 용액은 정량 투여 어플리케이터가 정확성을 높이는 안과 및 비강 관리로 번영합니다. 고형 필름과 분말은 여전히 작지만, 이동 중에 상처 케어와 소아에게 투여하는 데 필수적입니다.

패치, 마이크로니들 어레이, 스마트 붕대, 약물 용출성 드레싱을 포함한 디바이스 카테고리는 CAGR이 8.35%로 분명히 기세가 있습니다. Solventum의 VAC 필 앤 플레이스 시스템은 임상 전개 중에 병원에서의 작업 시간을 61% 단축하고 치료비를 41% 절감했습니다. 세마글루타이드와 같은 체중 관리제를 위한 프로그래머블 마이크로니들 패치는 기존의 크림으로는 불가능했던 한 달에 한 번의 투여 사이클을 가능하게 했습니다. 전자기기의 비용이 낮아지고 유연한 회로가 성숙함에 따라 '제형+장치'의 하이브리드 제품이 카테고리 경계를 모호하게 하고 모니터링과 데이터 취득을 통해 부가가치를 높이고 있습니다.

지역별 분석

북미는 깊은 연구개발 파이프라인, 1인당 높은 헬스케어 지출, 획기적인 디바이스의 신속한 규제 대응에 힘입어 2024년 매출 점유율은 38.77%를 유지했습니다. 미국은 통원 횟수 감소에 보답하는 가치 기반 상환을 통해 패치 채용을 추진하고 있습니다. 캐나다는 단일 지불 제도 내에서 바이오시밀러 크림 수요가 높다는 것을 보여주고 있으며, 멕시코의 민간 클리닉에서는 당뇨병성 궤양 치료를 위한 스마트 드레싱재의 재고가 증가하고 있습니다.

아시아태평양은 2024년 벤처 기업 자금 조달이 22% 감소하더라도 CAGR이 가장 빠른 9.56%를 나타냅니다. 중국은 국내 마이크로니들 신흥 기업에 자금을 제공하고 국내 및 수출 수요를 공급하는 대규모 GMP 공장을 지원합니다. 일본은 고령화의 가속에 직면하고 있으며, 붙이기 쉬운 진통 패치의 매출을 밀어 올리고 있습니다. Cipla가 주도하는 인도의 호흡기 영역 포트폴리오는 전년 대비 17.9% 증가하여 특수 기기에 대한 국내 수요 증가를 나타냈습니다. 한국에서는 녹내장 증가에 대응하기 위해 안과용제 Rhopressa가 승인되고 호주에서는 농촌 환자를 위한 원격 감시 솔루션이 추진되고 있습니다.

유럽은 꾸준한 성장을 기록하고 지속가능성에 관한 법규제로 주도하고 있습니다. 프랑스와 영국은 AI와 연동된 피부과 네트워크를 시험적으로 도입하여 규제 당국에 실세계의 증거를 제공합니다. 동유럽은 저성장이지만 제네릭 의약품에 대한 수요가 왕성하고, 국소 약물전달 업계의 수탁 제조업자의 타겟이 되고 있습니다. 남미와 중동 및 아프리카는 현재 규모가 작지만 건강 관리 인프라가 성숙하고 디지털 건강 연결이 확산됨에 따라 미래에 상승 할 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 및 감염성 피부질환의 높은 유병률

- 통증 및 호르몬 치료에서 경피 흡수형 패치의 급속한 보급

- 노년 인구 증가

- 자기 투여 및 재택 케어에 적합한 투약 형태 수요

- 고분자 마이크로니들의 돌파구에 의한 고분자 전달의 실현

- 장기 투여 컴플라이언스를 촉진하는 스마트 및 커넥티드 패치

- 시장 성장 억제요인

- 세계 코르티코스테로이드 국부약의 엄격한 가격 통제

- 빈번한 오염에 기인하는 제품 리콜과 경고장

- 강화제를 사용하지 않는 생물제제의 피부 투과성의 제한

- 유럽에서의 ESG 주도의 페트로라탐 기반의 단계적 폐지

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 투여 경로별

- 경피

- 안과

- 경비

- 구강 점막

- 귀

- 직장

- 질

- 폐(흡입)

- 기타

- 제품별

- 제형

- 고체(분말, 필름)

- 반고형

- 크림

- 연고

- 젤 및 페이스트

- 액체(용액, 스프레이)

- 폼

- 디바이스

- 경피 패치

- 마이크로니들 패치

- 흡입기 및 네뷸라이저

- 정량 분무기

- 제형

- 적응증별

- 피부과 영역(습진, 건선, 여드름)

- 통증 관리(근골격계, 신경 장애)

- 안과(안구건조증, 녹내장)

- 호흡기(천식, COPD)

- 이비인후과 및 비감염증

- 호르몬 보충 요법

- 중추신경계질환(편두통, 파킨슨병)

- 기타

- 최종 사용자별

- 병원

- 전문 클리닉 및 피부과 센터

- 재택치료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Bayer AG

- Johnson & Johnson

- GlaxoSmithKline plc

- Novartis AG

- Galderma SA

- Solventum

- Bausch Health Companies Inc.

- Hisamitsu Pharmaceutical Co.

- Cipla Ltd.

- Viatris Inc.

- MedPharm Ltd.

- Pfizer Inc.

- Leo Pharma A/S

- Sun Pharma Industries Ltd.

- AbbVie Inc.(Allergan)

- Teva Pharmaceutical Industries

- Lupin Ltd.

- Perrigo Company plc

- Taro Pharmaceutical Industries

- Glenmark Pharmaceuticals

제7장 시장 기회와 전망

JHS 25.10.28The topical drug delivery market stands at USD 125.75 billion in 2025 and is forecast to reach USD 176.43 billion by 2030, posting a 7.01% compound annual growth rate (CAGR).

This expansion reflects the shift from conventional creams and ointments toward precision-engineered patches, microneedle arrays, and smart, sensor-enabled devices that improve dosing accuracy and treatment adherence. Strong demand for non-invasive chronic-disease therapies, regulatory support for non-opioid pain solutions, and rapid progress in biologic formulations collectively sustain momentum. Companies also benefit from the steady launch pace of targeted dermatology drugs and the broadening role of connected health ecosystems that allow clinicians to monitor patient compliance remotely. Against this backdrop, the topical drug delivery market continues to attract both large pharmaceutical manufacturers and agile biotechnology firms that specialize in delivery platforms.

Global Topical Drug Delivery Market Trends and Insights

High prevalence of chronic & infectious skin diseases

Chronic skin disorders such as psoriasis and atopic dermatitis remain among the ten most common health conditions worldwide. Psoriasis alone affected more than 40 million people in 2024, spurring steady prescription growth for topical biologics. Galderma's Nemluvio, approved in December 2024, demonstrated superior itch reduction in trials with 1,900 patients, underscoring how IL-31 antagonists reshape moderate-to-severe atopic dermatitis management. Artificial-intelligence skin-mapping tools now guide personalized regimens, while multimodal vision models trained on two million images boost diagnostic accuracy in clinics. Together, epidemiologic pressure and technology convergence position chronic-disease care as a long-duration growth engine for the topical drug delivery market.

Rapid adoption of transdermal patches in pain & hormone therapy

The United States Food and Drug Administration cleared Journavx (suzetrigine) in January 2025 as the first non-opioid patch indicated for moderate to severe acute pain. The decision signals regulatory willingness to back novel, non-addictive analgesics. In hormone therapy, Bayer's elinzanetant New Drug Application targets vasomotor symptoms for the 1.2 billion global menopausal population anticipated by 2030. New adhesive chemistries such as Medherant's TEPI platform deliver uniform doses over extended wear periods, driving patient preference for patches over oral regimens. As a result, transdermal modalities continue to capture share within the broader topical drug delivery market.

Stringent global price controls on topical corticosteroids

Many governments have tightened reference pricing schemes, compressing margins on mainstream corticosteroid products and restricting cash flow available for novel delivery research. Patent expiries in 2025 for several branded formulations further intensify low-price competition, particularly in high-volume emerging markets. Suppliers are forced to re-engineer cost structures even as complex biologic pipelines demand higher R&D investment, creating a squeeze that could moderate growth in certain segments of the topical drug delivery market.

Other drivers and restraints analyzed in the detailed report include:

- Rising geriatric population

- Demand for self-administration & home-care-friendly formats

- Frequent contamination-driven product recalls & warning letters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dermal deliveries captured 45.33% of topical drug delivery market share in 2024, reflecting broad clinical familiarity and patient comfort. The topical drug delivery market size attached to dermal routes is forecast to expand steadily as biologics and smart patches penetrate dermatology and systemic indications. Nasal delivery, however, is registering the fastest 9.46% CAGR to 2030 as intranasal sprays for migraine, respiratory infections, and neurologic rescue therapy gain traction. A growing pipeline of antisense oligonucleotides formulated for the nasal cavity demonstrates commercial enthusiasm. Digital health integration now extends to dermal routes through sensor-equipped patches that relay dose records to electronic health records, while connected inhalers offer similar feedback loops for pulmonary applications. Ophthalmic therapy benefits from preservative-free multi-dose bottles that reduce ocular surface damage, and pulmonary devices leverage vibrating mesh technology to improve deep-lung deposition.

The convergence of microneedles with nasal and dermal platforms is widening access to large molecules. Smart interfaces guide users through app-based tutorials, lowering administration errors. Meanwhile, rectal and oral-mucosal routes maintain niche relevance for palliative care and buccal vaccine delivery, respectively. Across all pathways, formulation scientists increasingly employ permeation enhancers, nanoemulsions, and in situ gels to meet dosing targets without compromising safety. This broad toolbox strengthens each route's ability to address emerging clinical needs, reinforcing the long-term diversification of the topical drug delivery market.

Traditional creams, gels, lotions, and sprays represented 71.21% of topical drug delivery market size in 2024. Their entrenched physician acceptance and manufacturing scale keep volumes high. Semi-solids such as foams are popular with patients who prefer quick absorption, whereas liquids thrive in ophthalmology and nasal care where metered-dose applicators enhance accuracy. Solid films and powders remain small but essential for on-the-go wound care and pediatric dosing.

The devices category-comprising patches, microneedle arrays, smart bandages, and drug-eluting dressings-shows an 8.35% CAGR and is the clear momentum play. Solventum's V.A.C. Peel and Place system lowered hospital-labor time by 61% and treatment costs by 41% during clinical rollout. Programmable microneedle patches for weight-management agents such as Semaglutide demonstrate that devices can unlock monthly dosing cycles impossible with traditional creams. As electronics costs fall and flexible circuits mature, hybrid "formulation-plus-device" products blur category boundaries, adding value through monitoring and data capture.

The Topical Drug Delivery Market is Segmented by Route of Administration (Dermal, Ophthalmic, Nasal, and More), Product (Formulations [Solid, Semi-Solid and More] and Device [Transdermal Patches and More]), Indications (Dermal, Pain Management and More), End User (Hospitals, Home-Care Settings and More) and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained a 38.77% revenue share in 2024, backed by deep R&D pipelines, high healthcare expenditure per capita, and fast regulatory turnarounds for break-through devices. The United States drives patch adoption through value-based reimbursement that rewards fewer hospital visits. Canada shows strong demand for biosimilar creams within its single-payer scheme, while Mexico's private-sector clinics increasingly stock smart dressings for diabetic ulcer care.

Asia-Pacific shows the fastest 9.56% CAGR, even as venture funding fell 22% in 2024. China funds domestic microneedle startups and supports large-scale GMP plants that supply domestic and export demand. Japan faces accelerated aging, boosting sales of easy-to-apply analgesic patches. India's respiratory portfolio, led by Cipla, expanded 17.9% year over year and demonstrates rising domestic appetite for specialty devices. South Korea approved Rhopressa ophthalmic solution to address rising glaucoma prevalence, while Australia promotes remote monitoring solutions for rural patients.

Europe registers steady growth and leads in sustainability legislation, prompting rapid petrolatum replacement in Germany and the Nordic region. France and the United Kingdom pilot AI-linked dermatology networks that feed real-world evidence to regulators. Eastern Europe grows off a lower base but exhibits strong demand for generics, making it a target for contract manufacturers operating within the topical drug delivery industry. South America and the Middle East & Africa remain smaller today but represent future upside as healthcare infrastructure matures and digital-health connectivity widens.

- Bayer

- Johnson & Johnson

- GlaxoSmithKline

- Novartis

- Galderma

- Solventum

- Bausch Health

- Hisamitsu Pharmaceutical Co.

- Cipla

- Viatris

- MedPharm Ltd.

- Pfizer

- Leo Pharma

- Sun Pharma Industries Ltd.

- Abbvie

- Teva Pharmaceutical Industries

- Lupin

- Perrigo Company

- Taro Pharmaceutical Industries

- Glenmark Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Prevalence Of Chronic & Infectious Skin Diseases

- 4.2.2 Rapid Adoption Of Transdermal Patches In Pain & Hormone Therapy

- 4.2.3 Rising Geriatric Population

- 4.2.4 Demand For Self-Administration & Home-Care-Friendly Formats

- 4.2.5 Polymeric Microneedle Breakthroughs Enabling Large-Molecule Delivery

- 4.2.6 Smart/Connected Patches Driving Longitudinal Dosing Compliance

- 4.3 Market Restraints

- 4.3.1 Stringent Global Price Controls On Topical Corticosteroids

- 4.3.2 Frequent Contamination-Driven Product Recalls & Warning Letters

- 4.3.3 Limited Skin Permeation Of Biologics Without Enhancers

- 4.3.4 ESG-Driven Phase-Out Of Petrolatum Bases In Europe

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Route of Administration

- 5.1.1 Dermal

- 5.1.2 Ophthalmic

- 5.1.3 Nasal

- 5.1.4 Oral Mucosal

- 5.1.5 Otic

- 5.1.6 Rectal

- 5.1.7 Vaginal

- 5.1.8 Pulmonary (Inhalational)

- 5.1.9 Others

- 5.2 By Product

- 5.2.1 Formulations

- 5.2.1.1 Solid (powders, films)

- 5.2.1.2 Semi-Solid

- 5.2.1.2.1 Creams

- 5.2.1.2.2 Ointments

- 5.2.1.2.3 Gels & Pastes

- 5.2.1.3 Liquid (solutions, sprays)

- 5.2.1.4 Foams

- 5.2.2 Devices

- 5.2.2.1 Transdermal Patches

- 5.2.2.2 Microneedle Patches

- 5.2.2.3 Inhalers & Nebulisers

- 5.2.2.4 Metered-Dose Sprayers

- 5.2.1 Formulations

- 5.3 By Indication

- 5.3.1 Dermatology (Eczema, Psoriasis, Acne)

- 5.3.2 Pain Management (Musculoskeletal, Neuropathic)

- 5.3.3 Ophthalmology (Dry-eye, Glaucoma)

- 5.3.4 Respiratory (Asthma, COPD)

- 5.3.5 ENT & Nasal Infections

- 5.3.6 Hormone Replacement Therapy

- 5.3.7 CNS Disorders (Migraine, Parkinson's)

- 5.3.8 Others

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics & Dermatology Centers

- 5.4.3 Home-Care Settings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Bayer AG

- 6.3.2 Johnson & Johnson

- 6.3.3 GlaxoSmithKline plc

- 6.3.4 Novartis AG

- 6.3.5 Galderma SA

- 6.3.6 Solventum

- 6.3.7 Bausch Health Companies Inc.

- 6.3.8 Hisamitsu Pharmaceutical Co.

- 6.3.9 Cipla Ltd.

- 6.3.10 Viatris Inc.

- 6.3.11 MedPharm Ltd.

- 6.3.12 Pfizer Inc.

- 6.3.13 Leo Pharma A/S

- 6.3.14 Sun Pharma Industries Ltd.

- 6.3.15 AbbVie Inc. (Allergan)

- 6.3.16 Teva Pharmaceutical Industries

- 6.3.17 Lupin Ltd.

- 6.3.18 Perrigo Company plc

- 6.3.19 Taro Pharmaceutical Industries

- 6.3.20 Glenmark Pharmaceuticals

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment