|

시장보고서

상품코드

1836655

영국의 약물전달 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United Kingdom Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

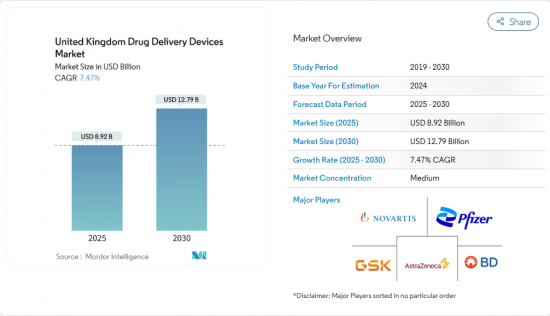

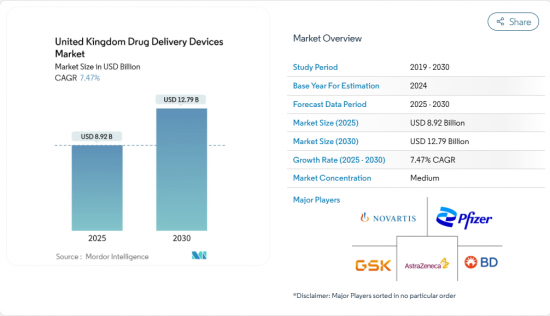

영국의 약물전달 기기 시장은 2025년에 89억 2,000만 달러로 평가되고, 2025-2030년의 CAGR은 7.47%를 나타내, 2030년에는 127억 9,000만 달러에 달할 것으로 예상되고 있습니다.

정밀의료를 추진하는 국민 보건 서비스(NHS), 재택 의료 환경의 채용 증가, 혁신적인 기기 시장 투입까지의 시간을 단축하는 승인 경로의 가속화 등이 성장을 뒷받침하고 있습니다. 치료 순응도가 1% 향상될 때마다, NHS는 입원 회피로 약 5억 파운드를 절약할 수 있을 것으로 추정되고, 비용 절감이 조달 전략의 중심에 자리잡고 있습니다. 브렉짓 후 규제는 UKCA 마킹으로 전환되었지만, 새로운 국제적인 신뢰성 절차는 호주, 캐나다, 유럽 연합, 미국에서 승인된 장치가 더 빠르게 영국의 약물전달 기기 시장에 진입할 수 있게 해주며, 외국 혁신자들에게 영국의 매력을 유지하고 있습니다. 지속가능성도 중요합니다. 차세대 가압식 정량 흡입기(pMDI)의 지구 온난화 계수(GWP) 제로에 가까운 추진제는 제조업체가 이산화탄소 감소 목표를 달성하면서 NHS 입찰을 획득하는 데 도움이 됩니다. 연결 장치의 병렬 급증은 NHS가 매년 약 6억 3,700만 파운드를 소비하는 복약 불준수에 대응합니다.

영국의 약물전달 기기 시장 동향과 인사이트

자기 관리와 재택 관리를 위한 정부의 이니셔티브

2025년에 장애인 시설 보조금이 8,600만 파운드 추가되어 더 많은 환자들이 집에서 병리를 관리할 수 있게 되었으며 현재 거의 모든 지역 약국에서 7개의 경증 질환을 다루는 Pharmacy First 체계를 보완하고 있습니다. 인공 췌장 기술을 5년 동안 배포하는 NHS의 계획은 직관적인 자기 사용 시스템에 대한 정책 중심 수요를 보여줍니다. 이러한 조치는 펜형 주사기, 웨어러블 펌프, 아마추어 조작용으로 설계된 흡입기 등 영국 약물전달 기기 시장에 볼륨을 흘리고 있습니다.

스마트 커넥티드 기기 개발 및 채택

커넥티드 기기는 전자 차트의 보급률이 NHS 트러스트의 95%에 이르면서 2030년까지 영국 헬스케어에서 CAGR이 2자리수가 될 것으로 예측됩니다. MedTech Funding Mandate 하에서 상환된 스마트 흡입기와 인슐린 펜의 DOSE와 같은 블루투스 애드온은 IoT 통합이 연간 2만 2,000명의 조기 사망으로 이어지는 논어히어런스를 어떻게 다루는지를 보여줍니다. 디지털 헬스케어 플랜으로 구축된 광범위한 데이터 백본을 통해 이러한 기기는 실시간 투여 데이터를 임상 워크플로에 직접 캡처할 수 있습니다.

엄격한 단편화된 규제 상황과 브렉짓 후 문제

제조체는 2030년까지 CE 인증과 UKCA 인증을 모두 유지해야 하며, 2025년 6월 발효 시판 후 감시 규칙은 심각한 인시던트의 정의를 확대합니다. 영국 이외공급업체는 책임자를 임명해야 하며 비용과 복잡성이 증가하지만 승인 기관의 확대와 국제 신뢰 경로가 부분적으로 완화됩니다.

부문 분석

2024년 영국의 약물전달 기기 시장 점유율은 주사제가 45.6%를 차지했습니다. 생물 제제의 보급과 자가주사에 대한 환자의 선호가이 리드의 이유입니다. 센서와 무선 모듈의 통합으로 프리필드 펜은 데이터가 풍부한 치료 순응도 툴로 변모하고 있습니다. 2025년부터 2030년까지는 OxCD3 등의 연구센터가 수개월에 걸쳐 약제를 방출하는 초음파 트리거 저장소를 개발하고 있기 때문에 임베디드 시스템의 CAGR이 가장 빠른 10.86%를 나타낼 전망입니다.

흡입제 부문은 NHS의 탈탄소화 목표로부터 혜택을 받았으며, GWP 제로에 가까운 추진제를 사용하여 pMDI에 조달하는 것을 조타하고 있습니다. 경피 패치는 마이크로니들 어레이가 바늘을 사용하지 않고 침투성을 개선함에 따라 확대되고 있습니다. 경비 및 경안용 장치는 여전히 틈새 시장이지만 영국의 약물전달 시장 전체의 다양화를 반영하여 전문적인 연구 개발 자금을 모으고 있습니다.

주사제는 2024년 매출의 52.3%를 차지하고 대용량 주사기의 처리 능력을 향상시키는 현대적인 무균 허브에 NHS에 의한 2억 400만 파운드의 투자를 활용했습니다. 그러나 경구 점막 시스템은 초기 통과 대사를 피하고 몇 분 이내에 혈장 중 농도가 피크에 달하는 점착 필름으로 예측 CAGR 9.38%로 지보를 굳히고 있습니다.

흡입 경로는 지속가능성의 의무화로부터 혜택을 받고, 경피 패치는 무통의 선택을 요구하는 환자 수요에 부응합니다. 비강 투여는 신경 질환에 대한 뇌로의 직접 전달을 약속하는 것으로, 알츠하이머 병과 파킨슨 병의 치료를 재구성 할 수있는 영국 약물전달 기기 시장에서 백스페이스의 기회입니다. 눈 임플란트는 매달 주사에서 반기 삽입으로 이동하고 있으며, 클리닉의 부담을 줄이고 치료 순응도를 향상시킵니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자기 투여와 재택 케어에 대한 정부의 대처와 동향

- 스마트·커넥티드·약물전달의 개발과 보급

- 연구개발 이니셔티브 증가와 정부의 지원

- 생물 제제 파이프라인의 성장이 고도의 주사기 수요를 견인

- 만성 질환 및 감염증의 유행과 이환율의 상승

- 브렉지트 후의 배합제의 신속 승인

- 시장 성장 억제요인

- 브레그지트 후의 지연과 비용에 관한 과제

- 높은 개발·제조 비용과 한정된 국내 클린 룸 제조 능력

- 다양한 기기와 관련된 위험과 우려

- NHS 가격 설정 및 리베이트 압력

- 가치/공급망 분석

- 규제와 기술적 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액-달러)

- 기기 유형별

- 주사 투여 기기

- 흡입 투여 기기

- 주입 펌프

- 경피 패치

- 이식형 약물전달 시스템

- 안구 삽입물 및 투여 임플란트

- 비강 및 구강 점막 투여 기기

- 투여 경로별

- 주사제

- 흡입제

- 경피제

- 구강 점막제(구강 내 및 설하)

- 안구제

- 비강제

- 용도별

- 당뇨병

- 호흡기 질환

- 종양학

- 심혈관 질환

- 감염성 질환

- 신경계 질환

- 기타

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 재택 의료 환경

- 전문 클리닉

- 기타

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Pfizer Inc.

- AstraZeneca plc

- GlaxoSmithKline plc

- Novartis AG

- F. Hoffmann-La Roche Ltd

- Solventum

- Becton, Dickinson and Company

- Baxter International Inc.

- Ypsomed AG

- Nemera

- Gerresheimer AG

- AptarGroup Inc.

- Owen Mumford Ltd.

- Teva Pharmaceutical Industries Ltd.

- West Pharmaceutical Services Inc.

- SHL Medical

- ICU Medical

- Terumo Corporation

- Insulet Corporation

- Tandem Diabetes Care, Inc.

제7장 시장 기회와 전망

KTH 25.11.04The United Kingdom drug delivery devices market is valued at USD 8.92 billion in 2025 and is forecast to reach USD 12.79 billion by 2030, reflecting a 7.47% CAGR during 2025-2030.

Growth is propelled by the National Health Service (NHS) drive for precision medicine, rising adoption of home-based care, and accelerated approval pathways that shorten time-to-market for innovative devices. Every 1% gain in adherence is estimated to save the NHS about GBP 500 million in avoided hospital admissions, keeping cost reduction at the center of procurement strategies. Post-Brexit regulation has shifted to UKCA marking, yet the new International Reliance procedure allows devices cleared in Australia, Canada, the European Union, or the United States to enter the United Kingdom drug delivery devices market more rapidly, sustaining the country's attractiveness for foreign innovators. Sustainability also matters: near-zero global-warming-potential (GWP) propellants in next-generation pressurised metered-dose inhalers (pMDIs) are helping manufacturers win NHS tenders while meeting carbon-reduction targets. A parallel surge in connected devices responds to medication non-adherence that costs the NHS roughly GBP 637 million each year.

United Kingdom Drug Delivery Devices Market Trends and Insights

Government initiatives for self-administration & homecare

An extra GBP 86 million added to the Disabled Facilities Grant in 2025 enables more patients to manage conditions at home, complementing the Pharmacy First scheme that now covers seven minor conditions at almost every community pharmacy. The NHS plan to distribute artificial-pancreas technology over five years exemplifies policy-driven demand for intuitive self-use systems. Such measures channel volume into the United Kingdom drug delivery devices market for pen injectors, wearable pumps, and inhalers designed for layperson operation.

Development and adoption of smart connected drug delivery devices

Connected devices are expected to post a doubt digit CAGR in United Kingdom healthcare through 2030 as electronic health-record coverage climbs toward 95% of NHS trusts. Smart inhalers reimbursed under the MedTech Funding Mandate and Bluetooth add-ons like DOSE for insulin pens show how IoT integration addresses non-adherence that leads to 22,000 premature deaths a year. The broad data backbone being built by the Digital Health and Care Plan lets these devices feed real-time dosing data directly into clinical workflows.

Stringent fragmented regulatory landscape coupled with post-Brexit challenges

Manufacturers must maintain both CE and UKCA certification until 2030, and the post-market-surveillance rules effective June 2025 widen the definition of a serious incident. Non-UK suppliers must appoint a Responsible Person, adding cost and complexity, although expansion of approved bodies and an International Reliance route offer partial relief.

Other drivers and restraints analyzed in the detailed report include:

- Biologics pipeline growth driving advanced injectors demand

- Increasing R&D investment

- High development and manufacturing cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Injectable formats held 45.6% of the United Kingdom drug delivery devices market share in 2024. The prevalence of biologics and patient preference for self-injection explain this lead. Integration of sensors and wireless modules is turning prefilled pens into data-rich adherence tools. Over 2025-2030, implantable systems will post the fastest 10.86% CAGR as research centers such as OxCD3 advance ultrasound-triggered depots that release drugs over months.

The inhalation segment benefits from NHS decarbonisation targets, steering procurement toward pMDIs with near-zero GWP propellants. Transdermal patches are expanding as microneedle arrays improve permeability without needles. Nasal and ocular devices remain niche but attract specialised R&D funding, reflecting an overall diversification of the United Kingdom drug delivery devices market.

Injectables delivered 52.3% of revenue in 2024 and leverage NHS investment of GBP 204 million into modern aseptic hubs that raise throughput for large-volume syringes. Oral mucosal systems, however, are gaining ground with a 9.38% forecast CAGR thanks to muco-adhesive films that avoid first-pass metabolism and reach peak plasma levels within minutes.

The inhalation route benefits from sustainability mandates, while transdermal patches ride patient demand for painless options. Nasal administration promises direct brain delivery for neurological disorders, a white-space opportunity within the United Kingdom drug delivery devices market that could reshape therapy for Alzheimer's and Parkinson's. Ocular implants are moving from monthly injections to semestral inserts, easing clinic workload and improving adherence.

United Kingdom Drug Delivery Devices Market Report is Segmented by Device Type (Injectable Delivery Devices, Inhalation Delivery Devices, Infusion Pumps, and More), Route of Administration (Injectable, Inhalational, Transdermal, and More), Application (Diabetes, Respiratory Diseases, Oncology, and More), and End User (Hospitals, Ambulatory Surgical Centers, and More). The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Pfizer

- AstraZeneca

- GlaxoSmithKline

- Novartis

- Roche

- Solventum

- Beckton Dickinson

- Baxter

- Ypsomed

- Nemera

- Gerresheimer

- AptarGroup Inc.

- Owen Mumford

- Teva Pharmaceutical Industries

- West Pharmaceutical Services

- SHL Medical

- ICU Medical

- Terumo

- Insulet

- Tandem Diabetes Care

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Initiatives and Trends for Self-Administration & Homecare

- 4.2.2 Development and Adoption Smart Connected Drug Delivery Devices

- 4.2.3 Increasing Research and Development Initiatives and Support from Government

- 4.2.4 Biologics Pipeline Growth Driving Advanced Injectors Demand

- 4.2.5 Rising Prevalence and Incidence of Chronic and Infectious Diseases

- 4.2.6 Fast-Track Approvals for Combination Products Post-Brexit

- 4.3 Market Restraints

- 4.3.1 Post Brexit Challenges Related to Delays and Cost

- 4.3.2 High Development and Manufacturing Cost Coupled with Limited Domestic Clean-Room Manufacturing Capacity

- 4.3.3 Risk and Concerns Associatied with Different Devices

- 4.3.4 NHS Pricing and Rebate Pressure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Injectable Delivery Devices

- 5.1.2 Inhalation Delivery Devices

- 5.1.3 Infusion Pumps

- 5.1.4 Transdermal Patches

- 5.1.5 Implantable Drug Delivery Systems

- 5.1.6 Ocular Inserts & Delivery Implants

- 5.1.7 Nasal & Buccal Delivery Devices

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Inhalation

- 5.2.3 Transdermal

- 5.2.4 Oral Mucosal (Buccal & Sublingual)

- 5.2.5 Ocular

- 5.2.6 Nasal

- 5.3 By Application

- 5.3.1 Diabetes

- 5.3.2 Respiratory Diseases

- 5.3.3 Oncology

- 5.3.4 Cardiovascular Diseases

- 5.3.5 Infectious Diseases

- 5.3.6 Neurological Disorders

- 5.3.7 Others

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Homecare Settings

- 5.4.4 Speciality Clinics

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Pfizer Inc.

- 6.4.2 AstraZeneca plc

- 6.4.3 GlaxoSmithKline plc

- 6.4.4 Novartis AG

- 6.4.5 F. Hoffmann-La Roche Ltd

- 6.4.6 Solventum

- 6.4.7 Becton, Dickinson and Company

- 6.4.8 Baxter International Inc.

- 6.4.9 Ypsomed AG

- 6.4.10 Nemera

- 6.4.11 Gerresheimer AG

- 6.4.12 AptarGroup Inc.

- 6.4.13 Owen Mumford Ltd.

- 6.4.14 Teva Pharmaceutical Industries Ltd.

- 6.4.15 West Pharmaceutical Services Inc.

- 6.4.16 SHL Medical

- 6.4.17 ICU Medical

- 6.4.18 Terumo Corporation

- 6.4.19 Insulet Corporation

- 6.4.20 Tandem Diabetes Care, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment