|

시장보고서

상품코드

1842419

세포 용해 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cell Lysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

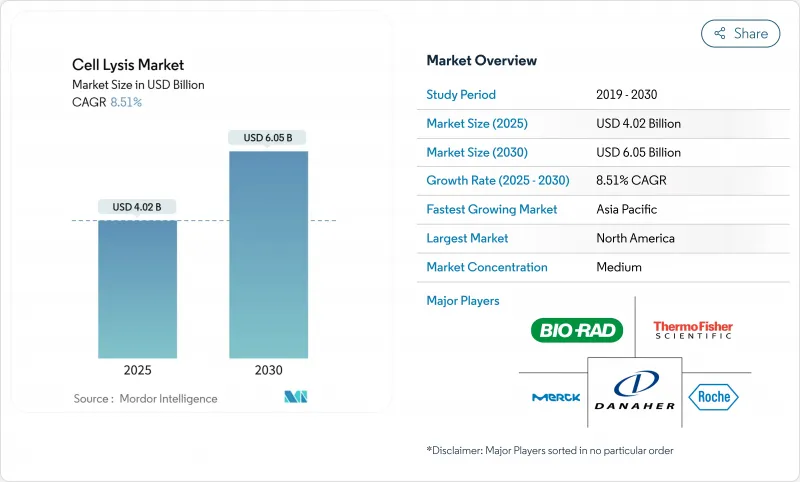

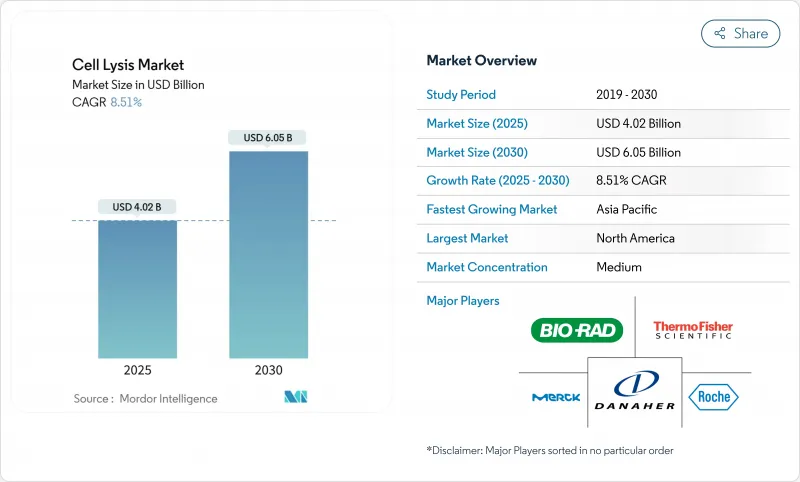

세포 용해 시장은 2025년에 40억 2,000만 달러로 평가되며, 2030년에는 60억 5,000만 달러에 이르고, CAGR 8.51%를 나타낼 것으로 예측됩니다.

단일 세포 오믹스, 연속 바이오프로세스, 자동 샘플 준비 플랫폼에 대한 지속적인 투자는 이러한 성장 궤도를 지원합니다. 온화하면서도 높은 처리량의 용해 프로토콜의 광범위한 채택은 유전자 치료 파이프라인의 확장을 지원하고 확장 가능한 기계 시스템은 포유류 관류 실행에서 제품의 무결성을 보호합니다. 정밀의료 요건과의 긴밀한 협력은 용해 효율성과 재현성이 구매 기준의 핵심을 차지하게 합니다. 기업은 오염 위험을 줄이고 규제 당국에 신청을 가속화하기 위해 폐쇄적이고 자동화된 하드웨어를 선호합니다. 한편, 세포 독성 세제의 단계적 폐지를 요구하는 환경 규제에 의해 환경에 배려한 시약이나 유효한 효소 칵테일의 조달에 방향타가 끊어지고 있습니다.

세계의 세포 용해 시장 동향과 인사이트

단일 세포 오믹스 샘플 전처리 수요 급증

단일 세포 시퀀싱과 단백질체학의 급속한 성장으로 인해 용해 요건은 매우 부드럽고 오염을 억제하는 방향으로 재조정됩니다. 첨단 액적 및 마이크로웰 플랫폼은 현재 수천 개의 세포를 병렬로 처리하고 하류 바코딩을 위해 RNA와 단백질 무결성을 유지하는 시약 처방을 요구하고 있습니다. 벤더는 서브마이크로리터의 반응량에 맞게 조정된 효소 완충액과 라이브러리 제조 사이클을 10시간 이하로 단축하는 마이크로플루이딕스 하드웨어로 대응해 왔습니다. 임상 실험실은 현재 최소 침습적 종양 프로파일링에 이러한 키트를 활용하여 대응 가능한 세포 용해 시장을 확대하고 있습니다. 시약 화학과 소모품 설계 간의 지속적인 피드백은 프로토콜 표준화를 가속화하여 다기관에서 재현성과 규제 신뢰성을 향상시킵니다.

생물 제제 및 바이오시밀러 파이프라인 확대

블록버스터 항체의 특허실효는 고세포 밀도의 포유류 배양을 처리할 수 있는 대용량으로 확장 가능한 용해 하드웨어 수요를 높이는 제조 증강의 방아쇠가 되고 있습니다. 아시아태평양 시설은 470만L 이상의 스테인레스 스틸 및 단일 사용 생산 능력을 보유하고 있으며 견고한 균질화기 및 마이크로플루이다이저에 대한 지역 견인력을 강화하고 있습니다. 바이오시밀러의 규제경로는 세포내 산물의 유효하고 일관된 방출이 요구되기 때문에 생산자는 실시간 모니터링을 통합한 폐쇄형의 자동용해 스키드를 채용하는 경향이 있습니다. 연속 관류가 1g/L/일을 초과하는 역가를 달성함에 따라, 온화한 용해는 글리코실화 패턴을 유지하고 응집을 최소화하기 위해 필수적입니다. 시약 공급업체는 장기 구매를 가능하게 하는 다중 로트 자격 증명 프로그램에서 이익을 얻을 수 있습니다.

엄격한 바이오프로세스 밸리데이션 및 QA/QC 프로토콜

FDA가 실시간 릴리즈 시험을 중시하게 됨에 따라 제조업체는 규모와 환경 변수에서의 용해의 일관성을 증명해야 하며, 개발 기간이 장기화되고 제품 비용이 상승합니다. 첨단 치료 개발 기업은 바이러스 무결성, 불순물 클리어런스 및 잔류 세제 프로파일을 문서화해야 하며, 종종 여러 해에 걸쳐 비교 시험이 필요합니다. 전임 품질 관리 팀이 없는 중소기업은 엄격한 장벽에 직면하고 있으며, 구매자는 광범위한 밸리데이션 자료와 과거 실적 데이터가 있는 플랫폼을 선호하는 경향이 커지고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 하이 스루풋 자동 워크플로우의 보급

- 세포 기반 백신에 대한 자금 조달 증가

- 미세 유체 용해 시스템의 높은 자본 비용

부문 분석

시약은 2024년 매출의 52.35%를 차지했으며 일상적인 워크플로우는 배치마다 소모품에 따라 달라집니다. 오퍼레이터의 개입을 최소화한 24시간 365일 연속 가동을 목표로 하는 스폰서의 움직임에 따라 스마트 균질기나 비드밀 라이저에 대한 수요가 높아지고 있습니다. 초음파 파쇄기는 현재 캐비테이션 강도를 추적하는 센서를 내장하고 있으며, 높은 처리량 운전 중 단백질의 무결성을 보장합니다.

장비의 성장은 또한 바이러스 입자와 인공 세포의 부드러운 파괴를 위해 설계된 microfluidizer에 의해 추진되고 있습니다. 단일 사용 흐름 경로를 제공하는 공급업체는 교차 오염 위험을 줄이고 세척 검증을 간소화하며 카트리지 판매로 장기 경상 수익을 창출합니다. 시약 측면에서 식물 세포와 조류 세포에 맞게 조정된 효소 칵테일이 인기를 끌고 있으며, 친환경 세제는 Triton X-100의 한계를 충족합니다. 완전한 용해 키트는 버퍼, 억제제 및 프로토콜을 통합하여 소규모 실험실이 자체 방법을 개발하지 않고 규제 기대에 부응할 수 있도록 합니다.

포유류 세포는 2024년 수요의 45.53%를 차지하며, 단일클론항체 및 재조합 단백질 생산에 있어서 중심적인 역할을 반영했습니다. 포유류 배양의 세포 용해 시장 규모는 강화된 관류 생물반응기에 의해 세포 밀도가 상승하고 견고하면서도 부드러운 파쇄가 필요하기 때문에 꾸준히 확대될 것으로 예측됩니다. 그러나 바이러스 입자는 유전자 및 세포 치료에서 아데노 관련 바이러스(AAV) 및 렌티바이러스 벡터 프로그램에 힘입어 CAGR 16.85%를 나타내 가장 빠르게 성장하고 있습니다.

바이러스 특이적 용해 프로토콜은 효소 분해와 저전단 마이크로플루이딕스 공학을 결합하여 하류에서 높은 감염 역가를 얻기 위한 필수 조건인 캡시드의 무결성을 유지합니다. 미생물 세포는 효소와 산업용 대사산물을 지속적으로 공급하고 비드 비팅과 고압 균질화에 대한 수요를 지원합니다. 식물 세포는 분자 농법에 대한 노력으로 당단백질의 품질을 유지하면서 견고한 세포벽을 파괴하는 독특한 효소에 틈새 길을 열고 있습니다.

지역별 분석

북미는 2024년에 38.82%의 매출을 획득했으며, 깊은 바이오의약품 제조거점, 대규모 NIH와 BARDA의 자금, 검증된 자동화에 보상하는 FDA의 틀에 의해 지원되고 있습니다. 대규모 멀티 사이트 제조업체는 용해 프로토콜을 원료 및 제제 시설간에 조화시키는 전사적인 사양을 도입하고 있습니다. 미국은 지속적으로 첨단 치료제의 신약 승인을 주도하고 있으며 GMP 등급 키트의 국내 수요를 강화하고 있습니다.

아시아태평양은 정부의 적극적인 장려책과 CDMO 활동의 활성화에 의해 CAGR 11.52%를 나타낼 것으로 예측됩니다. 중국은 2025년을 향해 41억 7,000만 달러의 바이오제조 공약을 내걸고 있으며, 모노클로날 요법이나 유전자 치료 프로그램용 폐쇄형 자동 용해 모듈을 지정하는 여러 산업 단지를 정비하고 있습니다. 인도는 미국 바이오시큐어법(BioSecure Act)에 따른 정책과 국내 풍부한 인재 풀로부터 혜택을 받아 대체 공급망의 허브로 확대하고 있습니다. 지역 생산자는 수출 급료의 질을 목표로, 종합적인 유효성 검사 포장을 가진 체계 수요를 증가하고 있습니다.

유럽은 여전히 매우 중요한 시장이며 어려운 환경 정책이 구매 결정을 형성하고 있습니다. Triton X-100의 사용 금지는 생분해성 세제로의 급속한 이행을 강요시키게 하고, 재빨리 진입한 공급자를 우위에 세우게 합니다. 제조업체는 대체 계면 활성제를 인증하고 마스터 배치 기록을 업데이트하여 대응합니다. 이 과정은 시약 판매를 촉진하지만 인증이 완료 될 때까지 새로운 장비의 조달을 지연시킵니다. 북유럽은 순환형 경제 원칙에 중점을 두고 있으며, 에너지 효율이 높은 초음파 장치의 채용을 장려하고 있습니다.

남미와 중동 및 아프리카는 전체적으로 점유율은 작지만 분산형 진단 키트와 현지 백신 충전 마무리 공장에 대한 관심이 높아지고 있습니다. 브라질의 공공 백신 연구소는 저전단 바이러스 용해 기술에 자본을 배분하고, 걸프 지역의 프리존은 바이오프로세스 장비의 수입을 대상으로 하는 세제 우대 조치로 CDMO를 유치하고 있습니다. 그러나 인프라의 제약은 고비용 마이크로플루이딕스 장비의 단기적인 보급을 억제하고, 수요는 유연한 자금 조달이 가능한 입증된 기계식 시스템으로 향하고 있습니다.

기타 혜택 :

- 엑세포 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 싱글세포 오믹스 샘플 전처리 수요의 급증

- 생물제제와 바이오시밀러의 파이프라인 확대

- 하이 스루풋 자동 워크플로우의 보급

- 세포 기반 백신에 대한 자금 제공 증가

- 식물분자 농업 플랫폼 채용

- 부드러운 용해가 필요한 CRISPR 기반 합성 생물학 툴킷

- 시장 성장 억제요인

- 엄격한 바이오프로세스의 검증과 QA/QC 프로토콜

- 미세 유체 용해 시스템의 높은 자본 비용

- 세포 독성 세제의 폐기와 ESG의 압력

- 포유류 세포 강화를 위한 스케일업의 비효율성

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측(금액, 달러)

- 제품 유형별

- 기기

- 균질기

- 비드밀 리저

- 초음파 분쇄기

- 마이크로플루이디저

- 원심분리기

- 시약

- 세제 키트

- 효소 및 뉴클레아제

- 화학 완충액

- 완전 용해 키트

- 기기

- 세포 유형별

- 포유류 세포

- 미생물 세포

- 식물 세포

- 바이러스 입자

- 기타

- 용해 기술별

- 기계적(물리적)

- 화학적/세제

- 효소적

- 삼투압 충격

- 용도별

- 단백질 정제 및 프로테오믹스

- 핵산 추출 및 게노믹스

- 세포 기반 백신

- 신약 개발 및 스크리닝

- 진단

- 최종 사용자별

- 바이오테크놀러지 및 바이오제약 기업

- 계약 연구 및 제조 기관(CRO/CMO)

- 학술 및 연구 기관

- 임상 진단 센터

- 기타

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- Merck KGaA

- Becton, Dickinson & Company

- Bio-Rad Laboratories Inc.

- Eppendorf AG

- F. Hoffmann-La Roche Ltd

- Takara Bio Inc.

- QIAGEN NV

- Miltenyi Biotec

- Qsonica LLC

- Claremont BioSolutions LLC

- Microfluidics International Corp.

- Labfreez Instruments Group Co.

- Cell Signaling Technology Inc.

- PerkinElmer(Revvity)

- Agilent Technologies Inc.

- Promega Corporation

- New England Biolabs

- Sigma-Aldrich(SAFC)

- Illumina Inc.

- Sartorius AG

제7장 시장 기회와 전망

KTH 25.10.28The cell lysis market is valued at USD 4.02 billion in 2025 and is forecast to reach USD 6.05 billion by 2030, advancing at an 8.51% CAGR.

Sustained investment in single-cell omics, continuous bioprocessing, and automated sample-prep platforms anchors this growth trajectory. Broad adoption of gentle yet high-throughput lysis protocols supports expanding gene-therapy pipelines, while scalable mechanical systems protect product integrity in mammalian perfusion runs. Tight alignment with precision-medicine requirements has elevated lysis efficiency and reproducibility to core purchasing criteria. Companies are prioritizing closed, automated hardware to reduce contamination risk and accelerate regulatory filings. Meanwhile, environmental mandates that phase out cytotoxic detergents are steering procurement toward eco-compliant reagents and validated enzyme cocktails.

Global Cell Lysis Market Trends and Insights

Surge in Single-Cell Omics Sample-Prep Demand

Rapid growth in single-cell sequencing and proteomics has recalibrated lysis requirements toward extreme gentleness and contamination control. Advanced droplet and microwell platforms now process thousands of cells in parallel, demanding reagent formulations that preserve RNA and protein integrity for downstream barcoding. Vendors have responded with enzyme buffers tuned for sub-microliter reaction volumes and microfluidic hardware that shortens library-prep cycles to under 10 hours. Clinical labs now leverage these kits for minimal-invasive tumor profiling, expanding the addressable cell lysis market. Continuous feedback between reagent chemistry and consumable design accelerates protocol standardization, driving multi-site reproducibility and regulatory confidence.

Expanding Biologics & Biosimilars Pipeline

Patent expiries on blockbuster antibodies have triggered a manufacturing build-out that raises demand for large-volume, scalable lysis hardware capable of processing high-cell-density mammalian cultures. Asia-Pacific facilities contribute more than 4.7 million L of stainless and single-use capacity, reinforcing regional pull for robust homogenizers and microfluidizers. Regulatory pathways for biosimilars require validated, consistent release of intracellular product, incentivizing producers to adopt closed, automated lysis skids that integrate real-time monitoring. As continuous perfusion achieves titers above 1 g/L/day, gentle lysis becomes essential for maintaining glycosylation patterns and minimizing aggregation. Reagent suppliers benefit from multi-lot qualification programs that lock in long-term purchasing.

Stringent Bioprocess Validation & QA/QC Protocols

Increased FDA emphasis on real-time release tests forces manufacturers to prove lysis consistency across scales and environmental variables, lengthening development timelines and raising cost of goods. Advanced therapy developers must document viral integrity, impurity clearance, and residual-detergent profiles, often requiring multi-year comparability studies. Smaller firms without dedicated quality teams face steep barriers, reinforcing buyer preference for platforms with extensive validation dossiers and historical performance data.

Other drivers and restraints analyzed in the detailed report include:

- Uptake of High-Throughput Automated Workflows

- Growing Funding for Cell-Based Vaccines

- High Capital Cost of Microfluidic Lysis Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents produced 52.35% of 2024 revenue as routine workflows rely on consumables for every batch, yet instruments are set to outpace with a 12.25% CAGR through 2030, underscoring their strategic importance to automated bioprocessing. Demand for smart homogenizers and bead-mill lysers is climbing as sponsors move toward 24/7 continuous operations that require minimal operator intervention. Ultrasonic disruptors now include embedded sensors that track cavitation intensity, ensuring protein integrity during high-throughput runs.

Instrument growth is also propelled by microfluidizers designed for gentle disruption of viral particles and engineered cells. Suppliers offering single-use flow-paths mitigate cross-contamination risks and streamline cleaning validation, creating long-term recurring revenue from cartridge sales. On the reagent side, enzyme cocktails tailored for plant or algal cells are gaining traction, while eco-friendly detergent replacements address Triton X-100 restrictions. Complete lysis kits integrate buffers, inhibitors, and protocols, enabling small labs to meet regulatory expectations without in-house method development.

Mammalian cells maintained 45.53% of 2024 demand, reflecting their centrality in monoclonal antibody and recombinant protein production. The cell lysis market size for mammalian cultures is projected to expand steadily as intensified perfusion bioreactors raise cell densities that require robust yet gentle disruption. Viral particles, however, represent the fastest-growing opportunity at a 16.85% CAGR, fueled by adeno-associated virus (AAV) and lentiviral vector programs in gene and cell therapy.

Viral-specific lysis protocols combine enzymatic digestion and low-shear microfluidics to preserve capsid integrity, a prerequisite for high infectious titers downstream. Microbial cells continue to supply enzymes and industrial metabolites, sustaining solid demand for bead-beating and high-pressure homogenization. Plant cells, driven by molecular-farming initiatives, open niche avenues for proprietary enzymes that break robust cell walls while maintaining glycoprotein quality.

The Cell Lysis Market is Segmented by Product Type (Instruments [Homogenizers, and More], and Reagents), Cell Type (Mammalian Cells, Microbial Cells, and More), Lysis Technique (Mechanical, Enzymatic, and More), Application (Protein Purification & Proteomics, and More), End User (Biotechnology & Biopharma Firms, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 38.82% revenue in 2024, supported by a deep biopharmaceutical manufacturing base, significant NIH and BARDA funding, and an FDA framework that rewards validated automation. Large multi-site manufacturers deploy enterprise-wide specifications that harmonize lysis protocols across drug-substance and drug-product facilities. The United States continues to lead new-drug approvals in advanced therapies, reinforcing domestic demand for GMP-grade kits.

Asia-Pacific is forecast to achieve an 11.52% CAGR, driven by aggressive government incentives and rising CDMO activity. China's USD 4.17 billion biomanufacturing commitment for 2025 anchors multiple industrial parks that specify closed, automated lysis modules for monoclonal and gene-therapy programs. India expands as an alternative supply-chain hub, benefiting from policy alignment with the US BioSecure Act and large domestic talent pools. Regional producers target export-grade quality, elevating demand for systems with comprehensive validation packages.

Europe remains a pivotal market where stringent environmental policies shape purchasing decisions. The ban on Triton X-100 forces rapid transition to biodegradable detergents, placing early-mover suppliers at an advantage. Manufacturers adapt by certifying alternative surfactants and updating master batch records, a process that drives reagent sales but slows new-equipment procurement until qualification completes. Northern Europe's focus on circular economy principles encourages adoption of energy-efficient ultrasonic devices.

South America and the Middle East & Africa collectively represent smaller shares but register rising interest in decentralized diagnostic kits and local vaccine fill-finish plants. Brazil's public vaccine institutes allocate capital toward low-shear viral-lysis technology, while Gulf region free zones court CDMOs with tax incentives covering bioprocess equipment importation. Infrastructure constraints, however, temper near-term uptake of high-cost microfluidic instruments, aligning demand toward proven mechanical systems with flexible financing.

- Thermo Fisher Scientific

- Danaher

- Merck

- Beckton Dickinson

- Bio-Rad Laboratories

- Eppendorf

- Roche

- Takara Bio

- QIAGEN

- Miltenyi Biotec

- Qsonica

- Claremont BioSolutions

- Microfluidics International Corp.

- Labfreez Instruments Group Co.

- Cell Signaling Technology

- PerkinElmer (Revvity)

- Agilent Technologies

- Promega

- New England Biolabs

- Sigma-Aldrich (SAFC)

- Illumina

- Sartorius

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge In Single-Cell Omics Sample-Prep Demand

- 4.2.2 Expanding Biologics & Biosimilars Pipeline

- 4.2.3 Uptake Of High-Throughput Automated Workflows

- 4.2.4 Growing Funding For Cell-Based Vaccines

- 4.2.5 Adoption Of Plant Molecular Farming Platforms

- 4.2.6 CRISPR-Based Synthetic Biology Toolkits Requiring Gentle Lysis

- 4.3 Market Restraints

- 4.3.1 Stringent Bioprocess Validation & QA/QC Protocols

- 4.3.2 High Capital Cost Of Microfluidic Lysis Systems

- 4.3.3 Cytotoxic Detergent Disposal & ESG Pressures

- 4.3.4 Scale-Up Inefficiencies For Mammalian-Cell Intensification

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.1.1 Homogenizers

- 5.1.1.2 Bead-mill Lyser

- 5.1.1.3 Ultrasonic Disruptors

- 5.1.1.4 Microfluidizers

- 5.1.1.5 Centrifuges

- 5.1.2 Reagents

- 5.1.2.1 Detergent Kits

- 5.1.2.2 Enzymes & Nucleases

- 5.1.2.3 Chemical Buffers

- 5.1.2.4 Complete Lysis Kits

- 5.1.1 Instruments

- 5.2 By Cell Type

- 5.2.1 Mammalian Cells

- 5.2.2 Microbial Cells

- 5.2.3 Plant Cells

- 5.2.4 Viral Particles

- 5.2.5 Others

- 5.3 By Lysis Technique

- 5.3.1 Mechanical (Physical)

- 5.3.2 Chemical / Detergent

- 5.3.3 Enzymatic

- 5.3.4 Osmotic Shock

- 5.4 By Application

- 5.4.1 Protein Purification & Proteomics

- 5.4.2 Nucleic-Acid Extraction & Genomics

- 5.4.3 Cell-Based Vaccines

- 5.4.4 Drug Discovery & Screening

- 5.4.5 Diagnostics

- 5.5 By End User

- 5.5.1 Biotechnology & Biopharma Firms

- 5.5.2 Contract Research & Manufacturing Organizations (CRO/CMO)

- 5.5.3 Academic & Research Labs

- 5.5.4 Clinical Diagnostics Centers

- 5.5.5 Others

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Danaher Corporation

- 6.3.3 Merck KGaA

- 6.3.4 Becton, Dickinson & Company

- 6.3.5 Bio-Rad Laboratories Inc.

- 6.3.6 Eppendorf AG

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 Takara Bio Inc.

- 6.3.9 QIAGEN NV

- 6.3.10 Miltenyi Biotec

- 6.3.11 Qsonica LLC

- 6.3.12 Claremont BioSolutions LLC

- 6.3.13 Microfluidics International Corp.

- 6.3.14 Labfreez Instruments Group Co.

- 6.3.15 Cell Signaling Technology Inc.

- 6.3.16 PerkinElmer (Revvity)

- 6.3.17 Agilent Technologies Inc.

- 6.3.18 Promega Corporation

- 6.3.19 New England Biolabs

- 6.3.20 Sigma-Aldrich (SAFC)

- 6.3.21 Illumina Inc.

- 6.3.22 Sartorius AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment