|

시장보고서

상품코드

1842422

수익 주기 관리 : 시장 점유율 분석, 업계 동향과 통계, 수익 예측(2025-2030년)Revenue Cycle Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

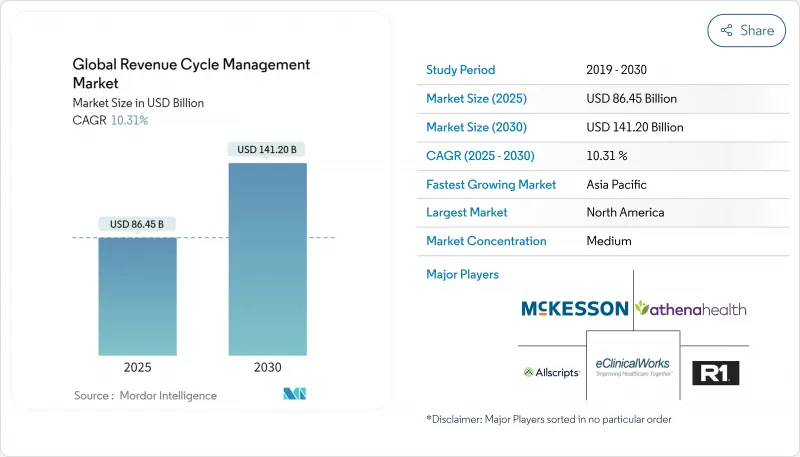

수익 주기 관리 시장의 2025년 시장 규모는 864억 5,000만 달러에 달하고, CAGR 10.31%를 나타내 2030년에는 1,412억 달러에 이를 전망입니다.

관리 오버헤드 확대, 가치 기반 상환에 축족, AI 채택 확대가 결합되어 자동화된 수익 획득이 이사회 수준에서 필요합니다. 의료기관은 임상 문서화, 부인 회피, 현금 흐름 분석을 하나의 작업 공간으로 통합하고, 수작업을 줄이고, 매출 금액을 단축하는 통합 플랫폼을 선호합니다. 북미의 의료 시스템이 계속 수요를 지지하고 있지만, 아시아태평양에서는 민간 보험이 침투하고 있어 새로운 대응 가능 볼륨이 확대되고 있습니다. 인적 부족으로 인해 서비스 아웃소싱은 여전히 널리 보급되고 있지만 클라우드 소프트웨어의 급속한 가속화는 노동 집약형 모델에서 환자 수에 따라 규모를 확장하는 구독 기반 아키텍처로의 단계적 전환을 시사합니다. 그 결과 예측 분석과 컴플라이언스 업데이트를 단일 상호 운용 가능한 스택으로 결합할 수 있는 기술 공급업체 간의 경쟁이 치열해지고 있습니다.

세계의 수익 주기 관리 시장 동향과 인사이트

가치 기반 및 성과 연동형 상환으로의 세계적 변화

밸류 베이스 케어는 현재 주요 지급자와의 계약에 포함되어 있으며, 서비스량보다 임상 질에 지불을 연결함으로써 수익 주기 관리 업계의 우선순위를 재구성하고 있습니다. 어카운터블 케어의 틀을 채용한 의료 시스템은 총액으로 7억 달러를 넘는 절약을 기록해, 조직이 품질 지표를 습득하면 재무적인 상적이 존재하는 것을 증명하고 있습니다. 이에 대응하기 위해, RCM 플랫폼은 임상 결과를 상환 트리거로 변환하는 집단 건강 대시보드를 통합하여 제공업체가 지불 위험이 현저해지기 전에 관리 갭을 추적할 수 있도록 합니다. 이 진화는 이종 소스로부터 정규화된 데이터를 암시적으로 요구하고 상호 운용성에 새로운 상업적 긴급성을 부여합니다.

RCM 자동화를 촉진하는 관리비 압력 증가

미국의 헬스케어 지출에 차지하는 관리비의 비율은 20-25%이기 때문에 경영 간부는 자동화를 비용 상승을 막는 효과적인 수단이라고 생각하고 있습니다. AI를 탑재한 봇은 이전에는 수작업으로 확인해, 스태프가 며칠에 걸쳐 후속할 필요가 있던 루틴의 사전 승인 트랜잭션을 몇 초로 완료시키고, 일부 병원에서는 도입 후에 청구서 작성 시간이 50% 단축된 것을 기록하고 있습니다. 이러한 개선으로 청구 담당자는 복잡한 예외 처리에 전념할 수 있게 되었고, 예정외의 생산성 향상으로 경영진은 환자 대응 업무에 전념할 수 있게 되었습니다. 중요한 것은 입원에서 회계까지의 워크플로우를 자동화한 의료기관에서는 지루하고 실수가 발생하기 쉬운 데이터 입력 작업이 없어져 직원 만족도가 높아졌습니다고 보고되고 있다는 것입니다.

이질적이고 변화하는 지급자의 규칙과 코딩 기준

부인률은 10-15% 정도로 추이하고 있어 지불 측의 편집이나 정책의 갱신이 얼마나 신속한가 하는 것을 이야기하고 있습니다. 의료그룹의 리더는 2024년 부인율이 더욱 상승한 것을 확인했으며, 조직은 지속적인 코드 갱신과 제출 전에 부인 가능성에 신고하는 예측 스크러버에 투자하고 있습니다. 첨단 의료 시스템은 부인의 근본 원인을 조사하는 전문 팀을 배치하고 코더와 임상의 사이의 반복적인 피드백 루프가 수정주기를 단축하고 있습니다. 지불인으로부터의 송금으로부터 자기 학습하는 AI 주도의 룰 엔진은 현재, 첨부 파일 요구의 측정 가능한 삭감을 실현해, 관리 오버헤드를 삭감하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 가속하는 디지털 헬스와 상호 운용성의 세계적인 의무화

- 헬스케어의 소비자화, 증가하는 환자 청구의 복잡성

- 숙련된 코딩과 RCM 인재의 지속적인 부족

부문 분석

2024년 수익 주기 관리 시장 규모의 78%는 서비스가 차지했는데, 이는 인력 부족 가운데 공급자가 턴키 전문 지식을 선호하고 있음을 반영한 것입니다. 서비스 파트너가 기술 투자와 지속적인 프로세스 개선을 책임지기 때문에 고객은 아웃소싱을 회수율 향상에 즉각적인 수단으로 간주합니다. 그럼에도 불구하고 클라우드 기반 소프트웨어는 2030년까지 연평균 복합 성장률(CAGR)이 14.2%를 나타내 시장 전체의 성장률을 상회하고 있습니다. 이는 구독 가격으로 비용과 사용 상황이 일치하고 대규모 자본 투자 장애물이 없기 때문입니다.

클라우드 RCM 스위트를 도입한 병원에서는 의사의 문서 갭을 실시간으로 대시보드에 표시하고, 한 번의 변화 내에서 수정 지도를 가능하게 하는 등, 부차적인 장점을 발견하는 경우가 많습니다. 시간이 지남에 따라 이러한 분석 기능은 원내 팀이 거래 업무에서 전략적 수준 무결성 역할로 전환하도록 촉구합니다. 이러한 두 가지 성장 패턴을 통해 사내 감독과 선택적 아웃소싱을 결합한 하이브리드 운영 모델이 널리 보급되고 소프트웨어 회사와 서비스 뷰로 모두 수익 주기 관리 업계의 비즈니스 기회가 확대될 것으로 예측됩니다.

2024년 수익 주기 관리 시장 점유율은 On-Premise형이 58.5%를 차지했습니다. 그러나 클라우드 배포는 유연한 인프라, 자동 업그레이드 및 지불자 API와의 간편한 통합으로 2030년까지 연평균 복합 성장률(CAGR) 14.2%를 나타낼 전망입니다. HFMA의 기술 도입 곡선을 높이는 조직은 사이클 타임 지표가 하강 경향으로 변하는 변곡점으로 클라우드 마이그레이션을 자주 들고 있습니다. 클라우드 벤더는 클라이언트의 IT 팀에 의존하지 않고 중앙에서 업데이트를 푸시하므로 규제 코드 세트를 더욱 신속하게 구현할 수 있습니다.

사이버 보안 프레임워크가 성숙함에 따라 오프사이트 호스팅에 대한 이사 수준의 저항은 사라지고 있으며, CFO는 예측 가능한 구독 수수료로 인해 다년간의 예산 구성이 간소화된다는 점에 주목하고 있습니다. 이러한 비용의 투명성은 수익 주기 관리 시장 전체의 성장을 가속화하는 숨겨진 요소입니다. 예전에는 대규모 학술센터 밖에 제공되지 않았던 기능을 중견병원에서도 이용할 수 있게 되었기 때문입니다.

지역별 분석

북미는 현재 수익 주기 관리 시장 규모의 48%를 차지하며 복잡한 다중 지불 보험 회사의 틀과 EHR 도입의 오랜 역사에 힘입어 있습니다. 공급업체의 통합은 활발했고 R1 RCM의 89억 달러 거래는 규모가 큰 프로세스의 전문성이 현금 흐름을 크게 향상시킬 수 있는 개인 자금의 확신을 보여주었습니다. 미국 병원에서는 46%가 이미 수익 주기 워크플로우에 어떤 형태로 AI를 활용하고 있다고 보고했습니다. 흥미롭게도 캐나다의 단일 지불 시스템은 주간 조정을 위해 RCM 도구가 여전히 필요하고 지불자의 복잡성만이 성장의 원동력이 아니라는 것을 보여줍니다. 이 지역의 진료 보상의 투명성은 풍부한 데이터 세트를 창출하고 공급업체가 다른 지역보다 빨리 머신러닝 모델을 개선할 수 있게 하여 북미의 리더십을 강화하고 있습니다.

아시아태평양의 2030년까지 연평균 복합 성장률(CAGR)은 16.4%를 나타내 수익 주기 관리 업계에서 가장 빠른 속도로 성장할 것으로 예측되며, 이는 정부가 지원하는 디지털 헬스 투자와 민간 보험에 대한 중간층 수요 증가에 힘쓰고 있습니다. 인도에서는 국민보험 확대로 청구 인프라가 표준화되고 조기에 청구를 디지털화한 병원은 결제 시간을 단축할 수 있습니다. 중국의 3급 도시에 있는 병원에서는 구형 클라이언트 서버 모델에서 도약하기 위해 클라우드 RCM을 요구하는 경향이 강해지고 있으며, 이는 다른 업계에서 볼 수 있는 스마트폰의 보급 곡선을 반영하고 있습니다. 데이터 현지화에 관한 법률이 호스팅 아키텍처를 형성하는 일본과 같은 시장에서 규제 당국의 승인을 얻으려면 현지 파트너가 필수적입니다. 이러한 상황 적응의 필요성은 세계 벤더에 있어서는 진입 장벽이 되지만, 동시에 선행자로서의 지위를 확보한 기업에 있어서는 높은 리턴이 됩니다.

유럽에서는 많은 국가가 청구 기준을 중앙 집중화하는 단일 지불 모델을 채택하고 있기 때문에 성장은 안정적이며 수익 주기 관리 시장 점유율은 여전히 높습니다. 그럼에도 불구하고 GDPR(EU 개인정보보호규정)의 요구사항은 병원을 엄격한 암호화 및 감사 추적이 있는 클라우드 환경으로 향하게 하고, 프라이버시 엔지니어링 경험이 풍부한 미국 및 유럽 소프트웨어 기업의 합작 투자에 박차를 가하고 있습니다. 영국에서는 국민보건서비스가 백로그 삭감에 다시 주력하고 있기 때문에 민간 RCM과 유사한 AI 스케줄링과 청구처리 기능에 대한 관심이 높아지고 있습니다. 한편, 중동 및 아프리카, 남미에서는 민간 병원 체인이 초기 수요를 견인하고 있어 규제 프레임워크이 성숙하면 도입이 가속하는 기반이 갖추어지는 신흥 지역이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 밸류 베이스 & 결과 연동형 진료 보상으로의 세계 변화

- RCM 자동화를 촉진하는 관리 비용 압력 증가

- 가속하는 디지털 헬스와 상호 운용성의 세계의 의무화

- 헬스케어의 소비화에 의한 환자청구의 복잡화

- 클라우드 네이티브의 의료 IT 플랫폼과 SaaS 이코노믹스의 보급

- 시장 성장 억제요인

- 이질적으로 계속 변화하는 지불자의 규칙과 코딩 기준

- 숙련된 코딩과 RCM 인재의 지속적 부족

- 보호된 의료 정보를 다루는 데이터 프라이버시와 사이버 보안의 위험

- 고액의 선행 투자와 변경 관리의 장벽

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌의 격렬함

제5장 시장 규모·성장 예측(금액, 달러)

- 구성 요소별

- 소프트웨어

- 통합 RCM 제품군

- 독립형 모듈

- 서비스

- RCM 아웃소싱 BPO

- 컨설팅 및 트레이닝

- 소프트웨어

- 배포별

- 클라우드 기반

- On-Premise

- 기능별

- 청구 및 거절 관리

- 의료 코딩 및 청구

- 전자 의료 기록(통합 RCM)

- 임상 문서 개선(CDI)

- 보험 자격 확인

- 기타 기능(환자 예약, 가격 투명화)

- 최종 사용자별

- 병원

- 진료소 및 클리닉

- 외래 수술 센터(ASC)

- 검사 센터

- 영상 진단 센터

- 기타 최종 사용자

- 전문 분야별

- 방사선학

- 종양학

- 심장학

- 병리학

- 기타

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Optum(UnitedHealth Group)

- R1 RCM Inc.

- Conifer Health Solutions

- Cognizant(Trizetto)

- athenahealth

- Oracle Cerner

- Epic Systems

- Veradigm LLC

- Solventum

- GeBBS Healthcare

- MCKESSON Corporation

- Accenture Health

- Infosys Limited

- Med-Metrix

- Access Healthcare

- Conduent

- eClinicalWorks

- XIFIN

- Quest Diagnostics RCM

- HCLTech Healthcare

제7장 시장 기회와 전망

KTH 25.10.28The revenue cycle management market is valued at USD 86.45 billion in 2025, is set to expand at a 10.31% CAGR, and should reach USD 141.20 billion by 2030.

Expanding administrative overhead, the pivot toward value-based reimbursement, and widening AI adoption are combining to make automated revenue capture a board-level necessity. Providers are prioritizing integrated platforms that merge clinical documentation, denial avoidance, and cash-flow analytics in one workspace, cutting manual touches and shortening days in accounts receivable. North American health systems continue to anchor demand, yet rising private-insurance penetration in Asia-Pacific is unlocking sizable new addressable volumes. Service outsourcing remains prevalent because staffing gaps persist, but cloud software's rapid acceleration signals a gradual hand-off from labor-heavy models to subscription-based architectures that scale with patient volumes. The net effect is heightened competition among technology vendors that can wrap predictive analytics and compliance updates into a single, interoperable stack.

Global Revenue Cycle Management Market Trends and Insights

Global Shift Toward Value-Based & Outcome-Linked Reimbursement

Value-based care, now written into major payer contracts, is recasting Revenue Cycle Management industry priorities by tying payment to clinical quality rather than service volume. Health systems that adopted accountable care frameworks recorded collective savings in excess of USD 700 million, proving that financial upside exists once organizations master quality metrics. As a response, RCM platforms are integrating population-health dashboards that translate clinical outcomes into reimbursement triggers, ensuring that providers track gaps in care before payment risk materializes. That evolution implicitly demands normalized data from disparate sources, giving interoperability a new commercial urgency.

Escalating Administrative Cost Pressure Prompting RCM Automation

Administrative expenses routinely consume 20 - 25 % of United States healthcare spending, so executives view automation as a proven lever to arrest cost inflation. AI-enabled bots now complete routine prior authorization transactions in seconds, a process that previously required manual review and days of staff follow-up, and some hospitals have documented a 50 % reduction in claim preparation time after deployment. These improvements free billing professionals to concentrate on complex exceptions, generating an unplanned productivity dividend that management can redeploy toward patient-facing roles. Importantly, institutions that automate admit-through-cash workflows report heightened staff satisfaction because tedious, error-prone data entry tasks disappear.

Heterogeneous, Ever-Changing Payer Rules and Coding Standards

Denial rates hovering around 10 - 15 % illustrate how quickly payer edits and policy updates can overturn otherwise compliant claims. Medical group leaders confirm that denials climbed further in 2024, so organizations are investing in continuous code updates and predictive scrubbers that flag likely rejections before submission. Forward-looking health systems allocate dedicated teams to mine denial root causes, and iterative feedback loops between coders and clinicians are shortening correction cycles. AI-driven rules engines that self-learn from payer remittances now deliver measurable reductions in attachment requests, cutting administrative overhead.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Digital-Health & Interoperability Mandates Worldwide

- Consumerization of Healthcare Increasing Patient Billing Complexity

- Persistent Shortage of Skilled Coding and RCM Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services hold 78% market share of the Revenue Cycle Management market size in 2024, mirroring providers' preference for turnkey expertise amid staffing shortages. Clients view outsourcing as an immediate route to improved collections because service partners assume responsibility for technology investment and continuous process refinement. Nevertheless, cloud-based software is posting a 14.2% CAGR through 2030, more than the overall market growth, because subscription pricing aligns cost with usage and removes large capital hurdles.

Hospitals that implement cloud RCM suites often discover secondary benefits, such as real-time dashboards that spotlight physician documentation gaps, enabling corrective coaching within a single shift. Over time, these analytics capabilities encourage in-house teams to transition from transactional tasks to strategic revenue integrity roles. The dual-track growth pattern implies that hybrid operating models, combining retained oversight with selective outsourcing-will become common, broadening the Revenue Cycle Management industry opportunity for both software firms and service bureaus.

On-premise deployments retain 58.5% Revenue Cycle Management market share in 2024, reflecting earlier capital purchases and residual security concerns. Yet cloud installations are expanding at a 14.2% CAGR to 2030, propelled by flexible infrastructure, automatic upgrades, and easier integration with payer APIs. Organizations that climb the HFMA technology-adoption curve frequently cite cloud moves as the inflection point when cycle-time metrics start to trend downward. One observed benefit is faster implementation of regulatory code sets, since cloud vendors push updates centrally instead of relying on client IT teams.

As cyber-security frameworks mature, board-level resistance to off-site hosting is receding, and CFOs note that predictable subscription fees simplify multi-year budgeting. This cost transparency acts as a hidden accelerant to overall Revenue Cycle Management market size growth because even mid-tier hospitals can now access features that were once reserved for large academic centers.

The Revenue Cycle Management Market is Segments by Component (Software [Integrated RCM Suite, and More], and Services [Outsourced RCM BPO, and More]), Deployment (Cloud-Based and On-Premise), Function (Claims & Denial Management, and More) End User (Hospitals, Laboratories, and More), Specialty (Radiology, Oncology, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commands 48% of the current Revenue Cycle Management market size, supported by complex multi-payer frameworks and a long history of EHR adoption. Vendor consolidation is active, evidenced by R1 RCM's USD 8.9 billion transaction, signaling private-equity conviction that scaled process expertise can deliver outsized cash-flow gains. Hospitals in the United States report that 46% already utilize some form of AI in revenue-cycle workflows. Interestingly, Canadian single-payer structures still require RCM tools for provincial reconciliation, revealing that payer complexity is not the only growth driver. The region's reimbursement transparency mandates create rich data sets, enabling vendors to refine machine-learning models faster than elsewhere, reinforcing North American leadership.

Asia-Pacific is forecast to post a 16.4% CAGR through 2030, the fastest regional pace in the Revenue Cycle Management industry, propelled by government-backed digital-health investments and swelling middle-class demand for private insurance. India's national insurance expansion is catalyzing standardized claims infrastructure, and hospitals that digitize billing early capture accelerated settlement times. China's tier-three city hospitals increasingly seek cloud RCM to leapfrog older client-server models, mirroring the smartphone adoption curve seen in other industries. Local partners remain critical for navigating regulatory approval in markets such as Japan, where data localization laws shape hosting architecture. This need for contextual adaptation presents a barrier to entry for global vendors but simultaneously offers high returns to firms that secure first-mover standing.

Europe retains meaningful Revenue Cycle Management market share, although growth is steadier because many countries operate single-payer models that centralize claim standards. Even so, GDPR requirements push hospitals toward cloud environments with strict encryption and audit trails, spurring joint ventures between U.S. and European software firms experienced in privacy engineering. In the United Kingdom, the National Health Service's renewed focus on backlog reduction has elevated interest in AI scheduling and billing triage features that resemble private-sector RCM. Meanwhile, Middle East, Africa, and South America represent emerging territories where private hospital chains drive early demand, setting a foundation for accelerated adoption once regulatory frameworks mature.

- Optum (UnitedHealth Group)

- R1 RCM

- Conifer Health Solutions

- Cognizant (Trizetto)

- athenahealth

- Oracle

- Epic Systems

- Veradigm

- Solventum

- GeBBS Healthcare

- MCKESSON Corporation

- Accenture Health

- Infosys

- Med-Metrix

- Access Healthcare

- Conduent

- eClinicalWorks

- XIFIN

- Quest Diagnostics RCM

- HCLTech Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global Shift Toward Value-Based & Outcome-Linked Reimbursement

- 4.2.2 Escalating Administrative Cost Pressure Prompting RCM Automation

- 4.2.3 Accelerated Digital-Health & Interoperability Mandates Worldwide

- 4.2.4 Consumerization of Healthcare Increasing Patient Billing Complexity

- 4.2.5 Proliferation of Cloud-Native Health IT Platforms & SaaS Economics

- 4.3 Market Restraints

- 4.3.1 Heterogeneous, Ever-Changing Payer Rules and Coding Standards

- 4.3.2 Persistent Shortage of Skilled Coding & RCM Talent

- 4.3.3 Data-Privacy & Cyber-security Risks Handling Protected Health Info

- 4.3.4 High Up-Front Investment and Change-Management Barriers

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Integrated RCM Suite

- 5.1.1.2 Standalone Modules

- 5.1.2 Services

- 5.1.2.1 Outsourced RCM BPO

- 5.1.2.2 Consulting & Training

- 5.1.1 Software

- 5.2 By Deployment

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.3 By Function

- 5.3.1 Claims & Denial Management

- 5.3.2 Medical Coding & Billing

- 5.3.3 Electronic Health Record (Integrated RCM)

- 5.3.4 Clinical Documentation Improvement (CDI)

- 5.3.5 Insurance Eligibility Verification

- 5.3.6 Other Functions (Patient Scheduling, Pricing Transparency)

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Physician Offices & Clinics

- 5.4.3 Ambulatory Surgery Centers

- 5.4.4 Laboratories

- 5.4.5 Diagnostic Imaging Centers

- 5.4.6 Other End Users

- 5.5 By Specialty

- 5.5.1 Radiology

- 5.5.2 Oncology

- 5.5.3 Cardiology

- 5.5.4 Pathology

- 5.5.5 Multi-specialty & Others

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Optum (UnitedHealth Group)

- 6.3.2 R1 RCM Inc.

- 6.3.3 Conifer Health Solutions

- 6.3.4 Cognizant (Trizetto)

- 6.3.5 athenahealth

- 6.3.6 Oracle Cerner

- 6.3.7 Epic Systems

- 6.3.8 Veradigm LLC

- 6.3.9 Solventum

- 6.3.10 GeBBS Healthcare

- 6.3.11 MCKESSON Corporation

- 6.3.12 Accenture Health

- 6.3.13 Infosys Limited

- 6.3.14 Med-Metrix

- 6.3.15 Access Healthcare

- 6.3.16 Conduent

- 6.3.17 eClinicalWorks

- 6.3.18 XIFIN

- 6.3.19 Quest Diagnostics RCM

- 6.3.20 HCLTech Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment